admin

January 7, 2010

By Tarang Gautam Saxena, Chandni Jain and Neha Singhal

In Retrospect

While India was a promising market to many international brands, it was not completely immune from the global economic flu. More than its primary impact on the economy, the global downturn sobered the mood in the consumer market. Even the core target group for international brands, that had just begun to splurge apparently without guilt, tightened their purse strings and either down-traded or postponed their purchases.

In 2008 in the midst of economic downturn, skepticism and uncertainty, the international fashion brands had continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008 targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many players ended up discounting the goods heavily to promote sales while a few also gave up and closed shop.

As the Third Eyesight team had foreseen last year, 2009 saw a further slowdown and fewer international brands being launched during the year. The brands that were launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack and Timberland. Some of these had already been in the pipeline for quite some time and invested a considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

International Fashion Brands in India

After many deliberations, the well-known global brand Donna Karan New York set foot in the Indian market in 2009 through an agreement with DLF Brands to set up exclusive DKNY and DKNY Jeans stores India. The brand is also reported to have signed a worldwide licensing agreement with S Kumars Nationwide Ltd to design, manufacture and retail DKNY menswear in certain specific countries.

Second Chances

Amongst the international brands that have recently entered the Indian market, a few are on their second or even third attempt at the market.

For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills, and the partnership intended opening 15 stores by 2010. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis on retailing international brands within the country. Within a few months of the ending of this relationship, Diesel signed a joint venture with Reliance Brands for a launch scheduled for 2010. Both partners seem to be strategically aligned with a common goal as the international iconic denim brand wants to take on the Indian market full throttle and the Indian counterpart has indicated that it wants to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008, despite plans to open more than 50 stores in the first three years of operations. Miss Sixty has finally entered India through a franchise agreement with a manufacturer of women’s footwear and accessories. The company has currently introduced only shoes and accessories category and is looking at potential partners for its label Energie and girls’ range Killah.

Other brands that have re-entered the Indian market include Germany-based Lerros whose first presence in India was back in mid-1990s. The brand re-entered the market in 2008 through own brand stores and is growing its presence through this route as well as through multi-brand stores.

Oshkosh B’gosh is another brand that had entered India in mid 1990s, through a licensing agreement with Delhi based buying house, Elanco. The licensee found the childrenswear market hard to crack, and closed down. In 2008, Oshkosh re-entered the Indian market through a licensing partnership with Planet Retail and is now available through shop-in-shop counters at Debenhams stores. Reports suggest that it may consider setting up exclusive brand outlets.

During the turbulence of 2008 and 2009, a few brands also exited the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both) to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations and for the amount of effort and money being invested, and that it was better to pull the plug.

Some brands that have been pulled out of the Indian market during 2008 and 2009 include Dockers, Gas, Springfield and VNC (Vincci). Gas (Grotto SpA) is reported to remain interested in the market but has not found another partner after its deal with Raymond fell through in 2007 and all dozen of its standalone stores were shut down.

The Scottish brand Pringle and its Indian licensee did not renew their agreement upon its expiry. The Indian partner has reportedly signed an agreement to launch another international brand in India, while Pringle is said to be looking for new licensee.

The good news is that successful relationships outnumber every exit or break in relationship possibly by a factor of ten. Some of the brands that have sustained are among the early entrants having a presence in India since the late-1980s and 1990s or even earlier. These include Bata, Benetton, adidas, Reebok (now also owned by adidas), Levi Strauss and Pepe. Having grown very aggressively during 2006 and 2007 Reebok quickly became the largest apparel and footwear brand in India, while Benetton and Levi’s are expected to cross the $100-million mark for sales this year.

Entry Strategy & Recent Shifts

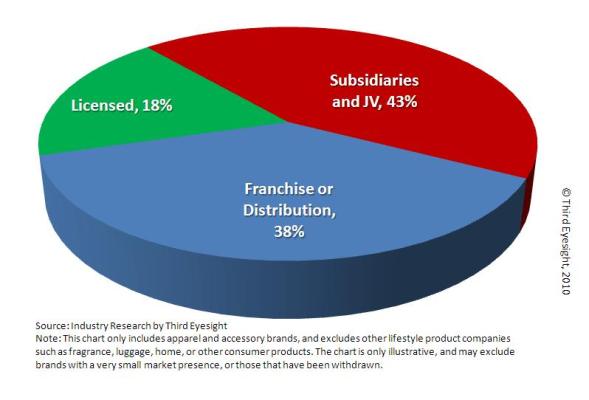

As envisaged in Third Eyesight’s report from a year ago, with changing market conditions and a growing confidence in the Indian market, there has been a shift among international brands in the choice of the launch vehicle. While franchising has been the preferred mode of market entry in the recent past for risk-averse brands, more brands today demonstrate a long-term commitment to the Indian market, and are choosing to exercise ownership through wholly or partially owned subsidiaries and through joint ventures.

In 2009, we have seen a noticeable shift in favour of joint-ventures as the choice for entry into the market. Even the brands already present are looking to modify the nature of their existing presence in India in order to exert more control over the retail operations, products, supply chain and marketing.

Current Operating Structure

(End 2009)

Brands that changed their operating structures and, in some cases partners, in recent years include VF (Wrangler, Lee etc.), Lee Cooper, Lee, and Louis Vuitton amongst others.

Mothercare, the baby product retailer, which is present through a franchise agreement with Shopper’s Stop has, in addition, recently formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores. Gucci, which had initially entered in 2006 with the Murjani Group as a franchisee, has recently changed over to Luxury Goods Retail, and is now in the process of restructuring the relationship into a joint venture.

VF has also been reported to be looking to license Nautica, Jansport and Kipling to a new partner. Until now, these brands were handled through the joint venture with Arvind Brands. Arvind has increasingly focused on its core business, closed stores and scaled down expansion plans for the international brands.

Burberry that had entered India in 2006 through a franchisee arrangement with Media Star opened two stores under this arrangement. It has now set up a new joint venture with Genesis Colors and plans to open 20 stores across the country.

More recently Esprit has also been reported to have approached Aditya Birla Nuvo to deepen its engagement by moving from its distribution arrangement into joint venture as the international brand sees excellent potential in the Indian market.

Buckling up for 2010

Throughout 2009, the one fact that became clear was that the Indian market was resilient. Now, as the global economic condition stabilizes, confidence levels of brands and retailers in India have also improved.

Several launches are already expected in 2010, and possibly many more are being worked upon. In the following 12 months, consumers can expect to find within India acclaimed brands such as Diesel, Topman, Topshop and the much-anticipated Zara. Many more Italian, British and French brands are examining the market.

Most of the international fashion brands already present in the market are also projecting a cautiously upbeat outlook in their plans, while a few are looking positively bullish.

For example, Pepe, an old player in premium and casual wear segment, has reported plans to grow its retail network further and open 50 more franchise stores by September 2010. Similarly the German fashion brand S. Oliver that entered the Indian market in 2007 is looking to grow significantly. It has already moved from a franchise arrangement with Orientcraft to a joint-venture with the same partner, and has stepped up its above-the-line marketing presence. The brand has recently reported its plans to scale up its retail presence to 77 stores by the end of 2012 while also strengthening its presence through shop-in-shop in multi-branded outlets in high potential markets.

Those international brands that have tasted success have not achieved it by blindly importing business models and formulas from other markets. Most have had to devise a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched. These include The Body Shop which decreased its prices by up to 30% this year, and Marks & Spencer which reduced prices by 20-40%. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

On the operational side, the good news for retailers and brands is that the average real estate costs have reduced significantly, although marquee locations remain high. In several locations lease models have also moved from only fixed rent to some form of revenue sharing arrangement with the landlord. And, while the sector has seen some employee turmoil as many non-retail executives who came into the business in the last 5-7 years have returned to other sectors, employee salary expectations are also more realistic.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s recent work with international brands’ business units in India highlights the international players’ concern with ensuring a consistent brand message, improved organizational capabilities right down to front-line staff, and focus on unit productivity (per store and per employee).

We may yet see a few more exits, and possibly some more relationships being reshuffled and partners being changed. However, all things considered, we can look forward to a net increase in the number of international brands in the country.

The Indian consumer is certainly demonstrating more optimism and as far as there are no major unforeseen global or domestic shocks, this optimism should translate into a healthier business outlook for international brands as well. According to early signs, 2010 could be an excellent curtain-raiser for a new decade of growth for international fashion brands in India.

[The 2009 report is available here: “International Fashion Brands – India Entry Strategies”]

(c) 2010, Third Eyesight

[Note: This report is based on information collected from a combination of public as well as proprietary sources, and in some cases may differ from press reports. However, no confidential information has been shared in this report.]

Devangshu Dutta

January 5, 2010

If we were to look at phrases that have cropped up during the recent recessionary times in the consumer goods sector, “private label” has to be among those at the top of the list.

From clothing to cereals, toothpaste to televisions, there is hardly a category that has not seen retailers trying their hand at creating own labelled products.

The first motivation for most retailers to move into private label is margin. On first analysis, it appears that the branded suppliers are making tons of extra money by being out there in front of the consumer with a specific named product. The retailer finds that creating an alternative product under its own label allows it to capture extra gross margin. Typically the product category picked at the earliest stage of private label development would be one for which several generic or commodity suppliers are available.

At this early stage, the retailer is aiming for a relatively predictable, stable-demand and easily available product whose sales would be driven by the footfall that is already attracted into the store. A powerful bait to attract the customer is the visible reduction in price, as compared to a similar branded product. If the product can be compared like-for-like, customers would certainly convert to private label over time.

However, maintaining prices lower than brands can also be counter-productive. In many products, while customers might not be able to discern any qualitative difference, they may suspect that they are not getting a product comparable to one from a national or international brand. And while private label can drive off-take, the price differential can also erode gross margin which was the reason that the retailer may have got into private label in the first place. Over time, such a strategy can prove difficult to sustain, as costs of developing, sourcing and managing private label products move up.

The other strong reason a retailer chooses to have private label is to create a product offering that is differentiated from competitors who also offer brands that are similar or identical to the ones offered by the retailer. Department stores, supermarkets and hypermarkets around the world have all tried this approach – some have been more successful than others. The idea is to provide a customer strong reasons to visit their particular store, rather than any of the comparable competitors.

Of course, when differentiation is the operating factor, the products need more insight and development, and closer handling by the retailer at all stages. A price-driven private label line may be sourced from generic suppliers, but that approach isn’t good enough for a line driven by a differentiation strategy. In this case, costs of product development and management increase for the retailer. However, to compensate, the discount from a comparable national brand is not as high as generic nascent private label. In fact, some retailers have taken their private label to compete head on with national brands – they treat their private labels as respectfully as a national branded supplier would treat its brand.

So what does it take to go from a “copycat” to being a real brand?

Third Eyesight has evolved a Private Label Maturity Model (see the accompanying graphic) that can help retailers think through their approach to private label, whether their product offering is dominated by private label, or whether they have only just begun considering the possibility of including private label in their product range. The model sketches out a maturity path on five parameters that are affected by or influence the strength of a retailer’s private label offering:

In some cases, retailers may have multiple labels, some of which may be quite nascent while others might be highly evolved, clear and comparable to a national brand. This could be by default, because the labels have been launched at different times and have had more or less time to evolve. However, this can also be used as a conscious strategy to target various segments and competitive brands differently, depending on the strength of the competition and their relationship with the consumer.

The interesting thing is that size and scale do not offer any specific advantage to becoming a more sophisticated private label player. Some extremely large retailers continue to follow a discounted-price “me-too” private label strategy where even the packaging and colours of the product are copied from national brands, while much smaller players demonstrate capabilities to understand their specific consumers’ needs to design, source and promote proprietary products that compare with the best brands in the market.

For a moment, let’s also look at private labels from the suppliers’ point of view. As far as we can see, private label seems to be here to stay and grow. Suppliers can treat private labels as a threat, and figure out how to ensure that they retain a certain visibility and relationship with the consumer. On the other hand, interestingly, some suppliers are also looking at private label as an opportunity. They see the growth of private label as inevitable, and would much rather collaborate in the retailer’s private label development efforts. This way they can maintain some kind of influence on the product development, possibly avoid direct head-on conflict with their own star branded products and, if everything else fails, at least grab a share of the market that would have otherwise gone over to generic suppliers.

If you are retailer, I would suggest using the Private Label Maturity Model to clarify where you want to position yourself, and continue to use it as a guide as you develop and deliver your private label offering.

If you are a supplier concerned about private label, my suggestion would be to gauge how developed your customer is and is likely to become, and ensure that you are at least in step, if not a step ahead.

Of course, if you need support, we’ll only be too happy to help! (Contact Third Eyesight to discuss your private label needs.)

Devangshu Dutta

January 4, 2010

Prompted by an article in the New York Times, Bernice Hurst, Contributing Editor of RetailWire, brought up an interesting subject to discuss – the tradition of small, independent retailers on Manhattan’s Lower east side, their survival despite the recession, and their determination to thrive.

One of the retailers interviewed for the article said that the business was “so much fun”. In referring to the kind of products she was developing said, “there are no boundaries to these things”.

Imagination may have no boundaries, but markets always do. When you’re small fry the pond seems limitless. And if all is in harmony (no tuna to gobble you, all fry remaining small, enough algae to feed off, forever), then the market is a good and boundless place. If only.

Personally, I hope there will always be some ponds with room in them to let such small fry bubble up their innovations: they keep the fashion business alive.

They also serve to remind us that there are reasons for running business that are not based on the race-to-scale.

The New York Times article is here – Yes, We’re Open – and the Retailwire discussion is here – Manhattan Still Home to Independent Retailers.

Devangshu Dutta

December 30, 2009

There’s been a lively debate on Retailwire.com initiated by Tom Ryan (Managing Editor), and prompted by an article in the Washington Post about how consumers are literally taking matters in their own hands and testing toys and domestic items for the presence of toxic substances.

Some of the commentators feel that this is going too far and could create waves of unnecessary panic, that consumers and consumer advocacy groups do not have the necessary expertise nor a balanced judgement, that it is a job for the government agencies. Others support the move and say that such moves are absolutely in order.

In my opinion, despite good intentions on the retailer’s part and the humongous bureaucracy in the supply chain, if product safety compliance is incomplete and if consumers feel insecure, then they will provide the wake-up call any which way they can.

We may decry the paranoia, but let’s also consider the increase and concentration of risk in recent years due to factors such as:

However the industry may feel about it, I think consumer advocates have the steering wheel on this one. Unless government outlaws ‘unapproved’ testing…but I wonder how palatable that would be, politically speaking.

Here’s the original article from the Washington Post.

And the discussion on Retailwire.com is here (needs a free sign-up).

Devangshu Dutta

December 18, 2009

(Contributed to the BusinessWorld cover story – “What 2 Expect in 2010”, issue of January 4, 2010)

Everything that can be said and assumed about the Indian market is true at some level of granularity. Very simply, in India there is a segment for every product, an opportunity for every service, be it ever so small. But when bubbles are bursting all over, as the Noughties Decade comes to a close, the puzzle that is Indian consumer market also warrants a fresh look.

For most of the Noughties Decade India has seen Generation-C, the “Choice” generation, coming of age. They have moved over from being “secondary customers” consuming off their parents’ incomes, to entering the work-force and becoming customers in their own right.

It may sound trite, but Gen-C customers have grown up with many models of 2-wheelers and 4-wheelers and colour television with multiple channels. They have many more career options and many more opportunities in each career. Not only have they grown up on a diet of choice, they have also grown up with much higher confidence about the future, about their place in the world and what they can expect. And they have infected the outlook of generations older than them as well with a similar confidence.

Therefore, for most of the decade, it has been a distinctly rosy picture for consumer goods marketers and retailers. Business plans routinely expected 20-50% annualised growth, and businesses even delivered those figures on some basis or the other. Organizations as diverse as retailers and management consultants were inspired by India’s age-old image as the Bird of Gold. Supermarket chains mushroomed like never before, department stores and speciality retailers grew their footprints, quick-service and casual dining expanded covers, while electronics, durables, leisure companies, and car brands all counted India among their hottest markets.

Product off-take reflected this outlook. Amongst the FMCG sector, while basic items such as the bath and shower segment demonstrated a steady annualised growth of about 7%, premium cosmetics galloped at almost 20% a year. While the relatively mature 2-wheeler market grew at just over 7.5% annually between 2002-03 and 2008-09, the 4-wheeler passenger vehicle market demonstrated growth of almost 14% a year in the same period.

All this was before the recent rude interruption.

A speed-breaker began showing up in the consumer market in late-2007 and grew larger through 2008. Once the global financial markets melted down in late-2008, media sentiment turned acutely negative about the Indian market as well. And, eventually, with uncertainty prevailing around the world, consumer spending in India did take a hit. Consumers cut back on the frequency of purchases or traded down.

On the trade side, retail businesses began acknowledging that stores were performing below plan and went into rationalisation mode. For branded suppliers, where some of the growth had come from stuffing the pipeline and filling new shelves, wholesale order books became thinner.

Yet, as painful as the economic scenario might have appeared, the Indian consumer market has shown remarkable resilience. Demand in smaller cities and towns has remained robust. Regional brands, especially, found plenty of opportunity to grow in markets and geographical regions where they were under-penetrated or absent.

And as the mood lifted through the latter half of 2009, consumer demand clearly moved back up. The speed at which the demand rebounded would suggest that the Indian market was relatively sheltered from the global economic storm.

However, there are some critical differences to understand.

On the one hand, Gen-C’s confidence shook for the first time – a generation that has only seen upward mobility, witnessed job cuts and salary freezes or declines even if only second-hand. Comparisons with the Great Depression may be exaggerated but it is a scenario they can now imagine as a possibility. At least three new professional academic batches have or will have moved into the job market under these sober conditions. On the other hand, tremendous inflation in basic costs supports some amount of uncertainty about the future. The fact that many of the Gen-C would have just begun or would be about to begin families serves to only heighten such anxiety.

So, let’s recognise two immutable facts about the Indian consumer market in the current environment.

First: that the ancestral “steel safes” are back, at least figuratively if not literally. Customers do want to save more for now. And if they are spending, they want to feel that they are extracting far more value than the price they are exchanging across the counter, value that will last long after the transaction at the store. In recent years, this inherent ‘value orientation’ of the Indian consumer was neglected by many. Now every product, service or brand must aim to deliver this sustainable value, and demonstrate the value repeatedly.

Secondly, each business needs to look at the lifetime value of a customer if it can. Rather than cutting the golden bird open and trying to extract all the golden eggs at once, one needs need to keep the bird well-fed, happy and healthy, and enjoy its rewards over several years. Rather than creaming the market, pricing, branding and distribution need to be structured for a sustainable relationship with the customer.

Some businesses will work better than others in this market, and strategies will need to be adapted. A lifecycle approach may handy in identifying the business segments which might meet the steel safe criterion, or the golden goose criterion, or both.

The first segment that comes to mind is weddings. Wedding expenditure is seen as a “social investment” for both the families, and the actual items bought are an investment into the couple’s future together. So, bridal trousseaux and wedding wardrobes, wedding arrangers and catering, and household goods provide significantly more tangible and intangible value than the money spent.

Similarly, “first child” isn’t usually a segment in any marketing handbook, but should be. The couple’s first born, especially if the baby is the first in its generation will usually get a disproportionate amount of attention and spending on clothing and utilities. A baby’s growth into a child, of course, can provide a relationship and marketing opportunity that can last for years, but the first 2-3 years are specifically valuable. What’s more, given India’s demographic dividend in the form of a sustained under-30 age group, baby products have a sustained and growing value as a market.

As the child grows, there are clear indicators of current and future value that can drive purchases. While base schooling is an essential expenditure, extra-classes and tuitions are a high-value discretionary investment that parents are choosing to make. Sports, on the other hand, however essential they may be to a child’s development are often seen as a distraction. That is, unless the child is attending sports coaching and the parents have an eye on helping the child create a career from it – in which case, a coach who is apparently good, branded equipment and kit are definitely worth investing in. So a cricket coaching franchise might just be the ticket to fortune, while a toy company may struggle. Some may decry the decline in art, craft, philosophy and fundamental sciences, but these are not on the list of priority of most parents. In the short to medium term, parents would continue to disproportionately push their wards into academic disciplines that are seen to develop marketable skills and pay well. Expect continued growth in the engineering, medical and management education market, but also in other vocational disciplines.

On the other hand, everything is not an investment for the future. Present comforts may also provide extra value, through convenience.

Some of these comforts may be as small as enjoying out-of-home exotic meals (pizza and pasta still qualify as exotic for the bulk of the population). Or if eating out looks out of budget, ready-to-eat and ready-to-cook meals are an easy substitute. Jubilant, Yum, McDonald’s, Haldiram, Sarvana’s, Nirula’s and the thousands of other casual dining and snack food chains have a long clear highway of growth ahead, as do snacks and packaged food companies such as Nestle, Britannia and ITC.

Brown goods and white goods that offer comfort and convenience – coolers, water heaters, convectors, air-conditioners and kitchen gadgets – continue their onward march, despite the huge shortfall in electricity. Even if the big brands struggle with their price points and overheads, regional brands and private labels will continue growing strongly in these segments.

Health is another area for significant investment. With prevalence of lifestyle-ailments, from stiff necks to high blood pressure, basic pharmacists to cardiovascular specialists are all in demand. Anticipate significant growth to continue in over-the-counter medication, medical devices, as well as clinical and hospital care.

At the other end of the scale, with decent and adequate public transport lacking in most cities, we can expect personal vehicles to increase multi-fold, despite the small blip in 2008-09. About 60 million 2-wheelers and over 10 million passenger vehicles have already been added during the decade, and the growth trend looks set to resume from 2010, unless there are significant oil price or vehicle taxation shocks delivered by the government.

And as consumer confidence resurges, more overt displays or personal spends will return as well, including apparel, footwear, home products, accessories, vacations, fitness and recreation, but we would expect them to follow behind the higher priority “safe” or “geese” segments.

Finally, the one thing that marketers in any product need not be really concerned about whether there is a future in this market. Even, Hindustan Unilever, a mature FMCG company with very high distribution penetration built over decades, still counts less than 60% Indians as its customers.

Surely most companies have a much longer road ahead before they need to be worried about their markets becoming saturated.