admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

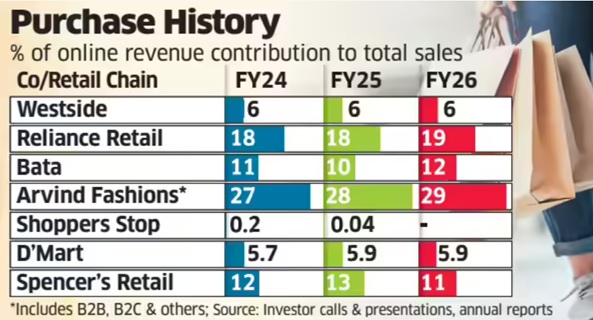

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

January 7, 2010

By Tarang Gautam Saxena, Chandni Jain and Neha Singhal

In Retrospect

While India was a promising market to many international brands, it was not completely immune from the global economic flu. More than its primary impact on the economy, the global downturn sobered the mood in the consumer market. Even the core target group for international brands, that had just begun to splurge apparently without guilt, tightened their purse strings and either down-traded or postponed their purchases.

In 2008 in the midst of economic downturn, skepticism and uncertainty, the international fashion brands had continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008 targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many players ended up discounting the goods heavily to promote sales while a few also gave up and closed shop.

As the Third Eyesight team had foreseen last year, 2009 saw a further slowdown and fewer international brands being launched during the year. The brands that were launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack and Timberland. Some of these had already been in the pipeline for quite some time and invested a considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

International Fashion Brands in India

After many deliberations, the well-known global brand Donna Karan New York set foot in the Indian market in 2009 through an agreement with DLF Brands to set up exclusive DKNY and DKNY Jeans stores India. The brand is also reported to have signed a worldwide licensing agreement with S Kumars Nationwide Ltd to design, manufacture and retail DKNY menswear in certain specific countries.

Second Chances

Amongst the international brands that have recently entered the Indian market, a few are on their second or even third attempt at the market.

For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills, and the partnership intended opening 15 stores by 2010. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis on retailing international brands within the country. Within a few months of the ending of this relationship, Diesel signed a joint venture with Reliance Brands for a launch scheduled for 2010. Both partners seem to be strategically aligned with a common goal as the international iconic denim brand wants to take on the Indian market full throttle and the Indian counterpart has indicated that it wants to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008, despite plans to open more than 50 stores in the first three years of operations. Miss Sixty has finally entered India through a franchise agreement with a manufacturer of women’s footwear and accessories. The company has currently introduced only shoes and accessories category and is looking at potential partners for its label Energie and girls’ range Killah.

Other brands that have re-entered the Indian market include Germany-based Lerros whose first presence in India was back in mid-1990s. The brand re-entered the market in 2008 through own brand stores and is growing its presence through this route as well as through multi-brand stores.

Oshkosh B’gosh is another brand that had entered India in mid 1990s, through a licensing agreement with Delhi based buying house, Elanco. The licensee found the childrenswear market hard to crack, and closed down. In 2008, Oshkosh re-entered the Indian market through a licensing partnership with Planet Retail and is now available through shop-in-shop counters at Debenhams stores. Reports suggest that it may consider setting up exclusive brand outlets.

During the turbulence of 2008 and 2009, a few brands also exited the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both) to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations and for the amount of effort and money being invested, and that it was better to pull the plug.

Some brands that have been pulled out of the Indian market during 2008 and 2009 include Dockers, Gas, Springfield and VNC (Vincci). Gas (Grotto SpA) is reported to remain interested in the market but has not found another partner after its deal with Raymond fell through in 2007 and all dozen of its standalone stores were shut down.

The Scottish brand Pringle and its Indian licensee did not renew their agreement upon its expiry. The Indian partner has reportedly signed an agreement to launch another international brand in India, while Pringle is said to be looking for new licensee.

The good news is that successful relationships outnumber every exit or break in relationship possibly by a factor of ten. Some of the brands that have sustained are among the early entrants having a presence in India since the late-1980s and 1990s or even earlier. These include Bata, Benetton, adidas, Reebok (now also owned by adidas), Levi Strauss and Pepe. Having grown very aggressively during 2006 and 2007 Reebok quickly became the largest apparel and footwear brand in India, while Benetton and Levi’s are expected to cross the $100-million mark for sales this year.

Entry Strategy & Recent Shifts

As envisaged in Third Eyesight’s report from a year ago, with changing market conditions and a growing confidence in the Indian market, there has been a shift among international brands in the choice of the launch vehicle. While franchising has been the preferred mode of market entry in the recent past for risk-averse brands, more brands today demonstrate a long-term commitment to the Indian market, and are choosing to exercise ownership through wholly or partially owned subsidiaries and through joint ventures.

In 2009, we have seen a noticeable shift in favour of joint-ventures as the choice for entry into the market. Even the brands already present are looking to modify the nature of their existing presence in India in order to exert more control over the retail operations, products, supply chain and marketing.

Current Operating Structure

(End 2009)

Brands that changed their operating structures and, in some cases partners, in recent years include VF (Wrangler, Lee etc.), Lee Cooper, Lee, and Louis Vuitton amongst others.

Mothercare, the baby product retailer, which is present through a franchise agreement with Shopper’s Stop has, in addition, recently formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores. Gucci, which had initially entered in 2006 with the Murjani Group as a franchisee, has recently changed over to Luxury Goods Retail, and is now in the process of restructuring the relationship into a joint venture.

VF has also been reported to be looking to license Nautica, Jansport and Kipling to a new partner. Until now, these brands were handled through the joint venture with Arvind Brands. Arvind has increasingly focused on its core business, closed stores and scaled down expansion plans for the international brands.

Burberry that had entered India in 2006 through a franchisee arrangement with Media Star opened two stores under this arrangement. It has now set up a new joint venture with Genesis Colors and plans to open 20 stores across the country.

More recently Esprit has also been reported to have approached Aditya Birla Nuvo to deepen its engagement by moving from its distribution arrangement into joint venture as the international brand sees excellent potential in the Indian market.

Buckling up for 2010

Throughout 2009, the one fact that became clear was that the Indian market was resilient. Now, as the global economic condition stabilizes, confidence levels of brands and retailers in India have also improved.

Several launches are already expected in 2010, and possibly many more are being worked upon. In the following 12 months, consumers can expect to find within India acclaimed brands such as Diesel, Topman, Topshop and the much-anticipated Zara. Many more Italian, British and French brands are examining the market.

Most of the international fashion brands already present in the market are also projecting a cautiously upbeat outlook in their plans, while a few are looking positively bullish.

For example, Pepe, an old player in premium and casual wear segment, has reported plans to grow its retail network further and open 50 more franchise stores by September 2010. Similarly the German fashion brand S. Oliver that entered the Indian market in 2007 is looking to grow significantly. It has already moved from a franchise arrangement with Orientcraft to a joint-venture with the same partner, and has stepped up its above-the-line marketing presence. The brand has recently reported its plans to scale up its retail presence to 77 stores by the end of 2012 while also strengthening its presence through shop-in-shop in multi-branded outlets in high potential markets.

Those international brands that have tasted success have not achieved it by blindly importing business models and formulas from other markets. Most have had to devise a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched. These include The Body Shop which decreased its prices by up to 30% this year, and Marks & Spencer which reduced prices by 20-40%. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

On the operational side, the good news for retailers and brands is that the average real estate costs have reduced significantly, although marquee locations remain high. In several locations lease models have also moved from only fixed rent to some form of revenue sharing arrangement with the landlord. And, while the sector has seen some employee turmoil as many non-retail executives who came into the business in the last 5-7 years have returned to other sectors, employee salary expectations are also more realistic.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s recent work with international brands’ business units in India highlights the international players’ concern with ensuring a consistent brand message, improved organizational capabilities right down to front-line staff, and focus on unit productivity (per store and per employee).

We may yet see a few more exits, and possibly some more relationships being reshuffled and partners being changed. However, all things considered, we can look forward to a net increase in the number of international brands in the country.

The Indian consumer is certainly demonstrating more optimism and as far as there are no major unforeseen global or domestic shocks, this optimism should translate into a healthier business outlook for international brands as well. According to early signs, 2010 could be an excellent curtain-raiser for a new decade of growth for international fashion brands in India.

[The 2009 report is available here: “International Fashion Brands – India Entry Strategies”]

(c) 2010, Third Eyesight

[Note: This report is based on information collected from a combination of public as well as proprietary sources, and in some cases may differ from press reports. However, no confidential information has been shared in this report.]

admin

May 9, 2009

By Devangshu Dutta, Tarang Gautam Saxena

While the Indian consumers have aspired to own international fashion brands, India’s large population base in turn has been an aspirational market for the international companies.

To remote observers, the Indian market may appear to be a virgin territory as far as international apparel and footwear brands are concerned. But India has seen the presence of international brands for almost a century, including mass brands such as Bata and luxury brands such as Louis Vuitton. However, as the colonial government systematically repressed local textile production, the local resistance to foreign products grew as well. Therefore, until the 1980s, the presence of international fashion brands was negligible.

In the early 1990s, as the Indian economy opened up again, a few international fashion brands entered the Indian market. The pioneering companies during this stage were Benetton, Coats Viyella and VF Corporation.

At this time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment which was thus a target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike).

In the midst of this the media industry was also witnessing a high growth which aided the international brands in gaining visibility and establishing brand equity in the Indian market.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. A growing supply of good-quality retail real estate in the form of shopping centers and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores and shops-in-shop.

The number of international brands continued to grow each year at a steady pace until the early 2000s, and took off exponentially thereafter. By 2005 the number of international fashion brands present in India was over three times compared to that in the mid 1990s. The last few years (since 2005) have continued the significant growth of international fashion brands, including luxury brands such as LVMH, Aigner, Tommy Hilfiger and Chanel.

The Popular Entry Strategies

Many of the international companies entering India in the late 1980s and 1990s chose licensing as the entry route to India to gain a quick access to the Indian market at a minimal investment.

A few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand.

In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought investors in retail real estate that were ideal franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in “Single Brand” retail). Using this route, many brands have entered India by setting up majority owned joint ventures, or transitioned their existing franchise arrangements into a joint venture structure.

The Entry Structure for Some International Brands

| Entry Strategy | Time Period | ||

| 1980s or Earlier | 1990s | Post-1999 | |

| Licensed | Louis Philippe, United Colors of Benetton and 012, Wrangler | Allen Solly, Arrow, Jockey, Lacoste, Lee, Nike, Van Heusen, Vanity Fair | Puma |

| Wholly Owned Subsidiary | Bata, Pepe Jeans | Levi’s® | Hanes, Triumph |

| Joint Venture (Majority) | Adidas, Reebok | Diesel, Nautica, Sixty Group | |

| Franchise or Distribution | Aldo, Burberry, Canali, Versace, Debenhams, Esprit, Gucci, Guess, Hugo Boss, Mango, Marks & Spencer, Mothercare, Tommy Hilfiger | ||

| Joint Venture (incl. Minority Stake) | Celio, Etam, Giordano | ||

Source: “Global Fashion Brands: Tryst with India” (A Report by Third Eyesight) © Third Eyesight, 2009

Note: The above table shows the structure used during entry, and not the structure that exists currently.

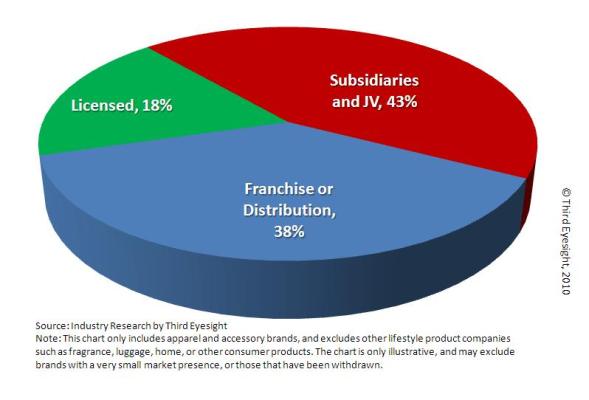

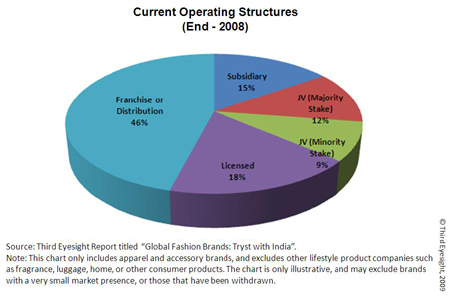

By the end of 2008, just under half of the brands were present through a franchise or distribution relationship, while over a quarter had either a wholly-owned or majority-owned subsidiary. These structures allowed the brands to have greater control of operations, particularly of product.

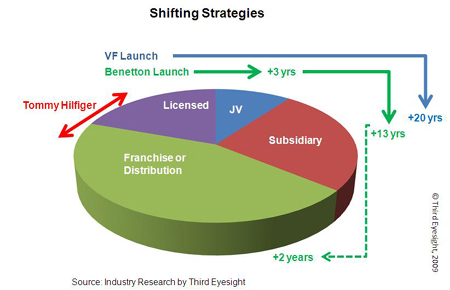

Shifting Strategies

Many international companies have evolved their presence in India into structures different from those at the time they entered the market.

A good example depicting the shift in business strategy is that of VF Corporation which entered India in 1980s by assigning the Wrangler license to Dupont Sportswear. Since then it has launched a variety of brands in different product categories with number of Indian partners and finally formed a joint venture, VF Arvind Brands Pvt. Ltd., with Arvind Brands.

Another example of a company that has evolved its presence is Benetton, which first entered India through a licensee (Dalmia). Benetton then transitioned in 1991 into 50:50 joint-venture and finally in 2004 took over the Indian business completely. However, it adopted the franchising route in 2006 for its premium fashion brand, Sisley, appointing Trent (a Tata Group company) as the national retail franchisee.

Many other companies such as Nike, Tommy Hilfiger, Marks & Spencer and Pierre Cardin (as described in our report “Global Fashion Brands: Tryst with India”) have changed their approach as the original structures did not perform as well as they had expected.

Obviously, each such change has cost the brands time, management effort, money and, sometimes, market share.

We believe that these shifts and the pain related to it could have been reduced, had the brands ruthlessly questioned the motivation for considering this market and their expectations from the market in determining an appropriate strategy.

What’s Ahead?

In the midst of economic upheaval around the world, how does India look as a market for international fashion brands?

Well, it is difficult to generalize even in the best of times. In the current global turmoil there is certainly a lot more unpredictability about international expansion for most companies.

Although India’s position as a target market for international brands has been improving, as is evident from the number of launches in the last 6-7 years, some companies considering international expansion may prefer entering other markets that may seem more “familiar”, developed and safe (such as Europe, Japan, South Korea or Taiwan). Against such comparisons, India’s growing but fragmented market can seem chaotic and difficult to deal with.

However, the fact remains that there are very few markets globally that can provide the sustained size of mid-term and long-term opportunity that India does. We are already seeing the more far-sighted and committed brands consolidating their position and presence in the market by continuing to look at expansion, even while examining how they can make their existing points of sale perform better. We also constantly come across new companies carrying out investigations into the market.

In the current environment we expect to see a shift in the nature of launch vehicle. While franchising seems to be a safe option for risk-averse brands in the current times, we will probably see more brands with a long term strategy, who would establish a controlled presence either through joint-ventures or through wholly-owned subsidiaries, since they can lay the foundation of the business today at much lower costs today than in the past few years.

India’s foreign direct investment (FDI) policy, allowing FDI only up to 51% in retail trading of “Single Brand” may have held back some fashion brands as they are still managed by owner founder with a conservative outlook on “control”. However, in the last couple of years, we have found companies not being deterred by the barriers to FDI.

As their comfort and familiarity with India has grown, international companies are more willing today to create corporate structures that allow them a presence in the market today and a step-through to a more controlling stake as and when government regulations allow.

All in all, we feel that international brands are in India not only to stay, but also to expand. There is yet a lot of potential untapped in the market, and as the integration of the Indian consumer with global trends continues, international brands can expect to find India an increasingly fertile ground for growth.

(c) 2009, Third Eyesight