admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

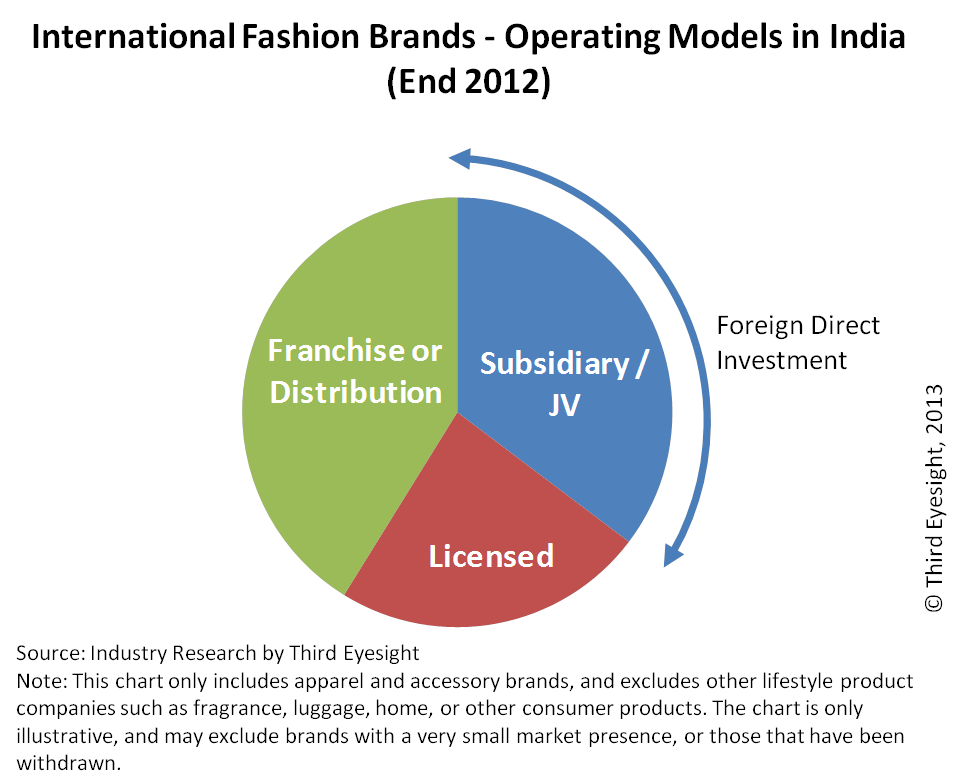

Routes to Market – The Evolution

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.

Devangshu Dutta

August 26, 2011

A few months ago, when asked to speak about value-addition at a food industry seminar, I decided, in a deviation from the usual discussion, to dissect the meaning of “value”.

Most people in industry focus on only one dimension of value-addition – the economic value added by processing and transforming food raw materials – virtually ignoring two other dimensions which are required for most of the (undernourished) population: calorific value and nutritional value (see “Perishable Value Opportunities”).

At the end of that seminar session, an agriculturist from the audience put forth a very pointed question: “What is the cost of the potatoes in a bag of branded chips that sells for Rs. 10? Or to put it another way, how much of the retail price actually goes back to the potato farmer?”

The question, of course, was completely loaded with angst on the economic imbalance between farm and factory, supplier and buyer, small and big, rural and urban. But it also underlined missed opportunities to capture economic value, which in turn accentuate the imbalances in growth.

Economic value can be added to food through improvement, providing protection, changing the basic product and through marketing. Improvement typically focuses on seeds, growing techniques and post-harvest areas for improved quality of harvests, disease resistance, better colours, size and flavour, possibly nutrition. Protection initiatives work across cultivation, harvest and post-harvest, storage, during processing, through packaging, while change is essentially focused on processing techniques (cooking, combining, breaking down and reconstitution).

There is a lot of work going on in the food supply chain to enhance the value captured closer to the farmgate. And, certainly, the “value-added” earlier is vital to maintaining and building value later in the supply chain.

However, what is striking is the fact that as we move downstream towards final consumption, the economic value captured as a price premium also increases dramatically.

So, as depressing as the multiplier may be to the farmer, on a kilo-for-kilo comparison, the bag of factory-fresh potato chips is priced many times higher than his farm-fresh potatoes. And, the maximum economic value is created, or at least captured, by the act of branding and marketing.

The Love is in the Brand

A short quiz break: can you recall the “most valuable company” in the world in August 2011, as measured by valuation on the stock market?

The answer is Apple. It is a company that physically manufactures nothing, but tightly controls the design, development, sourcing, distribution and, yes, branding of a group of products and services, whose fans seem to grow by the minute.

Of course, one can argue that Apple “produces” by the very act of designing completely new, highly desirable, products that are not available from anyone else, and that this is what provides the premium. But similar premium – which is due to branding and marketing, rather than proprietary products – is also visible in thousands of companies, across product sectors, including food. That sustained price premium is the sign that the consumer trusts and wants a particular brand’s product more than another one. There is a hook, a strong connect, due to which that consumer is willing to lighten her wallet just that much more.

In India, surprisingly, “value-addition” discussions in the food industry focus almost entirely on cultivation, storage and transformation through processing, virtually ignoring branding and marketing. In fact, branding is usually only discussed in the context of multinationals or some of the largest Indian companies. What’s more, most of the brands discussed are focussed largely in the area of processed food products that originated in the west.

Run these tests yourself. When you think of food and beverage branded companies who do you think of? And, when you think of food brands, what kind of products come to mind first?

The answer is that the brand landscape is dominated by products such as biscuits and cookies, jams, fruit and non-fruit beverages, potato chips, 2-minute noodles, confectionary products and food supplements, mostly from the portfolio of some of the largest companies operating in the market.

Of course, there are some alternative examples.

Aashirvaad and Kitchens of India present quintessentially Indian products (albeit from the gigantic stables of ITC which also has a multinational parent).

And, yes, there are cooperatives such as Lijjat, as well as home-grown mid-sized companies such as the Indian snack maker Haldiram’s, spice brands such as MTR and MDH, pickle brands such as “Mother’s Recipe”, rice brands such as Kohinoor and Daawat.

But, given the size of the Indian food market and the width and depth of Indian cuisine, shouldn’t there be more brands that are Indian and focussed on essentially Indian food products?

This is a tremendous opportunity – a gap – not just in the Indian market (among the largest and fastest growing in the world), but also globally.

The Hurdles to Branding

So, why aren’t there more Indian brands?

Let’s face it, for most companies, marketing fulfils one need: to communicate their name to potential customers. Most of them generally hope that if they do it enough, they would actually be able to sell more volume.

Of course, no one has been able to draw a straight line graph that correlates more marketing expense with higher sales.

Those are two self-destructive notions. Obviously, if marketing is an expense, then it must be minimised! And secondly, if it cannot be proven to be effective, why would you spend money doing it? For most people, branding is even fuzzier in that regard, in terms of what it is and what it achieves.

However, the picture changes when you look at marketing as an investment rather than an expense. As we evaluate any investment, there should be an expected return that should be quantifiable. Examples of Apple and other brands make it amply clear that branding and marketing, when done well, can certainly create quantifiable financial returns on the investment.

The second hurdle to branding and marketing is that they require consistency, which is not a strong point for most wannabe brands. They end up with too many messages to the consumer, or the messages keep changing and shifting. The company, the name, end up representing many things, sometimes everything, and eventually nothing.

The third, enormous, hurdle is the time needed to develop a brand with a decent sized marketing footprint and a deep relationship with the consumer. Most small and mid-sized companies, constrained as they are for resources, focus on areas that seem to offer more immediate returns, such as distribution margins or discounts, or even expansion of production capacity. Especially in the early years of the business, the benefits of branding and marketing seem to be too far in the future to be a priority for investment.

Due to these one of these reasons or a combination, many companies are unable to see their brands through to success. In fact, sadly, most companies do not last long enough to become owners of successful brands.

Even those who do achieve success and even market leadership, sometimes choose to cash-out on their success by selling their brands to larger competitors, rather than competing with the financial might of the giants (such as Thums Up being sold to Coca Cola; Kissan, Kwality and Milkfood being sold to Hindustan Unilever).

In the past, one of the other barriers in India was the hugely fragmented retail and distribution system, which essentially sapped energy, resources and focus for any company that wished to grow a brand across regions. In fact, one of the key lessons from the western markets is that the growth of brands has been closely linked to the expansion of retail chains. So, certainly, we should view the growth of modern retail in India as a platform for the emergence of regional, national and global Indian food brands.

However, there is a flip side to this retail growth. In the west, most retailers were focussed on running shops, and were content to leave product development and brand development to their suppliers, the national brands. These retailers began looking at private labels only as an additional source of margin well after they had gained scale, and even then they ventured rather carefully into the space. In India, on the other hand, private label is very high on the priority list of our nascent modern retailers, precisely because the effectiveness of that business model has been proven elsewhere and because there are such few national brands that have a strong, irrevocable connect with the consumer.

Should You Invest in Branding?

The short answer is to that question is: yes.

It doesn’t matter if you run a small company or start-up, or a more mature company. It doesn’t matter whether you are selling a consumer product directly, which is the most effective and most necessary playing field for building a brand, or an intermediate product or service where you can still achieve a premium within the trade.

If you are committed to selling only commodities, where your selling prices are determined only by the tug-of-war between supply and demand, government policies and Acts of God, then you wouldn’t be reading this article.

Since you are reading this, you should brand.

In the short to medium term, if you do the job well, your customers will pay you a premium. And in the mid to long term, financial investors looking to ride India’s economic growth are more willing to put their money in a company that has a recognisable hook and a trading premium over its generic competition.

The brand can be built on any platform for which there could be a discernible premium. This can be trust (quality, quantity), simplicity and convenience (prepared snacks and meals, pre-ground spices, flour instead of grain), or even novelty (fizzy coloured sweetened water, reconstituted potato “chips” so uniform in shape and size such that they fit into a cylinder). Organic, vegan, fair-trade – you take your pick of the platform on which to build the brand.

Possibly the strongest driver of premium and brand value is a properly maintained heritage. Some brands have a past, some of them even have a history, but very few have a heritage. If your business has a history, there is a heritage waiting to be discovered, and it is worth a lot.

Of course, this doesn’t mean that a brand should become anchored at a certain historical time point and expect to only milk its age. Heritage is always viewed in a cultural context and culture evolves over time, so the most effective brands maintain a link between the attributes of their past to their ever-evolving present.

As with most other things, it is good idea to start early. Take on board the lessons of branding early in the company’s life so that the foundation is strong, and the brand can grow organically. As a side benefit, strongly branded companies also have strong and cohesive organisation cultures, a fantastic defence during times of high employee attrition.

The Global Branding Opportunity for Indian Food Companies

One of the most important ingredients of a good brand is clarity of identity and origin.

Often we confuse identity with the name, the logo, fonts or colours associated with a brand. Yes, a brand’s identity is certainly indicated by these – as much as our name and our physical appearance indicate our identity. However, the identity itself is much larger; in fact, it is helpful to think of the brand’s identity as a personality. The personality gets expressed in many different ways, but is tied together in a definable manner and has some strong traits that define its actions.

There are clear statements that can be associated with effective brands, whether or not they have been expressed by the company or brand in any of its formal communications. For instance, some globally relevant Indian brands include Tata Nano (“frugal engineering”), the Taj Mahal (“timeless beauty”), Goa (“party”), Rajasthan (“royal exotica”), and Kerala (“bliss”).

(I am deliberately picking “global relevance” as a theme to keep in mind that there is, literally, a world of opportunity that we could be looking at.)

We find a high number of tourism-related brands in this list, because these are destinations that pull the customer in – as long as they are true to themselves and relevant to the context of the consumer, they will be successful.

More conventional consumer product brands, on the other hand, must work harder to fit into the consumer own context, especially as they move away from their geographical origin, their home market.

This is particularly true of food, which is widely divergent across geographies. Some products can be adopted into multiple cuisines, offering more easily accessible opportunities and potentially greater scale. Rice and generic spices fit the bill here. However, for most other food items, the context of the home country cuisine is vital. Therefore, the growth of food brands, not surprisingly, is linked to the expansion of cuisines across borders. It is partly driven by the movement of people, and partly by the movement of culture (television and movies being the most important in current times), mostly both together.

For Indian companies, there is certainly an opportunity to ride on the back of the Indian diaspora across the world. And now there is an additional opportunity: expatriates who spend a few years living and working in India can also help to carry the cuisine and its associated brands out.

Finished product brands such as Tasty Bite, Haldiram’s and Amul are good examples of diaspora-led expansion, where the original driver was to bring people of Indian-origin a taste of home. In fact, Amul has recently announced that it wants to set up a manufacturing plant for cheese and other dairy products in the US, to service the Indian-origin population more effectively. Should it be restricted only to that? Certainly not; availability, if supported well by branding, can help it to cross into other segments as well.

As the consumption of Indian food grows across ethnic lines, it is likely to drive the growth of Indian ingredients as well – a perfect vehicle for branded ingredient suppliers. What’s more, Indian recipe books could even specify Amul Cheddar Cheese, MDH Chaat Masala or MTR’s Dosa Mix as ingredients – they wouldn’t achieve a 100% hit rate, but it would certainly be significantly higher than zero!

There is an opportunity to capture economic value that branding offers, which is very often greater than any other process in the food supply chain. Remember two phrases made famous by Hollywood: “show me the money” and “show me some love”. In the business of brands, these are one and the same.

It’s worth asking: do we have the patience to live through the lifecycle of a brand, and can we commit resources to nurturing it? If the answer is “yes” to both, we are most likely to benefit from branding.

Here’s to more Indian food brands that grow within India and across the world.

(If you need support with growing brands, do connect with us.)

Devangshu Dutta

July 22, 2011

The apparel retail sector worldwide thrives on change, on account of fashion as well as season.

In India, for most of the country, weather changes are less extreme, so seasonal change is not a major driver of changeover of wardrobe. Also, more modest incomes reduce the customer’s willingness to buy new clothes frequently.

We believe pricing remains a critical challenge and a barrier to growth. About 5 years ago, Third Eyesight had evaluated the pricing of various brands in the context of the average incomes of their stated target customer group. For a like-to-like comparison with average pricing in Europe, we came to the conclusion that branded merchandise in India should be priced 30-50% lower than it was currently. And this is true not just of international brands that are present in India, but Indian-based companies as well. (In fact, most international brands end up targeting a customer segment in India that is more premium than they would in their home markets.)

Of course, with growing incomes and increasing exposure to fashion trends promoted through various media, larger numbers of Indian consumers are opting to buy more, and more frequently as well. But one only has to look at the share of marked-down product, promotions and end-of-season sales to know that the Indian consumer, by and large, believes that the in-season product is overpriced.

Brands that overestimate the growth possibilities add to the problem by over-ordering – these unjustified expectations are littered across the stores at the end of each season, with big red “Sale” and “Discounted” signs. When it comes to a game of nerves, the Indian consumer has a far stronger ability to hold on to her wallet, than a brand’s ability to hold on to the price line. Most consumers are quite prepared to wait a few extra weeks, rather than buying the product as soon as it hits the shelf.

Part of the problem, at the brands’ end, could be some inflexible costs. The three big productivity issues, in my mind, are: real estate, people and advertising.

Indian retail real estate is definitely among the most expensive in the world, when viewed in the context of sales that can be expected per square foot. Similarly, sales per employee rupee could also be vastly better than they are currently. And lastly, many Indian apparel brands could possibly do better to reallocate at least part of their advertising budget to developing better product and training their sales staff; no amount of loud celebrity endorsement can compensate for disinterested automatons showing bad products at the store.

Technology can certainly be leveraged better at every step of the operation, from design through supply chain, from planogram and merchandise planning to post-sale analytics.

Also, some of the more “modern” operations are, unfortunately, modelled on business processes and merchandise calendars that are more suited to the western retail environment of the 1980s than on best-practice as needed in the Indian retail environment of 2011! The “organised” apparel brands are weighed down by too many reviews, too many batch processes, too little merchant entrepreneurship. There is far too much time and resource wasted at each stage. Decisions are deliberately bottle-necked, under the label of “organisation” and “process-orientation”. The excitement is taken out of fashion; products become “normalised”, safe, boring which the consumer doesn’t really want! Shipments get delayed, missing the peaks of the season. And added cost ends in a price which the customer doesn’t want to pay.

The Indian apparel industry certainly needs a transformation.

Whether this will happen through a rapid shakedown or a more gradual process over the next 10-15 years, whether it will be driven by large international multi-brand retailers when they are allowed to invest directly in the country or by domestic companies, I do believe the industry will see significant shifts in the coming years.

Tarang Gautam Saxena

June 27, 2011

In most conversations we have had with international brands in the last 2-3 years, India consistently appears on list of the top-5 markets in which to expand into.

The second most populous country in the world, India has a young population that offers a vibrant population mix that will provide a workforce and consumers in decades to come. There is steady growth in per capita income and a greater availability of credit, as well as a significant change in the consumers’ outlook to life that has propelled consumption levels.

The United Nations Conference on Trade and Development ranked India as the second most attractive destination for global foreign direct investments in 2010. The lowest recorded GDP growth rate during the global slowdown was still a decent 6.7 per cent. This growth rate is expected to have returned around 9 per cent in 2011, and is driven by robust performance of the manufacturing sector, as well as government and consumer spending.

The ongoing opening up of the economy over two decades and its robust growth has steadily attracted brands and retailers into the country. Many of them have now been in the country since the early 1990s, and the numbers have grown exponentially during the last 8-10 years. Despite this, the market is far from saturation and many more international brands are actively scouting the market.

Many of them are value brands in their home markets and may, therefore, be more a logical fit into a “developing” market, but there are also plenty of premium and luxury names on the list. For instance while the growth has largely been led by soft goods product brands, as incomes have grown, the presence of more expensive consumer durable brands has also expanded.

While the journey to the Indian market has not been a smooth ride even for the well established and successful international brands in the market, brands that have invested in understanding the psyche of the Indian consumer, adopted flexibility in market approach and displayed persistence, have been paid off handsomely.

Some international brands have exceeded domestic brands in size and reach, while others have had to reconcile to being niche operators. Some have seen profits while others may have their senior management wondering what fit of madness brought them to tackle this market where they can only dream about making money sometime in the future.

Typically, when looking at a new market the very first question anyone would ask is: what is the market potential for brand?

However, you should also be prepared to ask yourself: what need is the brand addressing and what is the value being offered by the brand? How would it be able to effectively and efficiently deliver that value? In many cases, for those entering a non-existent product category a more basic question is: “Is there a need for my product offer?” Just because a brand is huge somewhere else in the world does not automatically make it desirable to the Indian consumer.

While most brands want to target the Indian middle-class millions, their sourcing structure and strategy places them out of the reach of most of the population. Brands that have succeeded in creating a significant presence, maintaining their brand image and having a sustainable operating model have, almost uniformly had a significant amount of local manufacturing. Notable examples from fashion include Bata, Benetton, Levi Strauss, Reebok, among others. In case of certain food brands such as Domino’s and McDonald’s, the companies have collaborated with and developed their vendors locally to bring down costs, and improve serviceability.

Apart from the costs and margins, another important issue is that of the adaptability of the product mix. Brands that are sourcing locally and have a significant product development capability in India are also able to respond to specific needs of the Indian market better, rather than being driven by what is appropriate for European or North American markets. This is an enormous advantage when you are trying to be “locally relevant” to the consumer in an increasingly cluttered marketplace.

Indeed the question is more to do with the brand’s willingness and capability to create a product mix that is most suitable for India through a blend of international and India-specific merchandise. The famous “Aloo-tikki” burger by McDonald’s is a great example of a product specifically developed for the Indian consumers. Not just that, India is probably McDonald’s only market in which its signature dish, the Big Mac, is not sold.

Of course, flexibility in tweaking the product to suit Indian market can become a concern when it amounts to losing control over the brand direction, and mutating away from the core proposition that defines the parent in the international market. Many brands wish to control every aspect of product development head office, but this also severely limits their ability to respond to local market needs and changes. A one-size fits all strategy obviously will limit the number of consumers that the brand can effectively address in a market such as India.

Another key question is: what is the degree of control that a brand wants to exercise on the brand, the product, the supply chain and the retail experience of the consumer? The corporate structure itself may be determined by the internal capabilities and strategies of the international brand in their home market or other overseas markets. A brand that has presence through a wholesale business in the home market may not have internal capability or experience in retail, and would look for an Indian partner who can fill in the gap.

Based on whether they want direct operational control over store operations, international companies can set up fully owned subsidiaries or joint ventures to manage the business in India. Many brands prefer to take a slow and steady approach as they do want to exert a significant amount of control over the business (including companies such as Inditex, the owner of Zara, and other retailers such as Wal-Mart and Tesco), entering only when they are fairly confident of being able to closely manage the business in India right up to the retail store.

During our work we have come across both extremes – companies that want to manage the minute details of the India business out of their own head offices, as well as companies that are so hands-off that they only want to hear from their franchisee or licensee when things are especially good or particularly bad. While a balanced, middle-of-the-road approach would be the logical one in each case, in reality individual styles of the top management have a huge influence on the approach actually taken. Also, the size of the potential market segment – relevant to the brand – has an important role to play in the strategy. If the brand is meaningful only to a small segment of the population, or priced at the top-most end of the market, one company may choose to establish an exploratory distribution relationship, while another might choose to set up an owned presence rather than look for an Indian partner to handle their small business.

While perfect partnerships seldom exist, companies could be a lot more careful we have found them to be, in questioning the criteria and motivations for choosing partners. In some cases, financial strengths, or past industrial glory were qualifying factors for picking franchisees, and the relationships have failed because the business culture was divergent from the Principal’s. In other cases, partners have been picked because they “have real estate strengths”, but no consideration has been paid to whether the partner has the operational skills to manage a fashion brand.

On several occasions, franchise relationships and joint ventures have split because one or both partners find that their expectations are not being fulfilled, or the water looks deeper than it did when they got into the business.

The opportunities in India are many. As the managing director of one international brand commented in a conversation with Third Eyesight, India is a market where a brand can enter and live out an entire lifetime of growth.

However, international brands do need to carefully identify what role they wish to play in the market, and what capability and capacity they need operationally to create the success that can truly root a brand into the rich Indian soil.

admin

February 28, 2011

![]() Business

Standard, Mumbai, February 28, 2011

Business

Standard, Mumbai, February 28, 2011

![]() Sayantani

Kar (with inputs from Preeti Khicha)

Sayantani

Kar (with inputs from Preeti Khicha)

When some of India’s big retail chains banded together recently to substitute Reckitt Benckiser’s products with private labels to protest the latter’s decision to cut sales margins on its products, they were doing something many global retailers have done with great success. Part of their overall strategy, especially for large chains in the US and Europe, is to develop quality private label products that complement other pieces in their marketing mix. While this is one way retailers can differentiate their firms from competition, it also helps them flex their muscles in their relationships with brand manufacturers. Indeed, retail giants Tesco, Walmart and Carrefour have a significant portion of their sales coming from private labels — ranging from 10 per cent for Costco and 50 per cent for Tesco.

India is a back runner in the private label race, but it is

catching up. A Shoppers Trend Study by Nielsen found awareness

about private labels has gone up from 64 per cent in 2009 to 78

per cent in 2010 across 11 cities in India. Nielsen Director (retail

services) Siddharthan Sundaram says, “Over the last three

to four months, we found an increased awareness of private labels

in categories such as staples, household products, personal care

products such as soaps, biscuits and packaged groceries.”

Thanks partly to the recent economic downturn, there is greater

acceptance — and even loyalty — to such brands in India,

say marketers. Future Group Business Head (private brands) Devendra

Chawla reasons, “A label on the shelf becomes a brand by

covering the two feet distance from the shelf to the trolley.

After all it is the consumer’s choice.” Even in the

toughest segment for private labels to crack — fast moving

consumer goods including food and personal care — store labels

claim share of 19-25 per cent.

Low-involvement categories such as household cleaners were among the first to see the entry of private labels (17-44 per cent of sale in modern trade), bringing in huge margin-lifts for modern retailers. In categories such as food products — jams, biscuits and staples — private labels today contribute more than 25 per cent of modern trade sales. Little wonder, retailers are now mining shopper data to make private labels shed their ‘low’ly tag — low involvement and low cost. Store chains are segmenting their brands according to consumer needs, combining more than one brand according to consumer behaviour, besides launching high-involvement premium products and innovative packaging to give national brands a run for their money.

Innovate or die

Retail innovation has had a big role to play in speeding up the

process of consumer acceptance. Future Group’s retail arm,

which includes Big Bazaar and Food Bazaar, calls its in-house

products ‘private brands’ not labels. It has a separate

team, headed by Devendra Chawla, to research and test FMCG products

before launch. The team has a range of private brands — Tasty

Treat, Fresh and Pure, Cleanmate, Caremate, Sach, John Miller,

Premium Harvest and Ektaa. Look at how it is using shopper data

to improve its products. The insight that kids found ketchup bottles

cumbersome and had to be served — making it inconvenient

if an adult was not around — led it to change the packaging

that in turn gave the brand a margin advantage. By offering ketchup

in pouches, it saved on the price of the glass bottle and freight

(pouches take up less space in a truck, hence more can be fitted

in). While ketchup in glass bottles continue to be Rs 99 for a

kilo, its Tasty Treat ketchup pouches come in Rs 59 packs.

By working with vendors it has also come up with interesting combinations — for example, its Tasty Treat jam has three small tubs packed as one unit, each tub containing a different flavour to offer consumers larger variety.

Retailers have now donned the hats of “product selectors” and “product developers” at the same time, points out Third Eyesight CEO Devangshu Dutta. “So far, most of the retailers were just selecting products from vendors which are mostly lower-priced knock-offs of manufacturer brands,” he says. Not any more.

Ashutosh Chakradeo, head (buying, merchandising and supply chain), HyperCity Retail, explains the process his company follows: “To develop food products, we identify vendors, tie up with food laboratories, chefs and consumers to be part of the tasting panels. Before launching a private label we do at least a month of consumer testing. We identify customers from our loyalty programme called Discovery Club, which tells us who buys a certain category of product. We give the relevant consumers our private label products for trial for a month. We meet the customers at their homes, take their feedback and these changes are incorporated into the private label brand.”

“Our stores act as research labs and are a constant source of feedback,” points out Chawla of Future Group. Chawla estimates 3-4 per cent of the sales of private labels are ploughed back into packaging and design innovation. Reliance Retail CEO Bijou Kurien says, “The teams are our main investment in private labels. Our 100-strong designers across all the formats help in coming up with product designs that fill a need gap or offer a few more features at the same price as national brands.” Reliance Retail has recently launched its own brand of watches priced Rs 149-199 which “no national player can offer” points out Kurien.

The edge

Most vendors directly supply to retailers’ distribution centres,

cutting out cost leakage at the distributor’s and carrying

and forwarding centres. Direct access to store shelves and aisles

also cuts out the high mainstream advertising costs that brands

have to bear. By clever product arrangements and in-store promotions,

retailers can sway the shopper and draw attention to the price

advantage. Chakradeo says, “We display private labels in

heavy footfall areas in the store. We complement displays —

so we keep our private label ketchup near the bakery.”

To tackle the tricky personal care category of face creams and shampoos that Aditya Birla Retail’s More chain has entered, it plans to communicate promotional offers straight to its loyalty programme members. “It will help us induce trials,” says Thomas Varghese, More’s CEO.

Bundling products is another way to woo the value-conscious consumer. Six months back, Future Group started bundling its private brands. Chawla says, “Take home-cleaning, which requires a floor cleaner, glass cleaner, toilet cleaner and utensil cleaner which we combined as a shudhikaran solution of our Cleanmate brand.” The combi-pack costs Rs 125, which would come to around Rs 220-250 if shoppers bought a la carte. The margins are still high at 26 per cent. “Vendors are assured of volumes,” points out Chawla.

What it also does is convert the fence-sitter who has not yet bought into a category. For example, consumers who avail of the shudhikaran solution also get into the habit of using glass cleaners — a category which has a small base and gets most of its sales from modern trade. Similarly, Future Group saw a 25 per cent spurt in the sales of soups when it clubbed soup mugs with its Tasty Treat soup packets based on the insight that Indians preference to sip their soup out of a coffee mug.

Don’t be surprised if you see MNC brands coming out with combo-offers for their products, way bigger than the occasional bucket with a detergent!

Growing up

There are signs the industry is evolving. Private labels in FMCG

are shedding their low-cost tags. But retailers know better than

to vacate low price-points altogether. Instead, they are segmenting

their brands just as a manufacturer brand would do. Chakradeo

of Hypercity says, “Over a period, we hope to increase the

stickiness and the differentiation our brands bring to our stores.

Particularly, in staples where we have seen our private label

business grow rapidly. This is a very quality and price-sensitive

category. We started with basic products but now we have premium

daals (lentils) and basmati rice as part of our portfolio.”

Future Group too has its ‘good, better, best’ policy firmly in place. In staples, the stores offer some products ‘loose’, such as rice, wheat, lentils, which is at the bottom of the ladder. Its Food Bazaar version of the products straddle the middle category, and above the two is its brand, Premium Harvest, which retails at a price higher than some manufacturer brands.

Stickiness may also result from the manner in which retailers are positioning their brands. Future Group’s brand Ektaa will retail regional food and staples across its stores in the country so that migrants can buy supplies they are comfortable with. Be it Govindbhog rice and kasundi (a rice variety and mustard sauce preferred by Bengalis), khakra (Gujarati snack) or murukku (loved by Tamilians). Boston Consulting Group Partner & Director Abheek Singhi says, “Indian retailers are not cut-pasting private label products from other markets but adapting them.”

Are private labels a risk worth taking? Chakradeo says, “The entire product formulation for our cleaners was done in partnership with Dow Chemicals, USA. We did not make any investment and we gave them a percentage of sales as fee. Investments are not huge in making private labels as in most cases it is partnered with vendors. It is more of operating expenses than capital expenditure.”

Future Group brought down logistics costs further by 6-8 per cent by appointing vendors in more than one region for 10 of its product categories to fill its distribution centres. Chakradeo adds, “As the volumes go up, we will be able to put up for backend infrastructure facilities for development and R&D.”

Should national brands be worried? Devangshu Dutta says, “As long as retailers have access to the production and development and have customers for it, the private labels will remain profitable.” India Equity Partners Operating Partner V Sitaram sums up, “In modern trade, though the market leaders will face some slip in market share, the number 3 or 4 brands might have a bigger problem in certain categories thanks to private labels.”

As retailers leverage consumer insights to deploy private labels more effectively, national brands are aggressively fighting the challenge. From sprucing up supply chains to galvanising in-store promotions, they are covering all bases. KPMG Executive Director Ramesh Srinivas says, “Earlier brands had to adjust between a modern trade and a general trade supply chain. The former had to be serviced directly at the stores or had their own supply chain while the latter used the manufacturer’s supply chain. Now, some brands separate modern trade teams and even distributors.”

Britannia Category Director (delight and lifestyle) Shalini Degan says, “We have divided our portfolio into three categories, A,B,C, each having its benchmark fill-rate. We don’t allow fill-rates to drop below those levels. Why the segmentation? We need to focus on brands which have a higher traction in modern trade when servicing it, else we might end up focusing on brands that are not modern trade-led.”

Fill-rates denote how often and to what accuracy the retailer’s orders for a product are supplied by the manufacturer. Low fill-rates could mean lost opportunity since the shopper sees an empty shelf or a private label instead of the brand she might have thought of picking up.

Samsung Vice-President and Business Head (home appliances) Mahesh Krishnan says, “We have gone in for central billing system 4-5 months back with all large-format retailers. Orders are tracked on a daily basis giving retailers more control over the chain.”

In other words, private labels are here to stay and will evolve as more and more chains gain national footprint and the economies of scale kick in. Dutta of Third Eyesight says, “Gross margins for organised retailers are still low compared to global standards: So, margin fights will continue for some time till retailers gain a bigger share of the pie.”

(Also read: The Private Label Maturity Model.)