Devangshu Dutta

October 26, 2018

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

To many, retail seems to be having an identity crisis.

Closed storefronts on American and European streets and dead malls in India and China are blamed on the growth of online retail. At the same time, the world’s largest online retailer, Amazon, is opening physical stores and buying offline retail operations in the US and in India, while the world’s largest retailer, Walmart, is busy digesting India’s ecommerce market leader. Even India’s online fashion and lifestyle websites – among them Myntra, Firstcry, Yepme and Faballey – are acquiring offline brands or opening stores. Or both.

What in the world is going on?

The short answer: consumers want choice; and retailers have no choice.

For many, ecommerce still seems to have the “new car smell” after more than 20 years, the message pitched so desperately by the founders of and investors in ecommerce companies still echoing: that this “new kid” will make customers’ lives a quintillion times better and wipe out the competition. Two decades on, and hundreds of billions of dollars of investment later, online retail is estimated to be about 12% of the global market. Ecommerce is 10% of the US market, of which Amazon takes up about half. In India the figure is in the vicinity of 2%, with that share is virtually stitched up between Walmart-owned Flipkart Group and Amazon.

Clearly, consumers value offline retail stores, whether for convenience or as holistic brand ambassadors. You can’t take away the fact that retail for us is theatre, experience, social.

Over at physical retail businesses, managers have been terrified of “channel conflict”. Senior management have squeezed resources for online, even when return-on-capital was demonstrably better than a new store. Some have refused to publicise their own company’s website through in-store banners, fearing that the customers would get sucked away from the store. It has been strange to see this opportunity being passed up – if a customer is trusts you to walk into your physical store, why would you not want to connect with them at other points of time when they are not near your store?

As I’ve written earlier, retail is not and should not be divided between “old-world physical” and “upstart online”. Successful retailers and brands have always been able to integrate multiple channels and environments to reach their customers.

For instance, British fashion retailer Next has long used a combination of physical stores (of varying sizes) as well as mail order catalogue side-by-side, and then ecommerce as the digital medium grew. Another British retailer, Argos, took another angle and embedded a catalogue inside the physical store – first a paper catalogue, and then on-screen.

American designer Rebecca Minkoff has taken this unification further. Without the weight of legacy systems, the brand attempts to create a seamless experience for the customer, unifying the store, in-store digital interfaces such as smart dressing rooms, the website and the mobile.

No doubt, for older companies, integrating is tough; business systems and people are in disconnected silos, incentivised narrowly. Each channel needs different mindsets, capabilities, processes and systems, to ensure that the optimal customer experience appropriate for the interface, whether it is a store, mobile app, website or catalogue. But etailers opening physical stores have their own challenges, too, tackling the messy slowness of the physical world, where you can’t instantly switch the store layout after an A:B test. They now need to develop those very “old-world skills” and overheads that they thought they would never need.

Regardless of where they begin, retailers need to mould and blend their business models with proficiency across channels. In the evolving environment, any brand or retailer must aim to offer as seamless an experience to the customer as feasible, where the customer never feels disconnected from the brand.

Varying circumstances make customers choose different buying environments. At different times or on different days of the week, even the same person may choose to shop in entirely different ways. Successful retailers that outlast their competitors have used a variety of formats and channels to meet their customers, and will continue to do so.

To my mind, retailers have no choice but to see the retail business as one, even as it is fluid and evolving. A retailer’s only choice is to bend with the customer’s choice.

(Published in the Financial Express under the title “Uniting retail: Why online versus offline debate must end“)

Devangshu Dutta

September 28, 2017

In recent decades, the dependence on established medical disciplines has begun to be challenged. There is the oft-quoted dictum that healthcare sector tends to illness rather than health. Another saying goes that some of the food you eat keeps you in good health, but most of what you eat keeps your doctor in good health. With a gap emerging between wellness-seekers and the healthcare sector, so-called “alternative” options are stepping in.

Some of these alternatives actually existed as well-structured and well-documented traditional medical practices for thousands of years before the introduction of more recent Western medical disciplines. This includes India’s Siddha system and Ayurved (literally, “science of life”), which certainly don’t deserve being relegated to an “alternative” footnote. Ayurved is also said to have influenced medicine in China over a millennium ago, through the translation of Indian medical texts into Chinese.

Other than these, there are also more recent inventions riding the “wellness” buzzword. These may draw from the traditional systems and texts, or be built upon new pharmaceutical or nutraceutical formulations. Broader wellness regimens – much like Ayurved and Siddha – blend two or more elements from the following basket: food choices and restrictions, minerals, extracts and supplements, physical exercise and perhaps some form of meditative practices. Wellness, thus, is often characterised by a mix-and-match based on individual choices and conveniences, spiked with celebrity influences.

A key premise driving the wellness sector is that modern medicine depends too heavily on attacking specific issues with single chemicals (drugs) or combinations of single chemicals that are either isolated or synthesised in laboratories, and that it ignores the diversity and complexity of factors contributing to health and well-being. The second major premise for many wellness practitioners (though not all!) is that, provided the right conditions, the body can heal itself. For the consumer the reasons for the surge in demand for traditional wellness solutions include escalating costs of conventional health care, the adverse effects of allopathic drugs, and increasing lifestyle disorders.

After food, wellness has turned into possibly one of the largest consumer industries on the planet. Global pharmaceutical sales are estimated at over US$ 1.1 trillion. In contrast, according to the Global Wellness Institute, the wellness market dwarfs this, estimated at US$ 3.7 trillion (2015). This figure includes a vast range of services such as beauty and anti-ageing, nutrition and weight loss, wellness tourism, fitness and mind-body, preventative and personalized medicine, wellness lifestyle real estate, spa industry, thermal/mineral springs, and workplace wellness. Within this, the so-called “Complementary and Alternative Medicine” is estimated to be about US$200 billion.

There are several reasons why “complementary and alternative medicine” sales are not yet larger. Rooted in economically backward countries such as India, these have been seen as outdated, less effective and even unscientific. In India, the home of Siddha and Ayurved, apart from individual practitioners, several companies such as Baidyanath, Dabur, Himalaya and others were active in the market for decades, but were usually seen as stodgy and products of need, and usually limited to people of the older generations and rural populations. In the West they typically attracted a fringe customer base, or were a last resort for patients who did not find a solution for their specific problem in modern allopathy and hospitals.

However, through the 1970s Ayurved gained in prominence in the West, riding on the New Age movement. Gradually, in recent decades proponents turned to modern production techniques, slick packaging and up-to-date marketing, and even local cultivation in the West of medicinal plants taken from India.

As wellness demonstrated an increasingly profitable vector in the West, Indian entrepreneurs, too, have taken note of this opportunity. Perhaps Shahnaz Husain was one of the earliest movers in the beauty segment, followed by Biotique in the early-1990s that developed a brand driven not just by a specific need but by desire and an approach that was distinctly anti-commodity, the characteristics of any successful brand. Others followed, including FMCG companies such as the multinational giant Unilever. The last decade-and-a-half has also brought the phenomenon called Patanjali, a brand that began with Ayurvedic products and grew into an FMCG and packaged food-empire faster than any other brand before! While a few giants have emerged, the market is still evolving, allowing other brands to develop, whether as standalone names or as extensions of spiritual and holistic healing foundations, such as Sri Sri Tattva, Isha Arogya and others.

An absolutely critical driver of this growth in the Indian market now is the generation that has grown up during the last 25-30 years. It is a class that is driven by choice and modern consumerism, but that also wishes to reconnect with its spiritual and cultural roots. This group is aware of global trends but takes pride in home-grown successes. It is comfortable blending global branded sportswear with yoga or using an Indian ayurvedic treatment alongside an international beauty product.

Of course, there is a faddish dimension to the wellness phenomenon, and it is open to exploitation by poor or ineffective products, non-standard and unscientific treatments, entirely outrageous efficacy claims, and price-gouging.

To remain on course and strengthen, the wellness movement will need structured scientific assessment and development at a larger scale, a move that will need both industry and government to work closely together. Traditional texts would need to be recast in modern scientific frameworks, supported by robust testing and validation. Education needs to be strengthened, as does the use of technology.

However the industry and the government move, from the consumer’s point-of-view the juggernaut is now rolling.

(An edited version of this piece was published in Brand Wagon, Financial Express.)

Devangshu Dutta

January 10, 2017

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

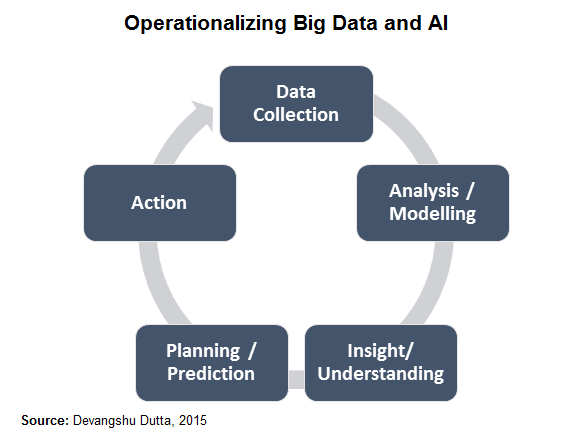

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

December 29, 2016

In 2016, brick-and-mortar modern retailers seemed to have begun recovering their confidence, and cautiously investing in expansion. However, currency shortage has significantly dampened demand at the end of the year. The hangover would continue into the first half of 2017, and consumers could be muted overall on discretionary purchases, including fashion, mobile upgrades and out-of-home dining.

On the other hand, while digital transactions introduce a note of caution (friction) in the consumer’s purchase decision, for e-tailers they do reduce complexity, cash-handling costs and potential returns which could provide significant unexpected wins.

I’ve written about this for years, and don’t tire of reiterating: the retail sector must recognise that shopping is a unified activity for the consumer; physical stores and non-store environments are alternative but complementary channels. Brands can and must use whatever channel mix works for them, and brick-and-mortar retailers need to invest in creating an integrated growth blueprint towards “unified commerce”.

On their part, while e-commerce companies are constrained by FDI policy, they will need to invest more in developing “old economy” strengths – strong product differentiation and distinguishable brands. Fashion, accessories, home decor and other lifestyle products are strong drivers of gross margin for all multi-product retailers, and e-commerce players struggling on the path to profit would focus on these even more, as well as on private labels. They also need to have management teams that are able to cast their minds 3-5 years into the future, while keeping close watch on immediate cash flows. Capital is available, but turning risk-averse. All businesses need to focus on up-skilling their teams, retaining good people, improving processes and adopting technology. In recent years, growth in the retail sector seems to have been driven by a “spray-and-pray” approach, not necessarily management sophistication. Spending like there’s no tomorrow is a sure way to no tomorrow.

In short, 2017 could be the year where the entire retail sector grows up – a lot. We hope.

(This piece was published in The Hindu – Businessline on 29 December 2016).

Devangshu Dutta

December 27, 2016

When American fast food standard bearers McDonald’s and Domino’s Pizza stepped into India in the mid-1990s, the market was just ripe enough for take-off.

McDonald’s and later Domino’s Pizza can be credited with not just growing the consumer appetite for fast food but also for fostering an entire food service ecosystem, including fresh produce, baked goods, sauces and condiments, and cold chain technology.

India has been typically difficult for business models driven by scale, replicability and predictability. The customer is price sensitive, operating costs are high and non-compliance of business standards is a frequent occurrence. In this environment, these brands have reinvented the meaning of meals, snacks and treats.

Their growth has set the stage for other international players and also set business aspirational standards for Indian food entrepreneurs and conglomerates alike.

Product experimentation has also been an important part of their success; it keeps excitement in the brand alive and help improve footfall. However, how far a product sustains and whether it becomes a menu staple can’t be predicted accurately. New products also need significant investment in both supply chain and front-of-house changes in standardisation-oriented QSRs, so the new product launch cannot be undertaken lightly. This is one reason these successful QSR formats don’t overhaul their menus drastically but make changes incrementally.

For these market leaders, future scale and deeper penetration is only feasible with higher visit frequency. For growth in middle-income India, they need to become a significantly cost-competitive option to be seen as more than a ‘treat’ or celebration destination.

So, while both McDonald’s and Domino’s Pizza have invested significantly in Indian flavours and menu offerings, perhaps it’s also best for them to reconcile with the fact that there will be a significant part of the consumer’s heart, stomach and wallet that will remain dedicated to indigenous offerings.

In a global environment that’s turning hostile to fast food, India isn’t a quick-fix growth market, but it’s certainly one to stay invested in, for the longer term.

And I have no doubt that as much as these companies aim to change India, over time India will also change them.

(Also published in Brand Wagon, The Financial Express)