admin

May 21, 2019

Written By Sangeeta Tanwar

Two of India’s leading retail chains are currently preparing the ground for their full-fledged e-commerce forays, albeit in totally different ways.

While the Kishore Biyani-led Future Group, which operates the popular Big Bazaar hypermarket chain, is busy listing its labels on Amazon, rival Reliance Retail is withdrawing its products from all e-commerce platforms, as parent Reliance Industries (RIL) gears up to launch its own online marketplace.

For both the traditional players, cracking online sales is important as they prepare for a future beyond high street retail.

Online sales in India will balloon from last year’s $18 billion (Rs1.25 lakh crore) to $170 billion by 2030, Jefferies India predicted recently. This potential aside, Indian e-commerce is still nascent and retailers are still perfecting their strategies.

“E-commerce is now a game of two dimensions, one of scale and the other of last-mile ubiquity. Whoever gets this right, will manage growth, revenue, and customer acquisition,” said Anil V Pillai, director of the independent marketing firm Terragni Consulting.

As for the Future Group, it thinks the best way to achieve this is by riding piggyback on Amazon’s proven capabilities in scale and last-mile delivery.

How the plan evolved

In 2016, the Future Group had made its first e-commerce acquisition by buying out the struggling furniture retailer FabFurnish from its German incubator Rocket Internet. Biyani had hoped to find synergies between the startup and his group’s furniture brand Hometown.

A year later, hit by heavy losses, FabFurnish was shuttered. Biyani downplayed the move saying his losses were “compensated” as the company had learnt “enough” from the episode.

The move now to partner Amazon seems to have stemmed from that learning.

Over the past month, the two have been trying to make joint plans, including in distribution, warehousing, and creating products for Amazon and its grocery format, Pantry. Also, Future group brands, including Big Bazaar, are being aligned with Amazon Now, which promises delivery of everyday essentials within two hours, suggest media reports.

A more serious handicap will be Amazon controlling Future Group’s data and customer relationships in the partnership. “In e-commerce, ownership of customer relationship and data, which offers consumer insights, is the real asset,” points out Devangshu Dutta, CEO of Third Eyesight, a consulting firm focussed on retail and consumer products.

Vianello agrees: “When you have your own e-commerce venture, as Reliance Retail plans, you are the owner of the data and you can slice and dice it to come up with exciting product offerings and improved service experience.”

This is one of the advantages that RIL might have seen in going it alone.

Going solo

“Reliance Retail has taken a more integrated approach towards e-commerce,” observed Dutta. “The company is set to leverage its pan-India retail presence and Reliance Jio’s (RIL’s telecom business) data capabilities to roll out an e-commerce platform,” explained Dutta.

The synergy between Reliance Jio and Reliance Retail is a big advantage. The retailer has about 10,000 stores across 6,500 towns in India, while Jio has a subscriber base of 306 million. After bringing many Indians online with Jio’s affordable data offerings, Reliance now hopes to get most of them to start shopping online as well.

The challenge, though, would be in getting the last-mile delivery right. “Reliance Retail could be at a disadvantage here compared to the Future Group, which has its delivery mechanism in place courtesy its partnership with Amazon,” suggested Vianello.

Moreover, like with Jio, consumers will expect heavy discounts from Reliance’s e-commerce venture as well, which may be difficult to sustain given the initial investments. “Biyani’s (online) launch involves lower upfront costs, while Reliance Retail’s will be resource hungry since it’s an almost greenfield project,” pointed out Pillai, adding, “Reliance’s challenge is the overwhelming perception about the group being a price warrior and disrupter.”

So, which strategy will triumph? Everything comes down to execution. “Success in retail, including e-commerce, is about more and more customers choosing to transact with you repeatedly. Achieving this is a difficult and ongoing process. There are no guaranteed or permanent winners,” says Dutta.

Source: qz

Devangshu Dutta

December 20, 2018

Do you have this feeling that 2018 went by a little too quickly? Well, however quick it seemed, it was certainly momentous for retail in India.

If 2016 was marked by the shock of demonetization, and 2017 by the pains of GST implementation, 2018 highlighted two threads – the obvious convergence of the online and offline world that had been ignored for far too long, and the interest of foreign capital in India’s consumer world.

Walmart bought India’s loss-making ecommerce leader for an eye-popping US$ 20.8 billion valuation, while ecommerce giant Amazon injecting equity into Shoppers Stop, bought Aditya Birla’s More grocery chain (49 per cent through a back-end entity), and held discussions with Future Group to acquire 9.5 per cent in Future Retail. There were rumours of a mega joint venture between Reliance Retail and China’s Alibaba, and media also reported Japan’s Softbank looking at ploughing US$200 million into Firstcry. Both rivals Amazon and Alibaba were reported to be looking at Spencer’s, one of India’s oldest retail chains currently owned by the RP-Sanjiv Goenka group.

Videos of the crush of curious crowds at India’s first, much anticipated Ikea went viral, and the company said it planned to open 40 locations over the next few years, upping its earlier projection of 25. Chinese retailer Miniso basically came out of nowhere and claimed to have clocked sales of ?700 crores in the very first year in the country.

But along with these cross-border “big bangs” we saw domestic confidence also quietly resurging. Indian retailers are not cowering before large foreign retailers and expensive ecommerce advertising splashes; today they are less defensive about their own prospects than they were two years ago. There is also a growing interest among entrepreneurs and corporates to create new retail businesses, which augers well for the diversity of competition and freshness of offerings in the market.

Going into 2019, one thing I can say with certainty is that the weather, economic and political – both in India and elsewhere – will be unpredictable, and might even turn stormy. Externally, retailers should “expect the unexpected”. To ensure that the business remains on track, however rough the track becomes, retailers must centre all major strategies and decisions on the customer. A theme that has been around for centuries, it is surprising how much it gets ignored in this most customer-facing business.

Retailers tend to divide customers into rigid segments. My suggestion would be to look at customers through the behaviour and experience lens and also recognise that the same customer behaves differently at different times and in different contexts – in effect there are no hard boundaries between “segments”.

It is often emphasised is that Indian consumers are “deal-seeking”. I don’t think we should treat this as a uniquely Indian thing: all consumers look for value-reassurance in unpredictable times and in uncertain conditions. Also remember that even in value-seeking, experience still rules. Retailers and brands that are solely focussing on price or price+feature comparisons are turning their business into a commodity. They are missing the long game: of defining the customer’s experience from the first moment of brand contact to the purchase and beyond.

In 2019, if you want to focus on a single competitive strategy, it would be this: for stickiness and sustainability, think about the customer’s experience, and actively design it, in every environment where the customer connects with you.

Lastly, technology is transformative, but tends to get restricted to being the contrast between ecommerce and physical retail. Indian retailers need to embrace technology in all forms, from using the zillions of transactions within the business and with the customer for developing actionable knowledge, to automating processes where unnecessary cost or time makes the business inefficient.

Having said that, keep the previous rule in mind when deploying at customer-facing technology – make customer-interfacing technology as invisible or intuitive as possible. When in doubt, learn from one of the leaders in the sector, Amazon: its 1-click ordering patent 20 years ago gave it a huge advantage over competitors, and it is now aiming to replicate the same seamless, friction-free behaviour physically with its Dash button. Or pick cues even from younger fashion businesses like Rebecca Minkoff, whose focus is on ease and convenience. The key reason for adopting technology is to remove friction for the customer and for processes that serve the customer.

I have no doubt that 2019 will be eventful – let the customer experience be the guiding light to keep our businesses off the rocks and afloat.

(Published in the Financial Express on 4 January 2019, under the title “Retail in 2019: Need for stronger brand-customer connections that go beyond purchase“)

Devangshu Dutta

October 26, 2018

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

To many, retail seems to be having an identity crisis.

Closed storefronts on American and European streets and dead malls in India and China are blamed on the growth of online retail. At the same time, the world’s largest online retailer, Amazon, is opening physical stores and buying offline retail operations in the US and in India, while the world’s largest retailer, Walmart, is busy digesting India’s ecommerce market leader. Even India’s online fashion and lifestyle websites – among them Myntra, Firstcry, Yepme and Faballey – are acquiring offline brands or opening stores. Or both.

What in the world is going on?

The short answer: consumers want choice; and retailers have no choice.

For many, ecommerce still seems to have the “new car smell” after more than 20 years, the message pitched so desperately by the founders of and investors in ecommerce companies still echoing: that this “new kid” will make customers’ lives a quintillion times better and wipe out the competition. Two decades on, and hundreds of billions of dollars of investment later, online retail is estimated to be about 12% of the global market. Ecommerce is 10% of the US market, of which Amazon takes up about half. In India the figure is in the vicinity of 2%, with that share is virtually stitched up between Walmart-owned Flipkart Group and Amazon.

Clearly, consumers value offline retail stores, whether for convenience or as holistic brand ambassadors. You can’t take away the fact that retail for us is theatre, experience, social.

Over at physical retail businesses, managers have been terrified of “channel conflict”. Senior management have squeezed resources for online, even when return-on-capital was demonstrably better than a new store. Some have refused to publicise their own company’s website through in-store banners, fearing that the customers would get sucked away from the store. It has been strange to see this opportunity being passed up – if a customer is trusts you to walk into your physical store, why would you not want to connect with them at other points of time when they are not near your store?

As I’ve written earlier, retail is not and should not be divided between “old-world physical” and “upstart online”. Successful retailers and brands have always been able to integrate multiple channels and environments to reach their customers.

For instance, British fashion retailer Next has long used a combination of physical stores (of varying sizes) as well as mail order catalogue side-by-side, and then ecommerce as the digital medium grew. Another British retailer, Argos, took another angle and embedded a catalogue inside the physical store – first a paper catalogue, and then on-screen.

American designer Rebecca Minkoff has taken this unification further. Without the weight of legacy systems, the brand attempts to create a seamless experience for the customer, unifying the store, in-store digital interfaces such as smart dressing rooms, the website and the mobile.

No doubt, for older companies, integrating is tough; business systems and people are in disconnected silos, incentivised narrowly. Each channel needs different mindsets, capabilities, processes and systems, to ensure that the optimal customer experience appropriate for the interface, whether it is a store, mobile app, website or catalogue. But etailers opening physical stores have their own challenges, too, tackling the messy slowness of the physical world, where you can’t instantly switch the store layout after an A:B test. They now need to develop those very “old-world skills” and overheads that they thought they would never need.

Regardless of where they begin, retailers need to mould and blend their business models with proficiency across channels. In the evolving environment, any brand or retailer must aim to offer as seamless an experience to the customer as feasible, where the customer never feels disconnected from the brand.

Varying circumstances make customers choose different buying environments. At different times or on different days of the week, even the same person may choose to shop in entirely different ways. Successful retailers that outlast their competitors have used a variety of formats and channels to meet their customers, and will continue to do so.

To my mind, retailers have no choice but to see the retail business as one, even as it is fluid and evolving. A retailer’s only choice is to bend with the customer’s choice.

(Published in the Financial Express under the title “Uniting retail: Why online versus offline debate must end“)

Devangshu Dutta

January 10, 2017

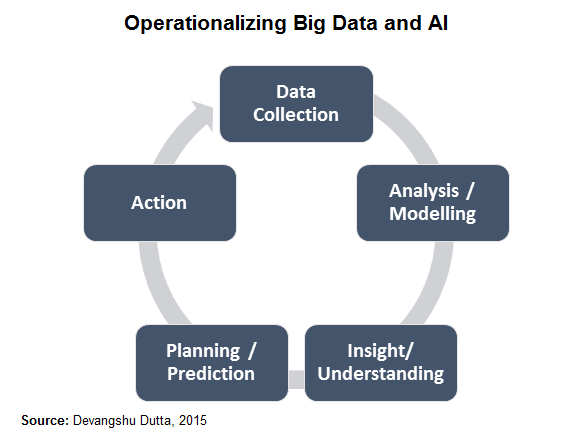

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

December 29, 2016

In 2016, brick-and-mortar modern retailers seemed to have begun recovering their confidence, and cautiously investing in expansion. However, currency shortage has significantly dampened demand at the end of the year. The hangover would continue into the first half of 2017, and consumers could be muted overall on discretionary purchases, including fashion, mobile upgrades and out-of-home dining.

On the other hand, while digital transactions introduce a note of caution (friction) in the consumer’s purchase decision, for e-tailers they do reduce complexity, cash-handling costs and potential returns which could provide significant unexpected wins.

I’ve written about this for years, and don’t tire of reiterating: the retail sector must recognise that shopping is a unified activity for the consumer; physical stores and non-store environments are alternative but complementary channels. Brands can and must use whatever channel mix works for them, and brick-and-mortar retailers need to invest in creating an integrated growth blueprint towards “unified commerce”.

On their part, while e-commerce companies are constrained by FDI policy, they will need to invest more in developing “old economy” strengths – strong product differentiation and distinguishable brands. Fashion, accessories, home decor and other lifestyle products are strong drivers of gross margin for all multi-product retailers, and e-commerce players struggling on the path to profit would focus on these even more, as well as on private labels. They also need to have management teams that are able to cast their minds 3-5 years into the future, while keeping close watch on immediate cash flows. Capital is available, but turning risk-averse. All businesses need to focus on up-skilling their teams, retaining good people, improving processes and adopting technology. In recent years, growth in the retail sector seems to have been driven by a “spray-and-pray” approach, not necessarily management sophistication. Spending like there’s no tomorrow is a sure way to no tomorrow.

In short, 2017 could be the year where the entire retail sector grows up – a lot. We hope.

(This piece was published in The Hindu – Businessline on 29 December 2016).