admin

October 26, 2023

Sagar Malviya, Economic Times

26 October 2023

Surging demand for fitness wear and sports equipment for disciplines other than cricket and football helped Decathlon’s India unit expand sales 37% to Rs 3,955 crore in FY23. With more than 100 large, warehouse-like stores selling products catering to 85 sporting disciplines, the French company is bigger than Adidas, Nike and Asics all put together in India.

In FY22, sales were Rs 2,936 crore, according to its latest filings with the Registrar of Companies. The retailer, however, posted a net loss of Rs 18.6 crore during the year ended March 2023 compared to a net profit of Rs 36 crore a year ago.

Experts said a host of factors – from pricing products about 30-40% lower than competing products to selling everything from running shoes, athleisure wear to mountaineering equipment under its own brands – has worked in its favour. “They have an extremely powerful format across different sporting activities and have something for both active and casual wear shoppers. For them, the market is still under penetrated with the kind of comprehensive product range they sell for outdoor sports beyond shoes and clothing,” said Devangshu Dutta, founder of retail consulting firm Third Eyesight. “Even their front end staff seem to have a strong domain knowledge about products compared to rival brands.”

By selling only private labels, Decathlon, the world’s biggest sporting goods firm, controls almost every bit of operations, from pricing and design to distribution, and keeps costs and selling prices low.

Decathlon uses a combination of in-house manufacturing and outsourcing to stock its shelves. In fact, it sources nearly 15% of its global requirement from India across sporting goods. And nearly all of its cricket merchandise sold globally is designed and made in India.

(Published in Economic Times)

admin

August 28, 2023

Viveat Susan Pinto, Financial Express

August 28, 2023

Coffee Day Global, which operates the Cafe Coffee Day (CCD) chain, has been given a temporary relief against bankruptcy proceedings initiated by lender IndusInd Bank last month. The Chennai bench of the National Company Law Tribunal (NCLAT) last week halted admission of IndusInd Bank’s plea against Coffee Day Global, a subsidiary of the listed Coffee Day Enterprises (CDEL), by the NCLT Bengaluru, till September 20.

What this means for CCD is that it get some more time at a time when it has swung into the black after struggling for the last few years, since the tragic demise of its founder VG Siddhartha in 2019. Coffee Day Global posted a net profit of Rs 24.57 crore for the June quarter of 2023-24 (FY24) versus a net loss of Rs 11.73 crore reported in the same period last year.

Revenue from operations stood at Rs 223.20 crore in the quarter under review, a growth of nearly 18% versus the year-ago period, CDEL results for Coffee Day Global showed.

More importantly, CCD outlets are down to 467 in the June quarter of FY24 from a peak of 1,752 stores in FY19, indicating that the company is shutting down unprofitable operations as it looks to manage its debt and other expenses. Group debt is down to Rs 1,711 crore, according to its latest annual report for FY23, versus Rs 7,214 crore reported in FY19.

“While the coffee retail market in India is growing, in CCD‘s case the need to downsize has to do with internal issues. Sometimes a smaller footprint just helps to manage operations better especially when you are dealing with larger problems such as a debt overhang,” says Devangshu Dutta, chief executive officer of retail consultancy Third Eyesight.

CCD’s financial health is critical for CDEL, which derives close to 94% of its group turnover from the coffee retail business, according to its FY23 annual report. In FY22, the contribution of the coffee retail business to group turnover was 85%. Losses of Coffee Day Global in FY23 narrowed to Rs 69.62 crore from Rs 112.48 crore in FY22. In FY19, the company had a net profit of Rs 10 crore.

Apart from cafes, CCD also has kiosks and vending machines installed in corporate offices, institutions and business hubs. While the number of kiosks has fallen over the last few years and is at around 265 now from a peak of 537 in FY19, the number of vending machines have been growing after briefly slowing down over the last few years. From a peak of 58,697 crore in FY20, it is now at 50,870 in number, the company’s latest results show.

CCD is also expected to fight the insolvency proceedings against it aggressively, according to industry sources. IndusInd Bank has claimed that Coffee Day Global defaulted on a loan of Rs 94 crore, which occurred on February 28, 2020. The company has disputed this in court.

(Published in Financial Express)

admin

June 29, 2023

Raghavendra Kamath, Financial Express

June 29, 2023

Zara, touted as “Fast Fashion Queen”, has achieved a unique feat in India. The Spanish brand has been growing its revenues without opening any new stores.

The fashion brand, run by a joint venture between Tata-owned Trent and Spain’s retail group Inditex, posted a 40.7% growth in its revenues to Rs 2553.8 crore in FY23. The catch is that while many retailers/brands garner sales from opening new stores, Zara did not open any store but closed one during FY23.

In FY21 and FY22, its store count remained constant at 21 but its revenue grew 61.2% in FY22. Zara’s revenues grew at a 15.5 % CAGR in the last five years.

“Zara did not foray into any new city and closed one store. That said, it saw an exceptional performance on store productivity (83% higher than FY19). The increase in revenues lead to highest ever Ebitda margins at 16.3%,” said Nuvama Institutional Equities in a recent report.

The contribution in productivity includes contribution from online and also increase in store sizes, the brokerage said.

A mail sent to Inditex did not elicit any response. Trent executives could not be contacted.

Experts attribute Zara’s success to increase in customer spends and improved offerings by the brand.

“The customer base they are targeting has grown and their merchandise mix has become sharper,” said Devangshu Dutta, chief executive officer at Third Eyesight, a retail consultant.

Dutta said when a retailer opens stores, it would immediately boost sales, but to maintain sales momentum, one has to have “right merchandise at right price and have stores at right locations”.

Zara is known to churn its designs and styles very fast, and target young customers. In its Indian venture also, its parent Inditex controls merchandise mix and so on.

“The said entities (Zara and Massimo Dutti) are obliged to source merchandise only from the Inditex Group. Also, the choice of product & related specifications are at the latter’s discretion. Further, the entities are dependent on Inditex for permissions to use the said brands in India subject to its terms & specifications,” Trent said in its FY23 annual report.

Zara is also focusing on opening in select locations, a reason it could not open more stores in the country, experts said.

“The incremental store openings for Zara continue to be calibrated with focus on presence only in very high-quality retail spaces,” Trent said.

Susil Dungarwal, founder at Beyond Squarefeet, a mall management firm, said that propensity to spend has gone up among Indian shoppers after the pandemic and Zara being a renowned global brand with its stylish merchandise seems to be have been the beneficiary of the trend.

“They understand customers very well and brought products which are liked by Indian shoppers in terms of looks, styles and so on,” Dungarwal said.

Zara is a case study for Indian brands as to how to run a retail business successfully, he said.

(Published in Financial Express)

admin

December 20, 2021

Written By Vaishnavi Gupta

The furniture brand’s retail roadmap includes city stores in Delhi, Mumbai and Bengaluru, followed by tier I and II towns

For the Ikea model to succeed, adequate demand-concentration is crucial, which is being currently provided by the bigger cities in India.

After launching two large-format stores in India in a span of three years — one each in Hyderabad and Navi Mumbai — Ikea opened its first small-format store in Worli, Mumbai, to become “more accessible and convenient”. About 90,000 sq ft in size, these ‘city’ stores are already present in markets such as New York, London, Paris, Moscow and Shanghai.

The furniture market in India stood at $17.77 billion in 2020, and is expected to reach $37.72 billion by 2026, growing at a CAGR of 13.37%, according to a Research and Markets report. Godrej Interio, UrbanLadder and Pepperfry are among the big players in this space, all with a significant online presence, too. Godrej Interio has 300 exclusive stores in India, while Pepperfry has more than 110 Studios.

Spread across three floors, Ikea’s first city store has 9,000 products in focus, of which 2,200 are available for takeaway and the rest for home delivery. “We have observed that it is not easy to find large retail locations in cities like Mumbai and Bengaluru. The small store offers convenience and accessibility for consumers to experience Ikea products,” says Per Hornell, area manager and country expansion manager, Ikea India. This launch is in line with the company’s aim to become accessible to 200 million homes in India by 2025, and 500 million homes by 2030.

More launches are being planned: another city store in Mumbai in the spring of 2022 and a large-format store as well as a city store in Bengaluru by the end of 2022. For its retail expansion in Maharashtra, the company plans to invest Rs 6,000 crore by 2030. “We are on track to exceed the investment commitment of Rs 10,500 crore made for India in December last year,” adds Hornell. Delhi, Mumbai and Bengaluru are the three cities on its radar at the moment, which will be followed by tier I and II towns.

Furthermore, Ingka Centres, part of Ingka Group that includes Ikea Retail, is coming up with its first shopping centre in Gurugram (followed by Noida), which will be integrated with an Ikea store.

In India, unlike its organised furniture market competitors, Ikea doesn’t have a pan-India online presence yet. It has been following a “cluster-based expansion strategy” for its online offering, but the company insists this is not a limitation. “At present, 30% of our overall India sales come from online channels,” Hornell informs. Through its e-commerce website and mobile shopping app, the company currently operates in Hyderabad, Mumbai, Pune, Bengaluru, Surat, Ahmedabad and Vadodara.

On the other hand, players like Godrej Interio and Pepperfry have big plans to tap new markets. The former aims to add 50 exclusive stores each year, while Pepperfry aims to achieve the 200 Studios mark by March 2022. In September this year, Pepperfry forayed into the customised furniture segment with the Pepperfry Modular offering, which focusses on modular kitchens, wardrobes and entertainment units.

Good start?

This is a good time for Ikea to establish its presence in the Indian market, says Alagu Balaraman, CEO, Augmented SCM. “Earlier, people used to rely on carpenters for furnishing their homes; now, they prefer to buy ready-made furniture. The market is moving towards acceptability, making plenty of headroom for growth for these companies,” he says.

Ikea’s cautious expansion approach in a market like India where several local dynamics are at play, is tactful, analysts say. Devangshu Dutta, founder, Third Eyesight, says, “In the past, Western businesses have made the mistake of simply copy-pasting formats and strategies in emerging markets from their more developed markets.” He believes there is “nothing wrong” in being incremental while growing footprint. “There’s no sense in carpet-bombing the market with stores, when many may end up being loss-making or sub-optimal,” he adds.

Getting the product mix and pricing right would be key in realising the full potential of this market. Balaraman says Ikea will have to balance its global portfolio with what it is doing locally, and make sure it is profitable.

For the Ikea model to succeed, adequate demand-concentration is crucial, which is being currently provided by the bigger cities in India. Given its global popularity, the furniture giant, analysts say, is poised to see traction in the metros and tier I cities.

Source: financialexpress

Devangshu Dutta

January 10, 2017

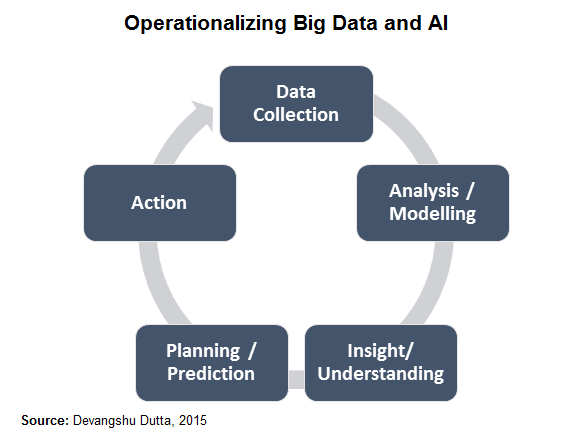

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)