admin

August 28, 2023

Viveat Susan Pinto, Financial Express

August 28, 2023

Coffee Day Global, which operates the Cafe Coffee Day (CCD) chain, has been given a temporary relief against bankruptcy proceedings initiated by lender IndusInd Bank last month. The Chennai bench of the National Company Law Tribunal (NCLAT) last week halted admission of IndusInd Bank’s plea against Coffee Day Global, a subsidiary of the listed Coffee Day Enterprises (CDEL), by the NCLT Bengaluru, till September 20.

What this means for CCD is that it get some more time at a time when it has swung into the black after struggling for the last few years, since the tragic demise of its founder VG Siddhartha in 2019. Coffee Day Global posted a net profit of Rs 24.57 crore for the June quarter of 2023-24 (FY24) versus a net loss of Rs 11.73 crore reported in the same period last year.

Revenue from operations stood at Rs 223.20 crore in the quarter under review, a growth of nearly 18% versus the year-ago period, CDEL results for Coffee Day Global showed.

More importantly, CCD outlets are down to 467 in the June quarter of FY24 from a peak of 1,752 stores in FY19, indicating that the company is shutting down unprofitable operations as it looks to manage its debt and other expenses. Group debt is down to Rs 1,711 crore, according to its latest annual report for FY23, versus Rs 7,214 crore reported in FY19.

“While the coffee retail market in India is growing, in CCD‘s case the need to downsize has to do with internal issues. Sometimes a smaller footprint just helps to manage operations better especially when you are dealing with larger problems such as a debt overhang,” says Devangshu Dutta, chief executive officer of retail consultancy Third Eyesight.

CCD’s financial health is critical for CDEL, which derives close to 94% of its group turnover from the coffee retail business, according to its FY23 annual report. In FY22, the contribution of the coffee retail business to group turnover was 85%. Losses of Coffee Day Global in FY23 narrowed to Rs 69.62 crore from Rs 112.48 crore in FY22. In FY19, the company had a net profit of Rs 10 crore.

Apart from cafes, CCD also has kiosks and vending machines installed in corporate offices, institutions and business hubs. While the number of kiosks has fallen over the last few years and is at around 265 now from a peak of 537 in FY19, the number of vending machines have been growing after briefly slowing down over the last few years. From a peak of 58,697 crore in FY20, it is now at 50,870 in number, the company’s latest results show.

CCD is also expected to fight the insolvency proceedings against it aggressively, according to industry sources. IndusInd Bank has claimed that Coffee Day Global defaulted on a loan of Rs 94 crore, which occurred on February 28, 2020. The company has disputed this in court.

(Published in Financial Express)

Devangshu Dutta

January 10, 2017

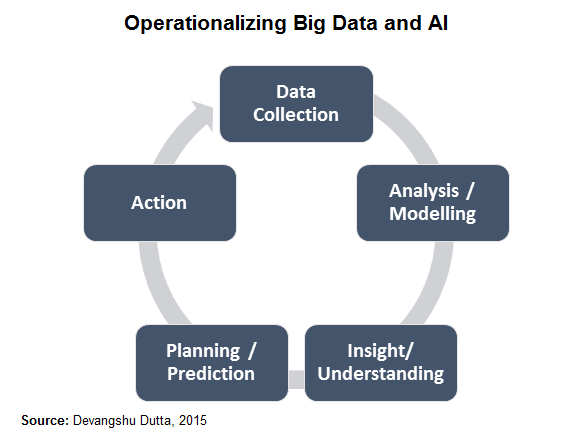

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

admin

February 21, 2016

![]() Shinmin

Bali, Financial Express

Shinmin

Bali, Financial Express

![]() Mumbai,

21 February 2016

Mumbai,

21 February 2016

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

TinyOwl last year was in the news for a poorly-handled downsizing

operation in Pune, with a dramatic hostage situation involving

its co-founder Gaurav Choudhary. PepperTap also recently shut

down operations in six cities.

Ironically, giants like Amazon have not only aggressively entered

the hyperlocal space, they are building on it. Amazon is currently

offering the service in Bengaluru, Amazon Now, after running a

pilot project, Kirana Now, in 2015.

The investor sentiment in India is also on a decline, as was

reported earlier this year. Investments by venture capitalists

have dropped from $2.12 billion (October-December 2014) to $1.15

billion (October-December 2015), according to a report by CB Insights

and KPMG International. This leaves an even shorter window of

opportunity for players to retain investor interest.

Albinder Dhindsa, co-founder, Grofers, states that differing

levels of technology literacy among the majority of merchants

and consumer adaptation to the online platform are concern areas

for the company. In 2016, the company is looking to bring over

one lakh merchants aboard and ensure that turnaround time stays

under an hour. Grofers delivers more than 35,000 orders per day

on average. In Q4 2015, the firm acquired teams of SpoonJoy and

Townrush to bring dynamic learning to the table.

For Swiggy’s co-founder Nandan Reddy, the focus is currently

to grow the market, while catering to a wide demographic of consumers.

He admits that in the early stages, the brand had trouble educating

even its partners. Furthermore, operating a delivery fleet in

an on-demand service offering sub-40 minute deliveries is a challenging

task, given that there are at least 15 points of failure in an

average order. Swiggy currently owns a delivery fleet of 3,800

delivery executives. The brand’s repeat consumers contribute

to over 80% of orders.

Debadutta Upadhyaya, co-founder, Timesaverz, says some of the

major challenges in a hyperlocal market are optimum resource utilisation

and matching locations, price points, and other specific requirements

to customer needs. Timesaverz currently has a service range spread

across 40 categories, aided by a network of over 2,500 service

partners across five metros. Its revenue model is commission based,

where 80% of earnings from consumers are shared with service partners.

Vinod Murali, MD, Innoven Capital, points out that as the hyperlocal

industry is in its nascent stages, it needs a fair amount of time

to grow. “One aspect to keep in mind is that a large sized

equity cheque does not imply that a company has achieved operational

maturity or robust business metrics, especially in this segment,”

he notes.

Given the recent consolidation in this category, the survivors

have the opportunity and time to focus on improving unit economics

and demonstrate that their businesses are viable and valuable.

Devangshu Dutta, CEO, Third Eyesight, is of the opinion that

hyperlocals make the mistake of borrowing business models and

terminologies from Silicon Valley, without adequately understanding

the real context of the Indian market. “Is there an existing

or even potential demand for the service claimed to be provided?

Or are you just going to introduce an intermediary and an additional

link in the chain, with additional costs and unnecessary administration

involved?” he asks.

(Published in Financial Express)

admin

September 8, 2015

![]() Devina

Joshi, Financial Express

Devina

Joshi, Financial Express

![]() Mumbai,

8 September 2015

Mumbai,

8 September 2015

Recently,

there was news of restaurant reservation site EazyDiner expanding

operations to Mumbai from the National Capital Region, having

secured Series A funding worth $3 million led by existing investor

DSG Consumer Partners, and Saamna Capital.

Recently,

there was news of restaurant reservation site EazyDiner expanding

operations to Mumbai from the National Capital Region, having

secured Series A funding worth $3 million led by existing investor

DSG Consumer Partners, and Saamna Capital.

As per a PwC analyst, investors have pumped more than $150 million

into companies like Grofers, TinyOwl, Swiggy, LocalOye, Spoonjoy,

Zimmber and HolaChef, among others. Judging by the patronage showered

upon them by customers and investors alike, it would appear that

hyperlocal start-ups are all set to create the next big boom in

the Indian retail sector. But is it really all that rosy? Probably

not, as can be amply witnessed by acquisitions taking place in

the nascent yet already overcrowded market.

Between November 2014 and February 2015, the Rocket Internet-backed

Foodpanda acquired rivals TastyKhana and JustEat.in, and is rumoured

to be in acquisition mode with TinyOwl. Restaurant search app

Zomato, which recently got into the food ordering space, is also

reportedly looking to acquire minority stakes in food-ordering

firms.

While investors are attracted to hyperlocal start-ups, controlling

logistics well is key to sustained growth for these businesses

— all of these will definitely go through a constraint in

the supply of delivery boys, for example. In India, organising

fragmented labour is a challenge and, hence, a services-based

hyperlocal needs to figure out the mechanics of human capital

even more than a traditional, product-based e-commerce firm.

For services, another challenge is customer stickiness. If a

user uses an app to obtain the services of a plumber, for example,

he may not go through the app to contact the plumber next time

if his services are found satisfactory. Discounting can induce

trials, but just like in any other business, prove fatal in the

long run. Like what led to the end of HomeJoy in the US —

excessive discounts to dissuade direct contact between servicemen

and customers.

Even for product-based start-ups, maintaining data quality is

a big hurdle as stock and prices may not be updated by retailers

in real time, making it difficult to track offline sales.

Since the game is hyperlocal, you need to be physically present

in the city to bring retailers aboard. For that, you need a city

team. Other challenges include retailer verification and assessment,

given that hyperlocals deal with small city retailers.

Stickiness is needed on both sides, and each locality will certainly evolve into having a market leader and a follower, with other players falling far behind. “So the critical success factor for a hyperlocal is being able to rapidly create a viable model in each location it targets, and then—to build overall scale and continued attractiveness for investors—quickly move on to replicate the model in another location, and then another,” says retail consultant Devangshu Dutta of Third Eyesight. As they do that, they will become potential acquisition targets for larger ecommerce companies, which could use acquisition to not only take out potential competition but also to imbibe the learning and capabilities needed to deal with microcosms of consumer demand.

(Published in Financial Express.)

Devangshu Dutta

December 5, 2013

(Published in ETRetail.com on 6 December 2013)

Franchising isn’t rocket science, but advanced space programmes offer at least one parallel which we can learn from – the staging of objectives and planning accordingly.

A franchise development programme can be staged like a space launch, each successive stage being designed and defined for a specific function or role, and sequentially building the needed velocity and direction to successfully create a franchise operation. The stages may be equated to Launch, Booster, Orbiter and Landing stages, and cover the following aspects:

Stage 1: Launch

The first and perhaps the most important stage in launching a franchise programme is to check whether the organisation is really ready to create a franchise network. Sure, inept franchisees can cause damage to the brand, but it is important to first look at the responsibilities that a brand has to making the franchise network a success. Too many brands see franchising as a quick-fix for expansion, as a low-cost source for capital and manpower at the expense of franchisee-investors. It is vital for the franchiser to demonstrate that it has a successful and profitable business model, as well as the ability to provide support to a network of multiple operating locations in diverse geographies. For this, it has to have put in place management resources (people with the appropriate skills, business processes, financial and information systems) as well as budgets to provide the support the franchisee needs to succeed. The failure of many franchise concepts, in fact, lies in weakness within the franchiser’s organisation rather than outside.

Stage 2: Booster

Once the organisation and the brand are assessed to be “franchise-ready”, there is still work to be put into two sets of documents: one related to the brand and the second related to the operations processes and systems. A comprehensive marketing reference manual needs to be in place to be able to convey the “pulling” power that the brand will provide to the franchisee, clearly articulate the tangible and intangible aspects that comprise the brand, and also specify the guidelines for usage of brand materials in various marketing environments. The operations manual aims to document standard operating procedures that provide consistency across the franchise network and are aimed at reducing variability in customer experience and performance. It must be noted that both sets of documents must be seen as evolving with growth of the business and with changes in the external environment – the Marketing Manual is likely to be more stable, while the Operations Manual necessary needs to be as dynamic as the internal and external environment.

Stage 3: Orbiter

Now the brand is ready to reach out to potential franchisees. How wide a brand reaches, across how many potential franchisees, with what sort of terms, all depend on the vision of the brand, its business plan and the practices prevalent in the market. However, in all cases, it is essential to adopt a “parent” framework that defines the essential and desirable characteristics that a franchisee should possess, the relationship structure that needs to be consistent across markets (if that is the case), and any commercial terms about which the franchiser wishes to be rigid. This would allow clearer direction and focussed efforts on the part of the franchiser, and filter out proposals that do not fit the franchiser’s requirements. Franchisees can be connected through a variety of means: some will find you through other franchisees, or through your website or other marketing materials; others you might reach out to yourselves through marketing outreach programmes, trade shows, or through business partners. During all of this it is useful, perhaps essential, to create a single point of responsibility at a senior level in the organisation to be able to maintain both consistency and flexibility during the franchise recruitment and negotiation process, through to the stage where a franchisee is signed-on.

Stage 4: Landing

Congratulations – the destination is in sight. The search might have been hard, the negotiations harder still, but you now – officially – have a partner who has agreed to put in their money and their efforts behind launching YOUR brand in THEIR market, and to even pay you for the period that they would be running the business under your name. That’s a big commitment on the franchisee’s part. The commitment with which the franchiser handles this stage is important, because this is where the foundation will be laid for the success – or failure – of the franchisee’s business. Other than a general orientation that you need to start you franchisee off with, the Marketing Manual and the Operational Manual are essential tools during the training process for the franchisee’s team. Depending on the complexity of the business and the infrastructure available with the franchiser, the franchisee’s team may be first trained at the franchiser’s location, followed by pre-launch training at the franchisee’s own location, and that may be augmented by active operational support for a certain period provided by the franchiser’s staff at the franchisee’s site. The duration and the amount of support are best determined by the nature of the business and the relative maturity of both parties in the relationship. For instance, someone picking up a food service franchise without any prior experience in the industry is certainly likely to need more training and support than a franchisee who is already successfully running other food service locations.

Will going through these steps guarantee that the franchise location or the franchise network succeeds? Perhaps not. But at the very least the framework will provide much more direction and clarity to your business, and will improve the chances of its success. And it’s a whole lot better than flapping around unpredictably during the heat of negotiations with high-energy franchisees in high-potential markets.