Devangshu Dutta

April 7, 2020

Oil shocks, financial market crashes, localised wars and even medical emergencies like SARS pale when compared to the speed and the scale of the mayhem created by SARS-CoV-2. In recent decades the world has become far more interconnected through travel and trade, so the viral disease – medical and economic – now spreads faster than ever. Airlines carrying business and leisure-travellers have also quickly carried the virus. Businesses benefitting from lower costs and global scale are today infected deeply due to the concentration of manufacturing and trade.

A common defensive action worldwide is the lock-down of cities to slow community transmission (something that, ironically, the World Health Organization was denying as late as mid-January). The Indian government implemented a full-scale 3-week national lockdown from March 25. The suddenness of this decision took most businesses by surprise, but quick action to ensure physical distancing was critical.

Clearly consumer businesses are hit hard. If we stay home, many “needs” disappear; among them entertainment, eating out, and buying products related to socializing. Even grocery shopping drops; when you’re not strolling through the supermarket, the attention is focussed on “needs”, not “wants”. A travel ban means no sales at airport and railway kiosks, but also no commute to the airport and station which, in turn means that the businesses that support taxi drivers’ daily needs are hit.

Responses vary, but cash is king! US retailers have wrangled aid and tax breaks of potentially hundreds of billions of dollars, as part of a US$2 trillion stimulus. A British retailer is filing for administration to avoid threats of legal action, and has asked landlords for a 5-month retail holiday. Several western apparel retailers are cancelling orders, even with plaintive appeals from supplier countries such as Bangladesh and India. In India, large corporate retailers are negotiating rental waivers for the lockdown period or longer. Many retailers are bloated with excess inventory and, with lost weeks of sales, have started cancelling orders with their suppliers citing “force majeure”. Marketing spends have been hit. (As an aside, will “viral marketing” ever be the same?)

On the upside are interesting collaborations and shifts emerging. In the USA, Jo-Ann Stores is supplying fabric and materials to be made up into masks and hospital gowns at retailer Nieman Marcus’ alteration facilities. LVMH is converting its French cosmetics factories into hand sanitizer production units for hospitals, and American distilleries are giving away their alcohol-based solutions. In India, hospitality groups are providing quarantine facilities at their empty hotels. Zomato and Swiggy are partnering to deliver orders booked by both online and offline retailers, who are also partnering between themselves, in an unprecedented wave of coopetition. Ecommerce and home delivery models are getting a totally unexpected boost due to quarantine conditions.

Life-after-lockdown won’t go back to “normal”. People will remain concerned about physical exposure and are unlikely to want to spend long periods of time in crowds, so entertainment venues and restaurants will suffer for several weeks or months even after restrictions are lifted, as will malls and large-format stores where families can spend long periods of time.

The second major concern will be income-insecurity for a large portion of the consuming population. The frequency and value of discretionary purchases – offline and online – will remain subdued for months including entertainment, eating-out and ordering-in, fashion, home and lifestyle products, electronics and durables.

The saving grace is that for a large portion of India, the Dusshera-Deepavali season and weddings provide a huge boost, and that could still float some boats in the second half of this year. Health and wellness related products and services would also benefit, at least in the short term. So 2020 may not be a complete washout.

So, what now?

Retailers and suppliers both need to start seriously questioning whether they are valuable to their customer or a replaceable commodity, and crystallise the value proposition: what is it that the customer values, and why? Business expansion, rationalised in 2009-10, had also started going haywire recently. It is again time to focus on product line viability and store productivity, and be clear-minded about the units to be retained.

Someone once said, never let a good crisis be wasted.

This is a historical turning point. It should be a time of reflection, reinvention, rejuvenation. It would be a shame if we fail to use it to create new life-patterns, social constructs, business models and economic paradigms.

(This article was published in the Financial Express under the headline “As Consumer businesses take a hard hit, time for retailers to reflect and reinvent”.

Devangshu Dutta

December 17, 2019

Remember the year 2000? After Y2K passed safely, that year some optimistic analysts predicted that India’s modern retail chains would reach 20 per cent market share by 2015. Two years after that supposed watershed, another firm declared that modern retail will be at around that level in 2020 – but wait! – only in the top 9 cities in the country. Don’t hold your breath: India surprises; constantly. As many have noted, “predictions are tough, especially about the future!” What we can do is reflect on some of this year’s developments that could play out over the coming year.

In many minds 2019 may be the Year of the Recession, plagued by discounting, but that demand slowdown has brewing for some time now. However, there’s another under-appreciated factor that has been playing out: while small, independent retailers can flex their business investments with variations in demand, modern retail chains need to spread the business throughout the year in order to meet fixed expenses and to manage margins more consistently.

To reduce dependence on festive demand, retailers like Big Bazaar and Reliance have been inventing shopping events like Sabse Sasta Din (Cheapest Day), Sabse Sachi Sale (Most Authentic Sale), Republic Day / 3-Day sale, Independence Day shopping and more for the last few years. In ecommerce, there’s the Amazon’s Freedom Sale, Prime Day, and Great India Festival, and Flipkart’s Big Billion Day Sale. This year retailers and brands went overboard with Black Friday sale, a shopping-event concept from the 1950s in the USA linked to a harvest celebration marked by European colonisers of North America. (The fact that Black Friday has a totally different connotation in India since the terrorist bombings in Bombay in 1993 seems to have completely escaped the attention of brands, retailers and advertising agencies.) Be that as it may, we can only expect more such invented and imported events to pepper the retail calendar, to drive footfall and sales. The consumer has been successfully converted to a value-seeking man-eater fed on a diet of deals and discounts. With no big-bang economic stimuli domestically and a sputtering global economy, we should just get used to the idea of not fireworks but slow-burning oil lamps and sprinklings of flowers and colour through the year. Retailers will just have to work that much harder to keep the lamps from sputtering.

Ecommerce companies have been in operating for 20 years now, but the Indian consumer still mostly prefers a hands-on experience. The lack of trust is a huge factor, built on the back of inconsistency of products and services. The one segment that has been receiving a lot of love, attention and money this year (and will grow in 2020) is food and grocery, since it is the largest chunk of the consumption basket. Beyond the incumbents – Grofers, Big Basket, MilkBasket and the likes – now Walmart-Flipkart and Amazon are going hard at it, and Reliance has also jumped in. Remember, though, that selling groceries online is as old as the first dot-com boom in India. E-grocers still struggle to create a habit among their customers that would give them regular and remunerative transactions, and they also need to tackle supply-side challenges. Average transactions remain small, demand remains fragmented, and supply chain issues continue to be troublesome. Most e-grocers are ending up depending on a relatively narrow band of consumers in a handful of cities. The generation that is comfortable with an ever-present screen is not yet large enough to tilt the scales towards non-store shopping and convenience isn’t the biggest driver for the rest, so, for a while it’ll remain a bumpy, painful, unprofitable road.

Where we will see rapid pick-up is social commerce, both in terms of referral networks as well as using social networks to create niche entrepreneurial businesses – 2020 should be a good year for social commerce, including a mix of online platforms, social media apps as well as offline community markets. However, western or East Asia models won’t be replicated as the Indian market is significantly lower in average incomes, and way more fragmented.

As a closing thought, I’ll mention a sector that I’ve been involved with (for far too long): fashion. In the last 8-10 decades, globally fashion has become an industry living off artificially-generated expiry dates. A challenge that I have extended to many in the industry, and this year publicly at a conference: if consumption falls to half in the next five years, and you still have to run a profitable business (obviously!), how would you do it? Plenty of clues lie in India – we epitomise the future consumers; frugal, value-seeking, wanting the latest and the best but not fearful about missing out the newest design, because it will just be there a few weeks later at a discount. If you can crack that customer base and turn a profit, you would be well set for the next decade or so.

(Published as a year-end perspective in the Financial Express.)

admin

May 27, 2019

(The following is the video and the text of the Commencement Speech by Devangshu Dutta, chief executive of Third Eyesight, at the Convocation of the batch graduating in 2019 from the National Institute of Fashion Technology, Patna, India.)

I would like to just share a few learnings from my own career. I hope some of these learnings will provide you some food for thought, and if they stick, I hope they prove valuable to you in some way in your own career.

I think as a graduate of a professional institute, there are 5 life-skills or attributes or pieces of advice that could be useful to you.

Thank you so much for patiently hearing me out. I hope some of the advice would have resonated with you, and will prove useful. I wish you all the very best and offer you my congratulations, on behalf of all the other alumni – welcome to the industry. Thank you!

Devangshu Dutta

September 28, 2017

In recent decades, the dependence on established medical disciplines has begun to be challenged. There is the oft-quoted dictum that healthcare sector tends to illness rather than health. Another saying goes that some of the food you eat keeps you in good health, but most of what you eat keeps your doctor in good health. With a gap emerging between wellness-seekers and the healthcare sector, so-called “alternative” options are stepping in.

Some of these alternatives actually existed as well-structured and well-documented traditional medical practices for thousands of years before the introduction of more recent Western medical disciplines. This includes India’s Siddha system and Ayurved (literally, “science of life”), which certainly don’t deserve being relegated to an “alternative” footnote. Ayurved is also said to have influenced medicine in China over a millennium ago, through the translation of Indian medical texts into Chinese.

Other than these, there are also more recent inventions riding the “wellness” buzzword. These may draw from the traditional systems and texts, or be built upon new pharmaceutical or nutraceutical formulations. Broader wellness regimens – much like Ayurved and Siddha – blend two or more elements from the following basket: food choices and restrictions, minerals, extracts and supplements, physical exercise and perhaps some form of meditative practices. Wellness, thus, is often characterised by a mix-and-match based on individual choices and conveniences, spiked with celebrity influences.

A key premise driving the wellness sector is that modern medicine depends too heavily on attacking specific issues with single chemicals (drugs) or combinations of single chemicals that are either isolated or synthesised in laboratories, and that it ignores the diversity and complexity of factors contributing to health and well-being. The second major premise for many wellness practitioners (though not all!) is that, provided the right conditions, the body can heal itself. For the consumer the reasons for the surge in demand for traditional wellness solutions include escalating costs of conventional health care, the adverse effects of allopathic drugs, and increasing lifestyle disorders.

After food, wellness has turned into possibly one of the largest consumer industries on the planet. Global pharmaceutical sales are estimated at over US$ 1.1 trillion. In contrast, according to the Global Wellness Institute, the wellness market dwarfs this, estimated at US$ 3.7 trillion (2015). This figure includes a vast range of services such as beauty and anti-ageing, nutrition and weight loss, wellness tourism, fitness and mind-body, preventative and personalized medicine, wellness lifestyle real estate, spa industry, thermal/mineral springs, and workplace wellness. Within this, the so-called “Complementary and Alternative Medicine” is estimated to be about US$200 billion.

There are several reasons why “complementary and alternative medicine” sales are not yet larger. Rooted in economically backward countries such as India, these have been seen as outdated, less effective and even unscientific. In India, the home of Siddha and Ayurved, apart from individual practitioners, several companies such as Baidyanath, Dabur, Himalaya and others were active in the market for decades, but were usually seen as stodgy and products of need, and usually limited to people of the older generations and rural populations. In the West they typically attracted a fringe customer base, or were a last resort for patients who did not find a solution for their specific problem in modern allopathy and hospitals.

However, through the 1970s Ayurved gained in prominence in the West, riding on the New Age movement. Gradually, in recent decades proponents turned to modern production techniques, slick packaging and up-to-date marketing, and even local cultivation in the West of medicinal plants taken from India.

As wellness demonstrated an increasingly profitable vector in the West, Indian entrepreneurs, too, have taken note of this opportunity. Perhaps Shahnaz Husain was one of the earliest movers in the beauty segment, followed by Biotique in the early-1990s that developed a brand driven not just by a specific need but by desire and an approach that was distinctly anti-commodity, the characteristics of any successful brand. Others followed, including FMCG companies such as the multinational giant Unilever. The last decade-and-a-half has also brought the phenomenon called Patanjali, a brand that began with Ayurvedic products and grew into an FMCG and packaged food-empire faster than any other brand before! While a few giants have emerged, the market is still evolving, allowing other brands to develop, whether as standalone names or as extensions of spiritual and holistic healing foundations, such as Sri Sri Tattva, Isha Arogya and others.

An absolutely critical driver of this growth in the Indian market now is the generation that has grown up during the last 25-30 years. It is a class that is driven by choice and modern consumerism, but that also wishes to reconnect with its spiritual and cultural roots. This group is aware of global trends but takes pride in home-grown successes. It is comfortable blending global branded sportswear with yoga or using an Indian ayurvedic treatment alongside an international beauty product.

Of course, there is a faddish dimension to the wellness phenomenon, and it is open to exploitation by poor or ineffective products, non-standard and unscientific treatments, entirely outrageous efficacy claims, and price-gouging.

To remain on course and strengthen, the wellness movement will need structured scientific assessment and development at a larger scale, a move that will need both industry and government to work closely together. Traditional texts would need to be recast in modern scientific frameworks, supported by robust testing and validation. Education needs to be strengthened, as does the use of technology.

However the industry and the government move, from the consumer’s point-of-view the juggernaut is now rolling.

(An edited version of this piece was published in Brand Wagon, Financial Express.)

Devangshu Dutta

January 10, 2017

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

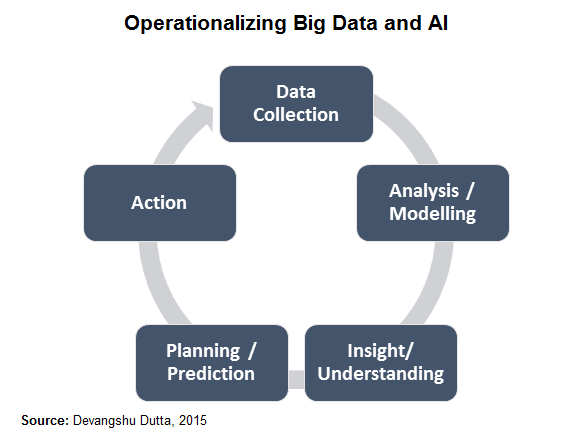

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)