Tarang Gautam Saxena

February 14, 2014

2013 has been a mixed year for retail in the Indian market with multiple factors working in favour of and against the business prospects.

Economic growth had slowed to 5% for 2012-13 (as per advance estimates by The Central Statistics Office, Government of India), down from 9.3% in 2011. The ray of hope is that the growth rate is expected to rebound to 6.8% in 2013-14. Spiralling inflation, with prices of some basic vegetables shooting up almost eight to ten times, distracted the consumers from discretionary spending. The year hardly saw irrational expansions by retail businesses as they primarily focused on bottom line performance.

While the Government of India liberalised Foreign Direct Investment (FDI) policy in retail in September 2012, international investors have been slow to respond and sizeable foreign investments have been announced only recently at the end of 2013.

The political environment also took unexpected turn with the success of Aam Aadmi Party (AAP) at the Delhi Assembly Elections held towards the end of the year. This may augur in a new era of politics driven by performance and results but in the short term it could restrict market access for international multi-brand retailers, as the AAP has declared their opposition to investment from foreign multi-brand retailers.

So is India still a strategic market for international fashion brands to look at?

FDI Policy – Clarifications and Impact

India’s Foreign Direct Investment (FDI) policy has come a long way with foreign investments now being allowed in multiple sectors including retail, telecom, aviation, defence and so on. The Indian government is now exploring the possibility of allowing FDI in sectors such as railways and construction.

The year 2006 was a significant year for international brands in fashion and lifestyle space as the Government of India allowed up to 51 per cent foreign direct investment in the newly-defined category of “Single Brand retail”. In September 2012 the Indian Government liberalised the retail FDI policy to allow foreign investment up to 100 per cent in single brand operations and up to 51 per cent in multi-brand retail albeit with certain conditions related to the ownership of the brand, mandatory domestic sourcing norms for both single-brand and multi-brand retailers and additionally certain investment parameters for the backend operations of the multi-brand retail business. The idea was to attract foreign investment in retail trading a part of which could flow into improving the supply chain while providing Indian businesses access to global designs, technologies and management practices.

Large Investments in the Pipeline

The investments flowed in slowly initially. Some of these have looked at converting existing operations, such as Decathlon Sports which was present in India through a 100% owned subsidiary in cash and carry business. The brand is converting its cash and carry business in India to fully-owned single brand retailing business.

But there have been some significant moves as well. A record breaking FDI proposal in single brand retail is the Swedish furniture brand IKEA’s, that had to apply three times since December 2012 before its’ proposed investment of €1.5 billion (Rs. 101 billion) received the nod from the Government. However, the proposal is reportedly still in the works, as Ikea looks to structure the business to comply with the laws of the land. And as the year came to a close the Government cleared Swedish clothing brand Hennes and Mauritz’s (H&M) US$ 115 million (Rs.7.2 billion) investment proposal. According to news reports the brand had already begun blocking real estate with the goal of launching its stores in India at the soonest.

While the initial response to the relaxation of FDI policy spelt positive inflow for single brand retail, there was no new investment forthcoming in multi-brand retail. The existing foreign multi-brand retailers present in India through the cash and carry format showed a marked lack of interest in switching to a retail business model. On the other hand Walmart, the only foreign multi-brand retailer having access to a network of retail stores through its wholesale joint venture Indian partner, Bharti Enterprises Ltd., ended its five year long relationship and has restricted itself to the wholesale business. Though the company cited that it was disheartened by complicated regulations, it was also caught up in its own corruption investigation as well as allegations that it had violated foreign investment norms. The sole bright spot was the world’s fourth largest global retailer Tesco proposing and getting approval for a US$ 115 million investment into the multi-brand retail business of its partner, the Tata Group. At the time of writing the precise scope of this investment remains unclear.

If you want the full paper please send us an email with your full name, company name and designation to services[at]thirdeyesight[dot]in.

admin

May 17, 2013

Organised by the Retailers Association of India the Delhi Retail Summit this year (10 May 2013) focussed on multi-fold growth for retailers utilising multiple channels to the consumer, with panel discussions and presentations by industry leaders who shared their experiences in exploiting the opportunities and dealing with the strategic and operational challenges of their varied businesses. Some snippets from the first panel discussion, comprising of the following panelists:

1. Devangshu Dutta, Chief Executive, Third Eyesight (Session Moderator)

2. Atul Ahuja, Vice President – Retail, Apollo Pharmacy

3. Lalit Agarwal, CMD, V-Mart Retail Ltd.

4. Atul Chand, Chief Executive, ITC Lifestyle

5. Rahul Chadha, Executive Director & CEO, Religare Wellness Ltd.

admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

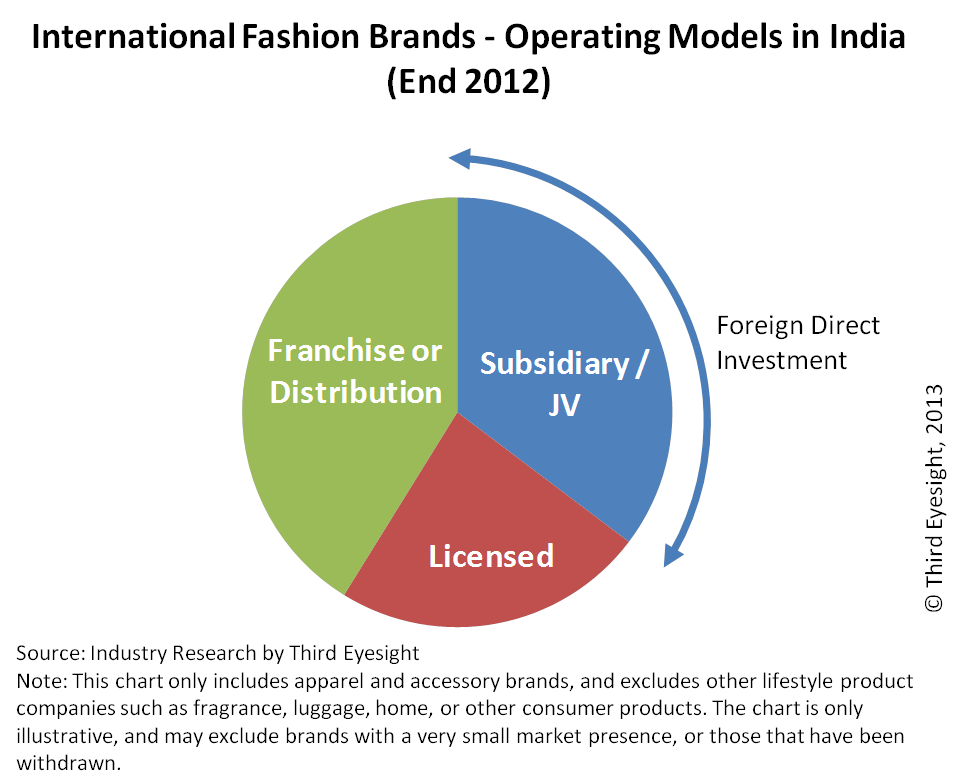

Routes to Market – The Evolution

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.

Tarang Gautam Saxena

February 1, 2012

As the debate over FDI (even for single brand retail) continues, over 250 international brands in the food service and fashion and lifestyle sectors alone continue to service the Indian consumers. Interestingly more than half of them are present in the Indian market through the franchising route.

Franchising has been a preferred entry strategy especially in case of the food service sector. Many of the international food brands have opted to give the master franchise to an Indian partner who can use the international brand’s name but is responsible for sourcing the ingredients and maintaining the international quality standards for food and service. One such example is Dominos, which incidentally is also the country’s largest international food service brand. Of course, as FDI liberalisation seems nearer the finish line, brands such as Starbucks are choosing to join hands with an Indian partner while others such as Denny’s Corp are planning to tie up with regional licensees.

In case of the fashion sector, in the early years of liberalisation few international companies chose franchising. Instead some chose licensing to gain a quick access to the Indian market at a minimal investment. Others set up wholly owned subsidiaries or entered into majority-owned joint ventures to have a greater control over their Indian business operations, product sourcing and supply chain and brand marketing.

However, at the turn of the last decade, many international fashion brands chose franchising owing to favourable business environment. An environment conducive for growth of franchising was created by reduction in import duties under WTO agreements, the absence of a wide network of multi-brand retail platforms, the need for using exclusive branded outlets as a marketing tool to create a full brand experience and the simultaneous growth of real estate investors who were potential master franchises ready to invest capital and real estate.

The question is how the liberalisation of FDI norms will impact the choice of market entry strategy for the international brands. Would franchising continue to remain the preferred entry mode as we set into the liberalised FDI regime? The change in foreign investment norms has already led to some brands (in particular those in the fashion and lifestyle sector) transitioning their existing licensing or franchise partnership into a joint venture or wholly owned subsidiary while the new entrants are actively considering ownership routes rather than franchising.

Certainly, the ideal scenario for an international brand would be to have complete ownership and control over the operations in a strategic market like India, but direct investment does also increase their risk and the investment is not financial alone. Amongst other choices licensing offers the least control, and while joint venture may be preferable for some brands, for many franchising still proves to be the practical choice for some time to come.

Franchising may potentially be quicker way to launch with higher chances of the retail business being successful. As it is an “entrepreneurship” model of business, the franchisee’s motivation to make the venture a success is high. The international brand has an assured income by way of royalty on the license agreement and could expand more rapidly in the market. Having a local partner with a closer understanding of the market and the ability to adapt to the changing needs of the consumers also helps to ensure that the international brand’s offering is tuned in to consumers’ demand.

Further, unlike more developed markets where brands have sizable networks of large-format store as a launch and growth platform, in India there are still limited choices to simply “plug-and-play” using department stores or any other large-format retail network. Partnering with a franchisee who has access to retail real estate can be a quick way to reach the target consumers. On his part the franchisor needs to ensure that the business model is well thought through in terms of the team and infrastructure required and is scalable.

For a successful relationship it is vital that the franchisee has an entrepreneurial mind-set. The essence of the brand needs be well understood, and the franchisee must have operational involvement rather than a “passive investment” approach.

If both partners understand their respective responsibilities, franchising can truly be a win-win business model.

Devangshu Dutta

January 6, 2012

The transition between calendar years offers a pause. We can use it to evaluate what passed in the previous year, chalk out our journey for the next one.

The transition between calendar years offers a pause. We can use it to evaluate what passed in the previous year, chalk out our journey for the next one.

The first response of most people to the question “What happened in the Indian retail sector in 2011” would be probably something like this: lots happened, and then – at the end – nothing did!

That is because one theme ran through the entire year, month after month, fuelled by tremendous interest in the mainstream media as well. This was about the change expected, hoped for, in the policy governing foreign direct investment (FDI) into the retail sector. Hearing the debate go back and forth, on one side it seemed as if FDI was going to cure every ill of the Indian economy, and on the other it seemed as if the country was being sold out to neo-colonists.

It’s worth remembering that not too long ago foreigners could invest in retail businesses in India freely. Benetton ran some of the key locations in the network through its joint-venture which subsequently became a 100 per cent owned subsidiary. Littlewoods (UK) set up a 100 per cent owned operation in India during the 1990s before its home market business collapsed, and its Indian operation was bought by the Tata Group to form Westside. And well before all these, one of the early multi-nationals, Bata, had already built a humongous network of stores across the length, breadth and depth of India.

The motivation for the decision to exclude foreigners from this sector may have been political, economic or mixed – that is not as important as the timing.

By the mid-90s India had just started to attract interest as private consumption was just about picking up steam. Several international apparel, sportswear and quick service brands entered the market during this time. Many of these brands started setting up processes and systems that changed the way the supply chain worked. They gained market share, and more importantly mindshare, with young consumers. In this process some of the domestic brands did suffer, some of them irrecoverably. However, with foreign investment suddenly blocked-off, many brands that wanted direct ownership in the business in India turned away. In their opinion the opportunity just wasn’t big enough to take on the hassle of a partner. Some did enter, but with wholesale distribution structures rather than in retail.

During this last decade, the Indian retail landscape has changed dramatically. During the 2000s the economic boom happened and India became “hot” again. So did retail and real estate, as large corporate houses pumped in significant amounts of capital into setting up modern chains to tap into the fattening consumer wallets. Clearly, FDI was going to come up on the agenda again, but not quite at once. Indian companies needed some headroom to grow; and grow they did, partly with indigenous business models and brands, and partly as partners to international brands.

By 2011, there was more of a clear consensus among the Indian businesses that retail could be opened to FDI and must be. Internationally, too, political and economic heavy-weights from the significant western economies pitched for opening up the retail sector in India to foreign investment. Here’s the small public glimpse of the hectic activity that happened internationally and domestically:

Such an anticlimax! For many, 2011 was the year that could have been a turning point. Could have been! If you had slept through the year and woken up on New Year’s Eve, would you have found nothing had really changed?

Ah, that’s the thing! I think most people observing the retail business actually slept through the year, because they were just focused on the FDI dream. Those actually engaged in the retail business know that many other things did change, some of which create the foundation for further growth.

The government did push on with the GST (goods and services tax) agenda. While stuck in politics at the moment, we look forward to incremental changes in harmonizing the taxes and tariffs regime, vital for truly unifying the country in the economic sense. On the downside, excise being levied on the retail price of clothing was a blow to retailers.

Growth continued. Indian’s retail giant, Future Group, grew to around 15 million square feet. The other giant, Reliance, announced renewed vigour and focus on the retail business with additions to the management team partnerships with international brands such as Kenneth Cole, Quiksilver and Roxy. Other new partnerships were announced, including significant American food service brands Starbucks (with the Tata Group) and Dunkin’ Donuts (with Jubilant). The British footwear brand Clark’s announced that it was aiming to make India its second-largest source country and among its top-5 markets within 5 years. Marks & Spencer pushed to expand its chain by more than 50 per cent, adding 10 stores to 19, while Walmart said its focus was on building scale rather than trying to squeeze profitability from its US$ 40 million investment so far. For fashion brands, the Rs 500 crores (US$ 100 million) sales threshold seemed more achievable as they used the accelerated pace of growth.

Many in the retail business talk about “the people problem”. Fortunately, some decided to demonstrate positive leadership, reflected in RAI’s announcement of an ambitious skill development plan for 5 million people in next 4-5 years, and industry veteran BS Nagesh announcing the launch of a non-profit venture, TRRAIN.

There was some bad news on the issue of shrinkage: a sponsored study placed India at the top of the list of countries suffering from theft. But the level was reported to be lower than the previous study, so there seemed to be hope on the horizon. The study didn’t say whether consumers and employees had become more honest, better security systems were preventing theft, or whether retailers themselves had become better at counting and managing merchandise over time.

A significant highlight was the e-commerce sector, which has found its way to grow within the existing restrictions and regulations, even as the online population is estimated to have grown to 100 million. Flipkart delighted customers with its service and racked up Rs. 50 crores (US$ 10 million) in sales. Deal sites proliferated and media channels celebrated the advertising budgets. Even offline businesses, notable among them pizza-major Domino’s, found their online mojo; Domino’s reported 10 per cent of its total revenues from online bookings within a year of launching the service.

In all of this the biggest story remains untold, which is why I call it an Invisible Revolution. This revolution is made up of the changes that are happening in the supply chain in the entire country, including investment by private companies in massive, large and small facilities to store, move and process products more efficiently. And in spite of the high costs of capital, suppliers are continuing to look at investing in upgrading their production facilities as well as their systems and processes. While the companies at the front-end will no doubt get a lot of the credit for modernizing India’s retail sector, it would be impossible without the support of the foundation that is being built by their suppliers and service providers.

2011 seems to have ended with a whimper. 2012’s beginning will be tainted by large piles of leftover inventory that needs to be cleared. Inflation seems tamer, but consumers have already tightened their belts, anticipating difficult times. The policy flip-flops and the political debates are sustaining the air of uncertainty. So what does 2012 hold?

Remember, the ancient Mayan calendar stops in December 2012, and no doubt there are many predicting doomsday! However, there are several others that see this as a possibility of rejuvenation, renewal.

Hope and fear are both fuel for taking action. Investment cycles are caused by an imbalance of one over the other.

In 2012, we’ll probably continue to see a mix of both. I recommend that we don’t take an overdose of any one of them. Even if you think 2011 was “the year that could have been”, I suggest still treating 2012 as “the year that could be”.

Here’s wishing you a successful New Year!