admin

May 9, 2009

By Devangshu Dutta, Tarang Gautam Saxena

While the Indian consumers have aspired to own international fashion brands, India’s large population base in turn has been an aspirational market for the international companies.

To remote observers, the Indian market may appear to be a virgin territory as far as international apparel and footwear brands are concerned. But India has seen the presence of international brands for almost a century, including mass brands such as Bata and luxury brands such as Louis Vuitton. However, as the colonial government systematically repressed local textile production, the local resistance to foreign products grew as well. Therefore, until the 1980s, the presence of international fashion brands was negligible.

In the early 1990s, as the Indian economy opened up again, a few international fashion brands entered the Indian market. The pioneering companies during this stage were Benetton, Coats Viyella and VF Corporation.

At this time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment which was thus a target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike).

In the midst of this the media industry was also witnessing a high growth which aided the international brands in gaining visibility and establishing brand equity in the Indian market.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. A growing supply of good-quality retail real estate in the form of shopping centers and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores and shops-in-shop.

The number of international brands continued to grow each year at a steady pace until the early 2000s, and took off exponentially thereafter. By 2005 the number of international fashion brands present in India was over three times compared to that in the mid 1990s. The last few years (since 2005) have continued the significant growth of international fashion brands, including luxury brands such as LVMH, Aigner, Tommy Hilfiger and Chanel.

The Popular Entry Strategies

Many of the international companies entering India in the late 1980s and 1990s chose licensing as the entry route to India to gain a quick access to the Indian market at a minimal investment.

A few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand.

In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought investors in retail real estate that were ideal franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in “Single Brand” retail). Using this route, many brands have entered India by setting up majority owned joint ventures, or transitioned their existing franchise arrangements into a joint venture structure.

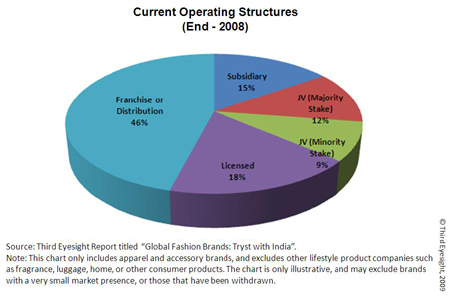

The Entry Structure for Some International Brands

| Entry Strategy | Time Period | ||

| 1980s or Earlier | 1990s | Post-1999 | |

| Licensed | Louis Philippe, United Colors of Benetton and 012, Wrangler | Allen Solly, Arrow, Jockey, Lacoste, Lee, Nike, Van Heusen, Vanity Fair | Puma |

| Wholly Owned Subsidiary | Bata, Pepe Jeans | Levi’s® | Hanes, Triumph |

| Joint Venture (Majority) | Adidas, Reebok | Diesel, Nautica, Sixty Group | |

| Franchise or Distribution | Aldo, Burberry, Canali, Versace, Debenhams, Esprit, Gucci, Guess, Hugo Boss, Mango, Marks & Spencer, Mothercare, Tommy Hilfiger | ||

| Joint Venture (incl. Minority Stake) | Celio, Etam, Giordano | ||

Source: “Global Fashion Brands: Tryst with India” (A Report by Third Eyesight) © Third Eyesight, 2009

Note: The above table shows the structure used during entry, and not the structure that exists currently.

By the end of 2008, just under half of the brands were present through a franchise or distribution relationship, while over a quarter had either a wholly-owned or majority-owned subsidiary. These structures allowed the brands to have greater control of operations, particularly of product.

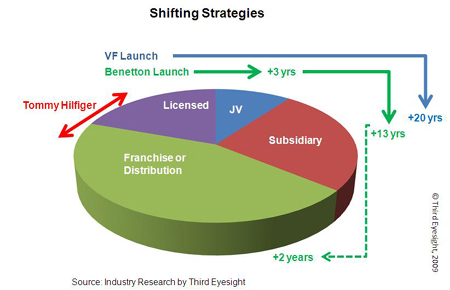

Shifting Strategies

Many international companies have evolved their presence in India into structures different from those at the time they entered the market.

A good example depicting the shift in business strategy is that of VF Corporation which entered India in 1980s by assigning the Wrangler license to Dupont Sportswear. Since then it has launched a variety of brands in different product categories with number of Indian partners and finally formed a joint venture, VF Arvind Brands Pvt. Ltd., with Arvind Brands.

Another example of a company that has evolved its presence is Benetton, which first entered India through a licensee (Dalmia). Benetton then transitioned in 1991 into 50:50 joint-venture and finally in 2004 took over the Indian business completely. However, it adopted the franchising route in 2006 for its premium fashion brand, Sisley, appointing Trent (a Tata Group company) as the national retail franchisee.

Many other companies such as Nike, Tommy Hilfiger, Marks & Spencer and Pierre Cardin (as described in our report “Global Fashion Brands: Tryst with India”) have changed their approach as the original structures did not perform as well as they had expected.

Obviously, each such change has cost the brands time, management effort, money and, sometimes, market share.

We believe that these shifts and the pain related to it could have been reduced, had the brands ruthlessly questioned the motivation for considering this market and their expectations from the market in determining an appropriate strategy.

What’s Ahead?

In the midst of economic upheaval around the world, how does India look as a market for international fashion brands?

Well, it is difficult to generalize even in the best of times. In the current global turmoil there is certainly a lot more unpredictability about international expansion for most companies.

Although India’s position as a target market for international brands has been improving, as is evident from the number of launches in the last 6-7 years, some companies considering international expansion may prefer entering other markets that may seem more “familiar”, developed and safe (such as Europe, Japan, South Korea or Taiwan). Against such comparisons, India’s growing but fragmented market can seem chaotic and difficult to deal with.

However, the fact remains that there are very few markets globally that can provide the sustained size of mid-term and long-term opportunity that India does. We are already seeing the more far-sighted and committed brands consolidating their position and presence in the market by continuing to look at expansion, even while examining how they can make their existing points of sale perform better. We also constantly come across new companies carrying out investigations into the market.

In the current environment we expect to see a shift in the nature of launch vehicle. While franchising seems to be a safe option for risk-averse brands in the current times, we will probably see more brands with a long term strategy, who would establish a controlled presence either through joint-ventures or through wholly-owned subsidiaries, since they can lay the foundation of the business today at much lower costs today than in the past few years.

India’s foreign direct investment (FDI) policy, allowing FDI only up to 51% in retail trading of “Single Brand” may have held back some fashion brands as they are still managed by owner founder with a conservative outlook on “control”. However, in the last couple of years, we have found companies not being deterred by the barriers to FDI.

As their comfort and familiarity with India has grown, international companies are more willing today to create corporate structures that allow them a presence in the market today and a step-through to a more controlling stake as and when government regulations allow.

All in all, we feel that international brands are in India not only to stay, but also to expand. There is yet a lot of potential untapped in the market, and as the integration of the Indian consumer with global trends continues, international brands can expect to find India an increasingly fertile ground for growth.

(c) 2009, Third Eyesight

Devangshu Dutta

March 13, 2009

The Indian consumer market remains one of the most attractive and sustainable markets for international companies. It has even been described as a market of a lifetime by some, meaning that a brand can live through a whole lifecycle of decades if it launches in the market today. The last decade has made the Indian consumer even more visible and desirable to consumer goods companies from around the world.

So it is hardly surprising that many international food and beverage brands have entered the market in the last few years, either by appointing wholesalers as their distributors in the market or, occasionally, establishing a more direct presence through joint ventures or subsidiaries.

These companies have been helped along by the growth of modern retail chains. These offer a familiar sales environment to most of these companies who sell through supermarket and hypermarket chains in other countries.

However, the market presents international brands and their distributors with two challenges.

First, the question whether they should stick to only selling through the more “organised” retail chains. If they do so, they could focus commercially on a limited number of larger business accounts, and service them efficiently as they do the large retailers in other markets. It would also provide them – in the Indian context – an upmarket environment where the display and promotional means allow a more premium positioning.

However, even the largest store chain has a limited footprint, while India’s vibrant mom-and-pop retailers form a much larger platform and continue to reach out to a much larger market than the modern traders. So by focussing on the chain-stores alone, international brands would miss out on the majority of the Indian consumers who do not have a chain store near them, or choose to continue shopping at the traditional stores.

On the one hand you might think that it is logical to reach out to as many customers as quickly as possible. On the other hand, “foreign” equals “exotic” in the dictionary, which equals mysterious, interesting, glamorous and so on. So some of these brands actually benefit from maintaining an aura of exclusivity, and it helps if their distribution is limited.

This challenge, therefore, needs to be addressed by each company specifically, keeping its brand and business objectives in mind.

The second concern is more widespread and includes both the branded supplier as well as the retailer, whether chain-store or traditional mom-and-pop. It is a given that the international brand will share a store environment with local brands. Unless, of course, an international brand creates a separate exclusive branded store (easier to do in fashion and lifestyle products than in food and grocery), or it is only sold in stores which sell only foreign merchandise (of which there are very few).

So the second question is: in the shared retail environment, should the international brands be mingled with local brands and products, or should they be displayed apart from local brands? This question is relevant even if a brand is only present in the modern Indian supermarkets.

Prices of imported merchandise of international brands tend to be high, because the base price can be high to start with, and import duties and other costs push the price up further. So a popular option so far has been to bunch imported brands together at the retail store on one or a few shelves. The reasoning is that these are speciality products, expensive and with a limited consumer base. Shoppers who know about these brands will seek them out, and they are likely to also shop for other imported brands at the same time, so it makes sense to display them together.

Some brands are happy with this display strategy, because it makes a clear statement that their brand is a premium “exclusive” brand, and it prevents a one-to-one comparison with lower priced local competitors.

However, brands that want to be visible to a wider set of consumers would be unhappy with this arrangement. Their take would be that by bunching high priced merchandise together, the retailer is creating an area which becomes a dead zone that is avoided by most shoppers. Thus, a brand that could be otherwise sold to more consumers is forced to become a niche product due to the limited visibility.

Regular readers would know that our approach to creating or judging strategy is dogmatic only in one aspect: “to avoid the cookie cutter”. Whether you’re selling meat snacks, exotic meal packs, kettle chips or iceberg lettuce, multiple factors determine whether a particular international product should be segregated or displayed alongside local brands. And that strategy needs to be dynamic.

The first factor to consider is how familiar is the product itself to the customer frequenting the store. Let’s take an imported salsa as an example. In a location where the customers may not be familiar with Mexican cooking, it makes sense to not just display tortillas, salsa, sour cream and beans together, but also to offer samplers and give away recipes. While the salsa may be of an imported brand, the beans may be of an Indian brand, and the tortillas and cream may be from a local supplier.

In this case, where each component of the meal originated is less important than the fact that the complete meal needs to be presented together to the customer. Putting the imported salsa with other imported products when most of them may not be sure how to use it does not encourage customers to buy it.

In any case, as familiarity increases with time, the product may become more widely available, other international and national brands may also appear on the shelves, and segregation becomes a non-issue.

The tendency of the store’s consumer to compare and decide on the basis of price – as mentioned earlier – can also be an important factor. In some cases, the product may need to be insulated from this comparison, and placed in a defined area with other high-priced imported brands. In other cases, if the brand is strong enough to stand on its own, it could be placed in high-traffic locations with higher-volume lower-priced brands.

The overall store positioning and product mix have a very large role to play in the decision about segregation. If a supermarket has an upmarket catchment, and carries a higher proportion of premium products, intermingling may be the norm rather than an exception. The customer who is serving herself would probably find it most convenient to have the local and imported baked beans or olive oils displayed together. The price premium may even play to the imported brand’s advantage in such upmarket environments and catchments, conveying some form of qualitative superiority.

If a store has a wide enough assortment of imported products which are significantly higher priced than local variants, then it may make sense to do an “international corner”. But for this to work, the customer base must already be reasonably aware of the individual products being sold. The international corner also needs to be kept fresh, with new brands and new varieties of product to keep the foot traffic alive and the products moving. Even then, “packaged solutions” and demonstrations are needed to maintain visibility.

Let’s understand one fact – people adapt exotica into their consumption culture so deeply until it you can’t differentiate between the local and the international. Indian cuisine would be incomplete without potatoes, chillies and mangoes. However, the varieties of all three crops available in India today are reported to have been brought from the Americas and west Asia a few hundred years ago. Among companies, Colgate, Vicks, Horlicks and Bata are all international brands that Indian consumers commonly accept as their own.

Most international companies want to target the millions of Indian middle class households, but their pricing, distribution and retail strategy is too exclusive, conservative and totally contrary to this objective.

Our suggestion would be: go out as wide as you believe is appropriate, because being invisible does no good to the brand. Put your exotica within the reach of the consumer, alongside competing local products.

As long as you’re prepared to support the brand, and sustain efforts to encourage consumers to try the product, there would be a time when your brand is no longer treated as exotic. And that would be a good thing, if you’re looking for large numbers.

Devangshu Dutta

January 18, 2008

The entertainment business suggests that nostalgia is a very powerful driver of profit.

It is quite clear that retro is “in”. The movie business worldwide is full of sequels, prequels, re-releases and remakes. The music business is ringing up the cash registers with remixes and jukebox compilations. Star Wars and Sholay still have a fan following. ABBA has leaped across three decades, Hindi film songs from 30-60 years ago have been given a skin-uplift by American hip-hop artists, while Pink Floyd is hot with Indian teens along with Akon and Rihanna.

As copyright restrictions are removed from the works of authors long-gone, the market gets flooded with several reprints of their most popular writings. Of course, we know that classic literature survives not just a few years but even thousands of years. Examples include the still widely-read 2,500-year-old Indian epic Ramayana by Valmiki, the Greek philosophers’ works that continue to be popular after two millennia and the Norse legends that have been told and re-told for over a thousand years. Spiritual and religious leaders’ writings are also recycled into the guaranteed market of their followers and possible converts for a long time after their passing away.

On the other hand, the basic premise of today’s fashion and lifestyle businesses is that silhouettes, colours and design-cues will become (or be made) obsolete within a few weeks or a few months, and will be replaced with new ones. This principle is true not just of clothing and footwear, but is applied to home furnishings, furniture, white goods, electronics, mobile phones and even cars. In fact, the fashion business (as it exists) would find it impossible to survive if customers around the world chose only classics which could be used for as long as the product lasted in usable form.

What Fashionability Means for Brands

Other than individual styles or products falling out of favour, as fashions move and as the market changes, it is evident that some brands also become less acceptable, are seen as “outdated” and may also die out as they lose their customer base.

Of course, that some brands become classics is quite apparent, especially in the luxury segment where brands such as Bulgari have survived several generations of consumers, and continue to thrive.

However, the past is of relevance to the fashion sector because, other than planned or forced obsolescence, the fashion business has also long worked on another principle – that trends are cyclical.

Skirts go up and down, ties change their width, and the colour palette moves through evolution across the years. A style formula that was popular in the summer of a year in the 1970s might be just right in another summer in the first decade of the 21st century.

So, the question that comes up is whether the same logic that is applicable to individual products, styles and trends, could also be applied to brands.

The answer to whether apparently weak, dead or dying brands could be brought back to life is provided by brands such as Burberry’s, Lee Cooper and Hush Puppies. Sometimes innovative consumers create the opportunity – as with Hush Puppies in the 1980s – while in other cases (such as Burberry’s, Volkswagen’s Beetle, or Harley Davidson), vision, concerted effort and resources can make the brand attractive again.

The question then is not whether brands can be relaunched – they can. The more important question for brand owners is: should a brand be relaunched. And using the logic of the fashion business, rather than being left to linger and then dying a painful death, could brands be consciously phased-out and later brought back into the market as the trends change?

The Brand Portfolio – Diversifying Opportunities and Risks

These questions are particularly important for large companies, or in times when market growth rates are slow, or when the market is fragmented. Organic growth can be difficult in all these scenarios, and companies begin to look at developing “portfolios” by acquiring other businesses and brands, or by launching multiple brands of their own.

The car industry worldwide has lived with brand portfolio management for long. Even as companies have merged with and acquired each other, the various marques have been retained and sometimes even dead ones have been revived. The companies generally focus the brands in their portfolio on distinct customer segments and needs (such as Ford’s ownership of “Ford”, “Volvo” and “Jaguar”, or General Motors with its multiple brands), and then further play with models and product variants within those. When things go right portfolio strategies can be quite profitable, but the mistakes are especially expensive. Sensible and sensitive management of the portfolio is absolutely critical.

In the fashion and lifestyle sector, the players who already follow a portfolio strategy are as diverse as the luxury group LVMH, mainstream fashion groups like Liz Claiborne (with brands in its portfolio including Liz Claiborne, Mexx, Juicy Couture, Lucky Brand Jeans) and LimitedBrands (Limited, Victoria’s Secret, La Senza etc.), retailers such as Marks & Spencer (with its original St. Michael’s brand having given way to “Your M&S”, and also Per Una) and Chico’s (Chico’s, White House | Black Market, and Soma Intimates) who wish to capture new customer segments or re-capture lost customers. Some of these companies have launched new brands, some have relaunched their own brands, and some have even acquired competing brands.

The issue is also relevant to the Indian market, whether we consider Reliance’s revival of Vimal, the new brand ambassador for Mayur Suitings, or the PE-funded take over of Weekender. As the market begins evolving into significantly large differentiated segments, branding opportunities grow, and so will activity related to existing or old brands being resurrected and refreshed. An additional twist is provided by Indian corporate groups such as Reliance, Future (Pantaloons) and Arvind that are looking to partner international and Indian brands, or grow private labels to gain additional sales and margin.

The issue also concerns those companies whose management is attached to one or more brands owned by them which may not have been performing well in the recent past, but due to historical or sentimental reasons the management may not like to close down or sell them.

It is equally critical for potential buyers who would like to take over and turn brands around into sustainable profits. This is a real possibility in this era of private-equity funds and leveraged buyouts, where a company or a financial investor might find it cheaper and more profitable to take over an existing brand and turn it around, rather than building a new brand. This is already happening in the Indian market. More interestingly, Indian companies have also already acquired businesses in the USA and Europe, and the potential revival or relaunch of brands is certainly relevant for these companies as well.

When to Recycle and Reuse

Relaunch or acquisition of an existing active or dormant brand can be an attractive option when building a portfolio, or when a company is getting into a new market.

For the company, acquiring an existing brand is often a lower cost way to reach the customers, and also faster to roll-out the business. The company may assess that the brand already has an existing share of positive customer awareness that is active or dormant, and that the effort and resources (including money) needed to build a business from that awareness will be much less than that to create a new brand.

The risk of failure may also be lower for a relaunched brand than for a new brand.

This is because the softer aspects, the hidden psychological and emotional hooks, are already pre-designed. This provides a ready platform from which to re-launch and grow the brand.

From the customer’s point of view, there is the confidence from previous experience and usage, and possibly also nostalgia and comfort of the ‘known’.

‘Age’ or vintage is respectable and trustworthy. This is especially powerful during volatile times or in rapidly changing environments when there is uncertainty about what lies in the future, and makes an existing brand a powerful vehicle for sustaining and growing the business.

On the Downside

However, when handling brands it is also wise to keep in mind the cautionary note that mutual funds issue: “past performance is no indicator of the future”.

In re-launching active or dormant brands, there is also a downside risk. While the brand may have been strong and relevant in its last avatar, it may be totally out of place in the current market scenario. The competitive landscape would have shifted, consumers would have changed – new consumers entering the market, old consumers evolving or moving out – and the economic scenario itself may now be unfriendly to the brand.

Also, the “awareness” or “share of mind” may only be a perception in the mind of the person who is looking to re-launch the brand, and the consumer may actually not care about the brand at all. There are instances where the management of the company has been so caught up in their own perception of the brand that they have not bothered to carry out first-hand research with the target segment to check whether there is actually an unaided recall, or at worst, aided-recall of the brand. They are imagining potential strengths, when the brand has none.

It is also possible that, during its last stint in the market, the brand may have gathered negative connotations – consumers may remember it for poor products or wrong pricing, the trade may remember it for late deliveries, vendors may remember it for delayed payments…the list goes on. In such a scenario, it may be a relaunch may be a disaster.

So how does one know whether to resurrect a brand, or to reincarnate it in another form, and when to just let it die? The answers to that lie in answering the question: what is a brand? And then, what is this brand?

A Critical Question: What is a Brand?

Even in these enlightened marketing times, many people believe that the brand is the name. They believe that once you advertise a name widely and loudly enough, a brand can be created. Nothing could be further from the truth. High-decibel advertising only informs customers of the name, it cannot create a brand.

If we put ourselves in the customer’s shoes, a brand is an image, comprising of a bundle of promises on the company’s part and expectations on the customer’s part, which have been met. When promises are delivered, when expectations are met, the brand develops an attribute that it is defined by.

The promise may be of edgy design (think Apple), and the customer expects that – when the brand delivers on the promise and meets the expectation the brand image gets re-affirmed and strengthened. However, these attributes are not always necessarily all “positive” in the traditional sense. For instance, a company’s promise may be to be low-cost and low-service (think Ikea, or “low-cost airlines”), and the customer may expect that and be happy with that when the company delivers on that promise. The promise may be products with a conscience (think The Body Shop), which may strike a chord with the consumer.

What that brand actually stands for can only be created experientially. Creating this image, creation of the brand, is a complex and step-by-step process that takes place over time and over many transactions. Repetition of the same kind of experience strengthens the brand.

The brand touches everything that defines the customer’s experience – the product design and packaging, the retail store it is sold in, the service it is sold with, the after-sales interaction – all have a role to play in the creation of the brand.

For instance, to some it may sound silly that market research or how supply chain practices can help define a brand, but that is exactly how the state of affairs is for Zara. Changeovers and new fashions being quickly available are what that brand is about, and it would be impossible for Zara to deliver on that promise without leading edge supply chains, or a wide variety of trend research.

Similarly, it may sound clichéd that your salesperson defines the brand to the consumer, but even with the best products, extensive advertising, and swanky stores, for service-oriented retailers everything would fall apart if the salesperson is not up to the mark. This is indeed a sad reality faced by so many of the so-called premium and luxury brands.

Of course, brand images can be changed or updated, but the new image also needs to be reinforced through repeated action, a process just like the first time the brand was created.

Reviving a Brand: the New-Old Seesaw

Given that a brand is created over multiple interactions and repetitive delivery of certain attributes, it is only natural that the older the brand, the more potential advantage it would have over a new brand. Just the sheer time it would have spent in the market would give an old brand an edge.

An old brand can appear to be proven, experienced and secure, while a new brand could be seen as untested, raw and risky. An old brand may have had a positive relationship with the consumer, but may have been dormant due to strategic or operational reasons. In this case, reviving the brand is clearly a good idea. There is already an existing awareness of an older brand, which can act as a ready platform for launching the same or a new set of products or services. Often, there may be a connection with the consumer’s past positive experience of the brand.

On the other hand, a new brand may appear to be fresh, more up-to-date and relevant, and vigorous, compared to an old one that may be seen as outdated and tired. Certainly, if nostalgia had been all that brands needed to thrive, then old brands would never die and it would be difficult to create new brands.

Clearly, there is no single answer to whether it is a good idea to re-launch an existing or old brand. If you are considering whether it would be a good idea to revive an old brand, or to acquire and turn an existing brand around, ask yourself this:

If the answer is “No” to any of these questions, then one needs to think again. However, if the answers are all “Yes”, then a resuscitation is just what the doctor might have ordered.

Devangshu Dutta

March 3, 2006

In February, just before the mega-blitz of “India Everywhere” at the World Economic Forum, the Indian government took a step forward. Amidst shrill outcries from its coalition partners and domestic anti-FDI lobbies, it finally decided to bell the cat, and let foreigners invest in retail again!

About a month has passed since the cabinet announcement, the dust has settled, and it is a good time to consider what has happened.

Since the initial euphoria of the early-to-mid 1990s when international retailers entered the market including companies such as Benetton (50% JV) and Littlewoods (100% subsidiary), this revised policy provides the first opportunity for large global companies to participate in the Indian market’s growth.

The key questions being raised are:

What Is Allowed, and Who Might Enter?

Let’s first deal with what the government has actually allowed. In a nutshell, a foreign retailer can set up a company in India in which it holds 51% equity, the balance being held by an Indian partner. This subsidiary can operate retail stores in India under one brand name. All products in the store must also carry the same brand name, and this branding must have been applied during the process of manufacturing.

This means that, as yet, a foreign department store selling multiple national and international brands cannot set up its own 51% owned operation in India. Nor can a supermarket or hypermarket chain like Wal-Mart, Carrefour or Tesco, sell their wide range of products under any name but their own, if they decided to take a majority stake in a retail operation.

In theory, you could have a Wal-Mart store selling Wal-Mart cola (not Pepsi), Wal-Mart butter (not Amul or Mother Dairy), Wal-Mart chocolates (not Cadbury’s), Wal-Mart cookies (not Britannia or Sunfeast), Wal-Mart T-shirts (not USI or Duke). You could have Tesco jeans (not Levi’s or Numero Uno) or Carrefour luggage (not Samsonite or VIP). This obviously dilutes the consumer proposition of the store, which may then have to primarily focus on a single-point agenda – such as low prices – to draw consumer footfall.

On the one hand, the cabinet decision clearly allows companies such as Starbucks and The Body Shop to step in with a majority stake, provided the branding is clearly by the primary name (store name) – thus, you may not be sold the famous “Tazo Tea” in Starbucks, but get “Starbucks Tea” instead.

However, to a brand such as Starbucks, this policy change is significant as its international expansion is largely through owned operations, especially in potentially large and strategic markets such as India. Starbucks would now have the option of not only controlling the retail operation through a 51% ownership, but also the raw material sourcing, storage and wholesale operation.

On the one hand, this may mean nothing to a retailer such as The Body Shop, whose international strategy in Asia has been largely driven through franchise relationships. This is true now of India as well, as The Body Shop announced its master franchise arrangement with Planet Sports in India.

A retailer such as Gap would need to set up separate retail operations for Gap, Old Navy, Banana Republic and Forth & Towne. There obviously are ways to consolidate operations even with the diverse retail corporate structure, but it does mean that the foreign retailer will be operating several corporate entities in India.

An existing company such as Benetton does not benefit from this change in regulation. In 2005 Benetton actually increased its stake in its joint-venture to 100%, but in the bargain had to forego the stores it was running. Its current network comprises entirely of franchise stores, and will have to remain so, unless Benetton reduces its stake to 51% in order to be able to run stores in India, which is highly unlikely.

Other existing international brands such as Levi Strauss, Adidas and Nike are not retailers in themselves, and are not dramatically affected by the change in policy at all. All of them operate subsidiaries in which they have complete or majority ownership. Brands such as Tommy Hilfiger, Wrangler and Lee are also present through licence or franchise relationships, and unlikely to change their strategy.

Will Global Retailers Come?

All of this obviously raises the question whether government regulations preventing foreign investment in retail were or are actually keeping foreign companies out of the Indian retail market.

The answer to that is both “No” and “Yes”. The reason is that companies that are looking at international expansion apply criteria that are specific to their own business needs which can lead to very different evaluations by each company.

Laws allowing or preventing FDI in retail are only one of the several factors that any global retailer would look at, when considering a market.

Other factors, such as various market options possible at the time, the state of development in the market, existing sourcing and other relationships, scale and scope of investment required vs. the rate of return expected, the risk factors involved, and the retailer’s own business strategy, all play a part in their decision-making process.

Thus, in one company’s case India may be the hottest market in which it would like to open a store at the earliest possible date this year, while for another company India may be of interest only after 5-7 years.

Opening single-brand retail to foreign direct investment, therefore, is at best an encouraging signal that the government has provided. It is unlikely to prompt international retailers to look at India any sooner than they might otherwise have.

The second key issue is whether FDI itself is of any consequence to whether the retailers enter India. This again is related to the individual retailer’s own strategy and business context, as well as how they perceive the risk-return ratio.

Thus, while China may not have any restrictions on foreign investment in retail, western retailers may still prefer to go with a local partner due to the differences in cultural and market nuances. Even in other unrestricted markets international retailers may prefer to enter through licensees or franchisees because the effort and investment in setting up their own company may not be compensated by the size of the opportunity, or their own investment strategy may not be in line with setting up international subsidiaries.

Some companies such as Wal-Mart, Tesco, Gap and Starbucks prefer to invest in international operations themselves, as ownership gives them a higher degree of control over the business. Of course, both Tesco and Wal-Mart have set up joint ventures in markets that are starkly different in cultural and business norms from their home markets but, by and large, where feasible these companies prefer majority or 100% stake in the business.

Other companies, such as Mothercare, Debenhams and The Body Shop, have expanded their international presence through franchises. Their premise is proprietary product and an enormously powerful brand that translates well across cultures. These companies have taken the less intensive route of franchise. In India, too, they have signed master franchises. Mothercare has assigned master franchise rights to the Rahejas’ Shoppers Stop. Debenhams and The Body Shop have both signed up with Planet Sports (soon to be renamed Plant Retail), which is also the franchisee for Marks & Spencer.

Thus, while allowing FDI may help some companies, it is unlikely to have investors beating down the door in a rush to enter.

What Does FDI in Retail Mean for India?

Permission for foreigners to invest in retail businesses in India obviously mean different things to different stakeholders in India.

For real estate owners, especially shopping centre developers, new entrants are always welcome, since it provides a wider basket of brands to present to the consumer, and the opportunity to differentiate one shopping centre from another.

To existing retailers, it does mean potentially more clutter in the market, possible higher marketing expenditure for them to maintain their position. However, it also means that more players can encourage the growth of the market, which otherwise can end up looking stale and in-bred. Brands that are entering the market for the first time can also bring fresh ideas in terms of merchandise, store planning and display, advertising etc.

To the question of whether Indian retailers are prepared to handle the competition, I would say that, while global best practices help, retail is a uniquely local business. Indian retailers who bother to listen to the consumer and constantly upgrade their own business are possibly in a stronger competitive position than a foreign brand that wants to impose its own alien sensibility on the market.

For suppliers, new brands bring in new avenues for business growth. Many of the international brands will look to increasing their sourcing from India, to take advantage of local labour costs and skills, or to down-play the disadvantage of duties on imported merchandise. Thus, especially for suppliers of fashion goods this is definitely a growth opportunity. Retailers might even prefer to work with the supply base from which they already source for their operations in other markets. Thus, the growth opportunity exists for exporters – the question is how many of them are willing and able to make the transition to begin supplying locally.

Not only do new retailers bring the prospect of increased business, but also the possibility of better systems and skills, improved product development, and in all, an opportunity for the supply base to upgrade itself. This will certainly have a positive fall-out for exporters, since their business is likely to become overall more competitive globally, too.

Let’s consider another stakeholder, who we tend to miss – the government itself. Organised retailers, including global companies, tend to be more constrained by law than a retailer from the unorganised segment. Based on that assumption, a large international retailer (and his Indian counterpart) will set up a local company that will carry out business by the book, recording all sales and purchase transactions. All local sales and purchases will be subject to VAT and sales taxes, while all imports would be documented and therefore subjected to import duties. All of this means more revenue for the government.

On the other hand, do foreign retailers pose a threat at all?

Well, there is certainly a threat to those retailers who insist that the market needs to remain structured the same way that it has been for years, and who refuse to upgrade their own business. There may even be a threat to the large Indian corporate retailers who are competing on the basis of their scale relative to the rest of the market. With the presence of global retailers with deeper pockets, these large Indian retailers will no longer be the big boys on the block. But the positive outcome for the many seems to outweigh the negative outcome for the few.

What I would certainly like to see is how quickly the government translates the promise of opening into a concrete plan that can benefit the Indian consumer, the Indian supplier, the Indian real estate market and the government itself.