Devangshu Dutta

August 17, 2019

Retail is such a pervasive and dynamic a sector of the economy, that it is impossible to identify a single point at which modernisation began. I’ve met countless people who perhaps entered the retail sector during the last 15 years, and who mark the beginnings of modern retail around then. There is no doubt that there has been an explosion of investment in retail chains in the last 2 decades, but we need to acknowledge the foundation on which this development is built. The current titans of the sector are standing on the shoulders of previous giants who have created successes and failures from which we are still learning.

This piece is not an exhaustive history of the evolution of the retail business in India, nor a census of all the brands operating in this sector, but the aim is to capture the flavours of the phases of development. (PDF available here to download.)

Early Years

If we were to trace back the growth of “organised” retail (mind you, I dislike that word!) or modern retail to the first retail chains, we will have to cast our mind back more than a hundred years. While many businesses of that time have disappeared, a few pioneers continue to survive, straddling three eras: the British Raj, the Socialist Raj and the Liberalised Lion economy. The businesses that continue to stand, having been through multiple transformations, include:

Fifty Years of Independence

The 1950s and 1960s remained fertile times, post-Independence and before the heavy-handed Socialist Raj truly began squeezing the life out of Indian businesses. Leading textile companies such as DCM, Bombay Dyeing and Raymond, and footwear companies such as Bata and Carona established chains of retail stores including company-operated stores as well as authorised dealers operating under the companies’ banners.

The 1980s brought the Asian Games, colour television, and a new up-to-date car model to India, all marks of a new vibrancy. Over the 1980s, a new retail wave was led by indigenous ventures such as Intershoppe (launched by a fashion exporter), Little Kingdom and The Baby Shop (children’s products), Nirula’s (fast food) and Computer Point (home computers, PCs and accessories). Many of these were certainly ahead of their time: the critical mass of consumers had yet to develop, the business infrastructure was inadequate, and funding norms were unsuitable to the capital-hungry business of retail. Unlike the textile companies that had large manufacturing and trading businesses, these new retailers were like shooting stars, glorious but visible for only a short period of time. This period, unfortunately, also witnessed the degeneration and disappearance of some of the older stalwarts such as DCM and Carona that were beset by labour disputes, management issues and disconnection from the transforming market.

Numero Uno, an indigenous denim brand, was launched in 1987 soon after VF’s American denim brands were launched, and it took nearly a decade for Numero Uno to reach other geographies in India. Nirula’s, one of the oldest fast food restaurant chains based in North India, expanded across the Delhi NCR in the 1980s and 1990s, and also explored other cities, albeit with mixed success.

Future Group, which today has a large retail and consumer brand portfolio, launched trousers under the name Pantaloons in 1987, initially as a distributed brand, and then denimwear under the brand name Bare. Within a few years the company also launched exclusive stores by the same names, to provide focussed visibility to the brands. About a decade of growth later, the group launched its first large format store under the Pantaloons name, but by now covering a much wider range of products, which became its launch pad for achieving scale.

The RPG group that had acquired Spencer & Co. relaunched it in 1991 in a spanking, new format as Spencer’s in Bangalore, and a short few years later rebadged it again as Foodworld in a joint-venture with a foreign partner. It subsequently went on to launch other formats such as Musicworld and Health & Glow.

Also in 1991, the Rahejas converted an old cinema into a department store, Shoppers Stop, aiming to provide an international shopping experience, although initially focussed on menswear. The store added women’s and children’s sections in subsequent years and the second store was launched four years later after the first one. Subsequent large scale retail expansion only came about towards the end of 1990s.

Little Kingdom is a notable example that I would like to dwell on briefly (partly for the purely personal reason that it was my first retail job!). The business was launched in 1987, headed by alumni of the illustrious IIMs around the country, built on processes and IT systems that could have been the envy of many retailers even 25 years later. The company – Mothercare India Limited – was the first purely retail company to start up and launch a public issue in 1991. During the early 1990s, it was the largest retail chain present across the country, in its categories. In 1991, it also attempted to bring the first home computer, Spectrum, to forward-thinking parents through a mix of in-store sales and door-to-door direct-selling. It was admittedly one of the first to expand internationally, opening a franchise store in Dubai in 1992. During its short life, the team launched multiple brands and formats, including Little Kingdom, Ms (a womenswear brand), The Baby Shop, and became a partner to the international giant VF Corporation’s Healthtex children’s brand and Vanity Fair lingerie brand in India. But, by the mid-1990s – financially overstretched between multiple brands and formats, and backward integration into manufacturing – it was gone.

Physical retail was not the only avenue being explored for growth during these decades. An Indian company imagined replicating the success of western catalogue companies, and launched the Burlington’s mail order catalogue retail venture and even became a joint-venture partner of one of the world’s largest catalogue retailers, Otto Versand (Germany). Other models included direct sales business, such as the Eureka Forbes introducing vacuum cleaners through demonstration parties (which was emulated for the Spectrum home computers mentioned above). With the growth of private television channels, products also began being promoted during non-peak hours through infomercials, though serious TV shopping was still a few years away, coming up in the mid-2000s with dedicated teleshopping channels.

The Foreign Hand and Corporate Retailing

The 1980s and 1990s also saw the launch of international brands from global giants such as VF Corporation (Lee, Wrangler, Vanity Fair, Healthtex), Coats Viyella (Louis Phillippe, Van Heusen, Allen Solly), Benetton (UCB and 012), Levi Strauss, Lacoste, Reebok, adidas, Pepe and Nike, grocery retailers such as Nanz (a three-way German-US-Indian partnership) and Dairy Farm International (with RPG Group’s Spencer’s Retail) and Quick Service formats such as Domino’s, McDonald’s, Pizza Hut, Baskin Robbins and KFC.

India was reopening to business, global management consultants were writing glowing reports about the untapped potential of the (mythical) 200 million middle-class customers and global retailers wanted to own part of the action.

Due to the lack of large-format stores and suitable environments, international brands that entered the Indian market during this phase needed to create exclusive stores to ensure that the brand could be communicated holistically to the consumer, in an environment that was more in the brand’s control, and many of them were, in a sense, “forced” to become retailers in India.

However, around 1996, a very senior member of the cabinet is reported to have said, “Do we need foreigners to teach us how to run shops?” It was an unexpected condemnation, coming as it was from a person and a party otherwise seen as champions of an open economy. It slammed the doors shut to foreign investment and, to my mind, the sector is still yet to fully recover from that ban and the policy contortions that have come over the years to allow international brands and retailers to play a more active role in the market.

Internal weaknesses compounded the decline or exit of some of the businesses. Nanz folded due to various operational challenges and lack of adequate experience. British retailer Littlewoods’ wholly-owned subsidiary pulled out of the market due to problems back home, and in 1998 sold the sole store to the Tata Group, which eventually renamed it Westside.

Despite the early hiccups, India continued to attract international players on account of the high growth and changing social norms. Not only was there greater purchasing power available amongst more Indian consumers, there was a shift in consumer attitude from saving to spending. Several brands, including fashion, luxury and quick service formats, entered the market through licensing, franchising, and joint ventures.

During this period the domestic retail market also drew in more corporate houses, attracted by the apparently abundant market opportunity for them to mine alone or to act as a gateway for foreign companies interested in India. Most were significant diversifications from their existing businesses.

Tobacco, paperboards, agri-commodities and hospitality conglomerate ITC ventured into retailing through Wills Lifestyle and as well as its rural initiative e-Choupal in 2000, followed by John Players and Choupal Sagar respectively. Pantaloon Retail launched a partial hypermarket format Big Bazaar in 2001 and went on to Food Bazaar in 2002, Central in 2004, Home Town and Ezone in 2006. Reliance entered in 2006 with multiple stores of Reliance Fresh being opened simultaneously and over the next few years the company expanded through multiple formats such as Reliance Mart, Reliance Digital, Reliance Trendz, Reliance Footprint, Reliance Wellness, Reliance Jewels to name a few. Telecom major Bharti set up a joint-venture with Wal-Mart at the back end, while the Tata group tied the knot with Woolworths and Tesco in two separate businesses supplying its retail stores, even as it expanded its successful watches and jewellery businesses, as well as Westside.

Even a retail operation like Fabindia, born as an export surplus outlet of a handicraft product business found investors to back a rapid expansion spree, becoming more of a corporate retailer than a front-end for producer organisations and craftspeople.

Through the 1990s and beyond, the market remained in ferment. In 1997 Subhiksha, a small modern retail format for food and grocery was launched. Venture-funded Subhiksha expanded rapidly and over the next decade grew to 1,600 outlets. However, in 2009 the business closed down owing to a severe cash crunch, amidst accusations of criminal mismanagement and fraud.

New product areas emerged highlighting the pace of change of lifestyles, cafes prominent among them. Café Coffee Day opened its first store in 1998 in Bangalore and became the largest organised coffee chain in India by far, though it is now living under the shadow of the recent death of its founder. Barista was also launched in 1999 as India’s Starbucks-wannabe, found its footing, scaled up and lost its way, going on to be sold to Tata Coffee and the Sterling Group, who turned it over to the Italian coffee company Lavazza in 2007, who also exited seven years later. Its current owner, the Amtex Group, is itself going through financial troubles in some of its key businesses.

In the last two decades, while some retailers have gone out of business due to unrealistic business plans, mismanagement or lack of funds, most have taken opportunities to rationalise their operations by shutting down unviable or underperforming locations, aligning businesses to market needs, assessing their brand consistency across various touch points, improving organizational capabilities right down to front-line staff, and focusing on unit productivity.

It’s not just Indian retailers that have faced trouble. Foreign brands have had their own share of problems – some have overestimated the market, or their own relevance to the Indian consumer, while others have had misalignment with their Indian franchisees or joint-venture partners. A number of foreign brands and retailers have also churned partners, or exited the market outright, but most remain committed and invested in the market for the long-haul. The last few years have also seen the successful launch and humongous growth of global leaders such as Zara and H&M, even mass-market Chinese retailers like Miniso, as well as the largest investment commitment made by Ikea (about US$2 billion).

Showing on a Screen Near You

The late-1990s also witnessed a dotcom frenzy that led to a plethora of travel sites, and a few product sales businesses such as Fabmall, Rediff and Indiamart.

However, the online market lacked critical mass in the 1990s and early-2000s. Despite apparent advantages of the online business model, success depended on internet penetration (low!), the appearance of value-propositions that were meaningful to Indian consumers (questionable), investments in fulfilment infrastructure (lacking) and the development of payment infrastructure (regulation-bound). Malls and shopping centres – the new temples of retail – seemed to be sucking up all of the consumer traffic, in any case.

By the mid-2000s the business had reached just about Rs 8-9 billion (US$ 180-200 million), despite 25 million Indians being online. Dotcoms became labelled dot-cons, with an estimated 1,000 companies closing down. However, multiple changes took place in the mid-2000s, among them being the price disruption of the telecom market and explosion of mobile connectivity, as well as a renewed funding appetite among venture funds.

This laid the path for growing the second crop of ecommerce in India. Billions of dollars of investment was poured into creating India’s Amazon wannabes, the high streets ran red by ecommerce-fuelled discounts, aggressive advertising budgets (most promoting discounts) and mergers/acquisitions pushed through by venture investors.

After more than a decade of the second coming, India’s ecommerce business accounts for a market share of total retail in the low single digits. India’s Amazon – if one can call it that – is the Flipkart group, now owned by Walmart, bought at an eyepopping $21 billion valuation and still bleeding cash, and the runner-up is relentless Amazon that continues its aggressive push to own what could be one of the three largest markets in years to come. The Chinese internet giants Tencent and Alibaba are also trying to hack piece off the market, having fulfilled their aim of kicking out Western competitors from their home market.

However, the wild card has just been played by the Reliance Group – having moved from textiles to fibre to oil, the group has made its move into telecom and data (didn’t someone say, “data is the new oil”?). It has strategically pushed handsets and cheap data plans into the hands of the consumers and, according to the latest announcement on Jio Fiber, will soon offer High Definition or 4K LED television and a 4K set-top-box for free. The play is to grab as much of the customer’s share of spend on products and services (including entertainment) as possible.

Looking Ahead

Possibly the biggest driver of modern retail in the coming years will be the shift in the demographic structure of the country. The young consumers who are joining the workforce now are a distinctly different set from previous generations. This is a generation that has grown up in the liberalised economy and has been exposed to innumerable choices since their childhood. The most important factor is that these consumers are increasingly located outside the top 10 or 20 cities in the country, and are becoming more accessible as both physical and virtual access improves for them.

A large number of them may have only occasionally, or perhaps never, experienced modern retail first hand while they were growing up, but they have seen this upmarket environment emerge before them and are not shy of spending within it, even if it is only on select special occasions. Most of them are handling mobile phones (even if it is their parents’) while still in school and being socially active online even on the go. Certainly most of them have hardly ever visited tailors, growing from one set of ready-to-wear clothes to another. It is this set of young consumers whose outlook and habits will drive retailing very differently in terms of product categories and services in the future.

There is another significant set of consumers whose number is swelling annually: that of working women. As they add to the discretionary household income available to spend, they gain influence in purchase decisions, and with them the entire household’s lifestyle also undergoes a shift. There is a greater demand of time-saving solutions and convenience products to make their lives easier. Modern retail environments where their various needs can be taken care of under one roof, and convenience pre-packaged products are natural winners in this shift. Ready-to-wear products for women, grooming, beauty and personal care, women-oriented media products, processed foods and eating out get a boost. Another important shift is that, due to busier lifestyles, they are time-crunched and more likely to rely on branded products and services that they can trust. However, given the nascent stage of the market, these brands could just as well be retailers’ own labels, if they are managed well.

In terms of business, significantly greater efficiency needs to be achieved, both at the front-end and in head office and supply chain operations. Process and system-led planning and execution needs to become the norm. With India’s burgeoning population, people are treated as a cheap resource: on the contrary, each extra person can be expensive beyond just their salary cost to the organisation. Each extra person adds some friction to decision making, reducing the responsiveness of the business. Smart business will begin to realise this, and look closely at employee efficiency and effectiveness in the context of the overall business, rather than just in terms of individual costs.

Even as the retail business in India is far from saturation, and fragmented growth continues, the business will also undergo consolidation simultaneously, as large scale retail operations are enormously capital intensive. Mergers will be a strategy that will be explored to improve the viability of many businesses in this sector.

Should you be tempted to think that, squeezed between large corporates, international retailers and ecommerce giants, it’s “Game Over” for smaller domestic retailers and brands, let me say that the India retail story is not only not over yet, but continues to be written and rewritten. As the market grows and matures, retail businesses also need to differentiate themselves, investing more in product selection or even product development through private label growth to help them stand out in the market. A one-size-fits-all strategy doesn’t work in a country as diverse as India. For the size of the market, we have surprisingly few brands, many of them virtually indistinguishable from their competitors. Development on this front, of indigenous brands and product development capabilities, is an absolute must.

The good news is that already there is more talent available than ever before. Most importantly this management pool has experience of the retail sector not just in good times but during (many) downturns as well.

Eventually, what is needed is a mix that will be healthy for India’s ecosystem at large for a long time to come. This will not be delivered by a blind transplantation of international templates or a rapid-fire expansion across the country, nor by fearful protectionism or regional parochialism. It will only be achieved by the evolution of market-appropriate business models and a mature approach that can be make the Indian retailers robust enough to grow not just domestically, but possibly even globally over time.

Devangshu Dutta

December 20, 2018

Do you have this feeling that 2018 went by a little too quickly? Well, however quick it seemed, it was certainly momentous for retail in India.

If 2016 was marked by the shock of demonetization, and 2017 by the pains of GST implementation, 2018 highlighted two threads – the obvious convergence of the online and offline world that had been ignored for far too long, and the interest of foreign capital in India’s consumer world.

Walmart bought India’s loss-making ecommerce leader for an eye-popping US$ 20.8 billion valuation, while ecommerce giant Amazon injecting equity into Shoppers Stop, bought Aditya Birla’s More grocery chain (49 per cent through a back-end entity), and held discussions with Future Group to acquire 9.5 per cent in Future Retail. There were rumours of a mega joint venture between Reliance Retail and China’s Alibaba, and media also reported Japan’s Softbank looking at ploughing US$200 million into Firstcry. Both rivals Amazon and Alibaba were reported to be looking at Spencer’s, one of India’s oldest retail chains currently owned by the RP-Sanjiv Goenka group.

Videos of the crush of curious crowds at India’s first, much anticipated Ikea went viral, and the company said it planned to open 40 locations over the next few years, upping its earlier projection of 25. Chinese retailer Miniso basically came out of nowhere and claimed to have clocked sales of ?700 crores in the very first year in the country.

But along with these cross-border “big bangs” we saw domestic confidence also quietly resurging. Indian retailers are not cowering before large foreign retailers and expensive ecommerce advertising splashes; today they are less defensive about their own prospects than they were two years ago. There is also a growing interest among entrepreneurs and corporates to create new retail businesses, which augers well for the diversity of competition and freshness of offerings in the market.

Going into 2019, one thing I can say with certainty is that the weather, economic and political – both in India and elsewhere – will be unpredictable, and might even turn stormy. Externally, retailers should “expect the unexpected”. To ensure that the business remains on track, however rough the track becomes, retailers must centre all major strategies and decisions on the customer. A theme that has been around for centuries, it is surprising how much it gets ignored in this most customer-facing business.

Retailers tend to divide customers into rigid segments. My suggestion would be to look at customers through the behaviour and experience lens and also recognise that the same customer behaves differently at different times and in different contexts – in effect there are no hard boundaries between “segments”.

It is often emphasised is that Indian consumers are “deal-seeking”. I don’t think we should treat this as a uniquely Indian thing: all consumers look for value-reassurance in unpredictable times and in uncertain conditions. Also remember that even in value-seeking, experience still rules. Retailers and brands that are solely focussing on price or price+feature comparisons are turning their business into a commodity. They are missing the long game: of defining the customer’s experience from the first moment of brand contact to the purchase and beyond.

In 2019, if you want to focus on a single competitive strategy, it would be this: for stickiness and sustainability, think about the customer’s experience, and actively design it, in every environment where the customer connects with you.

Lastly, technology is transformative, but tends to get restricted to being the contrast between ecommerce and physical retail. Indian retailers need to embrace technology in all forms, from using the zillions of transactions within the business and with the customer for developing actionable knowledge, to automating processes where unnecessary cost or time makes the business inefficient.

Having said that, keep the previous rule in mind when deploying at customer-facing technology – make customer-interfacing technology as invisible or intuitive as possible. When in doubt, learn from one of the leaders in the sector, Amazon: its 1-click ordering patent 20 years ago gave it a huge advantage over competitors, and it is now aiming to replicate the same seamless, friction-free behaviour physically with its Dash button. Or pick cues even from younger fashion businesses like Rebecca Minkoff, whose focus is on ease and convenience. The key reason for adopting technology is to remove friction for the customer and for processes that serve the customer.

I have no doubt that 2019 will be eventful – let the customer experience be the guiding light to keep our businesses off the rocks and afloat.

(Published in the Financial Express on 4 January 2019, under the title “Retail in 2019: Need for stronger brand-customer connections that go beyond purchase“)

Devangshu Dutta

October 26, 2018

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

[Accompanying Image credit: Amazon Go; CC/Wikimedia Commons/Brianc333a)]

To many, retail seems to be having an identity crisis.

Closed storefronts on American and European streets and dead malls in India and China are blamed on the growth of online retail. At the same time, the world’s largest online retailer, Amazon, is opening physical stores and buying offline retail operations in the US and in India, while the world’s largest retailer, Walmart, is busy digesting India’s ecommerce market leader. Even India’s online fashion and lifestyle websites – among them Myntra, Firstcry, Yepme and Faballey – are acquiring offline brands or opening stores. Or both.

What in the world is going on?

The short answer: consumers want choice; and retailers have no choice.

For many, ecommerce still seems to have the “new car smell” after more than 20 years, the message pitched so desperately by the founders of and investors in ecommerce companies still echoing: that this “new kid” will make customers’ lives a quintillion times better and wipe out the competition. Two decades on, and hundreds of billions of dollars of investment later, online retail is estimated to be about 12% of the global market. Ecommerce is 10% of the US market, of which Amazon takes up about half. In India the figure is in the vicinity of 2%, with that share is virtually stitched up between Walmart-owned Flipkart Group and Amazon.

Clearly, consumers value offline retail stores, whether for convenience or as holistic brand ambassadors. You can’t take away the fact that retail for us is theatre, experience, social.

Over at physical retail businesses, managers have been terrified of “channel conflict”. Senior management have squeezed resources for online, even when return-on-capital was demonstrably better than a new store. Some have refused to publicise their own company’s website through in-store banners, fearing that the customers would get sucked away from the store. It has been strange to see this opportunity being passed up – if a customer is trusts you to walk into your physical store, why would you not want to connect with them at other points of time when they are not near your store?

As I’ve written earlier, retail is not and should not be divided between “old-world physical” and “upstart online”. Successful retailers and brands have always been able to integrate multiple channels and environments to reach their customers.

For instance, British fashion retailer Next has long used a combination of physical stores (of varying sizes) as well as mail order catalogue side-by-side, and then ecommerce as the digital medium grew. Another British retailer, Argos, took another angle and embedded a catalogue inside the physical store – first a paper catalogue, and then on-screen.

American designer Rebecca Minkoff has taken this unification further. Without the weight of legacy systems, the brand attempts to create a seamless experience for the customer, unifying the store, in-store digital interfaces such as smart dressing rooms, the website and the mobile.

No doubt, for older companies, integrating is tough; business systems and people are in disconnected silos, incentivised narrowly. Each channel needs different mindsets, capabilities, processes and systems, to ensure that the optimal customer experience appropriate for the interface, whether it is a store, mobile app, website or catalogue. But etailers opening physical stores have their own challenges, too, tackling the messy slowness of the physical world, where you can’t instantly switch the store layout after an A:B test. They now need to develop those very “old-world skills” and overheads that they thought they would never need.

Regardless of where they begin, retailers need to mould and blend their business models with proficiency across channels. In the evolving environment, any brand or retailer must aim to offer as seamless an experience to the customer as feasible, where the customer never feels disconnected from the brand.

Varying circumstances make customers choose different buying environments. At different times or on different days of the week, even the same person may choose to shop in entirely different ways. Successful retailers that outlast their competitors have used a variety of formats and channels to meet their customers, and will continue to do so.

To my mind, retailers have no choice but to see the retail business as one, even as it is fluid and evolving. A retailer’s only choice is to bend with the customer’s choice.

(Published in the Financial Express under the title “Uniting retail: Why online versus offline debate must end“)

Devangshu Dutta

January 10, 2017

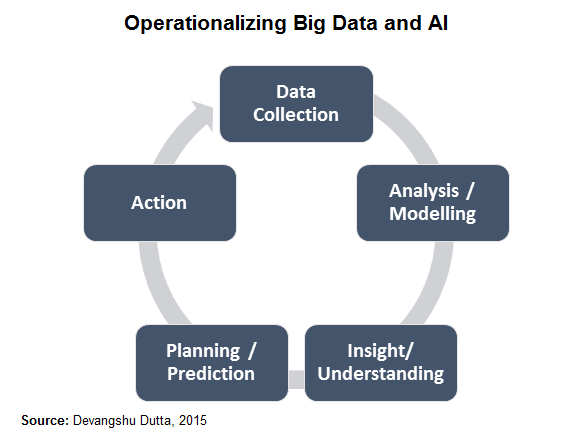

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

July 30, 2015

Much has been written recently, with more than a touch of surprise, about ecommerce companies opening physical retail stores. Whether it is Amazon, Birchbox and Bonobos in the US, Spartoo in France, Astley Clarke in the UK or FirstCry and Flipkart in India, young tech-based ecommerce businesses are adopting the ways of the dinosaur retailers that they were apparently going to drive into extinction.

Perhaps, the seeds of the surprise lie in the perception that the ecommerce companies themselves built for their investors, the media and the public, that it was only a matter of time that the traditional retail model would be dead.

Or perhaps we should pin it on their investors for keeping the companies on the “pure-play” path so far – venture funds that have invested in ecommerce have largely taken the view that the more “asset-light” the business, the better it is; so they’re far happier spending on technology development, marketing, salaries, and even rent, than on stores and inventory.

After a bloody discounting and marketing battle, in a few short years, there are now a handful of ecommerce businesses left standing in a field littered with dead ecommerce bodies, surrounded by many seriously wounded physical retailers who are trying to pick up unfamiliar technology weapons. And their worlds are merging.

Which is a Stronger Building Material – Bricks or Clicks?

Online business models offer some clear strengths. Etailers have a reach that is unlimited by time and geography – the web store is always up and available wherever the etailer chooses to deliver its products.

An ecommerce brand’s inventory is potentially more optimised, because it is held in one location or a few locations, rather than being spread out in retail stores all across the market including in those stores where it may not be needed.

However, we forget that consumers don’t really care to have their choices and shopping behaviour dictated by the business plans of ecommerce companies or their investors. The fact is that physical retail environments do have distinct advantages, as etailers are now discovering.

Firstly, shopping is as much an experiential occasion as it is a transaction comprising of products and money. In fact, the word “theatre” has been used often in the retail business. For products that have a touch-feel element, the physical retail environment continues to be preferred by the customer. Of course, there are products that could be picked off a website with little consideration to the retail environment. For standard products such as diapers or a pair of basic headphones, online convenience may win over the need for a physical experience. However, non-standard products such as apparel or jewellery lend themselves to experiential buying, where a physical retail store definitely has an edge.

Shopping in a physical retail environment is also a social and participative activity. We take our friends or family along, we ask for their opinion and get it real-time. The physical retail environment lends itself to the consumer being immersed in multiple sensory experiences at the same time. These aspects are not replicable even remotely to the same degree by online social sharing of browsed products, wish-lists and purchases, nor by virtual smell and touch (at least not yet!).

In a market that is dominated by advertising noise, a physical store also helps to create a more direct and stronger connect for the consumer with the brand than any website or app can. An offline presence creates credibility for a brand, especially in an environment where online sales are dominated by discounts and deals, and many brands have risen and fallen online in the customer’s eyes during the last 3-4 years.

As a matter of fact, every store acts as a powerful walk-in billboard for the brand. If used well, the store conveys brand messages more powerfully than pure advertisements in any form. This reality has been embraced by retailers for decades, as they have created concept stores and flagship stores in locations with rents and operating costs that are otherwise unviable, except when you see it as a marketing investment.

Showrooming vs. Webrooming

As ecommerce has grown and brands have become available across channels, offline and online, the retail sector has been faced with a new challenge: customers browsing through products in the store, but placing orders with ecommerce sites that offered them the best deal. This obviously meant that retailers were, in a sense, running expensive showrooms (without compensation) on behalf of the ecommerce companies! The industry adopted the term “showrooming” to describe the phenomenon.

However, ecommerce businesses are now getting a taste of their own medicine as retailers are benefitting from a reverse traffic.

Consumers have now started using websites to conveniently do comparative shopping without leaving the comfort of their homes, and collect information on product features and prices but, once the product choice has been narrowed down, the final decision and the actual purchase takes place in a physical store.

This is described with a slightly unwieldy term, “webrooming”. This is one among the reasons that lead to consumers abandoning browsing sessions and carts when they’re online.

Bricks AND Clicks

The wide split between offline and online channels is mainly because traditional offline retailers have been slow to adopt online and mobile shopping environments.

Most physical retailers around the world have approached ecommerce as an after-thought, with a “we also do this” kind of an approach. Ecommerce has typically been a small part of their business, and not typically a focus area for top management. So, in most cases the consumer’s attitude has also reflected these retailers’ own indifference to their ecommerce presence. However, due to the accelerating penetration of mobiles, tablets and other digital devices, a serious online transactional presence is now vital for any retailer that wants to remain top of the consumer’s list.

On the other hand, ecommerce companies, as mentioned earlier, have so far mainly stuck to “pure-play” online presence due to their own reasons. However, with passage of time there is bound to be a convergence and eventually a fusion between channels.

The Journey to Omnichannel

Omnichannel today, in my opinion, is still more a buzzword today than a reality. Being truly omnichannel requires the brand or retailer to offer a seamless experience to the customer where the customer never feels disconnected from the brand, regardless of the channel being used during the information seeking, purchase and delivery process. For instance, a customer might seek initial comparative information online, step into a department store to try a product, pay for it online, have the product delivered at home, and be provided after-sales support by a service franchisee of the brand.

Very few companies can claim to offer a true omnichannel experience, due to internal informational and management barriers. However, having an effective multi-channel presence is the first step to creating this, since operating across different channels needs a completely different management mind-set from the original single-channel business. Having a presence across different channel means that a retailer will need to juggle the diverse needs. Capabilities, processes and systems that are fine-tuned for one channel, may not be fully optimal for another channel. This requires the retailer to restructure its organisation, systems and processes to handle the different service requirements of the various channels.

For instance, brick-and-mortar retailers moving online need to rethink in terms of the service (“always open”), speed (“right now”), and scale (“everywhere”). A traditional retail organisation is seldom agile enough to work well with the new technology-enabled channels as well.

An etailer opening physical stores, on the other hand, needs to embrace product ranging and merchandising skills to allocate appropriate inventory to various locations, as well as the ability to create and maintain a credible, distinctive store environment – in essence, inculcating old-world skills and overheads that they thought they would never need.

The retail business is not divided black-or-white between old-world physical retailers and the upstart online kids – at least the consumer doesn’t think so.

Retailers need to and will see themselves logically serving customers across multiple channels that are appropriate for their product mix. They need to mould their business models until they achieve balance, proficiency and excellence across channels, and eventually become truly omnichannel businesses. It doesn’t matter from which side of the digital divide they began.