Devangshu Dutta

October 8, 2009

Here is a summary of the Sustainable Fashion Forum, and some more pictures from the afternoon.

And here is a previous article on sustainability and corporate responsibility.

admin

May 9, 2009

By Devangshu Dutta, Tarang Gautam Saxena

While the Indian consumers have aspired to own international fashion brands, India’s large population base in turn has been an aspirational market for the international companies.

To remote observers, the Indian market may appear to be a virgin territory as far as international apparel and footwear brands are concerned. But India has seen the presence of international brands for almost a century, including mass brands such as Bata and luxury brands such as Louis Vuitton. However, as the colonial government systematically repressed local textile production, the local resistance to foreign products grew as well. Therefore, until the 1980s, the presence of international fashion brands was negligible.

In the early 1990s, as the Indian economy opened up again, a few international fashion brands entered the Indian market. The pioneering companies during this stage were Benetton, Coats Viyella and VF Corporation.

At this time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment which was thus a target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike).

In the midst of this the media industry was also witnessing a high growth which aided the international brands in gaining visibility and establishing brand equity in the Indian market.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. A growing supply of good-quality retail real estate in the form of shopping centers and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores and shops-in-shop.

The number of international brands continued to grow each year at a steady pace until the early 2000s, and took off exponentially thereafter. By 2005 the number of international fashion brands present in India was over three times compared to that in the mid 1990s. The last few years (since 2005) have continued the significant growth of international fashion brands, including luxury brands such as LVMH, Aigner, Tommy Hilfiger and Chanel.

The Popular Entry Strategies

Many of the international companies entering India in the late 1980s and 1990s chose licensing as the entry route to India to gain a quick access to the Indian market at a minimal investment.

A few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand.

In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought investors in retail real estate that were ideal franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in “Single Brand” retail). Using this route, many brands have entered India by setting up majority owned joint ventures, or transitioned their existing franchise arrangements into a joint venture structure.

The Entry Structure for Some International Brands

| Entry Strategy | Time Period | ||

| 1980s or Earlier | 1990s | Post-1999 | |

| Licensed | Louis Philippe, United Colors of Benetton and 012, Wrangler | Allen Solly, Arrow, Jockey, Lacoste, Lee, Nike, Van Heusen, Vanity Fair | Puma |

| Wholly Owned Subsidiary | Bata, Pepe Jeans | Levi’s® | Hanes, Triumph |

| Joint Venture (Majority) | Adidas, Reebok | Diesel, Nautica, Sixty Group | |

| Franchise or Distribution | Aldo, Burberry, Canali, Versace, Debenhams, Esprit, Gucci, Guess, Hugo Boss, Mango, Marks & Spencer, Mothercare, Tommy Hilfiger | ||

| Joint Venture (incl. Minority Stake) | Celio, Etam, Giordano | ||

Source: “Global Fashion Brands: Tryst with India” (A Report by Third Eyesight) © Third Eyesight, 2009

Note: The above table shows the structure used during entry, and not the structure that exists currently.

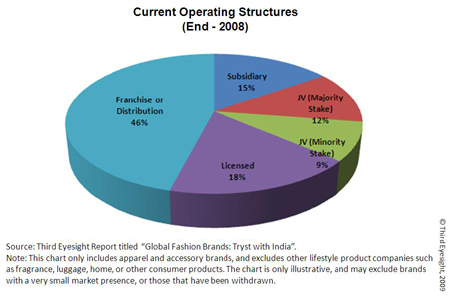

By the end of 2008, just under half of the brands were present through a franchise or distribution relationship, while over a quarter had either a wholly-owned or majority-owned subsidiary. These structures allowed the brands to have greater control of operations, particularly of product.

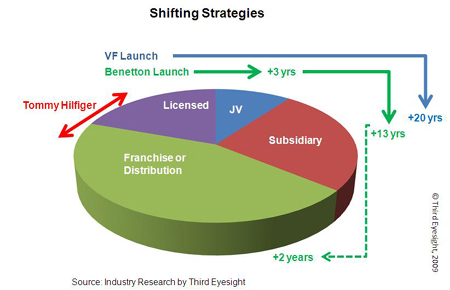

Shifting Strategies

Many international companies have evolved their presence in India into structures different from those at the time they entered the market.

A good example depicting the shift in business strategy is that of VF Corporation which entered India in 1980s by assigning the Wrangler license to Dupont Sportswear. Since then it has launched a variety of brands in different product categories with number of Indian partners and finally formed a joint venture, VF Arvind Brands Pvt. Ltd., with Arvind Brands.

Another example of a company that has evolved its presence is Benetton, which first entered India through a licensee (Dalmia). Benetton then transitioned in 1991 into 50:50 joint-venture and finally in 2004 took over the Indian business completely. However, it adopted the franchising route in 2006 for its premium fashion brand, Sisley, appointing Trent (a Tata Group company) as the national retail franchisee.

Many other companies such as Nike, Tommy Hilfiger, Marks & Spencer and Pierre Cardin (as described in our report “Global Fashion Brands: Tryst with India”) have changed their approach as the original structures did not perform as well as they had expected.

Obviously, each such change has cost the brands time, management effort, money and, sometimes, market share.

We believe that these shifts and the pain related to it could have been reduced, had the brands ruthlessly questioned the motivation for considering this market and their expectations from the market in determining an appropriate strategy.

What’s Ahead?

In the midst of economic upheaval around the world, how does India look as a market for international fashion brands?

Well, it is difficult to generalize even in the best of times. In the current global turmoil there is certainly a lot more unpredictability about international expansion for most companies.

Although India’s position as a target market for international brands has been improving, as is evident from the number of launches in the last 6-7 years, some companies considering international expansion may prefer entering other markets that may seem more “familiar”, developed and safe (such as Europe, Japan, South Korea or Taiwan). Against such comparisons, India’s growing but fragmented market can seem chaotic and difficult to deal with.

However, the fact remains that there are very few markets globally that can provide the sustained size of mid-term and long-term opportunity that India does. We are already seeing the more far-sighted and committed brands consolidating their position and presence in the market by continuing to look at expansion, even while examining how they can make their existing points of sale perform better. We also constantly come across new companies carrying out investigations into the market.

In the current environment we expect to see a shift in the nature of launch vehicle. While franchising seems to be a safe option for risk-averse brands in the current times, we will probably see more brands with a long term strategy, who would establish a controlled presence either through joint-ventures or through wholly-owned subsidiaries, since they can lay the foundation of the business today at much lower costs today than in the past few years.

India’s foreign direct investment (FDI) policy, allowing FDI only up to 51% in retail trading of “Single Brand” may have held back some fashion brands as they are still managed by owner founder with a conservative outlook on “control”. However, in the last couple of years, we have found companies not being deterred by the barriers to FDI.

As their comfort and familiarity with India has grown, international companies are more willing today to create corporate structures that allow them a presence in the market today and a step-through to a more controlling stake as and when government regulations allow.

All in all, we feel that international brands are in India not only to stay, but also to expand. There is yet a lot of potential untapped in the market, and as the integration of the Indian consumer with global trends continues, international brands can expect to find India an increasingly fertile ground for growth.

(c) 2009, Third Eyesight

Devangshu Dutta

April 16, 2009

The recession is taking a toll on the business models of premium and luxury retailers.

According to the Los Angeles Times, faced with sales declines at their full-price stores, Neiman Marcus, Saks Fifth Avenue and Nordstrom are lavishing more dollars and devotion on their outlets which are performing better than their traditional stores.

According to Robert Wallstrom, president of Off 5th, Saks Inc.’s outlet division, “These days, customers are saying they want a brand, customer service and a deal.”

Outlets may just be the lifeboat needed by some of the brands to get through the current downturn, with the mix of the “real steal” deals to get the footfalls and the “just a little off the top” to get the margin. The current outlet stores are good enough to avoid severe damage to the brand.

However, a critical question does remain unanswered: once the consumer becomes used to shopping at a certain price level, might some brands struggle to move back up the curve?

admin

September 22, 2008

The Textile and apparel industry is of particular importance to India. It not only provides employment to a broad base of semi-skilled and unskilled labour but also helps to extend the economic bounty to urban and semi urban areas. Though India has a history of thousands of years in global trading of textile, it contributes only 3% to the global exports of textile and clothing.

While the urge to grow exists, there is a huge difference between the current exports of about Rs. 864 billion (US$ 20 billion) and the target of Rs. 2,500 billion (US$ 55 billion) by 2012. To achieve this vision, exports must grow at around 25-35 per cent a year for the next 4 years, depending on how weak or stable the current year is. This growth rate seems difficult considering the fact India has actually grown its exports of textiles and apparel at an annualized growth of a little over 14 per cent from 2003-04 to 2007-08.

Even if the industry looks at increasing the volume of exports to achieve the vision, the ports do not have the handling capacity considering that they currently operate at 91 to 92 % of available capacity.

Hence, incremental thinking will not help to achieve the vision.

Our key concern is the value “lost” by the industry. Being the low cost supplier does not necessarily translate into greater market share. The Indian Industry must look at enhancing the value delivered rather than competing on the cost platform. Indeed, India compares poorly to other countries on the value captured per employee. (For instance, if the export value captured per employee in India was as much as Turkey, India’s exports would be close to China’s exports of US$ 161 billion.)

One major concern that needs to be addressed is that India’s exports are still weighted in favour of raw materials and intermediate products, rather than finished products. Apparel exports account for only 41% of India’s textile exports in 2007-08. India’s product mix also needs to be aligned to global market needs, rather than only focussing on “traditional strengths” – this includes enhancing the share of non-cotton products in the basket.

Another area that is neglected is the inherent competitive capability of developing new products. The industry needs to develop and nurture these skill sets to create a sustained competitive advantage in the global scenario. India already provides buyers with value in terms of product development and design, which needs focus and further strengthening.

Further, India’s domestic industry, and its skill at understanding market needs, creating and merchandising product, can also play a valuable role in the industry’s growth.

The competitive advantage offered by being able to influence the development of a product is immense. And given that sourcing lead times are shorter in unpredictable times, a supply base that has been involved with the buyer right from the development stage of the product is most likely to get the final order. Third Eyesight proposes a four dimensional model: Define, Design, Develop and Deliver so as to achieve the industry-wide development, of projecting India as a valuable supplier, and sustaining its value needs.

By creating an ecosystem focused on design and product development, India can create and capture the billions of dollars worth of value that is being lost to other countries.

This is an extract from Third Eyesight’s report presented at the FICCI 3rd Annual Textile And Garment conference in Mumbai. The report was released by the Minister of Textiles, Government of India. To download the full report prepared by Third Eyesight, please click here.

To discuss how we can help you with your specific business needs, please get in touch with us via email (please send it to services [at] thirdeyesight [dot] in) or via this form: CONNECT.

admin

August 10, 2008

The Third Eyesight Knowledge Series© comprises of workshops designed and developed to help functional heads, line managers and executives refresh and upgrade functional and product expertise.

Third Eyesight’s next workshop in this series is focussed on Creating & Managing Lifestyle and Fashion Brands.

IS THIS FOR YOU?

This workshop will be useful to you, if you are

THE WORKSHOP CONTENT

This workshop will help participants in understanding:

REGISTRATIONS

Click Here or Call +91 (124) 4293478 or 4030162