admin

September 22, 2008

About Third Eyesight

Third Eyesight is a consulting and management solutions firm focussed on retail and consumer products. Third Eyesight’s professionals have deep and extensive experience in the lifestyle merchandise sectors (such as textiles, apparel, accessories, home, footwear and other products).

Clients that have benefited from Third Eyesight’s experience and expertise include Indian and international retailers, brands and manufacturers, private equity & venture investors, suppliers to the retail sector, as well as government agencies and industry bodies. Third Eyesight has worked with companies that are market leaders (with annual sales of over US$ 80 billion) as well as early-stage and start-up businesses.

Strategy and operational support provided by Third Eyesight for retail and consumer products sectors includes: opportunity scanning, evaluating new business areas, market and industry research, business strategy and business plan development, development of sales and distribution networks, including support with acquiring key client relationships, business due diligence, partner evaluation, strategic alliances, mergers & acquisitions, sourcing and supply chain strategy, merchandising support, operational audits & assessment, training and skill-development, and a variety of other operational support.

Third Eyesight

Tel: +91 (124) 4293478

Website: www.thirdeyesight.in

About FICCI

Set up in 1927, FICCI is the largest and oldest apex business organization of Indian business. Its history is very closely interwoven with the freedom movement. FICCI inspired economic nationalism as a political tool to fight against discriminatory economic policies. FICCI’s commitment is now directed at changing the economic landscape of India, through reforms that expand the space for private sector and public private partnerships. FICCI is the rallying point for free enterprises in India. It has empowered Indian businesses, in the changing times, to shore up their competitiveness and enhance their global reach.

With a nationwide membership of over 1,500 corporates and over 500 chambers of commerce and business associations, FICCI espouses the shared vision of Indian businesses and speaks directly and indirectly for over 2,50,000 business units. It has an expanding direct membership of enterprises drawn from large, medium, small and tiny segments of manufacturing, distributive trade and services. FICCI maintains the lead as the proactive business solution provider through research, interactions at the highest political level and global networking.

In the knowledge-driven globalised economy, FICCI stands for quality, competitiveness, transparency, accountability and business-government-civil society partnership to spread ethics-based business practices and to enhance the quality of life of the common people.

Myth–Busting as an Introduction: Let’s Not Rebottle Old Wine There are many myths that are prevalent among the observers of the Indian textile and apparel industry. Here are a few illustrative ones that point to the need to seriously review of the way the Indian industry competes globally:

Myth # 1 – To grow, India needs to do what China has done:

Comparisons between the two countries are bound to happen, and surely there are some areas for India to learn from China. However, the fact is that India does not have many of the advantages that China had in the past (including a huge business portal in the shape of Hong Kong), nor can it so quickly build the advantages that China has developed over the last 15 years in terms of production capacity, infrastructure etc. India’s political and administrative structure, financial systems, and internal dynamics are completely different. Some obvious internal gaps need to be filled in India’s case, but sustainable competitiveness cannot be built through a copy-China strategy.

Myth # 2 – India is competitive because Indian labour is cheap:

India has low salaries and wages. But studies show that most Indian clothing factories are less productive, possibly even only half as productive as factories in India’s major competitors on the global stage. Add to that inefficient factory management, expensive power, higher financial costs, and costs of bureaucracy and corruption. The true cost of business can be far higher for Indian businesses – and with the market determining the price boundaries for exporters, it’s no surprise that many of them are losing money.

Myth # 3 – Indian handiwork is irreplaceable:

When embroidery was automated, suppliers of embroidered goods from Delhi and its surrounding areas certainly felt the heat but they maintained a competitive edge due to embellished (sequinned / beaded) products that are a staple in the “value-added segment” and that flood the market whenever the “India-look” is in. However, in recent times, machinery manufacturers have developed equipment that can provide the same look. The only difference is that the beads and sequins are stuck on with adhesive rather than being stitched on. The buyer is not likely to care about the production method – after all, the quality and look produced on these machines is more consistent, and the garment is less expensive because the machines have a very high throughput.

Myth # 4 – Compared to China and other Asian giants, the fragmented supply base of Indian manufacturers is more flexible and can competitively fulfil small orders:

For long, the small-scale reservation created a situation where the size of the factory was determined by an investment ceiling rather than by business economics. This base of small factories, by default, fitted into a specific competitive niche, where buyers wanting to place small orders (say, less than 2,000-3,000 pieces in a style) would mostly come to India, as most other factories around the world worked with higher “minimum-order quantities”. However, with retailers switching to the new mantras of quick-response, efficient supply chains and reduced inventory exposure, manufacturers in other countries are now working on much smaller orders.

Myth # 5 – India needs to focus on its core strengths – for example, India has a sustainable advantage in cotton that will maintain its competitive edge:

One of India’s great strengths is one of its greatest weaknesses. Due to its suitability to India’s climate, cotton has naturally achieved a very high share of the Indian production base. However, the global market is skewed in favour of man-made fibres. Cotton accounts for just about a third of global apparel consumption (including blended fabrics where cotton is used along with other fibres). For India to remain a globally-significant player, Indian production and exports must be aligned to consumption patterns – that means a strong thrust in products made out of synthetic fibres, as well as natural fibres such as wool. Similarly, Indian manufacturers need to look at the product range that their customers wish to buy, and identify new areas into which they can enter.

Perspective: India

The textile and apparel industry is of particular importance to India. The sector directly and indirectly results in the largest employment next to agriculture and retailing activity in the country. Its presence is not confined to the urban centres of industry and commerce – the textile sector is the most deep-rooted industry in rural India as well, and has been historically so.

India is one of the world’s oldest major textile suppliers and once was, in fact, the largest by far, with a recorded history of global trading in textiles dating back several thousand years. We treat globalisation as a new phenomenon – the fact is that many thousands of years ago, the Egyptian civilization was trading with the Indus Valley civilization, the Chinese and the Romans had discovered each other way before US department store buyers landed in Hong Kong and Korea.

The textile sector in India started industrialising in the late-1800s and early-1900s, heralding a new era for growth. However, shortly after independence in 1947, the industry was constrained by licensing that limited mill capacity growth and other restrictions that forced companies to remain small-scale.

Later in 1962, just as India’s exports had begun to grow, quota-restrictions closed the gates to free trade, nipping India’s exports in the bud. For years, quotas determined where buyers could place orders, and trade was accordingly channelled and fragmented. Preferential trade arrangements placed further constraints, as both the US and the EU provided duty-free and quota-free access to some countries.

The net result is that India currently has just over 3 per cent of the global exports in textiles and clothing. However, despite its low share, India remains among the Top-10 exporters of textiles and clothing in the world.

After the removal of quotas in 2005, India was expected to grow its share of the global marketplace. However, views varied widely on whether India really had the mettle to stand-up to China – the largest exporter. Some observers and even people from within the industry expected India’s share to decline in global trade.

India has actually grown its exports of textiles and apparel from US$ 13.6 billion in 2003-04 to US$ 20.5 billion in 2007-08, an annualised growth of a little over 14 per cent. During a similar period, China has grown its exports from US$ 95 billion to US$ 161 billion, with an annualised growth rate of almost 20 per cent.

Given the current market share positions, it is unrealistic to expect India to catch up with China any time soon. However, the trend clearly is towards a re-integration of India’s industry with the global trade.

India’s Global Textile and Clothing Trade

Source: Government of India Trade Statistics, Third Eyesight Analysis

We also feel that past perceptions, and prejudices ignore the potential India offers as a sustainable and strategic supply base. Among the Top-5 low-labour-cost clothing suppliers

(China, Turkey, Mexico, India, Bangladesh), only China and India do not have preferential access to their major markets and yet compete very effectively on the basis of their inherent strengths.

The fact that India is one of the few countries in the world that offers:

A vertical industry structure, from fibre to clothing

A large and replenishable low-cost pool of labour

A multi-product capability

Product development skills

A large domestic market that can sustain the industry in the face of global competition

The last is an important and under-weighted factor in the Indian industry’s competitive strategy. Worldwide, countries that have strong sectors for textile, apparel and other lifestyle products, have very strong domestic markets and strong ‘brand delivery’ mechanisms. The focus, in these countries, is not just on production but the entire ecosystem for the industry. We believe that India should be no different.

So far, exporters and domestic-market focussed companies have had very little common ground to work on. As compared to the customers based in the western markets, the domestic market needed very small quantities per style, processes and systems were weak, with high responsiveness required from the supplier – for exporters it was an “unviable” market to step into. On the other hand, for domestic buyers, exporters were far too rigid in their processes, payment terms, minimum quantity requirements etc. That has started to change with the emergence and significant growth of modern retailing in India (the so-called “organised retailing”).

Although many people believe that modern retailing is a recent development in India, the fact is that the textiles and apparel sector has been at the forefront of its development since the 1950s-1960s, when the first chains started coming up. In about 30-years significant single-branded dealer-networks (now widely morphed into exclusive branded outlet chains and franchise networks) were built by textile and then apparel companies.

However, since the mid-1990s, there has been significant and visible development in the domestic market for textiles, apparel and other lifestyle products. Large retail chains have begun appearing, and new platforms have emerged for apparel and textile companies to grow their business domestically. The large Indian retailers’ requirements have more in common with western retailers and brands (the customers for India’s exporters) than ever before. This provides an opportunity for the two sectors to work more closely together.

Thus, with its long history, and these two growth engines – the export industry and the domestic market – we believe the Indian textile and apparel sector can retain its significant role in the country’s economy, and create a differentiated position among global trade that is sustainable into the future. However, as the global economic growth slows, the domestic economy follows and inflationary pressures push up the cost of doing business, fresh thinking is also needed to keep the sector in growth mode.

The other urgent driver is the vision of what India’s export numbers could potentially be by 2012: Rs. 2,200-2,500 billion. The number currently stands at a little over Rs. 864 billion, and to achieve the vision, exports must grow at around 25-35 per cent a year for the next 4 years, depending on how weak or stable the current year is.

India’s Textile and Apparel Exports (Rs. Billion)

Let’s not debate whether this vision is achievable or not. The purpose of a vision being articulated is to drive the actions that will help in achieving it.

What is very clear is that this vision is not “incremental” in nature, and incremental thinking will not help in realising it.

Even if we assume a robust incremental growth rate of 15 per cent per annum, India’s exports will only be able reach Rs. 1,500 billion by 2012.

If this vision is to become reality, if India’s textile and apparel industry is to change from being (as described by the head of an international company) “the eternal hope” to a true global leader, the industry and the institutions supporting it, including the government need to put in place a radically different course of actions.

This report is not being presented as a definitive strategy document for the Indian textile and apparel industry, or for the Government to mould its policies. However, it does attempt to present a view on historical and recent developments, the constraints that the industry cannot wish away and must, therefore, embrace, and also to highlight the factors that can create a sustainable competitive advantage for India as a leading global resource of textiles and apparel products.

A Health Check on the Indian Industry

While the All-India Index of Industrial Production registered an increase of 8.1 per cent during April-March 2007-08, as against the corresponding period of the previous year, the growth of textiles sector was slow.

Although Jute & other vegetable fibre textiles (excluding cotton) registered significant growth (33.1 per cent), the other textile sub-groups showed small growth rates. Wool, Silk & Man-made fibre textiles registered a growth of 4.2 per cent followed by Cotton Textiles (4.1 per cent) and Textile Products [including wearing apparels] (3.3 per cent) as against the corresponding period of previous year.

According to Ministry of Textiles, during fiscal 2007-08, spun yarn production increased by 4 per cent and cloth production increased by 3.9 per cent. The handloom sector recorded the highest growth (6.0 per cent) followed by the power loom sector (4.5 per cent).

The Indian textile industry is export-weighted, with almost 55 per cent of the total production being exported. The US market is the largest destination for Indian textile and apparel exports. The recessionary trend in the US and relentless ascent of the rupee led to a decline in the total trade with India in 2007, resulting in smaller orders, lower prices and deep uncertainty for apparel exporters.

Indian exporters are now trying to increase their share in EU market and diversify to other markets other than US. However, the market scenario in most major global markets is looking grim in the short term.

Though the dollar’s appreciation this year should have brought a breather to exporters, the benefits of a weaker rupee has been offset by the surge in costs and the global economic slowdown. India’ textile & clothing companies’ margins are under severe pressure due to rising cost of raw material, fuel, real estate and more expensive credit.

In addition, many of India’s competitors have recently enhanced their export incentives in the context of declining demand in the US and EU markets. For instance, China has increased VAT refund rates from 9 per cent to 13 per cent for synthetic textiles and from 11 per cent to 13 per cent in case of others. Pakistan has introduced Research & Development assistance of 6 per cent for garments.

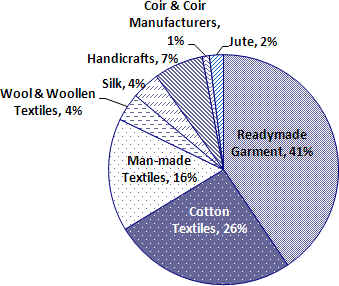

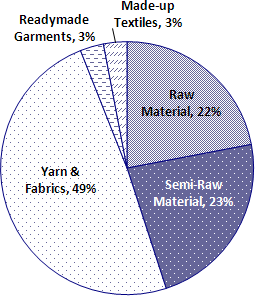

Clearly, India’s exports are still too weighted in favour of raw materials and intermediate products, rather than finished products, and this is a major concern if one looks at the long-term competitiveness and value-capturing capability of the industry.

Imports have also begun to grow in India, although the numbers are still small. Import of fabrics and other products for conversion into clothing has been allowed duty-free for several years, and now imports are also growing for domestic consumption.

Imports up to April-February 2007-08, indicate an overall increase in both, rupee terms and in US$ terms, to 3.78 per cent and 16.71 per cent respectively. Imports of Readymade Garments (RMG), Made-ups and Raw Materials increased by 36.80 per cent; 28.93 per cent and 11.75 per cent respectively, in rupee terms, over the corresponding period of the previous year.

Send download link to: