admin

February 28, 2011

![]() Business

Standard, Mumbai, February 28, 2011

Business

Standard, Mumbai, February 28, 2011

![]() Sayantani

Kar (with inputs from Preeti Khicha)

Sayantani

Kar (with inputs from Preeti Khicha)

When some of India’s big retail chains banded together recently to substitute Reckitt Benckiser’s products with private labels to protest the latter’s decision to cut sales margins on its products, they were doing something many global retailers have done with great success. Part of their overall strategy, especially for large chains in the US and Europe, is to develop quality private label products that complement other pieces in their marketing mix. While this is one way retailers can differentiate their firms from competition, it also helps them flex their muscles in their relationships with brand manufacturers. Indeed, retail giants Tesco, Walmart and Carrefour have a significant portion of their sales coming from private labels — ranging from 10 per cent for Costco and 50 per cent for Tesco.

India is a back runner in the private label race, but it is

catching up. A Shoppers Trend Study by Nielsen found awareness

about private labels has gone up from 64 per cent in 2009 to 78

per cent in 2010 across 11 cities in India. Nielsen Director (retail

services) Siddharthan Sundaram says, “Over the last three

to four months, we found an increased awareness of private labels

in categories such as staples, household products, personal care

products such as soaps, biscuits and packaged groceries.”

Thanks partly to the recent economic downturn, there is greater

acceptance — and even loyalty — to such brands in India,

say marketers. Future Group Business Head (private brands) Devendra

Chawla reasons, “A label on the shelf becomes a brand by

covering the two feet distance from the shelf to the trolley.

After all it is the consumer’s choice.” Even in the

toughest segment for private labels to crack — fast moving

consumer goods including food and personal care — store labels

claim share of 19-25 per cent.

Low-involvement categories such as household cleaners were among the first to see the entry of private labels (17-44 per cent of sale in modern trade), bringing in huge margin-lifts for modern retailers. In categories such as food products — jams, biscuits and staples — private labels today contribute more than 25 per cent of modern trade sales. Little wonder, retailers are now mining shopper data to make private labels shed their ‘low’ly tag — low involvement and low cost. Store chains are segmenting their brands according to consumer needs, combining more than one brand according to consumer behaviour, besides launching high-involvement premium products and innovative packaging to give national brands a run for their money.

Innovate or die

Retail innovation has had a big role to play in speeding up the

process of consumer acceptance. Future Group’s retail arm,

which includes Big Bazaar and Food Bazaar, calls its in-house

products ‘private brands’ not labels. It has a separate

team, headed by Devendra Chawla, to research and test FMCG products

before launch. The team has a range of private brands — Tasty

Treat, Fresh and Pure, Cleanmate, Caremate, Sach, John Miller,

Premium Harvest and Ektaa. Look at how it is using shopper data

to improve its products. The insight that kids found ketchup bottles

cumbersome and had to be served — making it inconvenient

if an adult was not around — led it to change the packaging

that in turn gave the brand a margin advantage. By offering ketchup

in pouches, it saved on the price of the glass bottle and freight

(pouches take up less space in a truck, hence more can be fitted

in). While ketchup in glass bottles continue to be Rs 99 for a

kilo, its Tasty Treat ketchup pouches come in Rs 59 packs.

By working with vendors it has also come up with interesting combinations — for example, its Tasty Treat jam has three small tubs packed as one unit, each tub containing a different flavour to offer consumers larger variety.

Retailers have now donned the hats of “product selectors” and “product developers” at the same time, points out Third Eyesight CEO Devangshu Dutta. “So far, most of the retailers were just selecting products from vendors which are mostly lower-priced knock-offs of manufacturer brands,” he says. Not any more.

Ashutosh Chakradeo, head (buying, merchandising and supply chain), HyperCity Retail, explains the process his company follows: “To develop food products, we identify vendors, tie up with food laboratories, chefs and consumers to be part of the tasting panels. Before launching a private label we do at least a month of consumer testing. We identify customers from our loyalty programme called Discovery Club, which tells us who buys a certain category of product. We give the relevant consumers our private label products for trial for a month. We meet the customers at their homes, take their feedback and these changes are incorporated into the private label brand.”

“Our stores act as research labs and are a constant source of feedback,” points out Chawla of Future Group. Chawla estimates 3-4 per cent of the sales of private labels are ploughed back into packaging and design innovation. Reliance Retail CEO Bijou Kurien says, “The teams are our main investment in private labels. Our 100-strong designers across all the formats help in coming up with product designs that fill a need gap or offer a few more features at the same price as national brands.” Reliance Retail has recently launched its own brand of watches priced Rs 149-199 which “no national player can offer” points out Kurien.

The edge

Most vendors directly supply to retailers’ distribution centres,

cutting out cost leakage at the distributor’s and carrying

and forwarding centres. Direct access to store shelves and aisles

also cuts out the high mainstream advertising costs that brands

have to bear. By clever product arrangements and in-store promotions,

retailers can sway the shopper and draw attention to the price

advantage. Chakradeo says, “We display private labels in

heavy footfall areas in the store. We complement displays —

so we keep our private label ketchup near the bakery.”

To tackle the tricky personal care category of face creams and shampoos that Aditya Birla Retail’s More chain has entered, it plans to communicate promotional offers straight to its loyalty programme members. “It will help us induce trials,” says Thomas Varghese, More’s CEO.

Bundling products is another way to woo the value-conscious consumer. Six months back, Future Group started bundling its private brands. Chawla says, “Take home-cleaning, which requires a floor cleaner, glass cleaner, toilet cleaner and utensil cleaner which we combined as a shudhikaran solution of our Cleanmate brand.” The combi-pack costs Rs 125, which would come to around Rs 220-250 if shoppers bought a la carte. The margins are still high at 26 per cent. “Vendors are assured of volumes,” points out Chawla.

What it also does is convert the fence-sitter who has not yet bought into a category. For example, consumers who avail of the shudhikaran solution also get into the habit of using glass cleaners — a category which has a small base and gets most of its sales from modern trade. Similarly, Future Group saw a 25 per cent spurt in the sales of soups when it clubbed soup mugs with its Tasty Treat soup packets based on the insight that Indians preference to sip their soup out of a coffee mug.

Don’t be surprised if you see MNC brands coming out with combo-offers for their products, way bigger than the occasional bucket with a detergent!

Growing up

There are signs the industry is evolving. Private labels in FMCG

are shedding their low-cost tags. But retailers know better than

to vacate low price-points altogether. Instead, they are segmenting

their brands just as a manufacturer brand would do. Chakradeo

of Hypercity says, “Over a period, we hope to increase the

stickiness and the differentiation our brands bring to our stores.

Particularly, in staples where we have seen our private label

business grow rapidly. This is a very quality and price-sensitive

category. We started with basic products but now we have premium

daals (lentils) and basmati rice as part of our portfolio.”

Future Group too has its ‘good, better, best’ policy firmly in place. In staples, the stores offer some products ‘loose’, such as rice, wheat, lentils, which is at the bottom of the ladder. Its Food Bazaar version of the products straddle the middle category, and above the two is its brand, Premium Harvest, which retails at a price higher than some manufacturer brands.

Stickiness may also result from the manner in which retailers are positioning their brands. Future Group’s brand Ektaa will retail regional food and staples across its stores in the country so that migrants can buy supplies they are comfortable with. Be it Govindbhog rice and kasundi (a rice variety and mustard sauce preferred by Bengalis), khakra (Gujarati snack) or murukku (loved by Tamilians). Boston Consulting Group Partner & Director Abheek Singhi says, “Indian retailers are not cut-pasting private label products from other markets but adapting them.”

Are private labels a risk worth taking? Chakradeo says, “The entire product formulation for our cleaners was done in partnership with Dow Chemicals, USA. We did not make any investment and we gave them a percentage of sales as fee. Investments are not huge in making private labels as in most cases it is partnered with vendors. It is more of operating expenses than capital expenditure.”

Future Group brought down logistics costs further by 6-8 per cent by appointing vendors in more than one region for 10 of its product categories to fill its distribution centres. Chakradeo adds, “As the volumes go up, we will be able to put up for backend infrastructure facilities for development and R&D.”

Should national brands be worried? Devangshu Dutta says, “As long as retailers have access to the production and development and have customers for it, the private labels will remain profitable.” India Equity Partners Operating Partner V Sitaram sums up, “In modern trade, though the market leaders will face some slip in market share, the number 3 or 4 brands might have a bigger problem in certain categories thanks to private labels.”

As retailers leverage consumer insights to deploy private labels more effectively, national brands are aggressively fighting the challenge. From sprucing up supply chains to galvanising in-store promotions, they are covering all bases. KPMG Executive Director Ramesh Srinivas says, “Earlier brands had to adjust between a modern trade and a general trade supply chain. The former had to be serviced directly at the stores or had their own supply chain while the latter used the manufacturer’s supply chain. Now, some brands separate modern trade teams and even distributors.”

Britannia Category Director (delight and lifestyle) Shalini Degan says, “We have divided our portfolio into three categories, A,B,C, each having its benchmark fill-rate. We don’t allow fill-rates to drop below those levels. Why the segmentation? We need to focus on brands which have a higher traction in modern trade when servicing it, else we might end up focusing on brands that are not modern trade-led.”

Fill-rates denote how often and to what accuracy the retailer’s orders for a product are supplied by the manufacturer. Low fill-rates could mean lost opportunity since the shopper sees an empty shelf or a private label instead of the brand she might have thought of picking up.

Samsung Vice-President and Business Head (home appliances) Mahesh Krishnan says, “We have gone in for central billing system 4-5 months back with all large-format retailers. Orders are tracked on a daily basis giving retailers more control over the chain.”

In other words, private labels are here to stay and will evolve as more and more chains gain national footprint and the economies of scale kick in. Dutta of Third Eyesight says, “Gross margins for organised retailers are still low compared to global standards: So, margin fights will continue for some time till retailers gain a bigger share of the pie.”

(Also read: The Private Label Maturity Model.)

admin

January 7, 2010

By Tarang Gautam Saxena, Chandni Jain and Neha Singhal

In Retrospect

While India was a promising market to many international brands, it was not completely immune from the global economic flu. More than its primary impact on the economy, the global downturn sobered the mood in the consumer market. Even the core target group for international brands, that had just begun to splurge apparently without guilt, tightened their purse strings and either down-traded or postponed their purchases.

In 2008 in the midst of economic downturn, skepticism and uncertainty, the international fashion brands had continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008 targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many players ended up discounting the goods heavily to promote sales while a few also gave up and closed shop.

As the Third Eyesight team had foreseen last year, 2009 saw a further slowdown and fewer international brands being launched during the year. The brands that were launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack and Timberland. Some of these had already been in the pipeline for quite some time and invested a considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

International Fashion Brands in India

After many deliberations, the well-known global brand Donna Karan New York set foot in the Indian market in 2009 through an agreement with DLF Brands to set up exclusive DKNY and DKNY Jeans stores India. The brand is also reported to have signed a worldwide licensing agreement with S Kumars Nationwide Ltd to design, manufacture and retail DKNY menswear in certain specific countries.

Second Chances

Amongst the international brands that have recently entered the Indian market, a few are on their second or even third attempt at the market.

For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills, and the partnership intended opening 15 stores by 2010. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis on retailing international brands within the country. Within a few months of the ending of this relationship, Diesel signed a joint venture with Reliance Brands for a launch scheduled for 2010. Both partners seem to be strategically aligned with a common goal as the international iconic denim brand wants to take on the Indian market full throttle and the Indian counterpart has indicated that it wants to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008, despite plans to open more than 50 stores in the first three years of operations. Miss Sixty has finally entered India through a franchise agreement with a manufacturer of women’s footwear and accessories. The company has currently introduced only shoes and accessories category and is looking at potential partners for its label Energie and girls’ range Killah.

Other brands that have re-entered the Indian market include Germany-based Lerros whose first presence in India was back in mid-1990s. The brand re-entered the market in 2008 through own brand stores and is growing its presence through this route as well as through multi-brand stores.

Oshkosh B’gosh is another brand that had entered India in mid 1990s, through a licensing agreement with Delhi based buying house, Elanco. The licensee found the childrenswear market hard to crack, and closed down. In 2008, Oshkosh re-entered the Indian market through a licensing partnership with Planet Retail and is now available through shop-in-shop counters at Debenhams stores. Reports suggest that it may consider setting up exclusive brand outlets.

During the turbulence of 2008 and 2009, a few brands also exited the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both) to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations and for the amount of effort and money being invested, and that it was better to pull the plug.

Some brands that have been pulled out of the Indian market during 2008 and 2009 include Dockers, Gas, Springfield and VNC (Vincci). Gas (Grotto SpA) is reported to remain interested in the market but has not found another partner after its deal with Raymond fell through in 2007 and all dozen of its standalone stores were shut down.

The Scottish brand Pringle and its Indian licensee did not renew their agreement upon its expiry. The Indian partner has reportedly signed an agreement to launch another international brand in India, while Pringle is said to be looking for new licensee.

The good news is that successful relationships outnumber every exit or break in relationship possibly by a factor of ten. Some of the brands that have sustained are among the early entrants having a presence in India since the late-1980s and 1990s or even earlier. These include Bata, Benetton, adidas, Reebok (now also owned by adidas), Levi Strauss and Pepe. Having grown very aggressively during 2006 and 2007 Reebok quickly became the largest apparel and footwear brand in India, while Benetton and Levi’s are expected to cross the $100-million mark for sales this year.

Entry Strategy & Recent Shifts

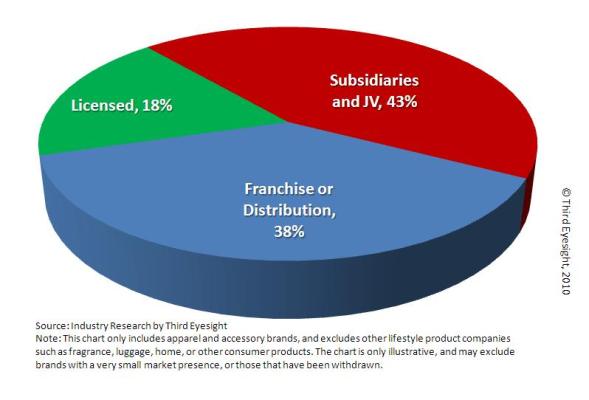

As envisaged in Third Eyesight’s report from a year ago, with changing market conditions and a growing confidence in the Indian market, there has been a shift among international brands in the choice of the launch vehicle. While franchising has been the preferred mode of market entry in the recent past for risk-averse brands, more brands today demonstrate a long-term commitment to the Indian market, and are choosing to exercise ownership through wholly or partially owned subsidiaries and through joint ventures.

In 2009, we have seen a noticeable shift in favour of joint-ventures as the choice for entry into the market. Even the brands already present are looking to modify the nature of their existing presence in India in order to exert more control over the retail operations, products, supply chain and marketing.

Current Operating Structure

(End 2009)

Brands that changed their operating structures and, in some cases partners, in recent years include VF (Wrangler, Lee etc.), Lee Cooper, Lee, and Louis Vuitton amongst others.

Mothercare, the baby product retailer, which is present through a franchise agreement with Shopper’s Stop has, in addition, recently formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores. Gucci, which had initially entered in 2006 with the Murjani Group as a franchisee, has recently changed over to Luxury Goods Retail, and is now in the process of restructuring the relationship into a joint venture.

VF has also been reported to be looking to license Nautica, Jansport and Kipling to a new partner. Until now, these brands were handled through the joint venture with Arvind Brands. Arvind has increasingly focused on its core business, closed stores and scaled down expansion plans for the international brands.

Burberry that had entered India in 2006 through a franchisee arrangement with Media Star opened two stores under this arrangement. It has now set up a new joint venture with Genesis Colors and plans to open 20 stores across the country.

More recently Esprit has also been reported to have approached Aditya Birla Nuvo to deepen its engagement by moving from its distribution arrangement into joint venture as the international brand sees excellent potential in the Indian market.

Buckling up for 2010

Throughout 2009, the one fact that became clear was that the Indian market was resilient. Now, as the global economic condition stabilizes, confidence levels of brands and retailers in India have also improved.

Several launches are already expected in 2010, and possibly many more are being worked upon. In the following 12 months, consumers can expect to find within India acclaimed brands such as Diesel, Topman, Topshop and the much-anticipated Zara. Many more Italian, British and French brands are examining the market.

Most of the international fashion brands already present in the market are also projecting a cautiously upbeat outlook in their plans, while a few are looking positively bullish.

For example, Pepe, an old player in premium and casual wear segment, has reported plans to grow its retail network further and open 50 more franchise stores by September 2010. Similarly the German fashion brand S. Oliver that entered the Indian market in 2007 is looking to grow significantly. It has already moved from a franchise arrangement with Orientcraft to a joint-venture with the same partner, and has stepped up its above-the-line marketing presence. The brand has recently reported its plans to scale up its retail presence to 77 stores by the end of 2012 while also strengthening its presence through shop-in-shop in multi-branded outlets in high potential markets.

Those international brands that have tasted success have not achieved it by blindly importing business models and formulas from other markets. Most have had to devise a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched. These include The Body Shop which decreased its prices by up to 30% this year, and Marks & Spencer which reduced prices by 20-40%. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

On the operational side, the good news for retailers and brands is that the average real estate costs have reduced significantly, although marquee locations remain high. In several locations lease models have also moved from only fixed rent to some form of revenue sharing arrangement with the landlord. And, while the sector has seen some employee turmoil as many non-retail executives who came into the business in the last 5-7 years have returned to other sectors, employee salary expectations are also more realistic.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s recent work with international brands’ business units in India highlights the international players’ concern with ensuring a consistent brand message, improved organizational capabilities right down to front-line staff, and focus on unit productivity (per store and per employee).

We may yet see a few more exits, and possibly some more relationships being reshuffled and partners being changed. However, all things considered, we can look forward to a net increase in the number of international brands in the country.

The Indian consumer is certainly demonstrating more optimism and as far as there are no major unforeseen global or domestic shocks, this optimism should translate into a healthier business outlook for international brands as well. According to early signs, 2010 could be an excellent curtain-raiser for a new decade of growth for international fashion brands in India.

[The 2009 report is available here: “International Fashion Brands – India Entry Strategies”]

(c) 2010, Third Eyesight

[Note: This report is based on information collected from a combination of public as well as proprietary sources, and in some cases may differ from press reports. However, no confidential information has been shared in this report.]

Devangshu Dutta

October 23, 2009

Trade, of course, has been global for millennia, so it seemed hardly unusual for retailers in the US, and in Europe to begin sourcing from distant countries in Asia where certain items were more readily available or significantly cheaper. Imports have also been encouraged as a political and developmental vehicle to aid friendly countries.

So, on the sourcing-end, large retailers have been comfortably operating beyond international borders for several decades even while the stores-end of their business was entirely domestic.

For most large modern retailers however, after the post-Second World War economic boom their core markets have grown relatively slowly (and rather predictably). While the sheer size of the US market kept American retailers busy domestically, planning and legal restrictions in terms of store size, locations, market share etc. limited manoeuvrability for retailers in Europe.

Among the current major retailers, the early retail explorer, Carrefour set out into neighbouring Spain in 1973 and then into distant Brazil in 1975. Soon after, Dutch retailer Ahold landed in the USA in 1977.

However, it took the opening up of East European economies in the 1990s to really prime the pump for growth of international retail. Suddenly, many more millions of consumers became available to European retailers close to their existing markets – both geographically and culturally – and western European retailers jumped at the opportunity.

At the same time, China seemed to have become steadily more open over the previous decade and in the early-1990s India looked accessible again. Some of the Latin American markets were also steaming up.

And, obviously, the prospect of 3-4 billion new consumers in emerging or developing markets was clearly not going to be ignored. In 2001, post dot-com, another inspiring idea hit the business world that was desperately looking for hope – the golden BRICs – the four countries focussed upon by Goldman Sachs as the biggest economies of the future: Brazil, Russia, India and China.

As incomes grew in these “developing” or “emerging markets”, the hypothesis was that consumer would want products and services similar to those in the more developed markets, creating the opportunity for retailers to cross borders. In the last 15 years or so, retail internationalization (and gradually “globalization”) has become an increasingly acceptable theme – in conceptual thinking, in retail boardrooms, in white papers, and finally in trade and mainstream media. The world has witnessed a network of retail subsidiaries, joint-ventures, franchise and other relationships spreading across continents.

Certainly, through the 1990s and 2000s, growing tele-connectivity, fashion, portable TV programming concepts, movies and print media seemed to give the impression that consumers around the world are becoming more similar, and can be reached by common formats and brands. Led by the FMCG companies on the one hand and fashion brands on the other, insights, concepts, products, formats, advertising campaigns are routinely extended across countries. (Unilever’s TV commercial for Close-Up in West Asia is a great example of this – an Anglo-Dutch company’s international brand of toothpaste, Indian models in Thailand, an Arabic voiceover and a Hindi song (“Paas Aao” – “Come Closer”) by Sona Mohapatra – surely you don’t get more global than that?)

But wait! Is the picture really as clear as that?

In 2006 Wal-Mart pulled the plug on its €2 billion German business that was a combination of German chains that it had acquired. In Russia it still has only a development presence since 2005, though it is reported to be looking at opening 10-15 stores in the following three years. According to Newsweek, Wal-Mart’s 13 year old Chinese business – even after an acquisition that is still to be approved – will have fewer stores than it would have opened in the US just in 2009. In the past it has struggled in Japan and Brazil.

In June 2009, Carrefour opened its first 86,000 sq. ft. hypermarket in Moscow, and a second one soon after that. In September, the company affirmed that the BRIC markets were its highest priority for international growth. However, in October it announced that it was pulling out of Russia. Within 4 months of the first store, Russia has gone from a market with “outstanding long term potential” to being a market to exit. In previous years the company has moved out of Japan, South Korea and Mexico. The Economist reports that significant Carrefour’s shareholders are forcing it to look at selling its Chinese business as well – obviously a move that would be politically very sensitive in China. The same shareholders are also reported to be urging a sale of its Latin American business. For now, the official statement from the company maintains an ongoing interest in all these markets.

Ikea has decided to freeze further investments in Russia, and has decided not to enter India until the Indian government allows 100 per cent foreign ownership of retail operations. It entered China in 1998, and has only 7 stores so far.

Even as Carrefour and Ikea announce plans to pull out of Russia, Russian retailers have pulled out from Ukraine, while Metro is cautious in its outlook about that country. French retailer Auchan has opened three stores in Ukraine since 2007, while the German retailer Rewe has opened all of nine since 2000.

Could the juggernaut of global retail be slowing, stopping or even – shock! – reversing? Are the BRICs and emerging markets falling out of favour?

Before we jump to conclusions, as they say in the television world: please don’t adjust your sets. As the French author Karr wrote: “plus ça change, plus c’est la même chose” (the more things change, the more they are the same).

It is a fact that, no matter how international or global a company becomes, when it gets to the business of retail, it needs to be intensely local. While elements of the business – concepts, products, people, money – can travel across borders, it is extremely difficult to take across an intact retail mix and expect to address a significant portion of the population in the new country. And given how important scale is to mass retailers, lack of localization would be a significant hurdle.

A company sourcing products from a developing country can fully expect his suppliers to adapt to his practices and customs. On the other hand, the same company entering that country as a retailer needs to do exactly that – adapt to the customers – rather than expecting them to fall in line because the “best practice” manual dictates certain processes or because central merchandising found some deals that were great for the home market which are totally irrelevant in the new market.

However, there are encouraging signs that retailers looking to grow internationally understand this more and more. Tesco, for one, has been following a localized approach in Thailand and South Korea, while Carrefour, Ikea, Wal-Mart have all steadily modified their approach in China and other markets. Wal-Mart’s cautious steps in India, including the stores opened by its joint-venture partner Bharti, are a complete contrast to the aggressive “plans” that were being reported in the press 2006-onwards. Recently Wal-Mart’s international chief C. Douglas McMillon was quoted by BusinessWeek as saying “we know you can’t run the world from one place”.

For the larger international retailers this means that, the benefits from international scale would be limited by the amount of localization that they carry out in their operations. For smaller and local competitors that are based in an emerging market this means a fighting chance to remain in business and even remain market leaders.

Lastly, as far as all the dark clouds gathered over international retailing and all the retreats being announced – stay tuned – this weather will change, too.

Devangshu Dutta

July 16, 2009

The grocery market is loud. From the times when food markets were in streets and town squares, hawkers have cried out their wares, and the freshness or newness of everything made evident to the customers passing by. So, I guess, it is no surprise that today’s FMCG and food market is also tuned to high-decibel promotion.

You don’t need to search too long for the reason – margins are generally thin on these frequent-use products and inventories need to move fast. And what you don’t make a noise about may not be visible to the customer and may remain unsold.

But if that was the whole story, most players should be focussing on one brand, or at most a few brands, and should be using their advertising budgets to maximum effect on these.

Instead we see exactly the reverse phenomenon in the market – more brands, more sub-brands, more varieties of everything. Why? Because newness sells – it creates excitement, anticipation, and in customers with a sense of experimentation it creates the urge to buy.

The old proven method of doing this was the “New Improved” starburst on the pack. The slicker, updated method is to launch a new variety that is apparently different in some way. For instance, if the old supplement helped to strengthen bones, the new line might contain separate “child” and “adult” versions (growth vs. osteoporosis). The old shampoo might have helped to keep hair clean and prevent dandruff – the new one might leave the customer wondering if she should pick the dandruff-fighter that also reduces hair loss, or the variety that makes her hair glossy, or even the one that provides a date for the next weekend! By the time she reaches the end of the shelf, she might have forgotten that her need essentially was to prevent dandruff.

Due to this, the grocery and FMCG product mix is fractal. Each grocery shelf or grocery store is susceptible to fragmentation. Each such fraction is supposed to act as the seed that can allow a new segment in the market or a new use occasion to grow, and provide the FMCG company or the retailer with an avenue for additional business. This phenomenon is particularly visible in a growing consumption environment – consumption feeds proliferation, while proliferation provides further occasions to consume.

However, an unfortunate outcome of this proliferation of brands and SKUs is the heightened noise, in which the brand often loses its unique voice. Also, over time, the brand may be too thinly spread or be undifferentiated from its competitors, and its sales only sustained through ever increasing bouts of expensive advertising – a vicious spiral.

Another issue is the real estate availability and the cost. Chris Anderson wrote about “the long tail” about 5 years ago – the myriad products for which the market is limited, but demand may be sustained over a long period of time through internet sales. However, while the long tail works for e-commerce businesses such as Amazon that carry limited inventory, the physical store runs out of space for micro-segment items very quickly.

All of these factors obviously start hurting visibly when the market turns down, and when marketing investments start being evaluated against the returns. This is when proliferation starts giving way to “rationalization”, reduction of the brand portfolio, narrowing the SKU focus.

We are already seeing signs of this in many of the developed modern retail markets currently, where retailers and their suppliers are closely analyzing which parts of their portfolio they need to sustain, and which they need to drop.

The story in the Indian market is slightly different for a variety of reasons.

First, the market is still growing, and for most FMCG suppliers there are vast expanses of the market are still blank canvases.

Secondly, India has been a branded supplier driven market for a long time, and remains so, by and large. However, the SKU and brand density is nowhere close to what is seen in the West. There is plenty of headroom still for new varieties to be added and new brands to be developed.

But possibly the most important factor is the new modern retailers, who are desperately seeking additional sources of margin. When there is a limit to the traffic that you can divert from traditional mom-and-pop stores, and when you hit the glass ceiling on transaction values per customer, proliferation becomes the game to play. Therefore, these retailers are either busy introducing own labels or encouraging new branded vendors who would offer them higher margins than the more established brands.

Own label is obviously the tricky one. The customer needs to feel comfortable with the switch – in the US, a study showed that consumers would more easily switch to own label merchandise in categories where the “risk” was perceived to be low (such as household goods, rather than children’s products). Also, the best own label gross margins typically come from products that are presented to the consumer as “brands” comparable to national branded products, because the pricing is more on par.

So, on the retailer’s part, this requires sophistication of product development and brand management that may be expensive and may need time to develop. A short-cut could be the acquisition of an existing brand, its entire assets including the organisation, as some retailers have been reportedly looking to do. How well they integrate the brands into their businesses remains to be seen.

In the long term, like their counterparts in more developed markets, these retailers may also come to the point where they wonder whether these owned brands offer them enough return on the expense and the management effort spent on them, or whether they would be better off just buying brands that consumers are already familiar with through multiple channels.

In the short term, however, we can expect proliferation, fragmentation, fractalization in all its forms. We can expect the illusion of plenty of choice to continue driving sales, and more and more products to fulfil needs that even the customer doesn’t know he has.

Devangshu Dutta

April 27, 2009

Retailwire.com prompted a discussion on what, if anything, should grocers and other stores be doing to accommodate the growth in stay-at-home dads?According to the US Bureau of Labor Statistics, the recession is putting more men out of work than women, which has led to an increase of stay-at-home dads who are increasingly taking on the traditional women’s roles of childcare, housework, school life, and shopping.

Here’s my contribution to the Dad wishlist: salespeople who don’t look down their noses when asked a (“stupid”) question Mom would never have dreamt of asking. (Also, considering this is the gender that apparently never stops to ask for directions, please treat the question as close to a life-or-death emergency.)