Devangshu Dutta

October 12, 2013

Much has been written about the various relationship break-downs that have happened in the Indian retail sector in recent years. The biggest, most recent high profile ones are between Bharti and Wal-Mart and the three-way conflict playing out at McDonald’s. Other visible ones include Aigner, Armani, Jimmy Choo, and Etam, while Woolworth’s faded away more quietly because, rather than being present as a retail brand, it was mainly involved in back-end operations with the Tata Group.

I think it’s important to frame the larger context for these relationship upsets. Most international companies, non-Indian observers as well as many Indian professionals are quick to blame the investment regulations as being too restrictive, and being the main reason for non-viability of participation of international brands in the Indian consumer sector.

However, India with its retail FDI regulations is not the only environment where companies form partnerships, nor is it the only one where partnerships break up. Regulations are only one part of the story, although they may play a very large role in specific instances. In most cases, FDI regulations are like the mother-in-law in a fraying marriage: a quick, convenient scapegoat on which to pin blame.

Many of the reasons for breaking up of partnerships can be found in the reasons for which they were set up the first place. The main thing to keep in mind is that the break-down is inevitably due to the changes that have happened between the conception of the partnership to the time of the split. The changes can fall into the following categories, and in most cases the reasons behind the break are a combination of these:

According to Third Eyesight’s estimates, more than 300 international brands are currently operating in the Indian retail sector across product categories, if we just count those that have branded stores, shop-in-shop or a distinct brand presence in some form, not the ones that merely have availability through agents or distributors.

Of these, about 20 per cent operate alone, while other others work with Indian partners, either in a joint-venture or through a licensing or franchise arrangement. The relationships that have broken up in the last decade are only about 5 per cent of the total brands that have come in, and in many cases the international brand has stayed in the market by finding a new partner.

So there’s life after death, after all. And my advice to those who’re feeling particularly defensive or pessimistic because of a few corporate break-ups: take time for a song break. Fleetwood Mac (“Don’t Stop”, “Go your own way”) or Bob Dylan (“Don’t Think Twice, It’s All Right”) are good choices!

Devangshu Dutta

October 9, 2013

[This article appeared in Daily News & Analysis (DNA) on 10 October 2013, under the headline “Without Wal-Mart, can Bharti play it alone?”]

A year ago, Wal-Mart had called Bharti its natural retail partner in India. But today the companies have jointly and publicly changed their relationship statuses to “single”, calling off the 6-year old marriage. Bharti will buy out or retire Wal-Mart’s debentures in the 200+ store Easyday retail business, while Wal-Mart in turn will acquire Bharti’s stake in the 20-outlet Bestprice cash-and-carry business.

By some estimates, the split was imminent for perhaps a year or longer, as the pressure rose for the two companies due to multiple factors. Several regulatory changes governing foreign investment in the Indian retail sector made it difficult for Wal-Mart to acquire a stake in the existing retail business that the two partners had set up. Anti-corruption investigations in Wal-Mart’s India business (in addition to Mexico, China and Brazil), as well as questions around the legality of US$ 100 million worth of quasi-equity compulsorily convertible debentures issued to Wal-Mart at a time FDI was not allowed in multi-brand retail businesses brought down even more external scrutiny upon the joint business. And finally, pressure against foreign investment in multi-brand retail of basic goods such as food and grocery, continued to exist not just amongst opposition parties but also parties within the ruling coalition and individuals in the government.

The split means that Wal-Mart can now overtly take complete ownership of the Bestprice business, and drive it as it sees fit. The fragmented retail market and the myriad small businesses in India do potentially provide a large customer base for the cash-and-carry business if Wal-Mart chooses to be more aggressive. However, that may not happen immediately. The business has been coasting for over a year without new openings that were already planned and significant personnel changes have happened from the seniormost levels down. Wal-Mart’s investigations of corruption allegations continue and before committing more resources it will definitely want to strengthen systems so as to not be in violation of Indian and US laws.

On the other hand, if it wishes to now enter the retail business, Wal-Mart would also have to look for a new Indian partner to set up new retail stores in a separate company. Retail is capital-hungry so Wal-Mart would need a cash-rich partner who can accept a junior position in the venture in which Wal-Mart would clearly be the driver financially, strategically and operationally.

At this time Wal-Mart seems to have decided to take a step back and evaluate what the Indian market means to it right now and in the future, what sort of investment – both in financial and management terms – it demands, and what returns the investment will bring. It remains to be seen whether it will choose to grow aggressively, coast up incrementally or, in fact, take the next exit out of the market as it has done in some other countries earlier.

And what of Bharti? Will it be able sustain the retail play without Wal-Mart’s close operational guidance and financial participation, or will it choose sell the Easyday operation to another domestic investor? On its part Bharti has stated an ongoing commitment to the business, and has also hired the former CEO of the joint venture, Raj Jain, as a Group Advisor. A 200-plus store chain is sizeable and credible in India’s fragmented food and grocery market, and is seen by the group as “a strong platform to significantly grow the business”.

However, Bharti’s core telecom business is also capital-intensive and highly competitive, and it will be difficult at this time to sustain high-paced growth in another cash-hungry, thin-margin business such as grocery retail. For now the Group’s best bet would possibly be to consolidate operations, unearth more margin opportunities and take a call at a more opportune time whether to further invest in growth or to treat retail as a non-core business and exit it.

Creating a substantial, profitable retail business is a long-term play in any part of the world. In India, as retailers are discovering, it takes just that extra dose of patience.

admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

Routes to Market – The Evolution

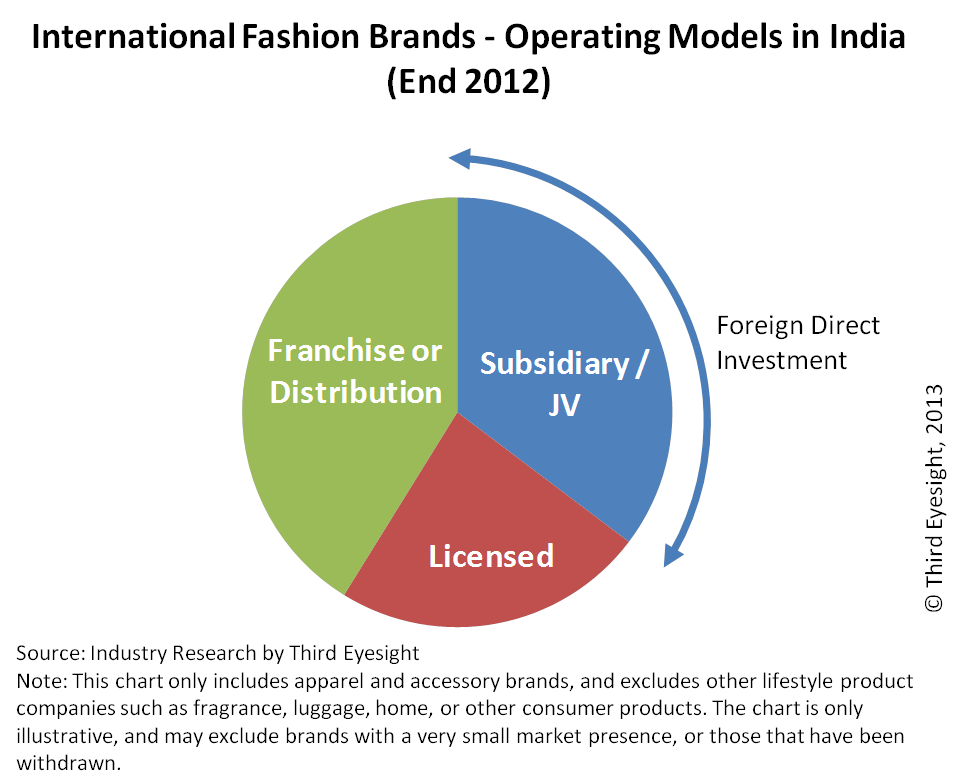

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.

Devangshu Dutta

March 13, 2012

Among consumer sectors, very few can match up to fashion in terms of its global nature. Despite food having led the way in global trade through spices, it is the fashion sector that led the global march of brands. As the economies in Europe and Asia recovered and grew, historical colonial linkages as well as modern culture-vehicles such as movies carried images of what was cool in the benchmark culture. Fashion brands were the most identifiable representation of cool.

India itself has known international fashion and luxury brands for several decades. From the mass footwear brand Bata to the top-notch luxury of LVMH, some of whose most important global customers included the rulers of Indian princely states, international fashion brands have an age-old connection with India.

In spite of these old links, the absolute base of consumers for fashion brands was small, and for them, prior to the 1980s , India was a relatively low potential market with low attractiveness and low probability of success.

A transition began in the 1980s, as India moved emphasis from central planning and a restrictive economy to a more liberal business regime, and brands and modern retailers started growing in presence gradually. During this transition period, other than the notable exception of Bata, it was mainly Indian brands that were at the forefront of modernisation of retail in India, with the first retail chains being set up for textiles, footwear and clothing. Though the seeds were laid earlier – Liberty is credited with the launch of the first ready-to-wear shirt brand in the 1950s, Raymond with the first ready-to-wear trouser brand in the 1960s – the growth started in real earnest only in the 1980s when apparel exporters such as Intercraft (with brands like “FU’s”), Gokaldas Exports (“Wearhouse”), and Gokaldas Images (“Weekender”) also tried their hand at modern retail, as did corporate groups (“Little Kingdom” for kids and “Ms” stores for womenswear).

Yet, even in the early to mid-1990s, when western companies looked at the Asian economies for international growth, West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow, steady process of increase.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun looking good. In a few years, from 2005 onwards, the number of international fashion brands entering the market has increased 4-fold.

Market Still Evolving, but Brands are Confident

The sheer number of brands that are now present in India and the new ones that are entering every year is a clear sign of strengthening confidence among international brands that India is now one of the most important markets that they cannot ignore for long.

There is a visible acceleration of growth in absolute revenues, too, being achieved by individual brands. Brands such as Levi Strauss, Reebok, Louis Philippe (a British brand formerly owned by Coats Viyella, now by Aditya Birla Group for India and other territories) and its sister brands took perhaps 12-15 years to break through the threshold of Rs. 500 crores (Rs. 5 billion) in sales turnover, but industry opinion is that the “0 to 500” trajectories today are faster and that younger brands are likely to take less time – under a decade – to cross the threshold. While modern apparel retail currently contributes less than 20 per cent of the total apparel market, with growing incomes and increased availability of modern retail environments, consumers are spending more on branded fashion than ever before. In the year closing March 2012, at least 2-3 additional brands (including Indian ones) are expected to cross the Rs. 500 crores threshold.

Clearly, there are few markets globally that can support potential growth from zero to US$100 million in a decade, with the potential to even reach a billion-dollar mark within the next couple of decades. However, some of these markets are already hugely competitive, and also going through painful economic churns. India, on the other hand, is a market that is at the earliest stages of consumer growth – it is, in the words of the managing director of a European brand, a market where “a brand can enter now and live out its whole lifecycle”.

In fact, it is tempting to compare the emerging golden bird of India to the golden dragon of China where western brands seem to have rapidly established as products of choice for the newly affluent Chinese consumer during the last 15 years or so.

In our work with brands and marketers from around the world, we have to constantly remind them that not all emerging markets are the same. The explosion of luxury and premium brands in China during the last decade or so has happened on the back of explosive economic growth that came after a long cultural and economic vacuum. When the new money wanted links with the old and when uniform grey-blue suits needed to give way to something more expressive, well-established western premium and luxury brands provided the most convenient bridge.

On the other hand, in India “discernment” may be a new experience to the newly-rich Indians for whom brands can be a valuable guide and “secure” purchase, but discernment and taste are not new to India as a whole. More importantly, differentiation and self-expression never disappeared even during India’s darkest years of “socialistic” economics. Therefore, the Indian market has a more “layered” approach to the premium fashion market and will continue to grow in a more fragmented, more organic manner than the Chinese market. There would be multiple tiers of growth available for international as well as Indian brands. For international brands customisation and Indianisation will be important. This is already visible in bespoke products by Louis Vuitton and Indian products by brands such as Canali (jackets) on the one hand, and significant re-thinking on product mix and pricing by brands such as Marks & Spencer. That brands are willing to rethink their position in the context of the Indian market demonstrates that they see India as a strategic market, worth investing in for the long term.

Another sign of the growing confidence amongst international brands in the Indian market is the number of companies that are looking at directly investing in joint ventures, or even going further to set up wholly-owned subsidiaries in the country.

It is worth keeping in mind that setting up a subsidiary is a decision that is not taken lightly, regardless of the size of the business and the amount of investment, since it involves a disproportionate amount of management time and effort from the headquarters during the launch and early growth phase where revenues are small and profits non-existent.

Among our clients, brands have taken the decision to step into an ownership structure in India when they feel that India is too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone may not be able to do justice to the brand in terms of management effort and financial capital.

In the last few years we have seen several brands take the plunge into investing in the Indian business, among them S. Oliver (Germany), Marks & Spencer (UK) and Mothercare (UK).

During 2011 specifically, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new JV in place, the venture is reported to be looking at opening 40 stores in the next five years.

Most recently, Canali was one of the brands that moved into a majority-owned joint-venture. The brand entered in India in 2004 through a distribution agreement with Genesis Luxury. This has recently given way to a joint venture between the two companies that is owned 51 per cent by Canali. The brand currently operates five exclusive stores in India has plans to accelerate the brands growth in India by opening 10-15 stores over the next three-four years.

The Impact of FDI Regulations

If a “theme of the year” has to be picked for the Indian retail sector in 2011, it must be ‘Foreign Direct Investment’. The debate during the year was hardly a clean and clear “pro vs. con” exchange of ideas. It was a motley mix of extreme lobbying for and against FDI, some balanced reasoning on why FDI should be allowed, and also moderate voices calling for governing the speed at which and the conditions under which foreign investment could be allowed. In many cases there seemed to be dissenting voices emerging from within the government. One possible impact of this uncertainty through the year was that several brands postponed their decisions regarding the potential entry and the strategy that they would follow in India with regard to partnership or investment.

In November 2011, the Indian government announced that 100 per cent foreign investment in single brand retail and 51 per cent foreign ownership of multi-brand retail operations, but was forced to back-track due to vociferous opposition from several quarters. At the very end of the year, the government finally reopened 100 per cent foreign ownership retail operations, albeit limiting it to single brand retail businesses. However, it allowed this under the condition that the Indian retail operation would source at least 30 per cent of its needs from Indian small and mid-sized suppliers.

The condition of 30 per cent domestic sourcing from SMEs is well-intentioned – aiming to provide a growth platform for India’s manufacturing enterprises – but unachievable for brands that do not currently source any serious volumes from India. In fact, for most international fashion brands India contributes less than 10 per cent of their total sourcing, in many cases well under 5 per cent.

Under these circumstances, we shouldn’t expect any dramatic changes, though we do expect the growth in joint-ventures and subsidiaries to continue in the coming months and years.

If an international brand perceives India to be at the right stage of development, and it wishes to exert significant or complete control over its Indian presence, then a majority or completely owned subsidiary seems the most logical step, and the brand will find a way to structure its involvement in India appropriately.

However, many brands that today have a 51 per cent ownership in India are stopping short of climbing to 100 per cent until they can sort out how to meet the SME sourcing conditions.

Getting Over the Sourcing Hurdle

The problem with the 30 per cent sourcing rider is simple. When a brand launches in India, it would like to present the consumer with the most complete product offering that showcases its capabilities and positioning as relevant to the target consumer in India. In most instances, the brand would not be sourcing the full range of its merchandise from India.

This is not a problem if the brand approaches the market through a wholesale or franchise structure, or even with a retail business that is not owned by it 100 per cent.

But for a retailer that wants to own the Indian business completely, complying with the 30 per cent domestic sourcing restriction means developing a new set of suppliers in India from scratch, pulling in the design and product development staff to work with them, and to develop ranges that suit not only the Indian market, but also other markets around the world. Simply putting together an India-specific sourcing team to replicate the entire range to buy small volumes for the Indian business is neither practical nor feasible for most of these brands. This means that the product development and sourcing team must be willing to see India as a strategic supply base for the future, just as their selling-side colleagues may be seeing it as a strategic market.

In this context it is worth repeating something that I have said before: retail managers are generally risk averse, and like to move in packs – where there are some brands, more come in and create a mutually reinforcing business environment. The presence of other international brands – especially from their own country – helps in creating a familiar context at first sight and encourages further exploration of the market. At least for the executives handling international retail expansion, India presents a more ‘familiar’ and ‘developed’ face today than ten years ago.

However, the explosive growth that we have witnessed in terms of the number of brands present in India is not mirrored by the growth of fashion sourcing out of India. In fact, even when compared to what has happened in the global textile, apparel and footwear sourcing environment since quotas were removed in 2005, the India’s export growth looks dispiritingly low, even stagnant. China still remains the largest source for fashion products, while countries such as Bangladesh, Indonesia and Viet Nam have grown their share aggressively. India’s share of clothing exports is a lowly one-tenth that of China.

In our work related to global sourcing strategies for western retailers, on an objective measurement matrix of sourcing competitiveness India rates highly. In several cases, sourcing from India as a hub (and, for European retailers, Turkey as a hub) has been seen as a logical counterweight to balance out the high concentration of current sourcing in China.

However, product development and sourcing is not entirely an objective process – in fact, sourcing habits are sometimes the hardest to change. The buyer’s subjective experiences – sometimes buried deeply in the past career – have a significant role to play. A conversation from 2001 with the sourcing head of a European brand sticks in my mind, when he said, “I don’t really want to buy anything from India – Indian suppliers can do a very limited product range, quality isn’t always good and the shipments are always late.” On probing further, I discovered that his last transaction was in 1992, after which he never set foot in India again. Much as we might present statistics and facts about the developments in the Indian textile and apparel industry, a personal injury early in his career has left a deep scar that obviously influenced this gentleman’s buying decisions worth over €300 million in global apparel sourcing, or about €700-800 million worth of sales.

There is clearly much to be done in terms of encouraging modernisation and better organisation amongst apparel suppliers, and making those changes visible to buyers. Even brands that are well-engaged with the Indian supply base have between 40-70% of their people here focussed on in-line and post-production quality issues. We are today at a stage where larger and better-equipped apparel exporters would be best placed to address the needs of international brands within India, but find the volumes too small to bother with setting up entirely different documentation and accounting processes.

Health & Safety and Labour compliances are also areas in which the brands will not forego their corporate standards. Can we imagine a brand saying that its European customers do not want their products made in sweatshops, but for the Indian consumers of the brand this is not (yet) an issue? While this may be a fact, would a high profile brand risk its global reputation to source competitively for its small Indian business?

So a government dictat to international brands’ fully-owned subsidiaries to ensure that they source 30 per cent of their needs is not enough. At best it will encourage some of the brands to start looking at India more seriously, but a more likely scenario for most brands is that they will carry on business as usual until the supply base in India pulls up its socks, or until the business in India becomes large enough to be interesting to their existing Indian suppliers who are currently focussed on exports.

Certainly the government itself needs to do much for more manufacturing-friendly policies, as well as focussed investment in infrastructure that can provide rapid, efficient and cost-effective transportation from the country and within the country.

It is time to bridge the gap between “textile exports” and “fashion retail” in the country. Remember, the explosive growth of brands in China followed the manufacturing explosion, not the other way round. Until the Indian apparel, textile and footwear manufacturing sector grows strongly, the actual volume growth of modern fashion retail will remain hobbled, regardless of the number of brands that enter the market.

To me this statement by a senior professional from one of Hong Kong’s largest apparel companies says it all: “The Indian industry looks like a formidable competitor, the day it decides to wake up.”

Drawing the Full Circle of Confidence

In closing I would like to mention the least acknowledged, but a very important part of the growth of international brands in India: the acquisition of brands overseas by Indian companies. The Aditya Birla group laid an early foundation when it bought out, for India and several other territories, the perpetual rights for Coats Viyella’s brands including Louis Philippe, Van Heusen and Allen Solly. Lerros was a slightly different example – being a brand that was set up by the House of Pearl in Germany – but that also circled back to India. More recently (2010) we have the example of the Swiss company Switcher Holdings, whose with brands including Switcher, Respect and Whale, was bought by PGC Industries.

In markets such as the EU, there are today brands that may be available because they are finding difficult to survive in harsh trading environments and that do not have the financial or management bandwidth to take on initiatives in growing markets like India. These offer a legitimate growth platform for Indian companies that are strong in manufacturing those product categories and want to move higher up the value chain from being a generic commodity “supplier”.

Although exporters may initially approach these brands for franchise or license relationships, to some it soon becomes clear that if they are in a position to make an incremental investment they could well own the perpetual rights and perhaps the whole business, rather than investing in building up someone else’s brand, especially in the business in India is likely to grow very rapidly. Obviously, this new-found confidence needs to be backed with solid management capability, but as other consumer goods companies such as Tata (beverages, automotive), Mahindra (automotive) and Dabur (personal care) have shown, it is entirely feasible to look at growth in India as well as internationally by using an existing international brand as a stepping stone.

It also presents a challenge of classifying such brands as international or Indian. Bata was founded in the Czech Republic and went global from there – however, today it is legitimate to treat it as a Canadian brand since its headquarters moved there in the 1960s. Among other products, Gloria Jean’s Coffee was founded in the USA, but is now completely Australian-owned. In that sense, today would that not make Louis Philippe, Allen Solly, Switcher Indian brands?

I think this puzzle is a challenge that many people in the industry in India would look forward to contributing to.

—–

Additional comment after reading the following blog post on Forbes on Single Brand Retailing (March 12, 2012):

Policies restricting foreign investment are not the biggest barrier to entering the Indian market. Brands and retailers that are clear that India is a strategic market with which they wish to engage will find a way. Even the largest global retailers have created structures that allow them a toehold in the market, awaiting a larger opening, despite the current ban on FDI in multi-brand retail.

The biggest barrier to entering India is actually the comfort zone within which the management team of an international retailer or brand may be operating. For some, the business environment of India needs at least a small step outside that comfort zone, for others it needs a big leap of faith.

There are encouraging signs of this happening already. Research carried out by Third Eyesight shows that the number of foreign brands operating in India in the fashion segment alone have quadrupled since 2005-2006, and a significant chunk of these are operating with direct investment in the Indian operations, whether as 100 per cent owned subsidiaries or as joint-ventures, indicating their growing comfort and confidence in the market.

One last word of advice: assess the opportunity pragmatically; don’t come looking for “a small percentage of the 1.3 billion population” in the short term – it takes time and patience to develop a meaningful share in the market.

Tarang Gautam Saxena

February 1, 2012

As the debate over FDI (even for single brand retail) continues, over 250 international brands in the food service and fashion and lifestyle sectors alone continue to service the Indian consumers. Interestingly more than half of them are present in the Indian market through the franchising route.

Franchising has been a preferred entry strategy especially in case of the food service sector. Many of the international food brands have opted to give the master franchise to an Indian partner who can use the international brand’s name but is responsible for sourcing the ingredients and maintaining the international quality standards for food and service. One such example is Dominos, which incidentally is also the country’s largest international food service brand. Of course, as FDI liberalisation seems nearer the finish line, brands such as Starbucks are choosing to join hands with an Indian partner while others such as Denny’s Corp are planning to tie up with regional licensees.

In case of the fashion sector, in the early years of liberalisation few international companies chose franchising. Instead some chose licensing to gain a quick access to the Indian market at a minimal investment. Others set up wholly owned subsidiaries or entered into majority-owned joint ventures to have a greater control over their Indian business operations, product sourcing and supply chain and brand marketing.

However, at the turn of the last decade, many international fashion brands chose franchising owing to favourable business environment. An environment conducive for growth of franchising was created by reduction in import duties under WTO agreements, the absence of a wide network of multi-brand retail platforms, the need for using exclusive branded outlets as a marketing tool to create a full brand experience and the simultaneous growth of real estate investors who were potential master franchises ready to invest capital and real estate.

The question is how the liberalisation of FDI norms will impact the choice of market entry strategy for the international brands. Would franchising continue to remain the preferred entry mode as we set into the liberalised FDI regime? The change in foreign investment norms has already led to some brands (in particular those in the fashion and lifestyle sector) transitioning their existing licensing or franchise partnership into a joint venture or wholly owned subsidiary while the new entrants are actively considering ownership routes rather than franchising.

Certainly, the ideal scenario for an international brand would be to have complete ownership and control over the operations in a strategic market like India, but direct investment does also increase their risk and the investment is not financial alone. Amongst other choices licensing offers the least control, and while joint venture may be preferable for some brands, for many franchising still proves to be the practical choice for some time to come.

Franchising may potentially be quicker way to launch with higher chances of the retail business being successful. As it is an “entrepreneurship” model of business, the franchisee’s motivation to make the venture a success is high. The international brand has an assured income by way of royalty on the license agreement and could expand more rapidly in the market. Having a local partner with a closer understanding of the market and the ability to adapt to the changing needs of the consumers also helps to ensure that the international brand’s offering is tuned in to consumers’ demand.

Further, unlike more developed markets where brands have sizable networks of large-format store as a launch and growth platform, in India there are still limited choices to simply “plug-and-play” using department stores or any other large-format retail network. Partnering with a franchisee who has access to retail real estate can be a quick way to reach the target consumers. On his part the franchisor needs to ensure that the business model is well thought through in terms of the team and infrastructure required and is scalable.

For a successful relationship it is vital that the franchisee has an entrepreneurial mind-set. The essence of the brand needs be well understood, and the franchisee must have operational involvement rather than a “passive investment” approach.

If both partners understand their respective responsibilities, franchising can truly be a win-win business model.