admin

January 7, 2010

By Tarang Gautam Saxena, Chandni Jain and Neha Singhal

In Retrospect

While India was a promising market to many international brands, it was not completely immune from the global economic flu. More than its primary impact on the economy, the global downturn sobered the mood in the consumer market. Even the core target group for international brands, that had just begun to splurge apparently without guilt, tightened their purse strings and either down-traded or postponed their purchases.

In 2008 in the midst of economic downturn, skepticism and uncertainty, the international fashion brands had continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008 targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many players ended up discounting the goods heavily to promote sales while a few also gave up and closed shop.

As the Third Eyesight team had foreseen last year, 2009 saw a further slowdown and fewer international brands being launched during the year. The brands that were launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack and Timberland. Some of these had already been in the pipeline for quite some time and invested a considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

International Fashion Brands in India

After many deliberations, the well-known global brand Donna Karan New York set foot in the Indian market in 2009 through an agreement with DLF Brands to set up exclusive DKNY and DKNY Jeans stores India. The brand is also reported to have signed a worldwide licensing agreement with S Kumars Nationwide Ltd to design, manufacture and retail DKNY menswear in certain specific countries.

Second Chances

Amongst the international brands that have recently entered the Indian market, a few are on their second or even third attempt at the market.

For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills, and the partnership intended opening 15 stores by 2010. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis on retailing international brands within the country. Within a few months of the ending of this relationship, Diesel signed a joint venture with Reliance Brands for a launch scheduled for 2010. Both partners seem to be strategically aligned with a common goal as the international iconic denim brand wants to take on the Indian market full throttle and the Indian counterpart has indicated that it wants to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008, despite plans to open more than 50 stores in the first three years of operations. Miss Sixty has finally entered India through a franchise agreement with a manufacturer of women’s footwear and accessories. The company has currently introduced only shoes and accessories category and is looking at potential partners for its label Energie and girls’ range Killah.

Other brands that have re-entered the Indian market include Germany-based Lerros whose first presence in India was back in mid-1990s. The brand re-entered the market in 2008 through own brand stores and is growing its presence through this route as well as through multi-brand stores.

Oshkosh B’gosh is another brand that had entered India in mid 1990s, through a licensing agreement with Delhi based buying house, Elanco. The licensee found the childrenswear market hard to crack, and closed down. In 2008, Oshkosh re-entered the Indian market through a licensing partnership with Planet Retail and is now available through shop-in-shop counters at Debenhams stores. Reports suggest that it may consider setting up exclusive brand outlets.

During the turbulence of 2008 and 2009, a few brands also exited the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both) to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations and for the amount of effort and money being invested, and that it was better to pull the plug.

Some brands that have been pulled out of the Indian market during 2008 and 2009 include Dockers, Gas, Springfield and VNC (Vincci). Gas (Grotto SpA) is reported to remain interested in the market but has not found another partner after its deal with Raymond fell through in 2007 and all dozen of its standalone stores were shut down.

The Scottish brand Pringle and its Indian licensee did not renew their agreement upon its expiry. The Indian partner has reportedly signed an agreement to launch another international brand in India, while Pringle is said to be looking for new licensee.

The good news is that successful relationships outnumber every exit or break in relationship possibly by a factor of ten. Some of the brands that have sustained are among the early entrants having a presence in India since the late-1980s and 1990s or even earlier. These include Bata, Benetton, adidas, Reebok (now also owned by adidas), Levi Strauss and Pepe. Having grown very aggressively during 2006 and 2007 Reebok quickly became the largest apparel and footwear brand in India, while Benetton and Levi’s are expected to cross the $100-million mark for sales this year.

Entry Strategy & Recent Shifts

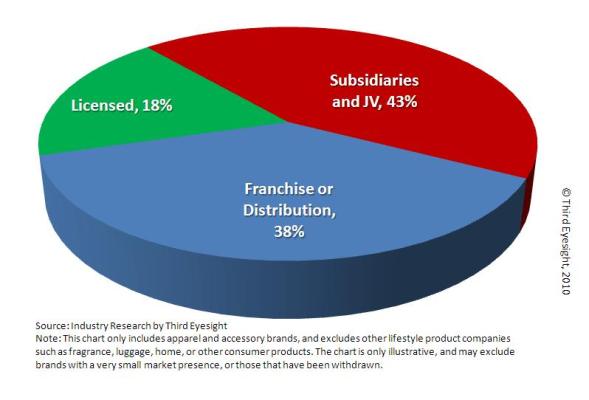

As envisaged in Third Eyesight’s report from a year ago, with changing market conditions and a growing confidence in the Indian market, there has been a shift among international brands in the choice of the launch vehicle. While franchising has been the preferred mode of market entry in the recent past for risk-averse brands, more brands today demonstrate a long-term commitment to the Indian market, and are choosing to exercise ownership through wholly or partially owned subsidiaries and through joint ventures.

In 2009, we have seen a noticeable shift in favour of joint-ventures as the choice for entry into the market. Even the brands already present are looking to modify the nature of their existing presence in India in order to exert more control over the retail operations, products, supply chain and marketing.

Current Operating Structure

(End 2009)

Brands that changed their operating structures and, in some cases partners, in recent years include VF (Wrangler, Lee etc.), Lee Cooper, Lee, and Louis Vuitton amongst others.

Mothercare, the baby product retailer, which is present through a franchise agreement with Shopper’s Stop has, in addition, recently formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores. Gucci, which had initially entered in 2006 with the Murjani Group as a franchisee, has recently changed over to Luxury Goods Retail, and is now in the process of restructuring the relationship into a joint venture.

VF has also been reported to be looking to license Nautica, Jansport and Kipling to a new partner. Until now, these brands were handled through the joint venture with Arvind Brands. Arvind has increasingly focused on its core business, closed stores and scaled down expansion plans for the international brands.

Burberry that had entered India in 2006 through a franchisee arrangement with Media Star opened two stores under this arrangement. It has now set up a new joint venture with Genesis Colors and plans to open 20 stores across the country.

More recently Esprit has also been reported to have approached Aditya Birla Nuvo to deepen its engagement by moving from its distribution arrangement into joint venture as the international brand sees excellent potential in the Indian market.

Buckling up for 2010

Throughout 2009, the one fact that became clear was that the Indian market was resilient. Now, as the global economic condition stabilizes, confidence levels of brands and retailers in India have also improved.

Several launches are already expected in 2010, and possibly many more are being worked upon. In the following 12 months, consumers can expect to find within India acclaimed brands such as Diesel, Topman, Topshop and the much-anticipated Zara. Many more Italian, British and French brands are examining the market.

Most of the international fashion brands already present in the market are also projecting a cautiously upbeat outlook in their plans, while a few are looking positively bullish.

For example, Pepe, an old player in premium and casual wear segment, has reported plans to grow its retail network further and open 50 more franchise stores by September 2010. Similarly the German fashion brand S. Oliver that entered the Indian market in 2007 is looking to grow significantly. It has already moved from a franchise arrangement with Orientcraft to a joint-venture with the same partner, and has stepped up its above-the-line marketing presence. The brand has recently reported its plans to scale up its retail presence to 77 stores by the end of 2012 while also strengthening its presence through shop-in-shop in multi-branded outlets in high potential markets.

Those international brands that have tasted success have not achieved it by blindly importing business models and formulas from other markets. Most have had to devise a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched. These include The Body Shop which decreased its prices by up to 30% this year, and Marks & Spencer which reduced prices by 20-40%. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

On the operational side, the good news for retailers and brands is that the average real estate costs have reduced significantly, although marquee locations remain high. In several locations lease models have also moved from only fixed rent to some form of revenue sharing arrangement with the landlord. And, while the sector has seen some employee turmoil as many non-retail executives who came into the business in the last 5-7 years have returned to other sectors, employee salary expectations are also more realistic.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s recent work with international brands’ business units in India highlights the international players’ concern with ensuring a consistent brand message, improved organizational capabilities right down to front-line staff, and focus on unit productivity (per store and per employee).

We may yet see a few more exits, and possibly some more relationships being reshuffled and partners being changed. However, all things considered, we can look forward to a net increase in the number of international brands in the country.

The Indian consumer is certainly demonstrating more optimism and as far as there are no major unforeseen global or domestic shocks, this optimism should translate into a healthier business outlook for international brands as well. According to early signs, 2010 could be an excellent curtain-raiser for a new decade of growth for international fashion brands in India.

[The 2009 report is available here: “International Fashion Brands – India Entry Strategies”]

(c) 2010, Third Eyesight

[Note: This report is based on information collected from a combination of public as well as proprietary sources, and in some cases may differ from press reports. However, no confidential information has been shared in this report.]

Devangshu Dutta

June 2, 2008

When we began studying the basic fundamentals of marketing, our professor introduced us to the 4-P framework covering Product, Price, Place and Promotion created by “the Great P” of Marketing, Philip Kotler, whose textbooks are classics among marketing management studies.

In time, others modified it to 5-P, 6-P and 7-P, but the basic framework stands best on the original four legs defined by Kotler.

The principle is that to design an effective marketing strategy you need to:

If you are truly disciplined, you may then extend any of these into spider-webs of clearer attribute definition. For instance, when you get involved with defining the product it can start from “breakfast” and then be further defined by attributes such as taste (e.g. sweetened or unsweetened), texture (e.g. crunchy or wet), fullness (e.g. light or filling), and go further into the benefits (e.g. helpful in losing weight, or in gaining body mass) etc.

Given that the basic framework is straight-forward and simple to apply, when we ask the question “what is your marketing strategy”, it is surprising to get the answer: “advertising”. It gets somewhat more distressing when we interrogate further, when we examine what the advertising is focussed on: “cheaper prices than competition”.

Okay, let’s grant a couple of reality checks here. One is that most retailers and consumer goods companies in the current stage of the market’s growth want to grab the maximum possible market share in the minimum possible time. Two, if you want to get the attention of a lot of customers very quickly, shouting out a great price offer is one of the easiest ways to do it.

Which brings us to the basic issue: in the current market scenario, if you are a retailer or if you have a brand that you want to scale up fast, advertising extensively about the “great value” is highly likely to quickly give you the footfall and conversions you need.

But the question is, when does it stop being a good tactic and just becomes lazy marketing? And once it’s in that territory, when does it become dangerously weak even as a sustained tactic?

Imagine a scenario with me: the CEO strides into a marketing strategy meeting and says, “I want you to stop advertising the way you do. In fact, I want you to stop advertising, period. But I don’t want sales to drop and I don’t want our brand image to suffer.”

Shock, horror, dismay at the thought of “where is this company going”? Resignations, even, on the CEO’s table?

But just stay with that thought for a minute, and then look at Kotler’s framework again.

Let’s look at “product” holistically because, in the noise of high-decibel advertising about low prices, typically the definition of the “product” is the first to slip from attention. How the customer relates to the store, what her experience is as she walks through from the entrance to the check-out and beyond is part and parcel of the “product”. What does she think the store is about? Does her perception of the store’s “product” (the entire experience of shopping) match with the retailer’s own perception? Does the retailer even have a clear perception of his product?

Secondly, “place”. Sure, in-store product placement is frequently governed by the marketing function. But how many retailers have marketing involved in selecting the store location? A great store location is the best live, “walk-in advertisement” that a retailer can have. If a fashion brand like Zara can eschew advertising (founder Amancio Ortega has been quoted as saying that “advertising” is a distraction), and instead focus on its stores to create the traffic and the awareness about the brands, surely the store location should receive some attention from the marketing heads of food and grocery companies.

Let’s also reconsider how much connection there is between the marketing strategy and the store layout itself (in many cases it is not enough). Whether the customer likes wide aisles and a “clean” experience or prefers a chaotic environment, the store must make a statement that is in sync with the overall business strategy and the target customer. Good retailers understand this intuitively, but it is important also to express it overtly within the organisation and get the marketing team involved in the planning and execution. Further, once the customer is actually in the store, clear price ticketing, intuitive adjacencies and clean signage can make a tremendous difference in converting walk-ins to purchases.

Let’s leave price alone for this inquiry because, whether high or low, it gets a lot of attention anyway, and let’s move to promotion.

If we define marketing’s role as getting customers into the store and getting them to buy, then the surely promotion is the driver of the marketing engine. But does promotion necessarily have to mean advertising?

We’ve discussed Zara’s example of using the stores as the medium of promotion. Another thing that works for Zara is word of mouth publicity, as well as the humongous amount of publicity the company gets due to its business model. (Other interesting companies, such as Pantaloon, Reliance, Wal-Mart, The Body Shop etc. also enjoy promotion through publicity.)

Pizza companies use cost-effective menu flyers dropped at the customer’s door and “box toppers” to drive the next purchase (yes, of course, they also advertise hugely, but during their lean years when they have had to reduce advertising, it is the flyers and box-toppers that have kept them going.) Direct selling companies can also offer some learnings about creating and sustaining interest, as do entrepreneurial start-ups. As a matter of fact, think of the last time you saw an advertisement of the most popular “unbranded” take-away in your area. Ever?

It may be time for us to dust off the notes from the Marketing 101 class, and re-examine what we do.

admin

April 6, 2008

In the business of fashion, time has always been important. However, speed and efficiency are now both a strategic imperative and a tactical necessity. With greater unpredictability in the market, it is critical to have the correct product at the correct time in the right quantity. Fast fashion requires completely different thinking in the way product is developed, how pre-production processes are undertaken and how production is organised. The Fast Fashion Seminar will draw upon the live experiences of leading practitioners from the area of product development and supply chain. It will be structured as an interactive session. This Third Eyesight Fast Fashion Seminar will provide you with a valuable insight into how to effect rapid changes in the market to your benefit.

Among other aspects, it will:

Describe in detail the concept of fast fashion

Identify key strategic actions to meet fashion consumer demand

Detail how leading brands such as Zara operationalise the concept

Discuss how to achieve less than 1% inefficiencies in their processes from design to delivery, including inventories and markdowns substantially below the industry average.

Understand the underlying principles of the fast fashion model and how these might be applied to retail and fashion business models in India

Attendance is strictly by pre-registration. Registration information is also available over phone (please contact on phone +91-124-4293478 or +91-124-4030162).

Devangshu Dutta

January 19, 2008

Even in these enlightened marketing times, many people believe that the brand is the name. They believe that once you advertise a name widely and loudly enough, a brand can be created. Nothing could be further from the truth.

High-decibel advertising only informs customers of the name, it cannot create a brand.

If we put ourselves in the customer’s shoes, a brand is an image, comprising of a bundle of promises on the company’s part and expectations on the customer’s part, which have been met. When promises are delivered, when expectations are met, the brand develops an attribute that it is defined by.

The promise may be of edgy design (think Apple), and the customer expects that – when the brand delivers on the promise and meets the expectation the brand image gets re-affirmed and strengthened.

However, these attributes are not always necessarily all “positive” in the traditional sense. For instance, a company’s promise may be to be low-cost and low-service (think Ikea, or “low-cost airlines”), and the customer may expect that and be happy with that when the company delivers on that promise.

The promise may be products with a conscience (think The Body Shop), which may strike a chord with the consumer.What that brand actually stands for can only be created experientially.

Creating this image, creation of the brand, is a complex and step-by-step process that takes place over time and over many transactions. Repetition of the same kind of experience strengthens the brand.

The brand touches everything that defines the customer’s experience – the product design and packaging, the retail store it is sold in, the service it is sold with, the after-sales interaction – all have a role to play in the creation of the brand.

For instance, to some it may sound silly that market research or how supply chain practices can help define a brand, but that is exactly how the state of affairs is for Zara. Changeovers and new fashions being quickly available are what that brand is about, and it would be impossible for Zara to deliver on that promise without leading edge supply chains, or a wide variety of trend research.

Similarly, it may sound clichéd that your salesperson defines the brand to the consumer, but even with the best products, extensive advertising, and swanky stores, for service-oriented retailers everything would fall apart if the salesperson is not up to the mark. This is indeed a sad reality faced by so many of the so-called premium and luxury brands.

Of course, brand images can be changed or updated, but the new image also needs to be reinforced through repeated action, a process just like the first time the brand was created.

(Extracted from the article “Brand Immortality and Reincarnation“)

Devangshu Dutta

April 5, 2006

Fashion is, by definition, perishable. Like, bread, eggs and milk. Or is it?

When bread turns stale, eggs turn rotten or milk turns rancid, you do have to throw it away. Fashion is different, because its perishability is artificial, driven by popular perception that something is “out-of-date” or that something else is “the look of the day”. You don’t really have to throw that blue peasant skirt out in the garbage or in the Salvation Army bin…but you do anyway, because it is so yesterday…or that’s what everyone else is saying.

Earlier, perceptions took time to spread, today they can be spread instantaneously through the web, TV and cell phones, and pretty quickly, even through slow media like print magazines.

So ‘Fast Fashion’ is really a product of fast media and communications technologies.

Having said that, it is here to stay, and regular (mainstream) slow-coaches do need to be worried about customers being seduced away by the ever-fresh look of a Chico’s or a Zara.

I can’t even begin to estimate the millions of dollars that must have been spent on “studying the Zara model”. However, while Zara’s model seems to scream “best practice” and everyone wants to emulate it – is it really for everyone?

Inditex (Zara’s parent company) has grown over 40+ years of evolution, in a specific market and business context. It may have “exploded” on the global scene when it floated its IPO in 2001, but the business model has been brewing a long time.

It has such significant investments in production that Inditex is as much a manufacturer as a retailer. Its people and process model almost diametrically opposite the command and control, “buying director – driven” model of other retailers. Its technology investments are focused better than most of its peers. (See case study and presentation)

Would your company’s DNA allow you to invest in and manage fabric and apparel manufacturing? Would it allow young people to be sent out to take bigger-ticket purchase decisions with fewer approvals than they do now? Would your design team really trust your frontline store staff with feeding them relevant trend information every day?

And yet, and yet…As labour costs rise in Europe, Zara is also being forced to rethink its model of local or regional production. As it does move more production to places like India and China, the big question is whether it can maintain the sanctity of its business model.

I won’t advise other retailers to breathe easy, but they don’t need to roll over and die just yet.