Devangshu Dutta

January 10, 2017

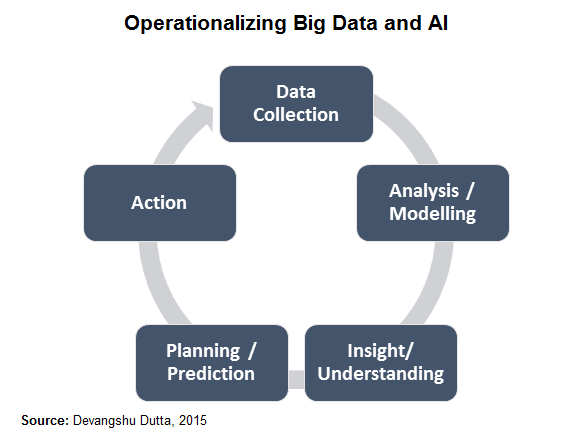

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

December 29, 2016

In 2016, brick-and-mortar modern retailers seemed to have begun recovering their confidence, and cautiously investing in expansion. However, currency shortage has significantly dampened demand at the end of the year. The hangover would continue into the first half of 2017, and consumers could be muted overall on discretionary purchases, including fashion, mobile upgrades and out-of-home dining.

On the other hand, while digital transactions introduce a note of caution (friction) in the consumer’s purchase decision, for e-tailers they do reduce complexity, cash-handling costs and potential returns which could provide significant unexpected wins.

I’ve written about this for years, and don’t tire of reiterating: the retail sector must recognise that shopping is a unified activity for the consumer; physical stores and non-store environments are alternative but complementary channels. Brands can and must use whatever channel mix works for them, and brick-and-mortar retailers need to invest in creating an integrated growth blueprint towards “unified commerce”.

On their part, while e-commerce companies are constrained by FDI policy, they will need to invest more in developing “old economy” strengths – strong product differentiation and distinguishable brands. Fashion, accessories, home decor and other lifestyle products are strong drivers of gross margin for all multi-product retailers, and e-commerce players struggling on the path to profit would focus on these even more, as well as on private labels. They also need to have management teams that are able to cast their minds 3-5 years into the future, while keeping close watch on immediate cash flows. Capital is available, but turning risk-averse. All businesses need to focus on up-skilling their teams, retaining good people, improving processes and adopting technology. In recent years, growth in the retail sector seems to have been driven by a “spray-and-pray” approach, not necessarily management sophistication. Spending like there’s no tomorrow is a sure way to no tomorrow.

In short, 2017 could be the year where the entire retail sector grows up – a lot. We hope.

(This piece was published in The Hindu – Businessline on 29 December 2016).

admin

August 1, 2016

The cold chain sector is expanding quickly due to increased investments from Indian and international organisations going towards both modernisation of the existing facilities and establishment of new ventures. Over the last few years cold-chain has gained a buzz, finding its way not only into industry presentations but also into budget speeches in Parliament. It is widely reported that India needs to build more cold chain capacity, especially to reduce the enormous amount of waste of food products in the chain from farm to consumer.

India is one of the largest producers of agro-products i.e. fresh fruits and vegetables, milk and related products, fishery products and meat. However, due to lack of the required facilities, spoilage of products is comparatively high.

In recent years, significantly incentivised both by business logic and by tax breaks, there has been a fair amount on investment in cold storages. However, the sector is still highly fragmented; there is inequitable distribution of cold storages, interlinkages between storages is also very poor and many facilities are also operating below capacity.

The National Centre for Cold Chain Development (NCCD) reported that as of December 2014, 70% capacity was utilised, where the total number of cold storages available in India was around 5300 and approximately 6000+ vehicles, providing about 30 Million Metric Tonnes capacity of storage. Most of these facilities are located in the states of Uttar Pradesh, Uttaranchal, Punjab, Maharashtra and West Bengal.

Storage and transportation capacity is only the very first step in strengthening cold chain capabilities but, unfortunately, that is where many entrepreneurs and investors in cold-chain are stopping their thought process. Many players in the industry have been using obsolete machinery, and storages are majorly for a single commodity. The result, predictably, is underutilisation of capacity or mishandling of food products leading to operational problems, cost escalations, spoilage and other losses. Just to mention a simple example that many seem to forget: even domestic refrigerators have at least 3-4 temperature-humidity zones: the freezer, the chill tray, the large cool area, and a vegetable tray. In comparison, many cold stores are built without adequate thought to the various influencing factors. It’s important to recognise that in developing a cold chain capability, the products to be handled, the environment in which the cold chain will operate, not only storage but intake, handling and transportation, all have a role to play.

With a fragmented operating environment, both in terms of production as well as distribution, often a single investor or company may not be able to create the business logic to set up a cold chain facility. Collaboration between multiple individuals and agencies may be a way out.

An example of successful use of integrated cold chain is the Tamil Nadu Bananas Growers Federation. Banana growers in the Tamil Nadu belt were diminishing due to lack of appropriate storage facilities, and farmers were forced to sell produce at throw away prices. With introduction of integrated cold chain solutions, the federation of farmers from Tamil Nadu has now managed to gain a hold of the banana market again. They have managed to increase their income manifold by growing better qualities and storing bananas for longer period of time in the integrated cold chains.

Cold chain logistics in the true sense begin with harvesting and post-harvest handling, going on to controlled atmosphere vehicles, cold storages, sorting and grading facilities, modern pack houses and controlled atmosphere retail stores. Most importantly, even operational know-how is something that is not made part of the investment plan, leading to unviable, unprofitable cold chain facilities.

The focus should be to integrate the cold chain, and also build capacities in all areas. As per NCCD (December 2014), India has approximately 6,000 reefer vehicles against a requirement of 60,000. Similarly the number of pack houses available is 250 and the projected requirement is for 70,000. Hence, the need for a more balanced investment in terms of modern pack-houses, refrigerated transport units and ripening chambers is evident and will bring far better results, both operationally and financially.

In addition, there has to be a significant improvement in developing the know-how and skills sets available to the sector. While the country is faced with large-scale unemployment annually, a well-thought out development of the cold chain sector including due investment in knowledge-based initiatives can create significant numbers of better paying jobs around the country, especially in rural areas from where the produce is sourced.

With development of the consumer and retail sector supporting its growth, integrated cold chain development should be at the top of the agenda for government as well as for private business.

admin

February 21, 2016

![]() Shinmin

Bali, Financial Express

Shinmin

Bali, Financial Express

![]() Mumbai,

21 February 2016

Mumbai,

21 February 2016

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

TinyOwl last year was in the news for a poorly-handled downsizing

operation in Pune, with a dramatic hostage situation involving

its co-founder Gaurav Choudhary. PepperTap also recently shut

down operations in six cities.

Ironically, giants like Amazon have not only aggressively entered

the hyperlocal space, they are building on it. Amazon is currently

offering the service in Bengaluru, Amazon Now, after running a

pilot project, Kirana Now, in 2015.

The investor sentiment in India is also on a decline, as was

reported earlier this year. Investments by venture capitalists

have dropped from $2.12 billion (October-December 2014) to $1.15

billion (October-December 2015), according to a report by CB Insights

and KPMG International. This leaves an even shorter window of

opportunity for players to retain investor interest.

Albinder Dhindsa, co-founder, Grofers, states that differing

levels of technology literacy among the majority of merchants

and consumer adaptation to the online platform are concern areas

for the company. In 2016, the company is looking to bring over

one lakh merchants aboard and ensure that turnaround time stays

under an hour. Grofers delivers more than 35,000 orders per day

on average. In Q4 2015, the firm acquired teams of SpoonJoy and

Townrush to bring dynamic learning to the table.

For Swiggy’s co-founder Nandan Reddy, the focus is currently

to grow the market, while catering to a wide demographic of consumers.

He admits that in the early stages, the brand had trouble educating

even its partners. Furthermore, operating a delivery fleet in

an on-demand service offering sub-40 minute deliveries is a challenging

task, given that there are at least 15 points of failure in an

average order. Swiggy currently owns a delivery fleet of 3,800

delivery executives. The brand’s repeat consumers contribute

to over 80% of orders.

Debadutta Upadhyaya, co-founder, Timesaverz, says some of the

major challenges in a hyperlocal market are optimum resource utilisation

and matching locations, price points, and other specific requirements

to customer needs. Timesaverz currently has a service range spread

across 40 categories, aided by a network of over 2,500 service

partners across five metros. Its revenue model is commission based,

where 80% of earnings from consumers are shared with service partners.

Vinod Murali, MD, Innoven Capital, points out that as the hyperlocal

industry is in its nascent stages, it needs a fair amount of time

to grow. “One aspect to keep in mind is that a large sized

equity cheque does not imply that a company has achieved operational

maturity or robust business metrics, especially in this segment,”

he notes.

Given the recent consolidation in this category, the survivors

have the opportunity and time to focus on improving unit economics

and demonstrate that their businesses are viable and valuable.

Devangshu Dutta, CEO, Third Eyesight, is of the opinion that

hyperlocals make the mistake of borrowing business models and

terminologies from Silicon Valley, without adequately understanding

the real context of the Indian market. “Is there an existing

or even potential demand for the service claimed to be provided?

Or are you just going to introduce an intermediary and an additional

link in the chain, with additional costs and unnecessary administration

involved?” he asks.

(Published in Financial Express)

admin

September 8, 2015

![]() Devina

Joshi, Financial Express

Devina

Joshi, Financial Express

![]() Mumbai,

8 September 2015

Mumbai,

8 September 2015

Recently,

there was news of restaurant reservation site EazyDiner expanding

operations to Mumbai from the National Capital Region, having

secured Series A funding worth $3 million led by existing investor

DSG Consumer Partners, and Saamna Capital.

Recently,

there was news of restaurant reservation site EazyDiner expanding

operations to Mumbai from the National Capital Region, having

secured Series A funding worth $3 million led by existing investor

DSG Consumer Partners, and Saamna Capital.

As per a PwC analyst, investors have pumped more than $150 million

into companies like Grofers, TinyOwl, Swiggy, LocalOye, Spoonjoy,

Zimmber and HolaChef, among others. Judging by the patronage showered

upon them by customers and investors alike, it would appear that

hyperlocal start-ups are all set to create the next big boom in

the Indian retail sector. But is it really all that rosy? Probably

not, as can be amply witnessed by acquisitions taking place in

the nascent yet already overcrowded market.

Between November 2014 and February 2015, the Rocket Internet-backed

Foodpanda acquired rivals TastyKhana and JustEat.in, and is rumoured

to be in acquisition mode with TinyOwl. Restaurant search app

Zomato, which recently got into the food ordering space, is also

reportedly looking to acquire minority stakes in food-ordering

firms.

While investors are attracted to hyperlocal start-ups, controlling

logistics well is key to sustained growth for these businesses

— all of these will definitely go through a constraint in

the supply of delivery boys, for example. In India, organising

fragmented labour is a challenge and, hence, a services-based

hyperlocal needs to figure out the mechanics of human capital

even more than a traditional, product-based e-commerce firm.

For services, another challenge is customer stickiness. If a

user uses an app to obtain the services of a plumber, for example,

he may not go through the app to contact the plumber next time

if his services are found satisfactory. Discounting can induce

trials, but just like in any other business, prove fatal in the

long run. Like what led to the end of HomeJoy in the US —

excessive discounts to dissuade direct contact between servicemen

and customers.

Even for product-based start-ups, maintaining data quality is

a big hurdle as stock and prices may not be updated by retailers

in real time, making it difficult to track offline sales.

Since the game is hyperlocal, you need to be physically present

in the city to bring retailers aboard. For that, you need a city

team. Other challenges include retailer verification and assessment,

given that hyperlocals deal with small city retailers.

Stickiness is needed on both sides, and each locality will certainly evolve into having a market leader and a follower, with other players falling far behind. “So the critical success factor for a hyperlocal is being able to rapidly create a viable model in each location it targets, and then—to build overall scale and continued attractiveness for investors—quickly move on to replicate the model in another location, and then another,” says retail consultant Devangshu Dutta of Third Eyesight. As they do that, they will become potential acquisition targets for larger ecommerce companies, which could use acquisition to not only take out potential competition but also to imbibe the learning and capabilities needed to deal with microcosms of consumer demand.

(Published in Financial Express.)