Devangshu Dutta

May 16, 2009

The world’s largest retailer earned bouquets as well as a few brickbats when it recently opened a Hispanic version of its large store format, named Supermercado de Walmart. The signs around the store are in Spanish as well as English, selling traditional Mexican national brands as well as traditional Hispanic food like tacos, tortas, aguas frescas, sopes, carnitas and barbacoa at the chain’s customary low prices.

The surprise, if any, was that this store was not in a city in Mexico but in Houston, Texas, USA.

Wal-Mart’s logic behind the format is that it would be more relevant to the heavily-Hispanic population in the catchment of the store in Houston, and that it was a natural evolution to what they had been doing for years.

However, some customers and observers do not agree. Quite a number of people are up in arms against this “pandering to immigrants”, which they see as a threat to the unity, homogeneity and identity of the United States of America. One internet commentator condemned this segregation with a rather unique view, saying that segregating customers like this was actually “racist” and belittled the Hispanic customers who live in that area.

We should probably wait for the dust to settle on this debate. Spanish-speaking customers may actually respond positively – or not – to this new format. Yes, some defensive or aggravated English-speaking customers may also boycott Wal-Mart over this move.

As for me, I believe that it is a good move for Wal-Mart to test how far customization can help their business and how finely they can tune their response to customer demands, because they will need all the learnings they can get to effectively tackle markets that are even more different around the world.

Of course, many retailers and marketers in a market such as India would be puzzled by all this fuss. After all, if a Chennai-based company opened stores in Maharashtra, it wouldn’t put up signs in Tamil, neither would a Punjab-based retailer expect its customers in Imphal to understand promotions in Punjabi. Fragmentation and customization is a fact of life to the Indian retailer.

Or is it really that clear?

In fact, India has its share of marketers who seem to think and plan mainly in upper income metropolitan-English, and this bias creeps in not only in the content and structure of promotions but also, unfortunately, influences the merchandise mix. Even while PowerPoint presentations are made about how diverse the country is, and how it is possibly more like many countries rolled into one, we often make use of cookie-cutters for designing our product plan, our marketing strategy and everything else that defines the retail store and the customer experience.

Now, before I am labelled unfair for making sweeping generalizations, let me also say that other than any such urban English bias, there are also another couple of reasons why a retailer may take a template-based or cookie-cutter approach to the market.

Firstly, if you’re launching a new retail chain, there is a need to derive efficiency by driving scale as quickly as possible. Repeating the product formula across locations allows a retailer to increase the impact of merchandising efforts in terms of additional margins due to volume margin terms and better negotiating power with the supplier. Also, the management effort is used in a much more focussed manner, lowering effective management costs.

Secondly, there is the need to demonstrate a consistent image across the entire footprint of the chain, and to appear to be a chain. Repeating the product and presentation formula reinforces the common image and branding.

However, the pertinent question is whether there is any point in following a consistent identity if it appears alien and irrelevant to most of your target customers? In a category such as grocery, where the customer don’t really shop across multiple stores in a chain, is it better to be locally relevant rather than consistent across the country or even a region? Clearly, if you have a national or international template that is locally irrelevant, you don’t have any chance of succeeding with the consumer.

On the other hand, is it really organisationally possible for a chain-store to be local, and if so how can it best strike the balance between chain-wide consistency and tweaking the offer to provide local focus?

To my mind the starting point is the definition of an identity based on a clear value proposition and operating principles. This includes a range of factors from the visual elements of branding to how the staff stack shelves or interact with the customer.

The next step is to make the merchandise locally relevant, because that is what creates the transaction. The answer to “how much local” would also provide the answer to “how the locally-relevant merchandise should be managed”. Organisational models could range from entirely centrally-managed local merchandise and data-driven decisions, to central management of range architecture and purchases but local pull-based replenishment, to outright purchase from local vendors by the specific store’s management to create a truly local store.

Of course, devolving range and purchase decisions to local management raises issues about maintaining control as well. To a certain extent processes and system can help to mitigate the risk of fragmentation of the identity or potential mismanagement.

But the strongest glue is culture, as the manifestation of the organisational identity. Culture defines most strongly “the way” the organisation works.

Imagine the business as an individual with a well-defined personality. In different cities that individual might speak different languages and dress in different clothes, but still express the same values.

With a well defined and well expressed organisational personality, localisation can occur without fear of corruption of the brand identity, consistency and controls. Then the chain-store can truly become a local store and part of the consumer’s life as it is.

The other choice, of course, is to wait for a significant part of the local consumer to adapt to your international or national template. Would you be prepared for that?

Devangshu Dutta

May 9, 2009

Bernice Hurst, Contributing Editor, RetailWire mentioned the “Let Children Grow” campaign in the UK jointly promoted by The Independent on Sunday newspaper and the highly respected gardening charity, the Royal Horticultural Society (RHS). Launched in 2007, the RHS Campaign for School Gardening, sponsored by the food and grocery retailer Waitrose, is a nationwide scheme designed to encourage schools to create gardens and teach children the skills of growing plants.

It is described as “an ambitious initiative to encourage the nation’s children to grow their own fruit and vegetables”. The programme targets deprived areas, particularly those with combinations of poor health, low income and levels of aspiration. By working with young people, the idea is to improve their health while teaching them what to eat and where food comes from. RHS research suggests it can “help improve academic achievement, behavior and confidence among pupils”.

According to the Independent on Sunday, most of the children “are learning for the first time about gardening, and with it the enjoyment of fresh air, appreciation of the environment, healthy eating and in turn the prospect of a longer life.”

Bernice Hurst asks, “Can/should retailers encourage and sponsor such education programs to inspire consumer loyalty?”

As far as I can tell, if there is a country in love with its gardens, it is the UK, so this should be a hit with the parents and the teachers.

Pre-teens certainly don’t mind getting dirt under their fingernails, so it should appeal to them as well.

Whether this has any tangible impact on Waitrose’s image and business remains to be seen but, then, some things should simply be done because they are the right thing to do.

The RetailWire discussion is here: Looking at Literal as Well as Figurative Growth, and the Independent article is here: Digging for victory: Schools back gardens plan.

admin

May 9, 2009

By Devangshu Dutta, Tarang Gautam Saxena

While the Indian consumers have aspired to own international fashion brands, India’s large population base in turn has been an aspirational market for the international companies.

To remote observers, the Indian market may appear to be a virgin territory as far as international apparel and footwear brands are concerned. But India has seen the presence of international brands for almost a century, including mass brands such as Bata and luxury brands such as Louis Vuitton. However, as the colonial government systematically repressed local textile production, the local resistance to foreign products grew as well. Therefore, until the 1980s, the presence of international fashion brands was negligible.

In the early 1990s, as the Indian economy opened up again, a few international fashion brands entered the Indian market. The pioneering companies during this stage were Benetton, Coats Viyella and VF Corporation.

At this time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment which was thus a target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike).

In the midst of this the media industry was also witnessing a high growth which aided the international brands in gaining visibility and establishing brand equity in the Indian market.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. A growing supply of good-quality retail real estate in the form of shopping centers and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores and shops-in-shop.

The number of international brands continued to grow each year at a steady pace until the early 2000s, and took off exponentially thereafter. By 2005 the number of international fashion brands present in India was over three times compared to that in the mid 1990s. The last few years (since 2005) have continued the significant growth of international fashion brands, including luxury brands such as LVMH, Aigner, Tommy Hilfiger and Chanel.

The Popular Entry Strategies

Many of the international companies entering India in the late 1980s and 1990s chose licensing as the entry route to India to gain a quick access to the Indian market at a minimal investment.

A few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand.

In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought investors in retail real estate that were ideal franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in “Single Brand” retail). Using this route, many brands have entered India by setting up majority owned joint ventures, or transitioned their existing franchise arrangements into a joint venture structure.

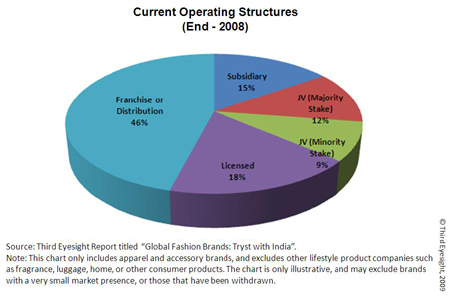

The Entry Structure for Some International Brands

| Entry Strategy | Time Period | ||

| 1980s or Earlier | 1990s | Post-1999 | |

| Licensed | Louis Philippe, United Colors of Benetton and 012, Wrangler | Allen Solly, Arrow, Jockey, Lacoste, Lee, Nike, Van Heusen, Vanity Fair | Puma |

| Wholly Owned Subsidiary | Bata, Pepe Jeans | Levi’s® | Hanes, Triumph |

| Joint Venture (Majority) | Adidas, Reebok | Diesel, Nautica, Sixty Group | |

| Franchise or Distribution | Aldo, Burberry, Canali, Versace, Debenhams, Esprit, Gucci, Guess, Hugo Boss, Mango, Marks & Spencer, Mothercare, Tommy Hilfiger | ||

| Joint Venture (incl. Minority Stake) | Celio, Etam, Giordano | ||

Source: “Global Fashion Brands: Tryst with India” (A Report by Third Eyesight) © Third Eyesight, 2009

Note: The above table shows the structure used during entry, and not the structure that exists currently.

By the end of 2008, just under half of the brands were present through a franchise or distribution relationship, while over a quarter had either a wholly-owned or majority-owned subsidiary. These structures allowed the brands to have greater control of operations, particularly of product.

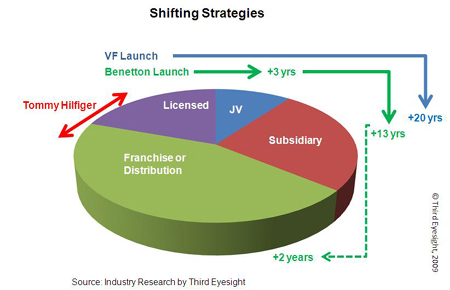

Shifting Strategies

Many international companies have evolved their presence in India into structures different from those at the time they entered the market.

A good example depicting the shift in business strategy is that of VF Corporation which entered India in 1980s by assigning the Wrangler license to Dupont Sportswear. Since then it has launched a variety of brands in different product categories with number of Indian partners and finally formed a joint venture, VF Arvind Brands Pvt. Ltd., with Arvind Brands.

Another example of a company that has evolved its presence is Benetton, which first entered India through a licensee (Dalmia). Benetton then transitioned in 1991 into 50:50 joint-venture and finally in 2004 took over the Indian business completely. However, it adopted the franchising route in 2006 for its premium fashion brand, Sisley, appointing Trent (a Tata Group company) as the national retail franchisee.

Many other companies such as Nike, Tommy Hilfiger, Marks & Spencer and Pierre Cardin (as described in our report “Global Fashion Brands: Tryst with India”) have changed their approach as the original structures did not perform as well as they had expected.

Obviously, each such change has cost the brands time, management effort, money and, sometimes, market share.

We believe that these shifts and the pain related to it could have been reduced, had the brands ruthlessly questioned the motivation for considering this market and their expectations from the market in determining an appropriate strategy.

What’s Ahead?

In the midst of economic upheaval around the world, how does India look as a market for international fashion brands?

Well, it is difficult to generalize even in the best of times. In the current global turmoil there is certainly a lot more unpredictability about international expansion for most companies.

Although India’s position as a target market for international brands has been improving, as is evident from the number of launches in the last 6-7 years, some companies considering international expansion may prefer entering other markets that may seem more “familiar”, developed and safe (such as Europe, Japan, South Korea or Taiwan). Against such comparisons, India’s growing but fragmented market can seem chaotic and difficult to deal with.

However, the fact remains that there are very few markets globally that can provide the sustained size of mid-term and long-term opportunity that India does. We are already seeing the more far-sighted and committed brands consolidating their position and presence in the market by continuing to look at expansion, even while examining how they can make their existing points of sale perform better. We also constantly come across new companies carrying out investigations into the market.

In the current environment we expect to see a shift in the nature of launch vehicle. While franchising seems to be a safe option for risk-averse brands in the current times, we will probably see more brands with a long term strategy, who would establish a controlled presence either through joint-ventures or through wholly-owned subsidiaries, since they can lay the foundation of the business today at much lower costs today than in the past few years.

India’s foreign direct investment (FDI) policy, allowing FDI only up to 51% in retail trading of “Single Brand” may have held back some fashion brands as they are still managed by owner founder with a conservative outlook on “control”. However, in the last couple of years, we have found companies not being deterred by the barriers to FDI.

As their comfort and familiarity with India has grown, international companies are more willing today to create corporate structures that allow them a presence in the market today and a step-through to a more controlling stake as and when government regulations allow.

All in all, we feel that international brands are in India not only to stay, but also to expand. There is yet a lot of potential untapped in the market, and as the integration of the Indian consumer with global trends continues, international brands can expect to find India an increasingly fertile ground for growth.

(c) 2009, Third Eyesight

Tarang Gautam Saxena

May 8, 2009

In a recent workshop on fashion styling, we were discussing how the retail seasons have evolved. In the developed economies, from the traditional two seasons – spring-summer and autumn-winter – the number of seasons grew as fashion brands discovered or invented (take your pick!) sub-seasons to create and satisfy distinct demand in specific time periods. For many companies, the number of “seasons” has grown to 10-12 now including transitions and “promo season” series.

India, you would think, essentially has two seasons, the summer and the festive season. However, in the last decade or so, as exposure to the global culture has increased, other “seasons” such as the “Valentine’s Day” have emerged and proved important for retailers.

In fact, events such as the “Sabse Sasta Din” (“the cheapest day”) on the 26th January (India’s Republic Day) created by Kishore Biyani’s Big Bazaar in 2006 should also qualify as seasons, given the huge sales upsurge during the event. In fact, the impact has been such that many other retailers and brands have also taken this concept rather seriously this year. In fact, after a rather dull consumer response in the festive season in 2008, many of our clients reported rocking sales in the last week of January 2009 on the back of heavy promotional campaigns.

More recently while voter awareness campaigns such as “Pappu can’t vote” have been effective marketing initiatives to get many of us out of our comfort zones and exercise our voting rights, many retailers and brands have also seized this opportunity of citizens’ awakening by offering up to 20% discounts to those who have voted. The economic slowdown is certainly getting people to think differently and more creatively. So, “Jago re” (awaken) brands, retailers and countrymen – go ahead and fashion your own season!

Devangshu Dutta

May 2, 2009

Wal-Mart has just opened a new store Supermercado de Walmart in Houston (Texas). The Houston Chronicle reports that the Supermercado aims to reach out to the Hispanic population, tailoring the foods more to Hispanic tastes and needs and adding signs in Spanish. Wal-Mart is also reportedly planning to open a Mas Club this summer, based on its Sam’s Club warehouse outlet, but focussed again on Hispanic customers. (The original article is here: Wal-Mart gives its Supermercado concept a tryout).

Going by some of the negative comments attracted by the article, it is legitimate to ask: what will Wal-Mart’s existing customers think, and how will they behave?

I guess the answer is clearly not black or white (or beige, red, yellow or brown for that matter).

Wal-Mart is segmenting and localizing its offer as a smart information-rich retailer should.

Some customers who hold a tightly parochial view may feel alienated when they read about this development and may stop shopping at Wal-Mart, but most probably won’t bother as long as their local Wal-Mart continues to deliver what they want at prices they like.

Vibrant societies and economies are true melting pots; rather than exclude, filter and ensure conformity, they imbibe and blend newness. The fact is that real assimilation causes both to change – the ones coming in and the society / geography taking them in – and we have to accept that change often brings some pain with it, as expressed by the reader commenting on Houston Chronicle’s website.

The first waves of European settlers created a change when they started landing in North America 500-odd years ago, and so has every wave of immigrants since – Chinese, Japanese, German, Irish, Italian, Eastern European, Korean, Indian, Caribbean and so on. The first settlers will always be suspicious and exclusive in their approach towards the second set, the second lot of the next and so on.

The wave of economic homogenization driven by the post-war baby boom and infrastructure expansion was possibly one of the largest in recent history (other than the Soviet Union and the Chinese Cultural Revolution, which were more political than economic). However, we’ve seen the US market grow in diversity in the last 2-3 decades – not only because of differences due to race or country of origin, but also due to geographic, economic and otherwise cultural differences.

Today many of the diverse segments today in the US are large enough to express their unique needs, and expect them to be fulfilled. While the cookie-cutter approach served well during the years of national expansion across homogenized markets, that approach is counter-productive today. A retailer like Wal-Mart can’t be expected to ignore that fact.