admin

May 1, 2026

Yuthika Bhargava & Vikash Tripathi, Outlook Business

Mumbai, 1 May 2026

For generations of Indians, the word Tata hasn’t just been a brand, it has been a permanent resident in our homes. Think back to the kitchens of your childhood. It was the familiar packet of Tata salt, the Desh ka Namak, that seasoned every meal. It was the steaming cup of Tata tea that signalled the start of the day for elders at home.

In every Indian household, the name represents trust and legacy.

Yet, when N Chandrasekaran, chairman of Tata Sons, wanted to hire Whirlpool India’s head Sunil D’Souza to lead Tata Global Beverages (TGBL) in September 2019, he got a shock refusal.

Who in their right minds wouldn’t want to join a Tata company?

Well, D’Souza hadn’t heard much about TGBL. In fact, his colleague at Whirlpool India had called it a “sleepy company”.

At the time, TGBL’s revenues were a meagre ₹7,408cr compared to close to ₹50,000cr and ₹40,000cr logged by fast-moving consumer goods (FMCG) heavyweights ITC and Hindustan Unilever (HUL), respectively, in 2018–19.

Experts had noted TGBL had not much to show in terms of major product innovation for years. Primarily a tea and coffee company, it was locked in a low-growth cycle.

In 2018, various analysts had remarked that TGBL’s growth was muted as it wasn’t selling anything beyond tea and coffee.

At TGBL’s annual general meeting on July 5, 2018, Chandrasekaran said the company would exit loss-making subsidiaries and focus on profitable ones that can be scaled up. “Even though in volume terms, the company continued to be number one in the Indian market, the same was not true in value terms,” he said.

So, D’Souza’s immediate “no way” to the job offer was justified. TGBL wasn’t on his radar or anyone’s at the time.

But the headhunter convinced him to meet Chandrasekaran.

This meeting, says D’Souza, made all the difference for him. He recalls the Tata Sons’ chairman saying “I have the money. But I don’t have the team to run it.”

But the clincher for him was Chandrasekaran’s larger plan to foray into the FMCG space and the intent to disrupt the market.

In December 2019, Tatas announced D’Souza’s appointment as managing director and chief executive effective April 2020. One more important addition to this FMCG team was Tata Sons’ Ajit Krishnakumar as chief operating officer.

What followed was the duo’s visits to Mumbai, Bengaluru and Gurgaon. They walked to distributor offices and kirana stores and sat through market visits. “We drew out in great detail what we wanted this company to look like,” says Krishnakumar.

The mandate from Chandrasekaran was simple. He wanted a company commensurate with the Tata name, one that shared the same shelf space as the likes of HUL and ITC.

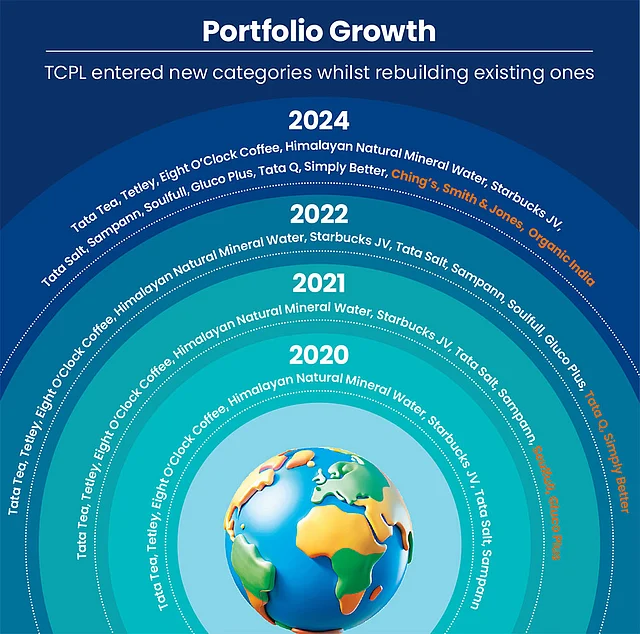

Humble Beginnings

The mission to become an insurgent company in the FMCG space kickstarted with the formation of Tata Consumer Products (TCPL) in February 2020 by merging TGBL’s tea and coffee units with Tata Chemicals’ salt and pulse businesses.

However, with established FMCG rivals like HUL, ITC and Nestlé India, D’Souza and Krishnakumar had their tasks cut out. The competition had a century of headstart in India.

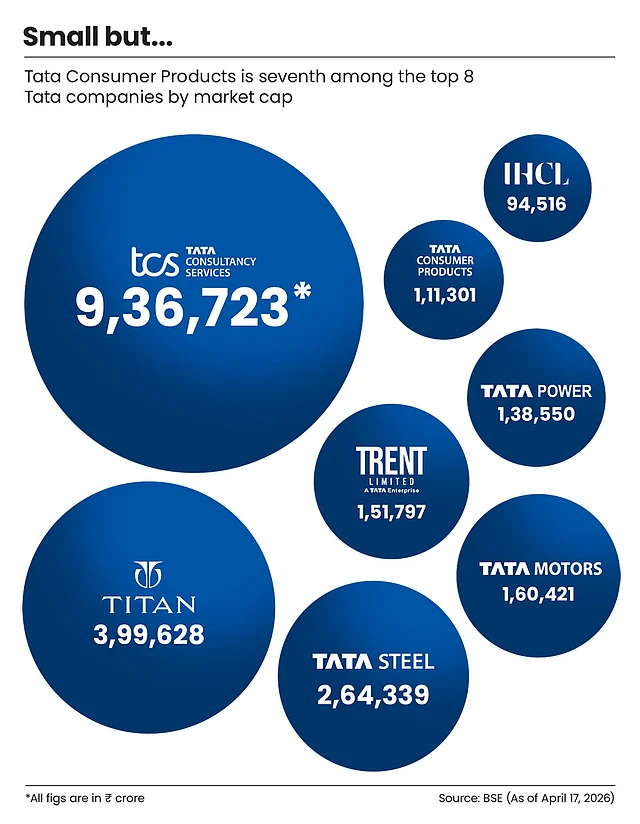

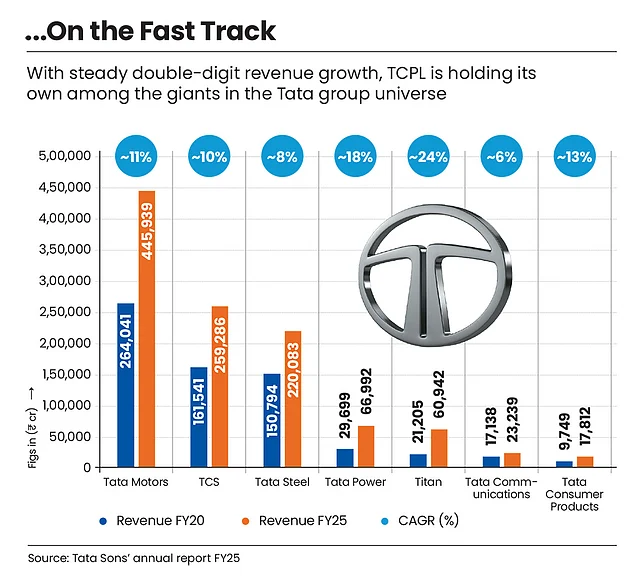

Within the Tata group itself, TCPL ranked eighth by revenue in 2019–20, behind Tata Motors, TCS, Tata Steel, Tata Power, Titan, Tata Communications and even Tata Chemicals.

But “things couldn’t get any worse than this, right? We were already at the bottom of the heap in FMCG. You could only get better,” recalls D’Souza about his mindset at the time (see pg 24).

Building a brand name as a Tata company opens doors. But competing is another. Could this new company take on HUL, Nestlé and ITC?

TCPL started by trimming the portfolio, streamlining the consumer products businesses spread across five continents, from India and the US to the UK, Canada, South Africa and Australia.

In Australia, the company held a 7% share of the tea market but was also running an out-of-home coffee dispensing business that was losing millions of dollars. It was shut down in December 2020.

In the US, a food-service joint venture, including a tea factory and a distribution unit, was disposed of as well in March 2021.

“We had 45 legal entities. That’s not tenable,” D’Souza says. “We exited areas where we didn’t see value. The focus clearly shifted to not just the topline, but margins.”

Six years later, TCPL’s entity count stands at 25 and is well on the way to the target of 18 entities.

What stood out in the next six years is TCPL’s sole focus to dominate the food and beverages (F&B) category. The company’s mantra: think big, move fast.

By late 2020, once the initial scramble post the merger had settled, TCPL ran a strategic exercise called Project Falcon. The result was a playbook: categories to foray into, categories to stay out of, where to build and what to buy.

The year 2021 provided a starting point for TCPL. In March that year, the United Nations officially declared 2023 as the International Year of Millets, acting on a proposal from India. The country being the largest producer of millets, accounting for 20% of global production, wanted to raise awareness of millet’s role in improving nutrition and creating sustainable market opportunities.

The timing was fortuitous for TCPL. In 2021, its first acquisition, Soulfull, was a millet-based health-food brand. This ₹155.8cr deal gave Tatas a foothold in a category it couldn’t have credibly entered on its own.

Within three years of acquisition, Soulfull’s distribution had grown from 15,000 outlets to 300,000, carried on the back of the Tata’s existing network.

Three years later, in January 2024, when TCPL announced two deals with combined worth of ₹7,000cr in quick succession, its stocks fell.

The market wasn’t convinced initially. TCPL had just committed roughly 40% of its annual revenue to two brands it did not build. At the time, it was a new player with its core business running on single-digit margins.

Analysts at Ambit Capital estimated the acquisitions would cut 2025–26 earnings by roughly 10%.

The first, a ₹5,100cr deal, was to buy Capital Foods, the company behind Ching’s Secret.

The second was a wellness play, a ₹1,900cr cheque for Organic India, a Lucknow-based brand with a devoted following in the US.

D’Souza had faith in these big-cheque acquisitions. “We are not playing this game for the next one or two years. We do these acquisitions knowing that we put money there. It will bear out over a period of time.”

Ching’s Secret had spent decades building the desi Chinese category in urban Indian homes almost single-handedly—the Schezwan chutney, the noodles and sauces.

As for Organic India, it had a network of farmers across Madhya Pradesh and Uttarakhand, a manufacturing facility in Lucknow and decades of Ayurvedic credibility in the American wellness market. It was built over years of relationships that TCPL simply did not have and could not quickly acquire.

And the numbers weren’t disappointing. By the third quarter of 2025–26, Capital Foods and Organic India together were generating ₹354cr in quarterly revenue, up 15% year on year, at gross margins of roughly 48%, well above TCPL’s blended average of 43%.

Motilal Oswal expects integration costs to ease substantially by 2026–27, after which the margin story should become clearer.

Fight for Shelf Space

From the get go TCPL was clear about the categories it wanted to enter and to avoid as well.

It didn’t want any stake in the basic edible-oil segment. This shelf had far too many players led by the likes of Fortune and Saffola.

But cold-pressed oil was a different ballgame. Consumers here were buying into a health claim with no way to verify if the product was trustworthy. “The Tata name does the magic there,” says D’Souza.

In August 2023, TCPL launched a range of cold-pressed oils under its brand Tata Simply Better, a new brand that was launched in 2022 to enter the plant-based mock-meat category.

The logic: find the trust deficit, fill it with the four-letter Tata name, became the basis for every category TCPL considered entering.

The sweet spot for the insurgent company was categories that were fragmented, where consumers didn’t fully trust what they were buying and where a credible brand could change the equation.

Biscuits was another category that TCPL gave a skip.

Britannia and Parle owned 56% of the market, built over decades of backward-integrated manufacturing and distribution muscle.

This restraint, wrote Motilal Oswal, in a recent note, is “rare in Indian FMCG”. Categories like biscuits, snacks, colas and base edible oils are permanently off the table, crowded segments where the Tata brand adds no meaningful trust-led differentiation. “Such portfolio discipline is a positive indicator of capital allocation quality,” the note observes.

Built organically, cold-pressed oil is now running at an annual revenue of ₹350cr. Dry fruits, another category Tatas entered with the same trust deficit logic is at a ₹300cr run rate.

What differentiates TCPL from other FMCG players?

The categories that Tatas have built or bought into are still being defined. HUL and Nestlé, on the other hand, are dominant in mature markets where penetration is already high. HUL is buying established brands in categories it rules, plugging gaps in existing portfolios. TCPL is buying into categories it has never played in, at scale, while the core business is still being built.

Whether this is disciplined offence or over-extension is a question the next two years of integration will answer.

Even before acquisitions came into play, among the first things D’Souza and Krishnakumar did was to build accountability. There had been no one person who owned a category (tea, salt or pulses) from manufacture to sales.

They created category leaders who were responsible for the product’s profit and loss, bar the fixed costs. Functions that did not exist were created.

In 2020, Tata Salt was present in nearly 2mn retail outlets across India. TCPL’s own salespeople directly visited just 150,000 of them. The remaining 1.85mn stores were being supplied through a chain of middlemen, called super stockists or consignee agents.

These middlemen picked up Tata Salt in bulk from big distributors and moved it onward through their own networks. No one from TCPL knew what was selling fast, what wasn’t or what product a rival had placed on the shelf just two rows away.

“That shows the strength of the brand and also the lack of distribution reach,” says D’Souza. In FMCG, this gap between a brand’s total reach and its direct reach is called the wholesale multiplier. It measures how many outlets are stocking your product for every outlet you directly supply. A multiplier of five is considered normal. TCPL’s was 15, a number almost unheard of.

This meant TCPL had no direct relationship with over 90% of the shops and no mechanism to introduce anything new in those shops.

“There was this big layer [of middlemen] in each state. We removed that entire layer. That layer alone was about 1.2% in terms of cost. Then we appointed proper distributors, recruited the right people and rebuilt the distribution system,” says D’Souza. This was a saving of 36 paise on every 1kg pack of Tata Salt with an MRP of ₹30.

Rebuilding the entire distribution ecosystem took six to seven months. The distributor base was cut from 4,500 to around 1,500–1,600. These distributors were now carrying the full portfolio, reporting directly to TCPL. The sales force was expanded by 30%.

The results were quick. TCPL’s direct outlet reach stands at approximately 2.3mn today from roughly 500,000 in 2019–20. The total reach is 4.4mn outlets now.

“There are two key benefits to getting closer to the retailer. It supports margins and gives you better visibility into what’s happening at the point of sale,” says Arvind Singhal, chairman of The Knowledge Company, a management-consulting company.

Progress is real. But TCPL has miles to go. HUL reaches more than 9mn outlets, built over nine decades. ITC reaches 7mn. Nestlé 5.2mn. India has roughly 12–15mn kirana stores.

“The whole premise was to create a distribution funnel through which you can then push different products,” says D’Souza.

Bump in the Road

The first real test for TCPL was whether the idea of pushing new products through the distribution funnel would work.

Pradeep Gupta, a kirana store owner in Varanasi, has been a witness that it worked. Six years ago, two products were always on his shelf: Tata Salt and Tata Tea Premium. He didn’t need a salesperson to tell him to stock them.

Now, new products from Tata Sampann spices to Ching’s Secret sauces and Soulfull rusk are on the shelves of Gupta’s tiny store. TCPL’s distribution network made it happen. A distributor who had built his business around Tata Salt would now also handle Ching’s Secret. A salesperson who knew how to move a commodity would now pitch a branded sauce.

But not everyone was happy. The All India Consumer Products Distributors Federation (AICPDF) went up in arms against TCPL in 2025. Distributors were protesting excessive targets, stocks were piling up in warehouses and damaged goods sitting for months with no settlement.

The mismatch was structural. Salt moves through wholesale with 80% of it never seeing a retail salesperson. Most of the newer growth products like Ching’s Secret are sold almost entirely through direct retail.

Running both through the same distributor was asking a man who sold salt by the tonne to also build a market for Schezwan chutney.

The AICPDF president Dhairyashil H Patil explains what went wrong. “Salt is typically sold in large volumes. Products like Tata Sampann [a packaged pulses brand launched in 2017 under Tata Chemicals] and tea are the opposite, only about 8–10% goes through wholesale. After the merger with Capital Foods, there was a complete mismatch.”

Distributors built around salt did not find it viable to handle retail-heavy products. “Most Tata distributors derive 60–70% of their turnover from salt, so their focus remains there,” adds Patil.

TCPL eventually had to take back damaged goods sitting with distributors for six to eight months. D’Souza’s response was to separate the networks entirely.

TCPL’s growth businesses like Ching’s, Soulfull and Organic India had their own distributors and sales teams in just three months. “For any other company, it would have taken at least a year or more,” D’Souza says.

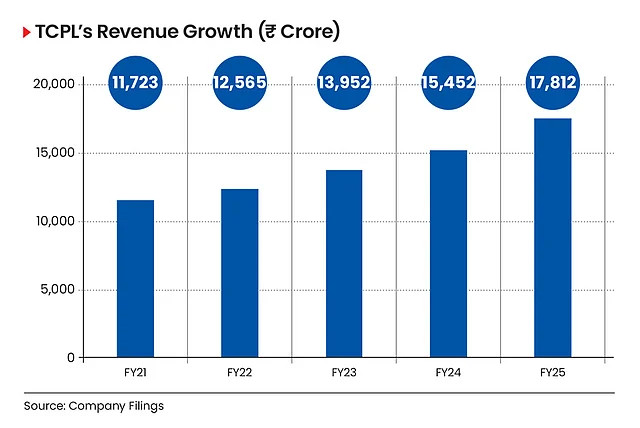

Also, the portfolio TCPL had inherited gave its own answer to what the distribution funnel could carry. Sampann, a “hobby for Tata Chemicals”, arrived at the merger doing ₹150–200cr in revenue. In 2025–26, Sampann is expected to touch ₹1,700–1,800cr, with pulses alone contributing ₹1,000 crore.

“The whole DNA of the company is to stay agile and make sure to move at full speed,” says D’Souza.

Fast and Furious

TCPL moved at full speed indeed when it came to trends. In May 2019, Beyond Meat, a company that made plant-based burgers from pea protein, listed on Nasdaq. Its stock more than doubled on the first day.

Within months, McDonald’s was testing a meatless McPlant and KFC was piloting plant-based chicken. Plant-based meat looked like the future of food.

TCPL bought into the trend. In 2022, it launched plant-based mock meat under the Tata Simply Better brand. However, the global buzz died sooner than expected. Two years later, TCPL exited the category.

The exit is not the point. What matters is that the product took 150 days from concept to shelf. TCPL had built something that would have been impossible two years before.

Mock meat required food science to replicate the texture of meat from plant protein, process technology, a team of chefs, food scientists and packaging engineers.

Capabilities were built from scratch. In the beginning, the R&D team was just 10–15 people. Today, it operates across three centres: Bengaluru as the research and packaging science hub, Mumbai for food innovation and product development, and Barabanki in Uttar Pradesh, anchoring the wellness work after the Organic India acquisition.

The team remains lean, around 60 people, roughly one-third the size of comparable FMCG rivals, estimates Vikas Gupta, R&D head at TCPL.

When D’Souza arrived in 2019, just 0.8% of TCPL’s revenue came from new product launches. The industry benchmark is 5%. TCPL was nowhere close. Today, that number stands at roughly 5%.

Onkar Kelji, research analyst at Indsec Securities, a brokerage firm, frames the economics of the chase: the early returns on innovation can be thin, he says, as companies push products aggressively and launch on e-commerce where margins are typically lower than general trade. “But if these products scale, they deliver better margins over time.”

Across the industry, the contribution of newly launched products has generally stayed under 5%. With acquisitions, that mix is expected to rise, notes Kelji.

In FMCG, innovation is not only about launching entirely new categories. It is also about rethinking what already exists. “We were singularly focused on vacuum-evaporated iodised salt,” says D’Souza.

The thinking that replaced it was simpler. “Give the consumer what they want. Plain salt. Salt with iron, with zinc. Low sodium for the health-conscious. Himalayan rock salt for the premium buyer. Sendha [during Navaratri]. One product became a portfolio,” adds D’Souza.

A patented granulation technology was developed for double-fortified salt, solving a long-standing industry problem of how to add iron to iodised salt and keep it stable.

TCPL also produced the Tata Coffee Cold Coffee liquid concentrate, a first-of-its-kind product in the Indian market that lets consumers make cold coffee at home without equipment.

The first 100 product launches after the merger took three-and-a-half years. The next 100 took 16 months. At one point, the company was turning out a new product every week, each one requiring its own supply chain, packaging, shelf-space negotiation and own sales story.

For a company that was criticised in 2018 for launching almost nothing new for years, this was a different metabolism entirely. “It’s easier when you are doing everything from scratch, says D’Souza, adding “As soon as we see a trend, we are on top of it and running with it.”

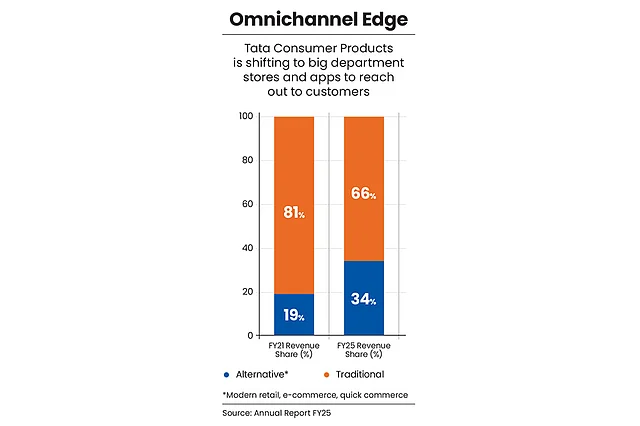

E-commerce is a good example of how TCPL, weeks into its merger, took on the very real challenge of lockdown and built a new digital vertical to boast of.

Lessons from Pandemic

In March 2020, most Indians had online grocery apps on their mobile phones. These were rarely used. But the Covid-19 pandemic and subsequent lockdown reshaped this landscape.

BigBasket’s servers strained with massive order volume surge. Dunzo crashed repeatedly. Amazon Fresh ran out of delivery slots. Millions of urban Indians were struggling to restock their kitchen shelves.

At the time, TCPL’s entire e-commerce operation was one person’s part-time responsibility. The southern regional sales head looked after e-commerce. TCPL had to race against time to build a digital channel. And D’Souza’s team built it fast.

E-commerce became a dedicated function with its own head. A modern trade team was created. Every new product launch went digital first. E-commerce gave TCPL something general trade never could: unfiltered data on what actually works.

While the company’s overall innovation-to-sales ratio was 3.4% by 2022–23, it was 10% on e-commerce. Products that proved themselves online were then pushed into general trade.

“The beauty of e-commerce is that it is only you and the consumer. It is the power of your product and your brand and your value proposition,” D’Souza said in an earnings call.

E-commerce’s revenue contribution at the time of merger was 2.5%. By late 2021, it was 7%, a growth of 130% in a single year. By 2024–25, it reached 14%, overtaking modern trade for the first time. By the third quarter of 2025–26, e-commerce and quick commerce together stood at 18.5%.

“I don’t think anyone else is in this ballpark,” says D’Souza. He is not wrong. HUL’s equivalent figure runs at 7–8%, Nestlé India’s at 8.5%. The company that almost missed the decade’s defining channel shift now leads it among its peers.

What makes the number more significant, according to Motilal Oswal, is TCPL’s margins on quick commerce are comparable to traditional channels, unlike most peers, who are seeing margin erosion on the platform.

The Tata group’s acquisition of BigBasket in May 2021 gave TCPL a window into how millions of Indians shop for groceries.

In an earlier earnings call D’Souza pointed out that BigBasket is a group company, not a TCPL asset. But within the group, he said, they were working closely to find synergies.

The channel shift also fits the company’s portfolio. Quick commerce skews toward the premium buyer: the person reaching for Himalayan rock salt at ₹100 rather than iodised salt at ₹30, Organic India’s tulsi tea rather than a commodity tea bag.

The premium end of TCPL’s portfolio, built over five years, is precisely what the fastest-growing channel wants. The mass business still dominates revenue.

Half-way Mark

In January 2021, D’Souza said, “If we get it right, the rewards would be endless. If we didn’t, we’d have to live with it for a long time.” Five years later, he rates himself “five out of 10”. Ask him what TCPL has that HUL and Nestlé don’t, and the answer is the four letters T-A-T-A.

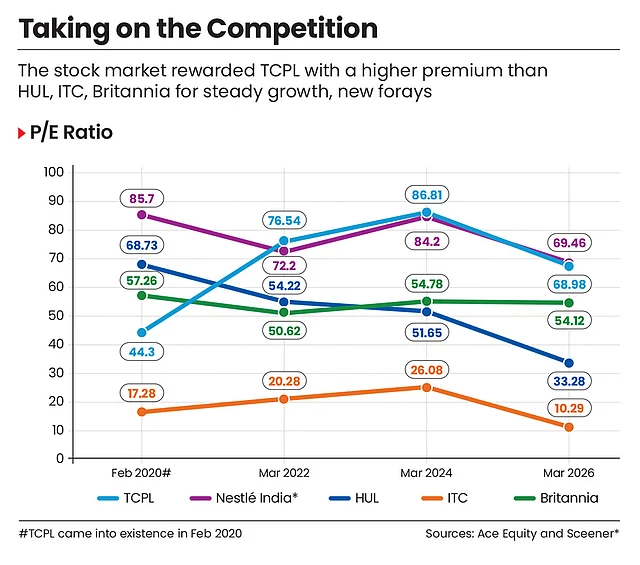

Here is what five out of 10 looks like. TCPL’s revenue has grown over 80% between 2019–20 and 2024–25. In annual terms, that is a compound rate of roughly 13%, faster than HUL’s 9.8%, Nestlé India’s 10.5% and ITC’s 9.7% over the same period, albeit off a smaller base.

TCPL reported a consolidated annual turnover of ₹17,618cr in 2024–25. Its operating margin, what survives from every rupee of revenue after paying for everything, runs at 14–15%. HUL’s is 23–24%.

Closing this gap requires high-margin businesses like Ching’s, Organic India, Soulfull, cold-pressed oil to grow fast enough to become roughly a third of total revenue. Right now, they are 8–9%.

Tea costs, which TCPL cannot control, need to normalise. Integration costs from the 2024 acquisitions need to wind down.

Motilal Oswal projects margins reaching 17% in three years. The path to 20%-plus, where HUL and Nestlé operate, is considerably longer than that.

Return on capital, how much profit a company earns on every rupee invested, tells the same story from a different angle. TCPL’s sits at roughly 10%. HUL’s is 27%. D’Souza points out that the core business, stripped of the 2024 acquisition capital, delivers 30%-plus.

The acquisitions are dragging the consolidated number while they are still being absorbed. Most analysts expect the trajectory to improve. The question is whether it does so within the timeline management has guided.

D’Souza describes the portfolio in three segments: the international business: Tetley, steady and cash-generative. The India staples: tea and salt, large but low-margin, subject to commodity costs he cannot control. And the growth businesses: Ching’s, Organic India, Soulfull and cold-pressed oil, which are small today but carry the highest margins and expectations.

“All three pieces need to come together,” says D’Souza.

“Each piece in the portfolio has a very specific purpose,” explains Krishnakumar. International for steady margins. Sampann for growth. Capital Foods and Organic India for both. “The headline target ties it together: a double-digit-plus topline and a bottom line growing higher than that,” he adds.

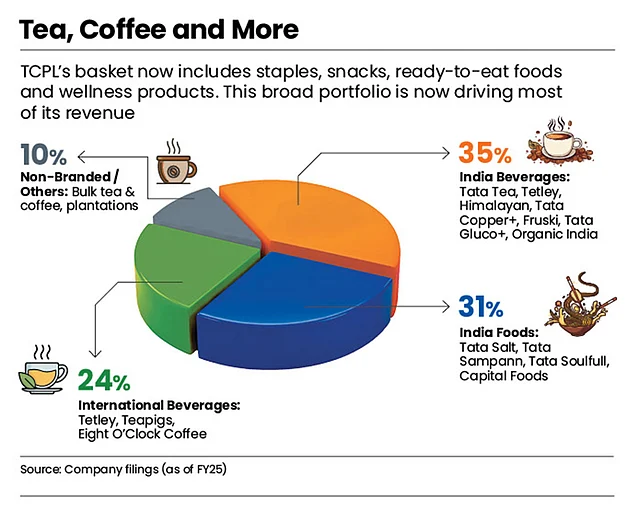

Today, the portfolio spans tea, coffee, water, ready-to-drink beverages, salt, pulses, spices, ready-to-cook and ready-to-eat offerings, breakfast cereals, snacks and mini meals.

However, the product range is in the food and beverages (F&B) universe. The company does not yet cover much else. “Without personal care or home care, TCPL is not yet a comprehensive FMCG powerhouse,” says Devangshu Dutta, founder of Third Eyesight, a boutique management-consulting firm.

Krishnakumar’s response is: “On a revenue basis, F&B accounts for nearly 80% of the FMCG universe. Outside of F&B, it requires a very different set of skills, a very different DNA.”

TCPL is not making bets in personal-care or home-care segments in the near future.

The Long Game

“There’s no magic breakout moment,” says Krishnakumar. What he points to instead are accumulations: salt crossing million packets a day, the stock market re-rating and the innovation pipeline turning out a new product every week.

The competition, however, is not waiting. HUL’s quick commerce is logging 3% of revenue, growing at over 100%. ITC plans to spend ₹20,000cr over five years with the bulk for foods. Nestlé is deepening its product pipeline.

These rival FMCG companies are now moving faster than they have in years. For TCPL, the race has gotten harder.

At the same time, these giant competitiors have their own challenges. HUL draws only 25% of its revenue from foods. Nestlé is concentrated in dairy and confectionery.

ITC, which is still moving away from tobacco, draws 40% of its revenue from packaged foods and personal care combined.

While these Goliaths have their attention split, TCPL’s focused approach is perhaps the one thing they cannot replicate. “In any category that we have a stake in, we would be among the top three brands,” says a confident D’Souza.

Six years in, the pieces are in place. “Our strategic road map and the strong foundation we have laid for the business have yielded good results…Our overarching ambition is to evolve into a full-fledged FMCG company,” Chandrasekaran said in TCPL annual report 2024–25.

Whether TCPL becomes big and matches his vision is a question the next six years will answer.

Within the Tata group, TCPL’s revenue ranking may not have moved much: eighth in 2019–20, seventh today. Both profits and market capitalisation have grown more than three times. It’s now worth over ₹1 lakh crore, nearly seven times Tata Chemicals, and more than double that of Tata Communications.

The market is not pricing what TCPL is. It is pricing what it might become. “Because if you’re not in the top three, there is no point,” says D’Souza. The man who chose to walk into the “sleepy company” is not done yet.

(Published in Outlook Business)

Devangshu Dutta

November 30, 2010

This article is based on a presentation at the 2nd International Summit of Processed Food, Agribusiness and Beverages, organised by the Associated Chambers of Commerce (ASSOCHAM) and supported by the Ministry of Food Processing, Government of India. The presentation was made to a mixed audience of retailers, manufacturers, farmers, government functionaries and service providers, and rather than provide answers, the objective was to raise questions that were not being discussed.

The old saying goes: where there are issues, there are opportunities. By that standard, the perishable commodities supply chain offers plenty of issues and, hence, opportunities.

Part of the problem, or opportunity, is that there are so many steps between the farmer and the consumer, so many hands through which the produce passes, especially in the case of India. With every step in this supply chain, there is the potential of waste and deterioration with time, and on the flip side, there is also an opportunity to add value and improve.

Misalignment on Motivation

One core issue, at the heart of most problems with the perishables supply chain, is widely different perspectives and the lack of alignment.

For instance, there is competition at the basic level between cities and villages. But there is even misalignment between the development needs of ever-growing cities that are taking over neighbouring agricultural lands, and the need to feed people living in those very cities. Similarly, the motivations for small sustenance-driven landholders are different from those of the wealthier farmers with large holdings. And, of course, within the supply chain, the tug of war is between consumer vs retailer, retailer vs brand, brand vs producer.

This is but natural in any economy, even more so in India whose rapid growth is widening the already existing gaps and intensifying the inherent disconnects.

Misalignment on Value

However, there is also another significant potential misalignment, of which we need to be keenly aware. This is in the very definition of value.

Given that we have been discussing “value-addition” as a driver for the food supply chain, I think we also need to understand that the word value has various connotations and implications, depending on who we are speaking about. Each throws up different challenges, and needs to be dealt with differently.

In my mind, the three aspects of value related to the food sector are:

The complication is that these three aspects address three very different audiences in society.

For a large part of India’s population, simply providing adequate calories is the main problem. For this chunk of people, not only do we need to have more productive land under use, we need to maximise the output from each piece of land, and ensure that the productive output reaches the population that needs it the most. Within that, there are several social, political, logistical and economic challenges to tackle: clarity of land-holding, availability of arable land to agriculture rather than non-agricultural uses, unit area productivity with efficient use of other resources, safety during transportation and storage, and distribution at prices that are affordable.

Nutritional value is the next step up: packing more nutrients into each gram of produce and delivering the right mix and balance is a critical issue for consumers who get enough calories, but can benefit hugely in physical and mental health through the quality of the nutrition they are taking in.

In pushing up both calorific and nutritional value, we also run into two entirely different debates.

One is whether genetic modification (GM) is desirable. The argument against GM foods is that we shouldn’t tamper with the most basic building blocks of biology, because we don’t understand the implications completely. The powerful argument for GM is that it is a must, to ensure that we have enough and ever-improving food available to a growing population.

The second debate is about organic produce. The organic camp believes strongly that organic is better, nutritionally superior. The other side argues that organic delivers no clear demonstrable increase in either calories or nutrition, and instead pushes production down and prices up: a recipe for complete disaster in a growing country.

But most interesting to me is the fact that in most industry platforms such as this, when we speak of “value-addition”, it is neither calorific nor nutritional value that is being targeted, but only economic value.

Obviously, companies are profit-driven by their very nature, and if calorific or nutritional value does not deliver economic value to them, they will not focus on those aspects. For that reason, most companies engaged in or being encouraged to participate in the food supply chain do so through food processing: the transformation of the basic produce into a manufactured packaged product with higher economic value per gram. A thinking consumer may be tempted to ask, am I getting proportionately better food (especially more nutrition) for the extra unit value that I am paying for orange juice (as compared to oranges), ketchup (as compared to tomatoes) or chips (when compared to potatoes)?

My concern is that such a deep misalignment in the definition of value can cause a huge amount of friction and potential politicisation, especially if only one aspect of “value-addition” is constantly in focus.

Misalignment on Losses

I’d also like to briefly comment on another aspect of value: losses.

We’ve all come across the much-quoted “fact” that in India 30-40% of the agricultural produce is wasted. That’s incredible! A country otherwise so frugal pushes a third of its valuable food into the gutters? Can that really be true?

I have not come across any authoritative study that clearly demonstrates that India actually wastes that much food.

Of course, there is wastage due to improper harvesting, lack of post-harvest processing and gaps in the storage and transportation infrastructure. But that figure, depending on what product and part of country you pick, varies hugely and the overall average is nowhere close to the 30-40% figure.

Overestimating the size of the problem leads to overestimation of the opportunity, and that misdirects investment. I think the correct way to look at the issue is not just in terms of value-lost, but in terms of opportunity lost. There is certainly an opportunity for farmers to grow their incomes by ensuring that better agricultural and post-harvest techniques are followed. If harvesting products at the right time, chilling the produce at the farm immediately, adequate sorting and grading, or even the simple act of washing can lead to higher prices for the farmer, I’m all for it.

The opportunities we are missing may be bigger than the waste that we imagine.

The Drivers of Value

Obviously, the technological, political and business mandate changes dramatically, depending on where we want to focus on building value. Is it to increase, improve, protect or change the produce? Are we going to focus on the seed, on growth, on harvest and post-harvest, on processing, on storage, on packaging or marketing.

Given the diversity of the questions, I think the discussion on value should also include – openly – a widely inclusive group. Obviously large corporate retailers, brands and producers, and the various arms of the government would be part of the discussion, but the table should also have room for farmers of every hue, technology innovators that address not just aggregated large land-holdings but also small farms, and platforms that encourage both ultra-modern and traditional knowledge, both from within India and outside.

By focussing on an over-simplified view of “value-addition”, we risk not addressing fundamental issues. In fact, we could be losing sight of humongous opportunities.

In the food supply chain, we are dealing with a product that is perishable; given our economy’s rapid transformation, the opportunities are perishable, too. We should get cracking.

(To download the PDF of the presentation, please click here.)

Devangshu Dutta

February 28, 2010

Who knew that a mere vegetable – the humble purple, shiny brinjal, eggplant, aubergine – could create such an uproar?

And why retailers and consumer product companies should be concerned about genetically modified (GM) crops is a complicated story with multiple twists and turns across political, economic, social, scientific and philosophical landscapes.

At their basic level, brinjals have so far been possibly equally hated and loved for their flavour and texture across the world. But their newest avatar – Bt Brinjal – is now being viewed on the one hand as an evil alien transplant that will kill everything good and natural, and the first step of capitalist monopolies to dominate food crops in a large and growing market, while on the other hand it is seen as a saviour of the embattled farmer, an eco-friendly alternative to pesticides and a well-thought out scientific solution to agricultural productivity.

Though it might appear that genetically modification is a 20th century invention, the fact is that such food is not new. Since the time we began farming some 10,000 years ago, we have been carrying out genetic screening and selection, and modifying to create plants and animals that suit our purposes. All farmed products are a product of artificial rather than pure natural selection, as humans have pure-bred and cross-bred strains of crops that are seen as more beneficial in terms of nutrition, hardiness and ease of cultivation.

However, there are some important differences between earlier efforts and now, which underlie the recent loud and violent debate. Let me outline the concerns as seen from the anti-GM side of the table.

Previous genetic selections and modifications happened not just over generations of plants, but generations of human beings. By default, this allowed time to try and test different variants and arrive at varieties that met multiple criteria – profitable cultivation, nutrition, taste, durability and safety. There are concerns that not enough is known about the eventual impact of the new GM crops on human and environmental health, and the speed of adoption frightens people. (In 1948 a Swiss chemist was awarded the Nobel Prize for his work on DDT’s effectiveness as a pesticide, just a few short decades before it was banned from widespread agricultural use for – among other things – apparently causing cancer, and being acutely toxic to organisms other than the pests at which it was targeted.)

In the past, if some variety was wiped out due to climatic variation or pests, it was very likely that alternative varieties were close at hand to substitute it. (Estimates about the number of brinjal varieties in India alone vary widely, from 2,000 to over 3,500 though most of them are not actively cultivated in any significant number.) On the other hand the agricultural information and supply chain today is far more integrated, allowing a previously unknown speed and completeness of adoption of new technology and inputs, frequently at the cost of traditional knowledge. Extinction of natural species is not just due to hunting or disasters, whether man-made or natural. If a new engineered variety is profitable in the foreseeable future, farmers would very likely replace other varieties without examining the long-term impact. (This is true also of other inputs, like overuse of heavily promoted synthetic fertilisers or pesticides.)

Previous ‘engineering’ was restricted to pollination, grafting and selection, whereas now we are attempting to manipulate individual genes or sets of genes, and transplanting genes across species (from a bacterium in the case of Bt). This approach is similar to how we look at most things, today – individually, separate from or devoid of the natural context, ignoring any interaction with other elements (other genes, in the case of genetically modified crops). While in some cases there may be no significant impact on the outcome, our knowledge of genetics is far from complete and holistic to be able to confidently make the statement about no long-term harm.

All agriculture in the last 10,000 years was based on the assumption that future generations of the crop could be raised from seed saved from previous generations. Current genetically modified varieties, on the other hand, are seen as corporate intellectual property created with huge investments, where the return of investment is sought from fresh seed being sold by the company to the farmer for each planting. This is one of the most violently opposed aspects of GM crops, not just in developing economies like India but in developed economies such as the US as well.

I believe I’ve listed the major concerns of the anti-GM side of the debate above, with the rider that not everyone on the anti-GM side shares all the concerns equally.

Unfortunately, the debate is neither simple nor clear as emotions and stakes run high on both sides of the debate.

Pro-GM groups and individuals express the view that their opponents are stuck in the past and are standing the way of progress that is urgently needed to solve immediate human problems.

For one, proponents of genetic modification will point out that the humongous increase in human population needs new strains of crops that can grow more with fewer inputs in terms of water, fertilisers and pesticides. Without such crops, we run the risk of widespread food and water shortages around the world. ‘Green’ concerns may also be quoted in favour of GM crops. The argument is that using genetically modified crops would actually do less damage to the environment than conventional crops, for instance by needing lower doses of pesticide, or producing more crop from smaller patches of land.

Another concern quoted by the pro-GM group is that publicly funded organisations do not have the skills, the scale or the funding to undertake massive and rapid research for the breakthrough agricultural solutions needed in the short term, and that fundamental research needs to be carried out by commercial for-profit organisations. Obviously, as an outcome of that, the profit from the intellectual property needs to be protected such that it can provide adequate returns over a period of time.

For now, most governments (including in India) are playing it safe by maintaining the current status, and disallowing the introduction of GM crops, although there are opposing viewpoints even within each government.

As consumers, also, we could take the view, as many consumers are taking, that what exists (or what existed many years ago) is the best and safest option, since it is the most proven. We could give more muscle to producers and sellers of natural, organically grown varieties, by choosing to buy only such merchandise and rejecting GM foods completely.

I wish it was that simple.

I wish we could say that everything artificial is harmful and everything natural is beneficial. I wish we could blithely accepts labels such as ‘Franken-foods’ for genetically modified crops, treating them as a monster creation.

I wish we could say that one side or the other is adopting more robust scientific methods so that we can take clear and well-informed decisions.

As consumers, unfortunately for us, the truth is not so clear. There are pros and cons on both sides, which will get quoted in and out of context, to support different arguments, for and against genetic modifications.

More importantly, both for consumers and the industry, what is not clear is how complete separation of GM and non-GM products can be maintained. Once GM foods enter the supply chain, it is likely that they will mix with non-GM produce, whether at the farm, in storage or in processing. The current compliance standards in the global food sector offer no confidence that the non-GM and GM supply chains can be sealed off from each other and monitored separately, such that retailers and consumers can make their choice with complete confidence that they are buying what it says on the label.

In this case, more time, and a more robust and holistic investigation may be the only solution. The Environment Minister has asked us to ‘watch this space’.

Now what we end up with in terms of individual, social and economic health will depend on what kind of effort and intent goes into that space. Industry, consumers, scientists, farmers, and governments, all have a role to play in shaping that intent. We all choose whether we want the green organic genes – or the other kind, be they blue genes, purple or yellow.

Devangshu Dutta

August 18, 2009

Four months ago in this column (“Organic – Hope or Hype?”) I wrote about the need for customers to make themselves aware of the true nature of organic products, and it is time to reopen that discussion.

Food is an emotive subject with us as consumers, food distribution and retail is big business with us as the trade, and agriculture is a sensitive area of governance.

On top of that, studies are seldom exhaustive enough in terms of sampling, duration of the study, establishment of controls etc., and for every study that proves the superiority of organics, you will be able to find counter-studies and opposing arguments.

In recent years brands have tended to make much of their organic certification. Marketers are known for overstatement anyway, and the promotional language used by some implies (or even explicitly states) that these products are superior to other alternatives. Surely, then, the consumer should be willing to pay higher prices for these “better” products?

If only, if only, facts were that straightforward.

In the earlier column I’d written: “We expect organic products to contain more nutrition and be better for our bodies. While this may be true of organic animal products compared to their inorganic counterparts, it has not been demonstrated for plant products, other than anecdotal experience of taste and appearance.” I had also raised the question: if organic foods are no better nutritionally than inorganic and could be as productive for the farmer, are many of the organic brands just skimming the gullible customer while the going is good?

Well, the debate just got messier. Recently a study sponsored by Britain’s Food Standards Agency last month (July 2009) really set the cat among the pigeons. The report was based on review of existing research papers to find out if organic products were nutritionally superior to inorganic products. And their conclusion was that the studies reviewed did not provide enough evidence that organic food is more nutritious.

Well, what the report really said was that on the basis of the limited number of studies that were deemed to be rigorous enough, there was not enough evidence to prove that organic food is more nutritious.

Okay.

Imagine an examiner saying that he does not have enough evidence to prove that a student who has passed did not cheat. Notice, he is not saying that the student actually cheated. But wouldn’t this statement alone raise suspicion in your mind about the student’s integrity?

Unfortunately, newspapers and electronic media sell headlines, and headlines need to be short and snappy. Here are a couple of examples about this study.

These clearly raise questions about any benefit at all from organics.

In the noise, the disclaimers by the team that prepared the report seem to have been ignored. For instance, this one: “It should be noted that this conclusion relates to the evidence base currently available on the nutrient content of foodstuffs, which contains limitations in the design and in the comparability of studies.” The report also states: “This review does not address contaminant content (such as herbicide, pesticide and fungicide residues) of organically and conventionally produced foodstuffs, or the environmental impacts of organic and conventional agricultural practices.”

Like any good research report, it admits that “it is important to recognise the potential limitations of the review process”. And the final line in the Conclusion section of the detailed report says: “Examination of this scattered evidence indicates a need for further high-quality research in this field.”

As a reader or TV viewer, how many of us would be motivated to go to the original source and read these disclaimers as well?

Promoters of organic farming, such as Britain’s Soil Association, of course, have trashed the study saying that it is too narrow having excluded most of the available research papers since they did not meet the review standards, and that it ignored the biggest long-term health impact – that of pesticides and other chemicals used in inorganic produce.

Their opponents, in turn have trashed defendants of organic farming by calling them unscientific and narrow-minded in their own right. They point out that high-output inorganic farming is far more useful to serving the exploding human population, than low-intensity organic farming.

One of the readers of the British newspaper Daily Mail was emphatic that she didn’t “eat organic stuff to get extra nutrition”, but was “happy to pay more to be free from additives”. Certainly that is a significant benefit that motivates most people who are well into organic products. In an unusual open letter, the Chief Executive of the Food Standards Agency clarified: “Pesticides were specifically excluded from the scope of this work. This is because our position on the safety of pesticides is already clear: pesticides are rigorously assessed and their residues are closely monitored. Because of this the use of pesticides in either organic or conventional food production does not pose an unacceptable risk to human health and helps to ensure a plentiful supply of food all year round.”

The other motivation for organics is our attitude towards the environment, which can either benefit us over the longer term or, if we are irresponsible, it could accumulate toxins which only show their impact over decades and generations. But, let’s be honest, are most consumers likely to buy products because of some distant benefit to the environment, or products that benefit themselves immediately?

Possibly the answer lies in the organic sector cleaning up its message.

Are consumers any wiser after this study and the debate? I’m not sure. For now, my take on this issue remains: be aware and make up your own mind about what you want to ingest, because this debate isn’t over yet.

Devangshu Dutta

April 15, 2009

The organic movement has touched a variety of products, including clothing, cosmetics and home products. Possibly the most emotive area is organic food, because food products are directly taken into the body while other products have a limited and external contact.

In a sense, before the appearance of industrial agriculture and the application of synthetic nutrients and pesticides, all farming was organic. In fact, the traditional Sanjeevan system of India dates back several millennia.

Even the existing organic farming movement has been around since its founding in Europe in the early-1900s. This was initially treated as fad and its proponents were seen as eccentric (at best) or insane. However, as damage to the environment and to human health became a bigger concern, organic farming emerged as the healthier option.

Organic farming is based on the following fundamental premises:

The aim is to drive a more healthy approach all around – for the environment, for people, as well as for the animals and plants.

The organic trade (all products) is currently estimated at over US$ 40 billion globally, with an annual growth of approximately US$ 5 billion. Organic production is driven today more by demand than by supply – in many cases supply constraints of certified organic produce is more of a concern than the market demand.

Every year, increasing numbers of consumers consciously buy organic products regularly or occasionally on the basis that it is good for them and good for the planet. Certainly, true organic farms do not use synthetic materials, avoiding damage to the environment and can help to retain the biodiversity. Whether measured by unit area or unit of yield, organic farms are more sustainable over time as they use less energy and produce less waste.

It is not as if, after decades of individual enthusiasts pushing their ideas from the fringes, consumers have suddenly become more environmentally conscious. This mainstream awareness has possibly been pushed up in recent years by the involvement of large companies which have spotted the tremendous growth of a profitable niche. “Organic” is the new speciality or niche product line that can be priced at a premium due to the greater desirability amongst the target consumer group, with potentially higher profits than inorganic products or uncertified products. Today, at least in the two largest markets (the USA and Europe), large companies have the lion’s share. For instance, statistics from Germany show that in 2007 conventional retail chains sold over 53% of organic produce, while specialist organic food retailers and producers lost share during the year. Similarly in the US, after the development of the USDA National Organic Standard in 1997, significant merger and acquisition activity has been visible.

However, as the interest in organic products has grown, so have the noise levels in the market. With that the potential for confusion in customers’ minds has also grown.

In day-to-day conversations, we tend to treat organic as superior to inorganic. But the reality is a little bit more complex.

For instance, we expect organic products to contain more nutrition and be better for our bodies. While this may be true of organic animal products compared to their inorganic counterparts, it has not been demonstrated for plant products, other than anecdotal experience of taste and appearance.

There are studies that suggest that inorganic farming can produce more crop per acre and more meat per animal, and is, therefore, the better option for a planet bursting with overpopulation. (Some proponents extend that argument to genetically modified foods as well, but let’s stay away from that for the moment.)

However, there are also other studies that counter this argument by suggesting that the organic farms can end up being more efficient and productive in direct costs, yield and long-term sustainability.

Then, the big question is: if organic foods are no better nutritionally than inorganic and could be as productive for the farmer, are organic brands just skimming the gullible customer while the going is good?

We might expect certification and regulation to clear the air, but in many instances these leave out as many things as they include. Labelling is yet another concern. Countries where labelling is more stringently monitored allow logos such as “100% organic”, “organic” (more than 95% organic ingredients) and “made with organic ingredients” (over 70% organic ingredients). In other countries logos and where labelling may be less strictly monitored, the use of the term organic is far looser and even more confusing. What’s more, the usage of terms such as “Bio” or “Eco” can also mislead consumers into believing that there is something distinctly superior about the product they are about to buy when, in reality, it is often only a marketing gimmick.

Further, just because something is certified as organic does not mean it is a higher grade of product. Organic produce may end up having a shorter shelf-life, or may also be otherwise inferior to inorganic produce in the store. In fact, as the KRAV (Sweden) website states: “The KRAV logo is a clear signal that the product is organically produced but does not say anything about the quality. That must be guaranteed by the producer, i.e. yourself”. This is similar to saying that the fact that someone has a management certification from a certain institute means that he or she passed the tests of that institute in a particular year, but that does not automatically make him or her a good businessperson.

Countries and regions that have a poor record of environmental consciousness, poor transparency norms, are also not seen as the best source for organic produce even if it is apparently from a certified producer. In some cases, certification may be carried out second-hand and unverified, leading to instances such as the one in 2008 where the US retailer Whole Foods pulled out pesticides-laden “organic-certified” ginger that was shipped from China. The mixing of inorganic ingredients of uncertain origin, especially in blended products such as juices or snacks, can also make a mockery of the organic labelling.

Another visible concern today is the carbon footprint, and some people raise the question whether buying local (whether inorganic or organic) may be less environmentally damaging than importing produce from distant countries. In such instances, the evidence of lax certification, such as the Chinese case mentioned earlier, takes support away from the cause of organic imports.

Arguments have also been raised about whether the larger “organic” factory farms merely follow the letter of the law rather than the principles behind the organic movement? Small organic farmers allege that large organic-certified factory farms – especially those selling animal products – do not really follow the core principles of “natural” growth, and confine their animals in unnatural surroundings.

With all these arguments and counter-arguments flying about, some organic (or nearly organic) producers elect not to be certified, letting their customers vote with their wallets. Some of these smaller farmers may be driven by economic necessity since certification could be costly and cumbersome, while others may just find it more feasible to stick with a local sales strategy where the customers are able to physically see the organic nature of the farm.

It’s clear that all of these questions will take years to sort out – through debate, research, legislation, as well as social and commercial pressure. Meanwhile, most conscientious retailers and concerned consumers will need to do their own studies to educate themselves, and will need to examine each product for genuineness of the organic promise.

And, if you are not quite that savvy, the final message would be: “caveat emptor” (“let the buyer beware”).