admin

September 12, 2016

Suneera Tandon, Quartz

New Delhi, 12 September

2016

The Platonic ideal

The Platonic ideal

“Efficiency

is doing better what is already being done.” – Peter Drucker,

Innovation & Entrepreneurship: Practices and Principles

The practice

Research

firm Gartner defines supply chain as, “…the processes of creating and

fulfilling demands for goods and services. It encompasses a trading

partner community engaged in the common goal of satisfying end

customers.”

Sounds simple? But it hardly is. In fact, the

supply chain can be one of the most complex structures in a business,

piecing together design, development, sourcing, manufacturing, and

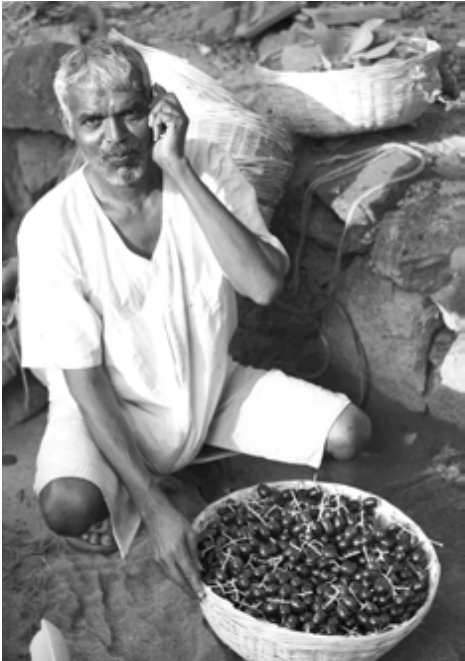

distribution. It gets even more complex when it relies on rural India,

which is scattered over 640,867 villages and are often hard to access.

Fabindia, a chain of retail stores, has spent close to five decades

scoping India’s hinterland to connect rural Indian artisans to urban

shoppers. Here’s how they did it.

Fabindia began its India

sojourn back in 1960 when John Bissell, who was first introduced to the

country in 1958 while on a two-year grant from the Ford Foundation,

decided to set up an export shop to sell home furnishings to overseas

customers. Bissell, whose work at the foundation involved advising

government-based craft organizations on handloom fabrics, spent a lot

of time traversing the length and breadth of the country.

In

1976, the export house diversified into retail through a small store

that sold leftovers from export orders in Delhi’s tony market of

Greater Kailash. It took another two decades for retail to became the

mainstay of the company’s business.

Fifty years later, Fabindia,

managed by John’s son William Bissell, is a widely recognized global

brand, known for handwoven and hand-made goods that connect some 55,000

artisans from the country to consumers worldwide. In the process, it

has achieved two broad goals: to market the handloom tradition of India

to the rest of the world and to provide sustained employment to

artisans in rural areas.

The chain sells everything from

handwoven saris, rugs, apparel, home d�cor, and organic food in its 220

stores across 83 cities in India, including eight stores in overseas

markets such as Dubai, Singapore, Malaysia etc. It also retails its

products online to 33 countries. For the fiscal year 2014-15, Fabindia

had a turnover of Rs1,148 crore (approximately $170 million).

But

behind the red and black Ikat-printed scarves, Kalamkari prints from

south India, and block-printed Bagru fabric from north India is an

extensive and complex supply chain that runs from villages across the

country, covering a third of India’s over 650 districts.

The

retailer has successfully taken its founder’s vision to enable social

change at the grassroots level while engaging in a profit-making

business for urban shoppers. It does this while building systems that

encourage not just fair remuneration to India’s rural artisans, but

also provides infrastructure, access to technology and systems, quality

guidelines, and timely payments to these craftsmen. Fabindia also

offers access to capital and raw materials to artisans working with the

retailer.

As William Bissell puts it in a Harvard Business

School case study: “It seems contradictory that we pursue both a social

goal and a profit, but I believe that is the only way to do it.”

Through most of the ’90s and early 2000s, Fabindia grew as a retail chain expanding modestly in the country’s top metros.

Since

the opening of the Indian economy through the economic reforms of 1991,

Fabindia’s interaction with artisans scattered across the country has

grown significantly (pdf). The complexity of the company’s supply chain

is far different from that of a regular manufacturer that works through

designated factories.

The company’s interaction with these

artisans is very localized since it works with them through multiple

associations. The retailer deals directly with individual artisans who

work out of their homes and also with clusters of crafters and rural

NGOs and organizations that have a crafts supply base.

In

addition, the company uses its 11 production hubs across the country,

which are basically aggregation points, to centralize orders and pair

up vendors with artisans. Each hub has a number of field offices

attached to it.

“The production hubs and field offices act as

nodal points for interaction with the artisans that constitute the

supply chain, which is one of the most unique in the world,” said

Prableen Sabhaney, head of communications and public affairs at

Fabindia Overseas.

While most artists have the skill and the

craft, they don’t have the acumen to decipher fashion trends for the

season. So Fabindia acts like a conduit between their crafts and the

market.

At Fabindia, a large proportion of products carry some

element of the handmade, which requires an ability to communicate with

artisans and institute quality control as most artisans work largely in

India’s hinterland. For instance, an 18-step process is required to

create a simple pattern in Bagru print, a traditional form of

block-printing using natural dyes perfected in the northern state of

Rajasthan.

And the company has spent years putting processes to

ensure newer collections reach the stores on time. Recently, the

product range has become more diversified as well.

As for

remuneration, Fabindia follows a bottom-up structure. It asks artists

what it costs them in terms of—time, energy, skills, and raw material

to hand-make a certain fabric or accessory and pays accordingly.

Analysts

who track the sector believe that Fabindia’s unique model sets it apart

from other domestic or export-focused handicraft companies purely

because of the sheer volume of artisans it works with.

“In

handicraft, there are several companies that have created substantial

export-led supply bases, which tap into craft both from the rural

artisans as well as those based in smaller urban centers,” Devangshu

Dutta, chief executive at consulting firm, Third Eyesight said.

“Among

these, Fabindia has certainly had the most visible success in terms of

size and brand profile domestically. Fabindia has achieved scale by

working through artists, intermediaries and supplier companies who have

acted as anchors in the rural communities,” said Dutta.

Sabhaney

offers that challenges span from co-creating contemporary products

while using traditional techniques to quality issues, since the

products are created in environments that are very different from where

they are finally used. The company also works hard to provide access to

raw material and capital across many hard-to-access areas—and doing all

of this at scale.

“The ability to do this and not lose anything

in translation has been and will continue to be Fabindia’s strength,”

added Sabhaney.

The takeaways

As

the market evolves with e-commerce and the entry of foreign brands,

which has altered consumer preferences and style-cycles, Fabindia knows

it needs to quicken its response to these changes.

Not all of

the innovations the company has tested remain. In a unique ownership

structure created by Bissell, Fabindia set up supplier regional

communities (SRCs), which were community owned companies, self-managed

by a group of artisans, weavers and craft workers in a particular

geography back in 2007. According to a case study by INSEAD (pdf),

these SRC’s “offered artisans joint ownership of resources and access

to common facilities. It also trained artisans and developed new

handicrafts. The SRC allowed Fabindia to consolidate supply capacity

instead of dealing with single-loom weaver units, and to implement a

standard system for production and delivery control.”

The 2010

book, The Fabric of Our Lives reveals how production worked under the

SRC model. A number of dedicated designers and sourcing officers worked

closely with rural artists giving them design inputs in tandem with the

latest trends in the market and order quantities through dedicated

distribution centers in key villages. These designers worked with the

weaver to develop samples. They were then shown by the designers that

refer it to a product selection committee. The fabric was then approved

and the cost price finalized. The quantity of fabric to be produced the

first time was pre-determined by software based on a minimum stock

requirement ratio and an order is given to the weaver to make the

product. The weaver produced the requisite amount of fabric in a month

and brought it into the distribution centers.

But the SRC model has now been diluted as the company looks more innovative ways to engage rural artisans.

In

the company’s next vision plan, it is focusing more on cluster

development that will basically help bring artisans up to speed with

the processes and market trends.

“There are plans for a greater focus on the handloom and hand-craft sector,” Sabhaney said.

“There

is a much bigger focus on the social aspect, there are going to be

significant investments in developing clusters and bringing them up to

what is required around the country,” she added.

(Published in Quartz)

admin

October 27, 2009

![]() 27/10/2009

27/10/2009

![]()

Mr Bruce E Bergstrom VP, Vendor Compliance,Li & Fung |

|

"Sustainability is a great concept like liberty. We are in a world with many problems and sustainability is the solution. This is the answer given by Bruce Bergstrom, VP vendor compliance of sourcing giant Li & Fung, who tackled the difficult question of What is Sustainable Fashion? at the first-ever Sustainable Fashion Forum held earlier this month. |

Session One:

Moderating the first session, Michael Lavergne, director-Asia, Worldwide Responsible Accredited Production (WRAP), posed to the panel "What does it really mean to be sustainable and what is best practice?"

Adding to his big-picture view of sustainable fashion, Mr. Bergstrom says economics play a strong role in the current approaches to sustainability, while solutions taken from social and environmental perspectives are sure to come.

"Sustainability is now a retailer and brand-driven initiative, but we need to convince the manufacturers to see the benefits of sustainable operation starting with raw materials,’" said Hong Lee, manager of Asia Pacific, Control Union.

But when widespread consumerism drives disposable fashion, is there really a place for sustainable fashion? The answer is yes, according to Janvier Serrano, creative director and founder of The 091/091’s Eco Couture brand, which features bags made from recycled scraps.

|

|

|

"Although it is difficult to achieve sustainability right now and it is a big challenge, we must do it. We must be open, we must be proactive. We must educate the consumers to go for quality and not quantity," advised Serrano.

Agreed Amy Small, Creative Director at Green2greener, a b2b trade platform for eco-fashion: "Sustainability is a continuous goal, it is to put back the same amount as what you take out". In her opinion, small companies, successful in sustainable production, can inspire big companies to follow.

"Fashion is not only in clothing but it is a lifestyle and attitude of life. We have to be vigilant on sustainability in day to day operation and living. It is important to impress upon the students of today the concept of sustainable living so that it can be passed down to the next generations", said Mary Yan Yan Chan, director of Style Central Ltd, the exclusive agent of Perclers Paris.

Taking questions and opinions from the floor, the panel and audience agreed that a paradigm shift is needed for the fashion industry to tackle sustainability effectively. There is a need to drive innovation. Governments can also play a part, through education and green policies.

Session Two:

Devangshu Dutta, chief executive of Third Eyesight led the 2nd session panelists to discuss "Is Sustainable Fashion Profitable?" He commented that sustainability is not viable in the long term without financial returns and a good business sense.

"Sustainable fashion can be profitable because shoppers today are looking for something more meaningful. Consumers are accepting the concept of reuse and recycle in a creative way", said Olivier Grammont, founder of eco fashion brand Francs-Bourgeois. He described how his company uses second hand materials for handbags and the finished products are selling well in boutiques.

Concurred James Ockenden, director of publishing house Media Karma which specializes in the environmental technology, energy and finance industries. Ockenden citied the case of an olive oil company that used olive pits to generate energy for the plant. The company has now expanded to processing palm oil waste to produce a power supply to 400 households. Ockenden strongly believes that green legislation is the way forward but subsidy for new technology is necessary. He proposed adding ‘government’ to the three pillars of sustainability, that being economics, environment and social.

Session 2 Panel: Mr Olivier Grammont, Mr James Ockenden, Ms Cassandra Postema, Ms Dong Shing Chiu |

|

|

Meanwhile Carolina Rubiasih, VP sourcing & product development of the SAK questioned whether today’s consumers, who want value-for-money products, are indeed ready to for sustainable options that generally incur greater costs. The younger generation, however, is adopting healthier lifestyles that will likely encompass sustainable fashion. As time goes by, sustainability will be the norm and a way of life and perspective.

Offering ideas on how to be profitable with sustainable products, Ms Rubiasih advises to produce only what you can sell, improve on the design to reduce wastage, use less packaging layers, increase efficiency in logistics and study the tariff code to tap lower tariff categories with minor adjustments to the material & design. Her privately owned company took such steps and yielded good results, outperforming their previous year’s revenue.

Echoing Rubiasih’s emphasis on the importance of design, Cassandra Postema, director of fair trade fashion brand Dialog said "As designers, we have to design a product that can sell and sustain and compete with the regular products. It took People Tree, an eco-friendly company, 10 years to breakeven."

Some audience members felt that sustainability must be price neutral if not cheaper to sell to consumers and noted that supply chain efficiently is critical to profitability, while innovation and good management can bring costs down. It was also suggested that designers should place attention towards engineering so as to produce more efficiency.

Session Three:

In Session 3 Mr Ockenden facilitated the panel to probe into the question of "Who Wants Sustainable Fashion?" People buy fashion for various reasons, but experts often agree is linked to an emotional element. Companies can encourage sustainable fashion purchases by strengthening its ‘feel-good’ factor.

Sustainable fashion is in-demand among fashion brands, but under the financially low-risk terms of cost and time-efficient production, says Mr. Lavergne. NGOs are nudging the concept of sustainability onto the brands and retailers and the social climate is ripe for them to take such a stand.

Meanwhile Mr. Dutta says that general perception of fast fashion is quite wrong; it is actually not about throw away clothing but a management system that can improve the efficiency of the supply chain. Fashion is by nature not a sustainable concept but how can we make it sustainable? He hopes that in 10-20 years time we will truly have sustainable fashion.

Moderator: Mr James Ockenden, Direct, Media Karma |

|

|

Summary:

The panelists recognise that sustainable business is still in its infancy, and urge the brands, retailers, buyers and suppliers to take small steps towards sustainability. There is no one answer to the complex and multi-faceted issue and finding solutions will require a collaborative effort. Improvements in education, innovation, technology and government policies will make sustainable fashion possible – and profitable.

admin

September 22, 2008

Devangshu Dutta

In a departure from popular retail philosophy, Devangshu Dutta calls for a new model of food supply based on multiplicity and diversity. Modern retail must, he says, take into account the changing environment and be sensitive to evolving consumer preferences and to the failures and obsolescence of traditional mass retail models adopted by western developed markets.

Devangshu Dutta is chief executive of Third Eyesight, a management consulting firm focused on consumer products and retail, whose clients include brand leaders and some of the largest companies in their respective markets.

Food price inflation it is still hogging the headlines. It is, after all, an emotive topic. We are terribly concerned not just as food and grocery professionals, but also as consumers and the general public. After all, food and grocery typically account for half of our monthly spend, give or take a few percentage points.

Most students of management, economics, and human behaviour are aware of Abraham Maslow’s classification of human needs into a hierarchy construct. Other economists and psychologists prefer to use other models. Whichever model you consider, the need to eat and the need for security are invariably at the bottom or base level which must be fulfilled the earliest.

The interesting fact is that well after you would imagine these basic concerns have been taken care of, they are actually never far from the surface. This is true not just of the poorest of the poor, but of the wealthy and the well-off as well—whether individuals, communities, or nations.

Increasingly, the agricultural supply chain is dependent on non-renewable petroleum and its products, rather than by the natural energy of the sun being converted into food by the plants.

Is it any wonder that “food security”—the combination of these two—is such a charged subject, especially in these times?

However, a significant set of questions is not really touched in the question of costs and in the question about the continuing security of food supplies: how the food supply chain is structured, how it is driving consumption, what impact that might have on food prices and several broader cost implications.

INDUSTRIALISING AGRICULTURE—FARMING PETROLEUM

Thousands of years ago, when hunter-gatherer human beings stumbled upon agriculture, it was a breakthrough similar to the discovery of controlled fire. Hunter-gatherers were dependent on the natural availability of food, while agriculture created the opportunity to have some control over food supplies and reduce the natural feast-famine cycle. Thereafter, farming, processing and storage techniques kept evolving incrementally to ensure that more food could be produced for each unit of land and effort, and stored for longer – all moving towards ensuring “food security”. This led to the age of empire-building, where monarchs grew their wealth (essentially food territory) with the help of military- imperial complexes, and the greater wealth in turn supported the military-imperial complex.

This remained the trend for a few thousand years, until the age of industrialisation and the age of petroleum. Through the industrialisation and the world wars, the military- imperial complex gave way to a military-industrial complex, which essentially became the military-industrial-petroleum- agricultural complex. Suddenly, there were not just machines to plant, reap, thresh, sort, clean and process, but also petroleum-based and synthetic substances to dramatically increase output and to keep the produce fresher for longer.

As farms industrialised, the parameters that began to be applied were the same as in any factory—how to produce more while spending less—and every year the target was to grow more for less. Underlying this was the principle of “efficiency from larger scale”. The same philosophy played out further down in the supply chain – from processing aimed at extending the shelf-life of the product as it was (chilling, cleaning, sorting) to processing and packing in order to change the nature of the product itself and gain additional value (such as turning tomatoes into puree and potatoes into chips).

Standardisation became a vital link in industrialisation — if you can standardise produce, you can cut down human handling — while you may lose product variety (including flavour and colour) you gain through lower production costs. By reducing unpredictability, you can also concentrate on building the scale of business, because it becomes more repetitive.

The interesting side-effect of this is that, gradually, we are converting ourselves (and people in many industrialised economies already have) into petroleum-burning machines rather than those running on solar energy, because increasingly, the agricultural supply chain is dependent on non-renewable petroleum and its products, rather than by the natural energy of the sun being converted into food by the plants.

The important thing to keep in mind is that, in this switch- over, energy efficiency is actually going down rather than up

Energy efficiency is actually going down rather than up – we are using more calories of fuel source to produce each calorie of food energy.

—we are using more calories of fuel source to produce each calorie of food energy.

So it is worth asking the question: can lower costs actually be costing us more?

THE DEMAND-SIDE STORY

The growth of industrial agriculture has not happened alone, but has been accompanied by the growth of modern or “organised” retail.

On the one hand, large retailers such as Wal-Mart, Carrefour, Tesco, Metro and others, have been widely credited for achieving cost-efficiencies from scale, and then passing on these efficiencies to the consumer in the form of lower prices (and, apparently, higher standards of living). That is a good thing and definitely of benefit to the population at large, especially in inflationary times such as these. Surely, it is good to push for lower costs rather than keeping prices high as a result of inefficient sourcing, wasteful and expensive handling, and non-value-adding costs in the supply chain.

On the other hand, these organisations are driven to standardise their own product offerings, reduce the number of supplier touch-points and increase the volume per supply source.

There is not just a reduction in diversity of suppliers, but also a reduction in the number of product variants. (I’m not referring to the number of “types” of potato chips or packaged meals, but to the actual core food product—the natural species or sub-species that are the basic source.) Of course, agriculture itself is a process of consciously selecting and encouraging species that are more useful to us humans, but industrial

Lower costs can be delivered by reducing the variation of products

Higher sales can come from either having consumers buy more of the same product (which in food does tend to taper off after a while), or by turning the basic product into a “value-added” product (e.g. potatoes into wafers, mash, fries; corn into syrup and food additives, and so on).

THE NEED FOR A DIFFERENT MODEL

We don’t have to look too far into the future to realise that this is not a sustainable model. (Or, as someone pithily said: “Only fools and economists believe in infinitely compounding growth.”) So far, this model has impacted less than a fifth of the world’s human population, but now the growth markets of choice for industrial agriculture companies are China and India. If these two countries move through the exactly same path as have the western economies in terms of agriculture and food processing, given the population base itself the impact may be 5-7 times (or more) on the demand for petroleum as well as the fall-out on the ecosystem.

You may ask: why should retailers and their suppliers worry about this?

Firstly, pure cost considerations – clearly, the costs of petroleum are ranging at the highest levels ever, and explosive demand through industrialised agriculture will only serve to push them up. How far can you push the food bill every month, before people start buying less? What impact would that have on large retail supply chains and farmers whose processes are increasingly built around products of industrial agriculture?

Secondly, what consumers are already beginning to express in western markets will possibly happen in India in the next few years as well: concern about where and how the product has been produced, what has been the fall-out on the environment and on the overall health of people involved with that supply chain as well as the health of consumers. Carbon footprint, food miles and locavores (people who only consume food that is produced within 100 miles of where they live) are terms that companies are increasingly becoming familiar with.

agriculture takes it to a completely different level. Carbon footprint, food miles

The industrial-agricultural-retail economic model can be paraphrased as follows:

Businesses (especially those that are publicly held) need to show growth in profits each year

Growth in profits can come from higher sales at the same cost base or lower costs

Carbon footprint, food miles and locavores (people who only consume food that is produced within 100 miles of where they live) are terms that companies are increasingly becoming familiar with

And an alternative set of questions is also being raised. Is it ok to burn non-sustainable fossil fuel if you get “carbon credits” by planting trees somewhere else—have all the carbon costs been accounted for from the start to the finish of the production process? Is it better to reduce the food miles and have food produced locally in a high-cost economy’s industrial agricultural model, or to have naturally grown foods from a more primitive farm in Africa or Asia where the environmental impact is only the “carbon debit” of the air-freight. And, even if the produce is carbon-friendly, what about the nitrogen footprint (from the fixation of nitrogen into fertilisers) and the methane footprint (from large scale animal farming)?

THE POWER OF THE SMALL AND THE MANY

And finally the question of maintaining diversity must be top- of-mind. For all its so-called inefficiency, diversity is actually a great shock-absorber. Imagine a bean bag or a piece of foam — what gives them their cushioning ability is the space and air between the little balls, or the material. Now imagine a cropland that is attacked by a pest—if there is diversity in the plant population, there is a good chance that certain varieties will survive even if others don’t; unlike a cropland with limited variety which may be totally wiped out (and possibly the farmer with it). Further imagine a supply chain that has multiple suppliers with the same or similar product versus one where the supply base is highly concentrated. Which ecosystem do you think will survive better during times of trouble, even if some of the suppliers—a part of the ecosystem—do not? (One doesn’t have to think too far: the example of the former Soviet Union with its mega manufacturing plants supplying the whole country are a case in point.)

To really find long-term solutions for food security issues, retailers, suppliers, economists and governments need to acknowledge that sustainable safety lies in numbers and diversity. A dispersed economic system with a lot of variety has resilience built in. And the solutions may actually be very close at hand, in the updating of traditional techniques.

It is high time to start figuring out how India (and China) can take the lead in creating an alternative and more sustainable model for food security for large populations, rather than blindly push development models borrowed from the 19th and 20th century western economic history.

Source: FLY ON THE WALL

Send download link to:

Moderator: Mr Michael Lavergne

Moderator: Mr Michael Lavergne Session 1 Panel: Mr Javier Serrano, Ms Mary Yan Yan Chan, Mr Bruce E Bergstrom, Mr Hong Lee

Session 1 Panel: Mr Javier Serrano, Ms Mary Yan Yan Chan, Mr Bruce E Bergstrom, Mr Hong Lee  Moderator: Mr Devangshu Dutta

Moderator: Mr Devangshu Dutta  Overview of the forum

Overview of the forum