admin

February 18, 2013

![]() Pia

Heikkila, International Bar Association

Pia

Heikkila, International Bar Association

![]() Mumbai,

February 18, 2013

Mumbai,

February 18, 2013

Multinational

corporations such as Vodafone, Shell and Nokia are rarely out

of the business pages as the Indian tax officials seemingly never-ending

chasing of unpaid taxes gives daily fodder to the Indian press.

Multinational

corporations such as Vodafone, Shell and Nokia are rarely out

of the business pages as the Indian tax officials seemingly never-ending

chasing of unpaid taxes gives daily fodder to the Indian press.

But, while it’s tempting to lump all three companies’ cases together under the headline ‘unpaid taxes’, each is, in fact, very different.

Take Shell, the Anglo-Dutch fuel giant. Indian tax officials are claiming unpaid taxes of over £1bn over an equity infusion undertaken four years ago worth £120m. The tax authorities are claiming that Shell underpriced its shares and as a result paid less tax on the internal shares transaction.

Shell India has described the demands as ‘absurd’ and says it will challenge the notion that alleged tax evasion is done by underpricing share transfer between member firms. ‘We do need the right signal that India is going to be a stable fiscal, legal, tax regime. We are not going to have surprises along the way,’ said Yasmine Hilton, the India Head of Royal Dutch Shell in a report by Firstpost.

The Finnish handset maker, Nokia, however, has come under fire for an entirely different reason. Nokia, the Indian tax department alleged, has violated the country’s transfer pricing rules. According to unanimous sources in the local media, Nokia’s case is related to tax payments the company made for supplying software from its parent company in Finland for devices produced in India.

Nokia India objected to officials entering its factory in Chennai, one of its biggest facilities and described the incident as ‘excessive, unacceptable and inconsistent with Indian standards of fair play and governance’.

Vodafone, on the other hand – the world’s largest mobile operator – is fighting a case over paying taxes of nearly £2bn on its 2007 majority stake buy in a local telecom company from Hutchinson. The company is also facing a charge from Indian authorities for underpricing an issue of shares of its Indian unit to a Mauritius-based group company by about INR 13bn (£200m). But Vodafone is fighting back and denies the charges.

These cases have one thing in common: the tax is being collected on transactions retrospectively. It seems, the experts say that India has gone on a hunt for unpaid taxes to boost its coffers. ‘With the slowdown of the global economy – and, more so, the Indian economy – tax collections in the country have been below estimates. Further, with rising concerns over the fiscal deficit scenario, every attempt is being made by the tax authorities to shore up tax collections to bridge the gap,’ said Girish Vanvari Partner and Co-Head of Tax at KPMG in Mumbai.

It could look like a witch hunt for foreign of multinationals operating in India. But, says Devangshu Dutta, CEO of Third Eyesight, a specialist management consultancy firm, ‘there is valid reasoning behind the government’s stand that for value gained on assets that are primarily in India, tax should be paid in India, and should not be avoided/evaded purely through offshore corporate structures that have no inherent value of their own.’

The lines between what is tax evasion and what is tax planning appear increasingly blurred today. ‘Each country should have their own rules but ultimately the idea is that you should pay appropriate taxes within the framework of law in that country,’ said Vanvari. ‘There is global trend by each country to increase their tax bases by taxing the superrich, transfer pricing adjustments, off shoring taxes and so on. Transitioning into these new concepts especially for years gone by is leading to debates, chaos and confusion.’

But continuing tax debacles can seriously tarnish India’s image and alienate foreign investors and companies alike. ‘Retrospective changes such as this affect the image of India as an investment destination not only in the eyes of foreign investors, but domestic investors as well,’ said Dutta.

Business leaders say there is much more to be gained from creating a policy environment that allows entrepreneurial and social energy to be unleashed – rather than be subjected to a constant barrage of rules and regulations.

Sadly, however, these cases and other tax-related litigation are not going to disappear any time soon experts warn.

‘However good or bad the case is, legal battles in India usually tend to be long. Once a tax demand is raised, a portion of the same needs to be deposited whilst litigation is ongoing,’ said Vanvari.

Ultimately India is still trying to get to grips with its own speed of change. But the government should be wary of sending out the message that it can bend the law at will. ‘In that environment, business and non-businesses that can contribute to positive changes and growth feel stifled and don’t do enough to achieve their own fullest potential, or otherwise they just move to another jurisdiction where they can,’ Dutta noted.

(This article appeared on the website of the

International Bar Association on February 18, 2013.)

Devangshu Dutta

February 16, 2013

About six years ago, Kishore Biyani of the Future Group and I were discussing a presentation I had delivered at CII’s National Retail Summit, during which I had mentioned “Purushartha”. This millennia-old living philosophy takes a balanced view of life. Aspects related to consumption are two of its major components including Artha (wealth, commerce) and Kama (sensory pleasure). Dharma (righteousness in society and individual life) and Moksha (liberation) are the other two. My point was that most “traditionalists” and certainly policy-makers in the country have tended to view the retail sector negatively or dismissively.

Of course, at that time most businesses themselves hardly demonstrated any sense of balance, let alone any connection with the reality of India, whether in terms of the consumer’s needs, or in terms of the operating environment in the country. By and large the theme was: push explosive growth, margins be damned; promote “westernised” consumption aspirations, regardless of capability to fulfil those aspirations. Conversely, the four years after the global financial crisis in 2008 have been possibly the worst that the retail sector has faced in recent decades, whether in terms of total losses or the quantum of lost growth opportunity, and business sentiment has swung to the other extreme.

On its part the government has not done much to encourage the sector. After several policy flip-flops, approving investment proposals of some high-profile global brands is a positive signal to the outside world, but none of them so far have unlocked or grown the value of Indian retail businesses in any significant way. There is no doubt that foreign brands and retailers can and should be an integral part of India’s developing retail landscape, but they cannot be the prime drivers of the retail business in India or the saviours of its supply chain. That vision and energy needs to come from within, and the resultant growth will benefit all – Indian and international companies, consumers and the government.

From the ancient treatise Arthashastra, Professor Thomas Trautman quotes the concept of concept of “shad-bhaag” (the state having one-sixth share) as “entrepreneurial” because it has a sense of mutual interest, promoting production and the growth of everyone’s share. This spirit of co-ownership and entrepreneurial participation is largely missing in today’s governance. Direct and indirect taxation remains a complex net for all but the savviest evaders, not to mention all the other regulation and approvals that each business – large or small – needs to comply with.

Somehow the mandarins don’t seem to see that the retail business is a platform for the multi-fold growth of new enterprise, that it is a vehicle for urban renewal, and that it can help enormously in channelling the economy into visible taxable revenues. It also seems to escape them that the biggest drivers for this growth and change will typically be small entrepreneurial businesses, who themselves can only thrive in a simpler and non-adversarial regulatory environment.

The wishlist is not large, but needs some bold steps: enact policies that free up unproductive real estate to reduce costs, reduce regulatory hurdles, remove tax traps, reduce import duties. For instance, one estimate for illegal imports in watches is 75 per cent, where the beneficiaries are the smugglers and those who oil the wheels for them, not the consumer, not the brands or retailers, not the revenue department.

It is an important budget year politically due to impending elections but also economically due to the dismal GDP growth. The animal spirits that the Prime Minister has referred to in the recent past are more in the nature of a “bheegi billi” right now rather than a roaring tiger. The caged golden bird will not lay any golden eggs. Will the Finance Minister choose to crack the whip this year, or cut the chains? We watch with bated breath.

(An edited version of this piece was published as in Daily News & Analysis – DNA on 19 February 2012, under the title “Foreign brands can’t be prime drivers of retail”.)

admin

February 16, 2013

Taneesha Kulshrestha, Outlook Business

New Delhi, February 16, 2013

When

the first Debenhams outlet opened in India in October 2007, the

British retailer was more than optimistic about the road ahead.

Never mind that the store — opened in partnership with Planet

Retail at Gurgaon’s Ambience Mall — was nearly 18 months

behind schedule. Debenhams’ international director, Francis

Mcauley, declared that he would be disappointed if the company

did not have 30 stores in India over the next 10 years, by when

the Indian operations could be the retailer’s biggest outside

the UK, he predicted. Now, six years later, those forecasts are

nowhere close to realisation — the department store has just

three stores across India, two in the national capital region

and one in Mumbai. The brand also has a new partner in Arvind

Lifestyle Brands, which bought out Planet Retail’s interest

in November 2012. Expectations are rising again, although they

are considerably more muted than the last time. “I am confident

that within the next five years, we will have around eight Debenhams

stores in the five biggest cities,” says a company spokesperson.

When

the first Debenhams outlet opened in India in October 2007, the

British retailer was more than optimistic about the road ahead.

Never mind that the store — opened in partnership with Planet

Retail at Gurgaon’s Ambience Mall — was nearly 18 months

behind schedule. Debenhams’ international director, Francis

Mcauley, declared that he would be disappointed if the company

did not have 30 stores in India over the next 10 years, by when

the Indian operations could be the retailer’s biggest outside

the UK, he predicted. Now, six years later, those forecasts are

nowhere close to realisation — the department store has just

three stores across India, two in the national capital region

and one in Mumbai. The brand also has a new partner in Arvind

Lifestyle Brands, which bought out Planet Retail’s interest

in November 2012. Expectations are rising again, although they

are considerably more muted than the last time. “I am confident

that within the next five years, we will have around eight Debenhams

stores in the five biggest cities,” says a company spokesperson.

At the other end of the spectrum, several high-end brands, too, have switched partners or changed business models. In 2009, the Murjanis parted ways with Jimmy Choo and Bottega Veneta, both of which moved to Genesis Colors. Aigner, meanwhile, dumped Genesis Colors in 2010, while last year, Versace and Corneliani ended their franchise agreements with Delhi’s Blues Clothing. Again last year, Giorgio Armani quit its joint venture (JV) with DLF Brands and moved to Genesis Colors. DLF terms the termination a “strategic” one. “The luxury business cannot be scaled up in India as fast as we previously believed. So, for now, we will focus on the premium segment of the fashion and retail business,” says DLF Brands CEO Dipak Agarwal, adding that Armani, too, has scaled down its expectations. “The move to end a JV and enter a franchisee model shows that the brand has narrowed its business interests in India,” he adds.

Despite the promise of a big consumer market — a growing middle class with rising disposable incomes, growing awareness of international brands and trends and an increasing willingness to spend on them — many international fashion brands have been forced to rethink their India ambitions. Research by Delhi-based retail consultancy Third Eyesight shows that since 2006-07, some 50-odd brands, including Next, Guess, Gas, Etam, Rifle, Morgan, Saville Row, Lerros, Corneliani and S.Olivers, among many others, have either exited India or have restructured their operations in the country. And the trend continued in 2012, despite the government allowing 100% foreign ownership for single-brand retail outfits in January last year. Brands such as Versace and Alfred Dunhill are said to be eyeing the exit sign currently. How did so many brands get their India strategy so wrong?

Misreading the market

Since 2005, there has been a four-fold increase in the number of international fashion brands entering the Indian market, triggered by the government decision to allow 51% FDI in single-brand retail in January 2006. It didn’t hurt, either, that import duties on apparel came down sharply from about 100% in the 1990s to 35% currently. The result: the organised fashion retail market more than doubled from about Rs 1,000 crore in 2005 to Rs 2,500 crore currently and is expected to touch Rs 6,000 crore by 2015, according to Technopak.

At the same time, for many brands, finding the right business model and understanding the Indian consumer has been an uphill task. “Some find India too complex a market. Besides, partners also tend to have differences when it comes to dealing with the marketplace, the waiting time and investments required to make things work,” points out Devangshu Dutta, CEO, Third Eyesight.

Ankur Bisen, VP, retail and consumer products, Technopak, offers

another reason. “The mistake many people make is they think

of India as one big market, when it is actually many markets in

one.” For instance, Delhi starts buying winter clothing when

it is still hot in Chennai. And people in the north have different

colour and style preferences than those in South India. “Add

to that poor retail infrastructure — the lack of trained

manpower, high rentals etc. — and you know why brands have

been finding it tough.”

Consider Marks & Spencer (M&S). The British retailer entered

India in 2000 with a franchisee agreement with Planet Retail,

positioning itself as a luxury brand although it was just a high-street

label back in the UK. All merchandise was imported from the UK

and, not surprisingly, was substantially overpriced. In 2009,

M&S switched to an equal JV with Reliance Brands and has started

sourcing and manufacturing 60% of its merchandise in India and

South Asia, which has brought down its prices by almost 20-30%.

The store has also repositioned itself as a mid-market retailer

and is making clothes more suited to Indian preferences —

longer lengths, higher necklines and more colour options. “We

have a better understanding of local taste and style now and our

range has been tailored to suit these,” says Venu Nair, MD,

Marks & Spencer India.

Similarly, in October 2012, Esprit broke its seven-year licensing and distribution deal with Madura Fashion & Lifestyle after reportedly suffering losses of Rs 20-25 crore every year. German brand Lerros, which had a JV with House of Pearl, too, met a similar fate in 2008 and switched to Numero Uno instead.

Like M&S, these brands also misread the market completely, charging way too much and trying to pass themselves off as premium offerings when their international positioning was more middle market. British brand Next, too, signed up with Arvind Lifestyle recently, breaking a seven-year relationship with Planet Retail.

As it is, most exits or change of Indian partner have some common threads — increasing cost pressures with aggressive expansion of the brands at expensive locations; high pricing due to costly merchandise imports and little or no local sourcing; and the inability to position and price a brand correctly and communicate it to the target customer group.

That’s what happened with Benetton. The iconic Italian fashion

brand was one of the earliest entrants into India, with a 50:50

JV with the DCM group in 1991. In 2004, it split with DCM and

began operating as a wholly-owned subsidiary. But by then, Benetton

was already seen as a T-shirt company that was always on sale

— the company advertised heavily during its two annual sales

but did virtually nothing the rest of the year; it didn’t

help that the ads showed products that weren’t available

in India. The Italian parent brought in a new team, focused on

increasing local sourcing and made the product offering more up

to date. “Earlier, there was a view in the company that the

Indian consumer did not have the same sensibilities for fashion

as international customers. That was a mistake,” concedes

Sanjeev Mohanty, Benetton’s MD in India. Now, the Indian

stores are on par with stores in London, Paris and Milan, with

the same clothes and visual merchandise effects, although all

manufacturing is done locally. There’s also been a change

in how Benetton sells in India: the company is now a pure wholesale

player in India, catering to over 500 stores across 110 cities,

with reported sales upwards of Rs 650 crore. “We own no stores

and have instead appointed master franchisees that distribute

our products,” says Mohanty. “We do have a complete

grip on design, marketing and guidelines for selling our products,

though.”

The Local edge

Where Benetton and M&S have realised the need to source locally, many brands falter by insisting on importing merchandise. “This alone can push up costs by 30-35%,” says Third Eyesight’s Dutta. If the retailer can’t pass on the increased cost to the customer, margins are immediately hit. Several international brands have faced this problem and are now increasing their local sourcing or giving licences to Indian partners to manufacture on their behalf. At Lacoste, for instance, long-time partner Sports & Leisure Apparel has the licence to manufacture and retail the French company’s apparel in India. “Manufacturing in India has helped in cutting costs, allowing us to maintain a better bottomline. We are also able to get new designs and clothes to the market faster,” says Rajesh Jain, CEO, Lacoste India.

It’s not only about cost; importing apparel also means limited scope to adapt sizes and styles. “India has very local aesthetics and some brands don’t allow for that. They try to plug and play and that’s where the trouble starts,” says Max India executive director Vasanth Kumar. The Dubai-based Landmark Group’s value clothing brand has a design team of 20 people working in India to adapt Max’s global lines to local sensibilities. That hasn’t saved it from mistakes, though: over the past six years, the chain has grown to over 70 stores but has also closed outlets at places like Jalgaon and Nanded. “It takes time to understand the different tastes and needs of consumers across the country,” points out Kumar.

Trouble is, foreign brands can be rather impatient and their

haste to expand can backfire. High-cost rentals were part of the

reason Gas exited India the first time and it’s also a key

reason why S.Oliver is yet to make a profit here. The German brand

entered India in 2007 through a joint venture with Orient Craft

and opened large stores — 5,500 sq ft on average — in

prime locations; the brand reportedly signed a long lease for

a 7,000 sq ft store in Delhi’s Select Citywalk mall for Rs

3 crore. In May 2012, Orient Craft sold its 49% holding in the

JV to Design Pod India. The new strategy includes halving the

size of outlets to 1,200-2,400 sq ft. While clothes will still

be imported, they will be procured directly from hubs like China,

Bangladesh and Hong Kong instead of being routed through Germany.

Prices are also being slashed by almost 30-40% to bring the brand

in line with rivals like Zara, Benetton and Mango.

Equally dissatisfied

It’s not only the foreign brands that are unhappy with how their Indian operations are being run. In May 2009, at a luxury conference in Delhi, Mohan Murjani, chairman, Murjani Group, took everyone by surprise when he declared the termination of the Murjani Group’s JVs with brands such as Gucci and Jimmy Choo, citing unfavourable terms of trade. Most foreign brands did not partner the Indian owner for losses, but wanted all profits to accrue to them in the form of royalty and profit share. “Sadly, brand owners have pursued one-sided and imbalanced agreements, which have now started to unravel,” Murjani noted at the conference.

But some of that problem also stems from the fact that Indian partners oversold the India potential to their own peril. That’s the reason DLF Brands snapped its four-year-old ties with Ferragamo and Armani in 2012. “We found that we could only open five or six stores for these brands and there isn’t much potential for the luxury market over the next five or six years. So, we have decided to focus on mid-market and premium brands such as Mothercare, Alcott and Boggi,” says Agarwal. Incidentally, Mothercare is another foreign brand that’s switched partners in India — the British chain came into India through a franchisee agreement with Shoppers Stop but changed to a 30:70 JV with DLF in 2009, which has since been expanded to a 51:49 arrangement in favour of Mothercare.

There’s also trouble when the Indian partner underestimates just how deep its pockets need to be to develop a fashion brand. Blues Clothing was started by Dinesh Sehgal in the mid-1990s to sell suiting material from premium international brands such as Cadini and Canali at the family’s stores in Delhi’s posh South Extension. Since 2005, the company signed on a number of brands such as Corneliani, John Smedley and Versace but has suffered heavy losses. While Versace has moved on to a partnership with Majgenta Fashions, Corneliani has formed a JV with OSL India, which also holds dealerships of BMW and Volkswagen.

Unfortunately, the list of failed marriages is a long one when it comes to the luxury business. But the good news is that, despite the stumbling blocks, foreign brands are a long way from breaking ties with the Indian market. M&S plans to open 10 more stores by Summer 2013, its biggest expansion in a single year after having been in the country for over a decade. India is among the four biggest emerging markets for Lacoste globally — the Indian operations grew 33% last fiscal and Jain is confident of maintaining the pace this year as well. Benetton, Levi’s and Max have stuck on over the years and now have turnovers in excess of Rs 650-800 crore. Market research firm Booz & Co expects organised apparel retail — which accounted for 17% of the $36 billion market in 2010 — to grow to 25% of the market by 2015 as the apparel retail industry, too, continues to grow by 5-10% in the same period. That means an opportunity of nearly $10 billion awaits apparel industry players who hang around for the next few years. Surely that’s reason enough to cultivate a little patience and tolerance.

admin

February 14, 2013

Mayu Saini, WWD

New Delhi, February 14, 2013

The

Indian government on Wednesday approved foreign direct investment,

or FDI, in single-brand retail by four retailers – French brands

Promod, Decathlon and Le Creuset and U.S. firm Fossil Inc.

The

Indian government on Wednesday approved foreign direct investment,

or FDI, in single-brand retail by four retailers – French brands

Promod, Decathlon and Le Creuset and U.S. firm Fossil Inc.

The four companies will invest a total of 7.5 billion rupees, or about $140 million, in India, according to an official of the Foreign Investment Promotion Board.

According to officials, Fossil Inc. and Decathlon, both of which already are present in India, applied for 100 percent FDI. Promod, which first entered India with a franchise agreement that was changed to a joint venture with Indian company Major Brands in 2012, continues to look at a joint venture model. Promod is in nine locations at this time, including New Delhi, Mumbai, Pune and Bangalore.

Decathlon, the giant sports retailer, will bring in foreign equity of 7 billion rupees, or $130 million, officials said. Promod and Fossil are smaller, at 300 million rupees, or $6.1 million, and 220 million rupees, or $4.1 million, respectively.

"The move to invest directly in the Indian market for all three brands is a demonstration of longer-term commitment and confidence," said Devangshu Dutta, chief executive of Third Eyesight, a specialist consulting firm focused on the consumer products and retail sector. "For these and other brands who have joint ventures or subsidiaries in India, the engagement goes beyond the financial investment, it also needs a commitment of senior management time and attention."

He said that Promod’s move from a distribution or franchise arrangement to a joint venture has "been in the pipeline for a while. Fossil has also been distributing through various channels, and a fully owned retail business will enable them to take direct control of how the brand interfaces with the discerning Indian consumer. Decathlon entered the market about three years ago with a fully owned cash-and-carry [wholesale] venture, which has given them an advance insight into the market; the change to a retail business will now enable them to directly tap into the growing consumer demand for sporting goods and sportswear in the country."

Allowing foreign direct investment in retail has been a politically

sensitive issue for the last decade, and 100 percent FDI in single-brand

retail was permitted only in September 2012. Global retailers

are now looking at the Indian market with a different perspective

to evaluate the long-term gains and the potential of a retail

market that is still growing at more than 20 percent a year.

admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

Routes to Market – The Evolution

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

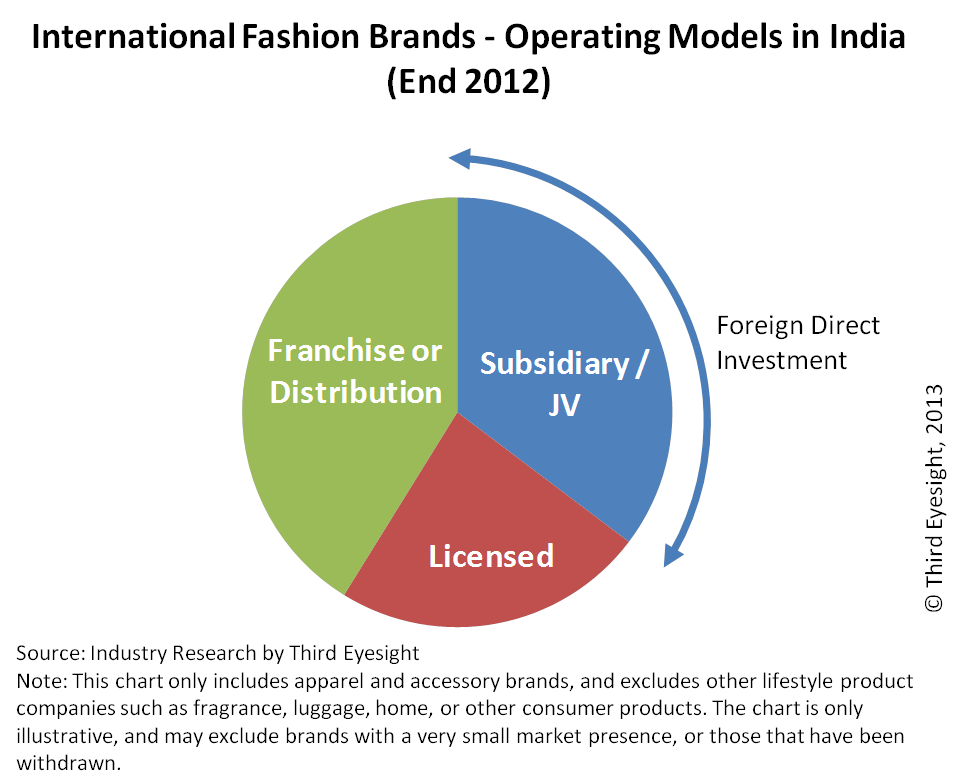

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.