admin

January 28, 2021

Written By DEBOJYOTI GHOSH

Sabyasachi Mukherjee, founder, Sabyasachi Couture

Sabyasachi Mukherjee has made it to the top of the couture sweepstakes. And now, with a new partner in Kumar Mangalam Birla-led ABFRL, the designer aims to expand his brand to the larger mass market.

Over the last two decades, Kolkata-based fashion designer Sabyasachi Mukherjee didn’t allow outside funding into his business which is now almost synonymous with Indian luxury wedding fashion. Years ago, L Capital (now L Catterton, the $20 billion private equity firm co-founded by LVMH) wanted to back the luxury fashion house but, for Mukherjee, it was too premature a business then for large investors to fund. In an interview to Fortune India in 2019, however, Mukherjee expressed interest in investor money. “The business has developed an identity now… and I will be in control of the situation. I will not let outsiders control it,” he had said then.

Circa 2021: On Wednesday evening, Mumbai-based fashion retailer Aditya Birla Fashion and Retail Limited (ABFRL) announced an infusion of ₹398 crore for a 51% stake in the designer’s fashion company Sabyasachi Couture which sells garments, accessories, and fine jewellery under his eponymous label. Reason: To ensure continuity and long-term sustainable growth, the designer said in a statement.

“Sabyasachi’s is among the most successful designer businesses to have emerged in the last two decades. While most designers have struggled to scale their business, Sabyasachi Mukherjee has successfully scaled his product offer as well as brand portfolio over the years. However, the business has been hit hard during the pandemic like all fashion and retail businesses, and a significant injection of money is needed to maintain the business momentum, and to scale it further,” said Devangshu Dutta, chief executive of retail consultancy Third Eyesight.

Experts say that the overall luxury market has suffered from a Coronavirus-induced shutdown in global travel since March last year. The pandemic has slowed over a decade of growth across luxury categories including fashion.

According to a December report by consulting firm McKinsey and The Business of Fashion, the global fashion industry’s profit is expected to fall by 93% in 2020. “Many fashion companies have taken time during the crisis to reshape their business models, streamline their operations, and sharpen their customer propositions,” the report added.

Dutta feels corporate partnerships and acquisitions allow a designer-entrepreneur and his/her investor partners to unlock some of the value that is being built.

Mukherjee has built arguably the biggest couture wear brand in the country, collaborated with global brands such as Christian Louboutin, the French king of luxury footwear, American upscale home furnishing chain Pottery Barn, Hong Kong-based luxury retail store Lane Crawford, Forevermark Diamonds and even Indian brands like Asian Paints. The designer brand also has a strong export business and ships garments, accessories, and fine jewellery to countries such as the U.S., the U.K., Hong Kong and the Middle East.

In the 20 years since he started out, Mukherjee has dressed heiresses, Bollywood actors, models, and hundreds of brides across the world. In 2018, he didn’t just design for the Deepika Padukone-Ranveer Singh wedding, but also other high-profile weddings including those of Priyanka Chopra-Nick Jonas and Isha Ambani-Anand Piramal.

Over the last few years, the Sabyasachi label has grown slowly but steadily. In FY18, Sabyasachi Couture posted a revenue of ₹209 crore followed by ₹253 crore in FY19 and ₹274 crore in FY20.

Indian fashion is predominantly sold in India, with wedding clothing comprising more than 90% of the market. The Sabyasachi brand is associated with opulent traditional wedding lehengas and sherwanis that start at about ₹1 lakh but can go above ₹10 lakh. In an earlier interview to Fortune India, Mukherjee expressed his desire to go beyond being just a wedding apparel designer and create a global luxury lifestyle brand that includes everything from undergarments and perfume to cosmetics and home furnishings.

“If you look at the model of Chanel, there’s nothing minimalistic about the clothes. The clothes are the trophy of their business, but the main money comes from cosmetics, shoes, accessories, and jewellery,” the 47-year-old designer had said then, adding that he wanted to grow the business into products that people can afford, such as cosmetics and perfumes. “You go mass without diluting the sensibilities of the brand,” Mukherjee had noted.

ABFRL expects the deal to accelerate the company’s strategy to capture a large share of the ethnic wear market through a comprehensive and attractive portfolio of brands, across key consumer segments, usage occasions and geographies, the company said in a statement adding that it plans to build a large ethnic wear business over the next few years.

ABFRL, which owns fashion brands such as Peter England, Louis Philippe, and Van Heusen, has made two key acquisitions in the Indian ethnic wear and lifestyle space in the past. In 2019, ABFRL picked up a 51% stake in fashion designers Shantanu & Nikhil’s Finesse International Design which makes bespoke apparel, footwear and accessories for men and women reportedly for ₹60 crore. The same year it also acquired ethnic wear and lifestyle retailer Jaypore for ₹110 crore.

“Over the next few years, ABFRL intends to craft a portfolio that addresses the entire gamut of ethnic wear segments: value, premium, and luxury,” Ashish Dikshit, managing director, ABFRL noted in a statement.

In October last year, Walmart-owned Flipkart Group, which owns fashion portal Myntra, acquired a 7.8% stake in ABFRL at an investment of ₹1,500 crore. For ABFRL, which operates a network of more than 3,000 stores and has over 6,700 points of sale across India, the deal will lead to a significant reduction in its debt.

Industry experts point out that ABFRL would have acquired a majority in a business with an eye towards scaling Sabyasachi into a larger brand, available at more accessible price points to a much larger audience, both in India and internationally. This may happen using the much larger retail platform that is available to ABFRL. Dutta feels it is quite likely that, in due course, ABFRL will wish to own the business in its entirety.

“There may be benefits from operational and systems disciplines, sourcing strengths, the financial muscle of a larger partner, but the brand and its intrinsic identity must not be diluted. If the brand has to maintain its cachet, its distinctiveness, it would need to be allowed to run with significant independence on the product and the customer experience side,” he adds.

Source: fortuneindia

admin

January 25, 2021

Written By Devika Singh

As demand for formal footwear dips, brands shift focus to casual wear such as flip-flops and slides

Overall, industry watchers predict that the footwear market will be out of the woods by mid-2021.

The pandemic has forced footwear brands to retrace their steps. As sales of formal footwear declined, with consumers working from home, the spotlight has fallen on casual footwear. Footwear manufacturers such as Lakhani Footwear, Red Chief and Metro Brands (which houses Metro Shoes), Mochi and Walkaway, have rejigged their strategy in the past year to suit this trend.

According to Ayyappan Rajagopal, head of business, Myntra, the relatively smaller segment of open footwear, which includes flip-flops and slides, has posted the strongest growth in the footwear segment on Myntra in 2020. “This rising demand led to several leading brands placing a higher emphasis on the casual segment on our platform,” he adds. Meanwhile, formal and occasion wear have taken a big hit.

Abheek Singhi, MD and senior partner, BCG, estimates that the footwear market in India is valued at Rs 75,000-85,000 crore, and about 45-50% of this market is unbranded. Most of the companies operating in the branded segment reported a 90-100% recovery in sales in the third quarter of FY21 (October-December), compared to the pre-Covid period. For the entire financial year, however, the revenue for the segment will see a drop of 10-15%, as per ICRA.

Informal is in

Much like the apparel and electronics categories, footwear, too, has seen better recovery in tier II cities and beyond. Lakhani Footwear claims it will close the year at the same revenue as last year — Rs 165 crore — despite the tough initial two-three months owing to the lockdown. The company currently caters to consumers at the bottom of the pyramid, with products such as slippers, sandals and shoes in the range of Rs 100-1500.

Lakhani Footwear is now bringing out a casual footwear range, with an eye on tier I cities, which will include sneakers and fashion footwear. “We have tied up with e-commerce marketplaces to introduce these products, and will also retail them through our website by Diwali,” says Mayank Lakhani, MD, Lakhani Infinity Footwear. These products will be priced in the Rs 700-2,000 range.

Red Chief is planning to launch a new brand, Comfort Walk, which would include products like flip-flops and slides for “value-seeking” consumers. “The demand for our products priced above Rs 2,500 was sluggish in 2020; hence, we plan to introduce a product range priced below Rs 1,000,” says Akhilesh Singh, COO, Leayan Global, which owns brand Red Chief. The company earns 40% of its revenue from formal leather shoes and 60% from casual footwear. Its products fall in the Rs 1,800-4,000 price range.

Making casualisation a priority, Metro Brands has reshuffled its inventory, and also designed a work-from-home collection in-house. “A few external formal brands are being phased out, while some like ID and Buckaroo are moving from offering formal to more casual footwear,” says Alisha Malik, VP, e-commerce and marketing, Metro Brands.

Further, the company is putting off investing in new inventory for its super-premium range of footwear that are priced at Rs 10,000-25,000. Metro Brands also plans to amplify the presence of Crocs, for which it is the retail partner in India, in the metro cities.

A good step?

Although the fashion industry has been moving towards casualisation since a while, the pandemic has certainly accelerated the pace, experts say. “In the past, most fashion trends cycles have lasted at least for a decade, so the shift towards casualisation is going to stay for a longer term,” says Singhi of BCG.

But footwear manufacturers, especially those that are mid-sized, will have to tread with caution as they will have to invest in building new capabilities — wider distribution networks and a robust online strategy — as they diversify their portfolios.

Devangshu Dutta, chief executive, Third Eyesight, says that footwear products, in general, have a longer lead time. They typically take about a year to be designed and launched in the market, and, hence, need more investment. “Companies will have to ensure that they make good of this investment,” he cautions.

Overall, industry watchers predict that the footwear market will be out of the woods by mid-2021.

Source: financialexpress

admin

January 1, 2021

Written By ANSHUL DHAMIJA

Sunder Genomal, MD, Page Industries

Page Industries got the underwear out of the closet and achieved a decadal success story like no other. A slowing economy has dented its sheen, but the company believes it is still in a sweet spot.

A visit to a Jockey store for day-to-day apparel like underwear or just plain pyjamas is sure to make one’s wallet lighter. For example, for men who like to laze at home in their boxers, the cost of the garment is upwards of ₹419 apiece. Pyjamas, another comfort garment, costs a shade under ₹1,000 apiece. Jockey, an American brand that re-entered India in 1995 (it was around for about three-four years in the early 1970s), generally carries a premium of at least 20% over other Indian mainline innerwear brands like Lux, Rupa, and Dollar.

Billionaire Sunder Genomal, though, likes to think of Jockey as a “value for money proposition” for the Indian consumer. “An aspirational, yet affordable brand,” says the 67-year-old managing director of Page Industries, the exclusive licensee of Jockey International Inc. in India, Sri Lanka, Bangladesh, Nepal, the U.A.E., Oman, and Qatar. The company is also the licensee of the U.K.’s swimwear brand, Speedo International, in India and Sri Lanka. Jockey, though, is the mainstay brand of Page Industries. Genomal, along with his elder brothers Nari and Ramesh, holds about 54% stake in Page Industries, which commands a market capitalisa – tion of about $3.2 billion, as of mid-November. “We like to offer the consumer more than what we have promised—quality, style, and comfort at a sensible price,” Genomal tells Fortune India. His words are solidly backed by the performance of the company

Image : Graphics by Rahul Sharma

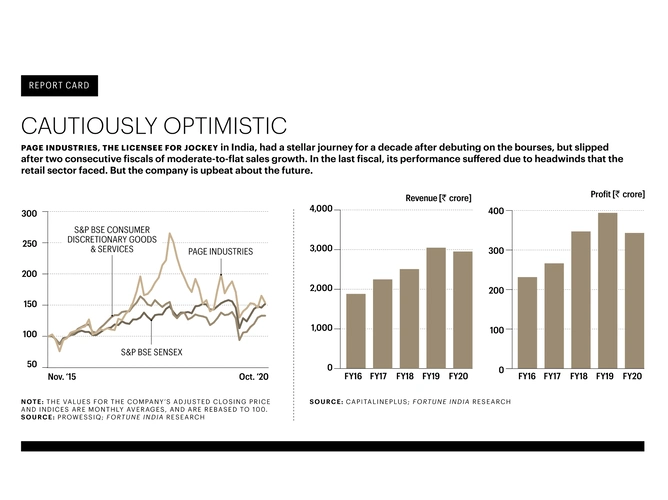

Having reported a nine-year revenue and profit CAGR (compound annual growth rate) of 27% and 29%, respectively, in this decade, Page Industries has been the fastest-growing apparel company in India, according to a report by brokerage firm Anand Rathi.

Jockey, too, is the single largest-selling apparel brand in India. On the bourses, the Page Industries share price has moved from ₹395, after its stock market debut in 2007, to ₹22,185 as of mid-November this year—a whopping 5,550% growth and an indication of investor confidence in the company. Its share price had even touched a high of ₹34,688 in August 2018 but slipped after two consecutive fiscals of moderate-to-flat sales growth. This made retail analysts question whether the innerwear maker had peaked out. “At some point you start to hit the glass ceiling of overall market growth, which also depends on how the economy is doing,” points out Devangshu Dutta, CEO of Third Eyesight, a consultancy firm.

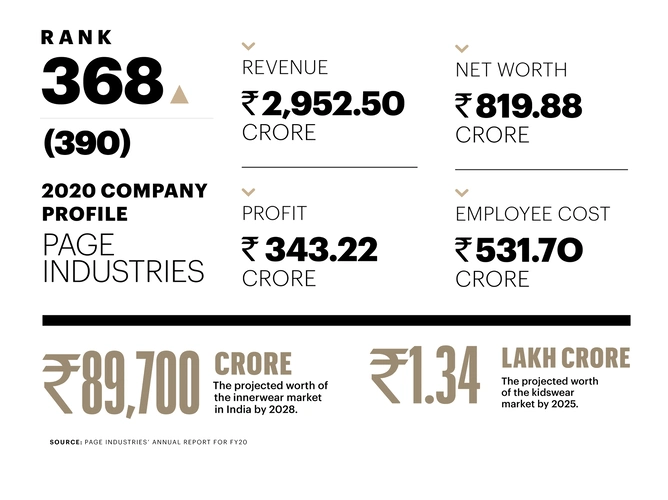

Ranked No. 368 on the Fortune India 500 list, Page Industries has no doubt been a decadal success story like no other. “Post 1995, a new generation of professional executives in IT, banking, and other sectors had emerged, and Jockey, being an international brand, appealed to them,” says Govind Shrikhande, the former managing director of departmental store chain Shoppers Stop. Ironically, the brand is “not as strong in the U.S. as it is in India,” he adds.

Regarded by stock analysts as a quiet and efficient performer, Page Industries has been devoid of any major controversy. That’s up until September this year when reports of human rights violations at a company factory in Bengaluru surfaced. The Worldwide Responsible Accredited Production (WRAP), a non-profit entity dedicated to promoting safe, lawful, humane, and ethical manufacturing around the world, began an investigation into the alleged violations; Jockey is a founding member of the industry watchdog.

Image : Graphics by Rahul Sharma

While Genomal steered clear of the issue, a Reuters report in October said: “Page [Industries] denied wrongdoing and called allegations of verbal abuse and workplace intimidation against employees ‘outrageous’.”

Brokerage firm Edelweiss, in its results report on Page Industries in November, highlighted that clearance from WRAP could come in the coming weeks. The report, which detailed the conference call highlights with the company’s management, said: “WRAP has conducted a rigorous inspection in October and they are satisfied with the status of affairs… WRAP has indicated that none of the allegations highlighted were mentioned by the employees.”

Brand consultant Raghu B. Viswanath says the investigation by WRAP would hardly dent the overall image of the company. “I don’t believe that brand Jockey will be seen in a lesser light by the consumer given its extremely strong equity,” says Viswanath, also the chairman and chief vision holder of consultancy firm Vertebrand. From a low of `18,000 in September, Page Industries’ share price was up 23% by mid-November, showing no signs of investors losing confidence in the company.

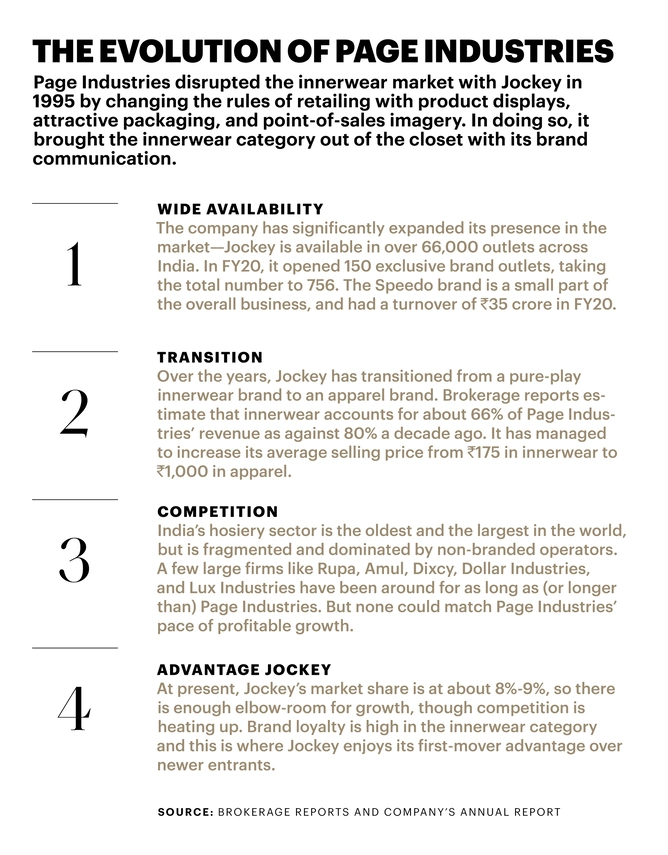

Jockey re-entered the Indian market at a time when innerwear was a segment of little worth to the consumer, and investing in a premium brand was hardly a trend. But Page Industries focussed on product quality and quickly built a go-to brand around Jockey. It developed an extensive network of distributors, much like an FMCG company, across the country; changed the rules of retailing with product displays and attractive packaging, and—to a great extent—brought the innerwear category out of the closet. “It helped redefine the entire category,” says Viswanath. “This created a headstart advantage for the brand, even as many other players with deep marketing budgets are still trying to play catch-up.”

Page Industries plant

Data sourced from Page Industries’ FY20 annual report shows that India’s innerwear market has an estimated worth of ₹32,000 crore, accounting for 9% of the total fashion retail market. Of that, 64% comprises the women’s innerwear segment, with the balance being the men’s and kid’s segments. The innerwear market is projected to grow at a CAGR of 11% to reach ₹89,700 crore by 2028. The women’s segment is projected to grow at 12.5%, almost double the pace of the men’s segment. According to brokerage firm Geojit, Jockey has a 19%-20% market share in the men’s premium innerwear segment, and 5%-6% in the women’s segment.

Given the projected growth in the women’s category, Page Industries is already on the ball. It has been adding exclusive brand outlets for women to its retail network (44 such outlets have been rolled out so far), and is adding another 90,000 sq. ft. of manufacturing space in Hassan, Karnataka, to cater to the growth of the women and kidswear segments. The latter is another key growth driver for the company, given its projected market size of ₹1.34 lakh crore by 2025. At present, almost 45% of Jockey sales in India is driven by the men’s innerwear category, where competition has picked up pace.

Image : Graphics by Rahul Sharma

Over the last 24 months, the retail industry has suffered heavily—beginning with a slowdown in the economy and followed by the Covid-19 pandemic, which led to brick-and-mortar retail being shut for about two months. “Right from the last quarter of 2019, the Indian economy has been under stress. There have been huge pileups of unsold inventory across many brands since then,” says Viswanath. Page Industries’ FY20 performance (see graph) was a testament to the headwinds in the retail sector.

Now, in the shadow of Covid-19, there are more headwinds for innerwear brands, and they need to re-examine their strategies given that people aren’t going out as often as they did. Consequently, the need to buy more undergarment pieces comes down. Intrinsically, the category has challenges such as a higher replacement cycle, especially among men. “In the U.S. and Europe, men typically buy underwear multiple times, and every year, as it is part of their fashion and lifestyle wardrobe. In India, the replacement cycle varies between two to three years as this category is still only a necessity,” says Shrikhande.

“This can only be addressed through product innovation, fashion, personality, and brand-led differentiations,” he adds. And that’s already visible with niche men’s innerwear brands such as XYXX and One8, which is owned by India’s cricket captain Virat Kohli. Page Industries’ profitable growth and low barriers to entry have also led to a rise in competition.

Three years ago, Pepe Jeans Europe entered into an equal joint venture partnership with hosiery major Dollar Industries to manufacture and market premium fashion innerwear, loungewear, gymwear, and sleepwear clothing for adults and kids. Likewise, for a play in the premium segment, Kolkata-based Rupa & Co.’s subsidiary, Oban Fashions Private Limited, acquired the brand licences of FCUK and Fruit of the Loom. Apart from this, a few domestic and international fashion brands like Van Heusen, U.S. Polo Assn., and Tommy Hilfiger have also started jostling for space in this category.

Jockey re-entered the Indian market at a time when innerwear was a segment of little worth to the consumer, and investing in a premium brand was hardly a trend. But Page Industries focussed on product quality and quickly built a go-to brand around Jockey. It developed an extensive network of distributors, much like an FMCG company, across the country; changed the rules of retailing with product displays and attractive packaging, and—to a great extent—brought the innerwear category out of the closet.

“While in the past the competition wasn’t credible, the newer competition is more credible, has sound brand equity, and better distribution,” says the Anand Rathi report. “We believe the increase in competition will have a slight impact on Page’s [Industries] growth ahead.” Moreover, the new entrants have the second-mover advantage: entry into a market that’s primed and ready for a brand. “It took Van Heusen innerwear about two years to reach revenue of ₹200 crore while Jockey had taken about nine years to hit half of that, and another 14 years to reach ₹200 crore,” the report added.

Many within the industry believe that the innerwear category will evolve much like the fashion space, where different kinds of products would be positioned for different occasions. For example, different underwear for work, home, and for partying. “That said, the brand Jockey, I feel, is still synonymous in India with what is ‘inside’. It’s the ‘Intel Inside’ of the Indian innerwear market,” quips Viswanath.

If Covid-19 is ensuring that people aren’t going out enough and, hence, not changing their underwear often enough, then leisurewear, which includes the athleisure clothing segment, is “going through the roof”, says Genomal. “People have realised that these are multi-functional products and the athleisure segment’s share of the pie will certainly increase significantly, in terms of the overall sales, going forward.” For the first six months of the ongoing fiscal, Page Industries reported revenue of ₹1,025 crore, a 36% drop compared to the corresponding period a year ago, on account of the impact of the pandemic. Its profit fell by 68% to ₹71.3 crore. Genomal maintains that sales are back to near pre-Covid-19 levels across product categories.

But it still begs the question whether Page Industries would be able to repeat its phenomenal decadal growth in the next decade. Despite the headroom for growth, analysts are doubtful, given the rise in competition. “It will be vital for them to retain the appeal among younger consumers, without which the momentum is bound to slow down,” says Dutta of Third Eyesight.

Genomal, a citizen of the Philippines who has set up base in Bengaluru, though, believes that brand Jockey is in a sweet spot. “We just need to focus on our core competency and keep our heads down,” he says. “The kind of portfolio that we have is still highly under-penetrated. We are actually more excited today than we ever were about the future,” says Genomal, whose exposure to the Jockey brand began when he was 10 years old. His father, Topandas Verhomal Genomal, was granted the exclusive licence to manufacture and retail Jockey in the Philippines in 1959. Genomal brought that legacy partnership to India and the rest, as they say, is history.

Source: fortuneindia

admin

December 14, 2020

Written By Yashi Gupta

The numbers are not working in Walmart’s favour either. More than a decade after entering the country, Walmart has accumulated a loss of Rs 2,500 crore. In the year ended March, Walmart India posted a net loss of Rs 299 crore while revenue grew 20 percent to Rs 4,926 crore.

Flipkart plans to cut Walmart’s store size by half to turn the remaining space into warehouses for its online business, according to an Economic Times report. Sources told ET that Flipkart could entirely convert some stores into fulfilment centres.

Walmart started its operations in India in 2009 and currently operates 29 stores with the size of 50,000 sq ft. In July 2020, Flipkart acquired Walmart’s cash-and-carry business and announced the launch of a new B2B marketplace, Flipkart Wholesale. This reverse acquisition was expected to accelerate its expansion in the food and grocery segment and strengthen its supply chain.

However, the falling relevance of brick-and-mortar stores in India has now prompted the e-commerce firm to convert twenty-nine of Walmart’s cash and carry stores into wholesale and warehousing centres. Before the acquisition, Walmart was planning to cut its store sizes from 50,000 to 45,000 sq ft. The then President and CEO of Walmart India, Krish Iyer, had said in 2019: “Customer centricity and availability of right real estate land parcel help us determine the location and size. At a couple of locations, we have developed smaller stores of 45,000 sq ft more so to help us meet the member needs of those unique geographies based on the availability of right land parcels.” This strategy gave it an advantage in terms of market penetration to serve the customers optimally.

The latest decision was taken to adapt to the changing consumer in behaviour and mounting losses. According to the latest data, Walmart’s stores generate half of their revenues from online sales or sales teams visiting B2B members for orders.

“The existing stores serve local businesses and Kirana stores but combining it with online will help address the entire catchment area better,” said Devangshu Dutta, founder of strategy consulting firm Third Eyesight. “So they are making the assets work a little harder and clearly it is a logical move to combine their online strength with a brick-and-mortar presence.”

The numbers are not working in Walmart’s favour either. More than a decade after entering the country, Walmart has accumulated a loss of Rs 2,500 crore. In the year ended March, Walmart India posted a net loss of Rs 299 crore while revenue grew 20 percent to Rs 4,926 crore.

Flipkart has also announced absorption of 5000 of Walmart’s employees on Friday. It said that Walmart’s employees would be given corresponding roles in Flipkart with matching terms of compensation, responsibility, and profiles.

Source: cnbctv18

admin

December 10, 2020

Written By Samreen Ahmed

Grofers, which has a strong play in the private labels segment across categories, is likely to follow this strategy in the fashion segment

Grofers is replicating this BigBazaar kind of model giving more options to increase the amount of spending they get from households, says Meena.

Online grocer Grofers started selling apparel and footwear for better margins. Grocery forms the largest chunk of consumer spending and highly competitive but fashion offers better profits, according to ecommerce experts.

“From a scale and stickiness perspective grocery as a segment is very attractive but from a margin perspective, it is quite competitive. In all of food and grocery sales across the country, even in large cities where internet penetration is high, grocery still remains focussed largely on offline. This segment also requires deep pockets,” said Devangshu Dutta, Chief Executive Officer of Third Eyesight./

The SoftBank and Tiger Global-funded company has started selling low-priced items in apparel, footwear, non-clothing and travel accessories categories to expand its basket size. It has already seen a 40 per cent increase in its overall basket size as compared to the pre-Covid era.

“This category is important as it is the second largest after electronics in online shopping and attracts new customers on board.

While there is good margin in fashion, it grows further when it comes to private labels,” explains Satish Meena, Senior Forecast Analyst at Forrester Research. The private label brands have been providing an opportunity to make fashion more affordable to the masses and these changes in pricing are driving more customers to online platforms, said a RedSeer report.

Grofers, which has a strong play in the private labels segment across categories, is likely to follow this strategy in the fashion segment.

With 1,200 products across all categories, the private labels segment constitutes more than half of the company’s sales. Currently, its own brands form 40 per cent of the business, and the company is expecting to grow this to 60 per cent.

Grofers is replicating this BigBazaar kind of model giving more options to increase the amount of spending they get from households, says Meena. Apart from fashion and lifestyle products, it has also forayed into the winter assortment category selling blankets, comforters, room heaters, beginning mid-October.

According to RedSeer, while the fashion market is growing at a CAGR of 11 per cent in the country, online fashion is growing the fastest at a CAGR of 32 per cent. With players such as Myntra and Ajio already having a stronghold in the segment, it will be challenging for Grofers to make a mark in this new category.

“We don’t expect this to be a great strategy as category leaders like Myntra outperforms Grofers both in offering (variety) and price,” says IDBI Capital in a note.

Currently operational in 27 cities, Grofers claims to have acquired 1.8 million new customers since the lockdown. “We have seen a spurt in demand from non-metro markets as online grocery has become a mass household phenomenon. We have witnessed an increase of 54 per cent in orders in smaller cities like Indore, Agra, Panipat,” said the Gurugram-based company.

According to reports, the company is also in the process of raising up to $60 million from investors as marquee players such as Tatas, Reliance, and Amazon make big bets in the online grocery space.

Customer trends during Covid-19 pandemic

* 1.8 mn new customers

* 40% increase in basket size

* 54% rise in orders from Tier II/III

* 64% first time online grocery shoppers

* 20% first time online shoppers

Source: Company

Source: business-standard