admin

June 16, 2009

![]() By Raghavendra Kamath

By Raghavendra Kamath

![]() Business Standard

Business Standard

![]() Mumbai June 16, 2009

Mumbai June 16, 2009

Speciality homeware retail chains, such as Kishore Biyani’s HomeTown, Landmark group’s Max Retail and Wadhawan group’s Home Store, have changed tack as home sales drop and shoppers defer buying big-ticket items like furniture and furnishing to save cash in the downturn.

The realty sector has seen home sales fall by up to 70 per cent in the early part of this calendar year from the peak in 2007-08 and developers have shifted to smaller, affordable homes to counter the drop in sales.

Consequently, retailers are witnessing a drop in sales, too.

Pantaloon Retail, the country’s largest listed retailer, has seen a continuous slide in same-store sales in its home retailing segment in the last seven months. From a steep fall of 36 per cent in November 2008, Pantaloon has seen further drops, ranging from 4 per cent to 28 per cent, in home retailing from January-May 2009.

To counter the slowing sales, retailers have adopted strategies to prop sales and cut losses. For instance, HomeTown has increased its offering in the value segment and launched furniture and bedroom sets in the Rs 10,000-15,000 category to boost sales.

HomeTown is also planning a shopping event called ‘Home Carnival’ soon .

"Home retailing was in doldrums in the end 4-6 months of 2008. People were not buying new homes and that was impacting home retailing," said Mahesh Shah, chief executive of HomeTown, a part of Pantaloon Retail.

Max Retail, a part of the Dubai-based Landmark group, has removed the home category from its stores altogether, while others like the Mumbai-based Wadhawan group – which acquired Home Store, a chain selling homeware items earlier – is not expanding its half-a-dozen stores to conserve cash.

Max is also reducing its store size to 10,000 sq ft from 14,000 sq ft to optimise costs. The home category used to occupy 6 per cent of its space, while contributing 10 per cent of its revenues.

After a lackluster performance in the last six months, homeware retailers believe things have changed in the last two-three weeks with the sales of affordable homes picking up.

"Sales have picked up since last month. We are expecting 5-6 per cent growth from next month onwards," said Shah of HomeTown, which is planning to open four stores in Mumbai, Bangalore and Kolkata in the coming months.

According to estimates, the overall home retail market in the country is over Rs 50,000 crore in size, with organised retail segment accounting for just 10 per cent of that. Local carpenters and small furniture shops cater to most homeware needs.

"There is a lot of competition from unorganised players and it is difficult to make an impact here," said Vasanth Kumar, executive director of Max Retail.

Analysts say retailers prefer those categories which require less working capital and shorter inventory levels to beat a downturn. The home segment is considered as a high-inventory and capital-intensive segment. Food and grocery requires an inventory of 15-30 days, furniture and furnishings require inventories of 4-6 months.

"Besides a large inventory of goods, the home segment requires large space to showcase items. In the current financial scenario, retailers are looking at those segments which have a better sales-to-stock ratio," said Devangshu Dutta, chief executive of Third Eyesight, a retail consultancy.

International retail consultancy AT Kearney’s Debashish Mukherjee feels organised home retailing is yet to make a dent in the country.

"The average number of rooms per family and average square feet per person in India is very low. Since most of the furniture is imported, people do not have space for that. Besides, since the chains sell furniture made out of composite materials, Indian consumers are yet to move from wood to new materials," Mukherjee said.

admin

June 12, 2009

![]() By Sangita Ghosh and Sarimul Islam Choudhury

By Sangita Ghosh and Sarimul Islam Choudhury

![]() Indiaretailing.com

Indiaretailing.com

![]() 12 June 2009

12 June 2009

The sustainability of any business depends – to a large degree – on loyal customers who come back again and again for more shopping and organised retail is not an exception to that. This is a part of strategic management where the retailer has to think on the pointers of his business model; this includes service that leads to customer satisfaction, which leads to customer loyalty and which in turn leads to profitability. The factors related to retailer-customer relationship and the customer’s satisfaction help retailers to have a better understanding of the shopping experience.

The factors that help to integrate and influence customer satisfaction demand a quick and continuous flow of information and analyses of customer behaviour. Consumer purchase data is one of the most important tools to measure customer satisfaction in relation to overall sales and market performance of a particular retailer. Therefore, besides developing a new customer base, retaining the existing customers is also a challenge for most retailers.

To have an understanding of the subject, IndiaRetailing posted a poll on the theory that "Customers don’t return because retailers don’t stay in touch with them." This question was angled to scrutinise if for retailers it is enough to just stay in touch with customers to drive sales, or are there other factors that impact customer retention?

Out of the total votes cast, around 78 per cent of the respondents negated the statement, whereas only 22 per cent of their counterparts believe that not staying connected with customers can be a major contributor of customers not staying with a retailer.

When IndiaRetailing put the question to individual retailers, most agreed that not staying in touch can be a reason, but can never be the only reason.

Samar Singh Sheikhawat, VP, marketing, Spencer’s Retail Ltd said that with the economic downturn and constrained demand, customer experience is the first line of defense in sustaining a long-term customer relationship. "For that matter a favourable customer experience is fundamental in building consumer loyalty and improving consumer retention. Therefore, retailers would have to look at ways and means of being in touch with consumers – understand their shopping needs, design retail strategies around them and ensure that consumers get what they want," he stated.

Anup Jain, head-marketing, Pizza Hut, stated, "The statement is partly right but in the retail business, customers don’t return frequently when they don’t get much value for the money spent. At Pizza Hut, we don’t have loyalty programmes as such, but we do have online programmes where VIP (Very Into Pizza) members can access offers on our delivery channels. They can also get to know the latest information about the products from the site."

Harkirat Singh, MD, Woodland believes that it is not possible to keep in touch with the customers regularly unless there is a structured loyalty system in practice. But the retailer claims that very often he finds his customers returning repeatedly to his stores, even though he does not run a loyalty programme. Clearly, a mere showcase of a customer loyalty programme without value added services and cutting edge products on offer can’t retain customers in the long run.

As to what these other determinants may be, Devangshu Dutta, chief executive of Third Eyesight states that frequent visits of a customer to a particular store are guided by various elements. Sometimes it is the nature of the product – something like furniture will feature long gaps between purchases. In such cases, measuring loyalty can be a challenge. But there are other reasons that play a part. For instance, the location may be not the most convenient, or the store may not be distinguishing itself from its competitors, and may be selling a generic product, at average prices and with an indifferent service.

So, in that case, customers may be drawn back to the store more often by making sure the merchandise is updated frequently, especially if the retailer is not selling staples such as groceries, which draw the customer in at predictable intervals. "This is as true of books and music, as it is of fashion," Dutta notes.

However, a retailer has to distinguish between loyalty that is earned and loyalty that is bought, he points out.

"Earned loyalty is based on a store consistently performing better than other stores that are competing for the customer’s attention. On the other hand, in the short-term, loyalty can also be bought through discounts. But even in loyalty discounts there is an underlying feeling of ‘being recognised’ that keeps the customer tied to the store," Dutta says. "I believe loyalty that is earned is more lasting. All the elements that make up the store – the product, the pricing, the location, the knowledge and attitude of the store staff, the infrastructure – must work together to provide an experience that is truly distinctive and memorable, and that make a customer loyal. Therefore, it is much more difficult for a competitor to replicate the unique combination of product and service that makes a store special to the customer."

Having said that, Dutta believes that loyalty schemes do have a role to play in both cases — whether a retailer wants to earn the customer’s loyalty or buy it. "If structured well with a well-developed information system, a loyalty scheme can enable a retailer to not only to be in touch with its customers more regularly, but also to distinguish between customers and service the individual customers much better," he concludes.

admin

May 9, 2009

By Devangshu Dutta, Tarang Gautam Saxena

While the Indian consumers have aspired to own international fashion brands, India’s large population base in turn has been an aspirational market for the international companies.

To remote observers, the Indian market may appear to be a virgin territory as far as international apparel and footwear brands are concerned. But India has seen the presence of international brands for almost a century, including mass brands such as Bata and luxury brands such as Louis Vuitton. However, as the colonial government systematically repressed local textile production, the local resistance to foreign products grew as well. Therefore, until the 1980s, the presence of international fashion brands was negligible.

In the early 1990s, as the Indian economy opened up again, a few international fashion brands entered the Indian market. The pioneering companies during this stage were Benetton, Coats Viyella and VF Corporation.

At this time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment which was thus a target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike).

In the midst of this the media industry was also witnessing a high growth which aided the international brands in gaining visibility and establishing brand equity in the Indian market.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. A growing supply of good-quality retail real estate in the form of shopping centers and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores and shops-in-shop.

The number of international brands continued to grow each year at a steady pace until the early 2000s, and took off exponentially thereafter. By 2005 the number of international fashion brands present in India was over three times compared to that in the mid 1990s. The last few years (since 2005) have continued the significant growth of international fashion brands, including luxury brands such as LVMH, Aigner, Tommy Hilfiger and Chanel.

The Popular Entry Strategies

Many of the international companies entering India in the late 1980s and 1990s chose licensing as the entry route to India to gain a quick access to the Indian market at a minimal investment.

A few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand.

In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought investors in retail real estate that were ideal franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in “Single Brand” retail). Using this route, many brands have entered India by setting up majority owned joint ventures, or transitioned their existing franchise arrangements into a joint venture structure.

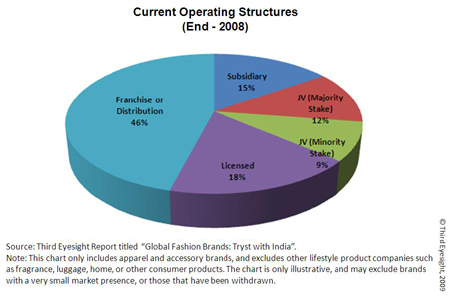

The Entry Structure for Some International Brands

| Entry Strategy | Time Period | ||

| 1980s or Earlier | 1990s | Post-1999 | |

| Licensed | Louis Philippe, United Colors of Benetton and 012, Wrangler | Allen Solly, Arrow, Jockey, Lacoste, Lee, Nike, Van Heusen, Vanity Fair | Puma |

| Wholly Owned Subsidiary | Bata, Pepe Jeans | Levi’s® | Hanes, Triumph |

| Joint Venture (Majority) | Adidas, Reebok | Diesel, Nautica, Sixty Group | |

| Franchise or Distribution | Aldo, Burberry, Canali, Versace, Debenhams, Esprit, Gucci, Guess, Hugo Boss, Mango, Marks & Spencer, Mothercare, Tommy Hilfiger | ||

| Joint Venture (incl. Minority Stake) | Celio, Etam, Giordano | ||

Source: “Global Fashion Brands: Tryst with India” (A Report by Third Eyesight) © Third Eyesight, 2009

Note: The above table shows the structure used during entry, and not the structure that exists currently.

By the end of 2008, just under half of the brands were present through a franchise or distribution relationship, while over a quarter had either a wholly-owned or majority-owned subsidiary. These structures allowed the brands to have greater control of operations, particularly of product.

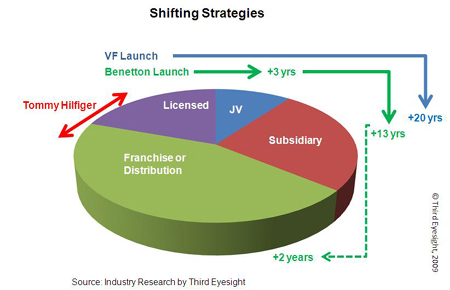

Shifting Strategies

Many international companies have evolved their presence in India into structures different from those at the time they entered the market.

A good example depicting the shift in business strategy is that of VF Corporation which entered India in 1980s by assigning the Wrangler license to Dupont Sportswear. Since then it has launched a variety of brands in different product categories with number of Indian partners and finally formed a joint venture, VF Arvind Brands Pvt. Ltd., with Arvind Brands.

Another example of a company that has evolved its presence is Benetton, which first entered India through a licensee (Dalmia). Benetton then transitioned in 1991 into 50:50 joint-venture and finally in 2004 took over the Indian business completely. However, it adopted the franchising route in 2006 for its premium fashion brand, Sisley, appointing Trent (a Tata Group company) as the national retail franchisee.

Many other companies such as Nike, Tommy Hilfiger, Marks & Spencer and Pierre Cardin (as described in our report “Global Fashion Brands: Tryst with India”) have changed their approach as the original structures did not perform as well as they had expected.

Obviously, each such change has cost the brands time, management effort, money and, sometimes, market share.

We believe that these shifts and the pain related to it could have been reduced, had the brands ruthlessly questioned the motivation for considering this market and their expectations from the market in determining an appropriate strategy.

What’s Ahead?

In the midst of economic upheaval around the world, how does India look as a market for international fashion brands?

Well, it is difficult to generalize even in the best of times. In the current global turmoil there is certainly a lot more unpredictability about international expansion for most companies.

Although India’s position as a target market for international brands has been improving, as is evident from the number of launches in the last 6-7 years, some companies considering international expansion may prefer entering other markets that may seem more “familiar”, developed and safe (such as Europe, Japan, South Korea or Taiwan). Against such comparisons, India’s growing but fragmented market can seem chaotic and difficult to deal with.

However, the fact remains that there are very few markets globally that can provide the sustained size of mid-term and long-term opportunity that India does. We are already seeing the more far-sighted and committed brands consolidating their position and presence in the market by continuing to look at expansion, even while examining how they can make their existing points of sale perform better. We also constantly come across new companies carrying out investigations into the market.

In the current environment we expect to see a shift in the nature of launch vehicle. While franchising seems to be a safe option for risk-averse brands in the current times, we will probably see more brands with a long term strategy, who would establish a controlled presence either through joint-ventures or through wholly-owned subsidiaries, since they can lay the foundation of the business today at much lower costs today than in the past few years.

India’s foreign direct investment (FDI) policy, allowing FDI only up to 51% in retail trading of “Single Brand” may have held back some fashion brands as they are still managed by owner founder with a conservative outlook on “control”. However, in the last couple of years, we have found companies not being deterred by the barriers to FDI.

As their comfort and familiarity with India has grown, international companies are more willing today to create corporate structures that allow them a presence in the market today and a step-through to a more controlling stake as and when government regulations allow.

All in all, we feel that international brands are in India not only to stay, but also to expand. There is yet a lot of potential untapped in the market, and as the integration of the Indian consumer with global trends continues, international brands can expect to find India an increasingly fertile ground for growth.

(c) 2009, Third Eyesight

admin

April 20, 2009

![]() By VISHAL KRISHNA

By VISHAL KRISHNA

![]() Businessworld Issue Dated 14-20 April 2009

Businessworld Issue Dated 14-20 April 2009 ![]()

Kishore Biyani took on a huge debt to expand Pantaloon Retail very quickly. Now the slowdown has made his life difficult

Rapid rollout of new stores has been Future Group founder and CEO Kishore Biyani’s major focus area. In the past two years, the country’s largest retailer has thrown open 7 million sq. ft of new shopping space across 24 formats in over 63 Indian cities, often at the rate of one store a day. The day BW met Biyani, 26 March, was another of those days. He was preparing to inaugurate three stores of flagship firm Pantaloon Retail India (PRIL) in Mumbai, the next day. Such frenzied expansion has kept PRIL, with 12 million sq. ft of retail space, well ahead of rivals Reliance Retail, Spencer’s Retail and Aditya Birla Retail. In fact, the three of them put together have less sq. ft of shop area than PRIL. But it has also taken a toll on PRIL’s balance sheet. A Rs 2,300-crore debt burden is the price Biyani paid for that expansion spree.

And now Biyani needs to cope with a slowdown. Coupled with PRIL’s debt burden is a 30 per cent drop in footfalls experienced by retailers across the country. While Biyani insists his stores have not seen any drop in footfalls, he admits that customer conversion has taken a hit — that basically means that the number of customers has not decreased, but the sales have.

Consulting firm KPMG says that for the first time in six years the same store sales of retailers is in the negative. At least 70 per cent of respondents surveyed by it reported a drop in footfalls. “People are downtrading, but they have not stopped buying,” insists Biyani. “The consumption story is not over in India, as portrayed by the media. Retail is a $350-billion market here, and it is a large canvas to capture for organised retailers.” What he doesn’t say is that when people downtrade, it also means lower margins for the retailer. So though Biyani has managed to increase some revenues, the margins have actually worsened.

In response to the slowdown, PRIL — which already owns 48 Pantaloon mid-market apparel stores , 110 Big Bazaars hypermarkets and 148 Food Bazaar supermarkets, besides 160 KB’s Fair Price Shops (the neighbourhood store format) — has decided to scale down its ambitions. It is going slow on setting up 30 Big Bazaars or adding another 1.5 million sq. ft that it had planned by June 2009. Predictably, the target of expanding even more aggressively to 30 million sq. ft has been pushed back from 2011 to 2013, denting the revenue target of Rs 20,000 crore by 2013. Plans to enter the cash-and-carry business have also been shelved.

Food Bazaar and KB’s Fair Price Shops have been the biggest casualty as organised retail struggles to cope with higher rentals, power and staff costs, which constitute 18-25 per cent of the revenues. Biyani’s bets have come down to managing these stores, which are constantly threatened by kirana stores. He confesses that it is the end of an era for the neighbourhood supermarkets. “This year, we will add only 2.5 million sq. ft and will not expand in suburbs of cities any more,” he says. A report by CLSA Asia Pacific Markets lays out the mistakes in the Indian market and states that small-sized food and grocery or supermarket format is unviable.

Earlier, in 2006, Biyani decided to exit the home furnishing format ‘Mela’ within a month of its launch. Fashion Station, a discounted private-label fashion merchandise, was converted to Fashion@Big Bazaar. Such slam-bang experimentation is common in all high-growth sectors, but Biyani has also had to look over the shoulder at the competition closing in on him.

Leader’s Resolve

In 2006, a host of existing and wannabe retailers were snapping at Biyani’s heels. While some such as RPG group-owned Spencer’s Retail were still some steps behind Biyani’s PRIL, others such as Raheja group’s Shoppers Stop were neck and neck in sales. But what threatened Biyani’s numero uno status the most was Reliance Industries’ announcement of a Rs 25,000-crore plan to enter the retail sector and dominate it with 10 million sq. ft of space and 1,000 stores by 2010.

As the leader in organised retail, Biyani had to act to keep ahead. And he did. PRIL grew 2.5 times from 5 million sq. ft to 12 million sq. ft in a span of two years until March 2009. It came at a steep price. The expansion raised his interest outgo by five times, from Rs 43 crore to Rs 200 crore in fiscal 2009. PRIL’s interest coverage ratio (which shows how easily a firm can pay interest on outstanding debt) has fallen to 2.20 times — it was 5.17 in 2006 and 2.69 in 2007. This means making interest payments are becoming more difficult than it used to be.

Here’s the nub of the problem. While PRIL’s revenues seem to be growing nicely, its other financials are actually deteriorating. The company recored a profit of Rs 102 crore in the first nine months FY09, a 27 per cent rise compared to FY08. But on consolidated basis PRIL reported net loss of Rs 61.55 crore in FY08 because of high depreciation, rentals and wages.

The company also seems to be running out of cash. “They have not generated any cash from operations (in the past five years). The downtrading of domestic consumption is affecting retailers. Apart from such shrinkages, higher debt costs are also pinching them,” says Indrajeet Kelkar, retail analyst at Dolat Capital in Mumbai. And its return on investments are not all that hot either.

With Rs 362 crore payable every year to meet long-term debt obligations for the next six years, PRIL’s 3 per cent return on capital employed may not be enough. On capital employed of Rs 5,342 crore, PRIL delivered a turnover of Rs 5,295 crore in 2007-08, representing a cash churn of only 0.98 times of capital employed. Internationally, Wal-Mart generates 2.29 times, but then the firm is a global behemoth. PRIL also has Rs 250 crore worth of inventory on its books and many believe the group’s extended discount sales are testimony to this. But Biyani rubbishes such statements and remains rooted to the Indian retail story.

Investor confidence in PRIL has hit a low too. As against a 63.7 per cent drop in the Sensex from its peak, PRIL’s stock has fallen 80 per cent from a high of Rs 876 on 2 January 2008 to 169 on 6 April 2009. Its market cap has dipped from a peak of Rs 12,913 crore in January 2008 to Rs 2,961 crore on 6 April 2009 (See‘Market Captalisation’). And with 21 million warrants worth Rs 1,050 crore coming up for conversion in three months, Biyani is a burdened man. He refuses to discuss the details of how he would arrange the finances for this but he is believed to have committed shares worth $85 million as a secondary pledge. This is a collateral to a primary pledge, which he would not disclose.

It is a tight-rope walk for Biyani, a man who has his moorings in western and oriental philosophies. He candidly admits that the supermarket format is challenged. “Businessmen make mistakes and only one Indian retailer has lost out so far. That man too can return if he raises money. The Indian retail business is alive,” insists Biyani, convinced that he can fight the slowdown. Only the short-term forecast is not very encouraging. According to Mumbai-based Cartesian Consulting, 53 per cent of retailers’ confidence in the market is shaken as they believe that the current uncertainty is likely to continue for at least 18 months.

All figures in Rs and for financial year 2008; EBITDA: earnings before interest,

taxes, depreciation and amortisation

Source: CLSA

Biyani’s book It Happened In India swears by his ability to defy the conventional wisdom. Only this time, his wisdom will be tested in the kind of market that no one has faced before. According to Crisil Research, the retail sector had grown at a CAGR (compound annual growth rate) of 10-14 per cent in the past three years driven by favourable demographics, rising disposable income and increasing urbanisation. During this period, organised retail grew at a higher rate of 28 per cent. With the slowdown, Crisil expects organised retail to grow 13 per cent per annum from Rs 85,000 crore in 2007-08 to Rs 1,10,970 crore in 2009-10.

Retail Rout: All In The Same Boat

The drop in customer footfalls and conversion ratios have been a double whammy for the retail business, resulting in low-er inventory turnover and higher working capital requirements. “Retailers overestimated the growth potential in India,” says Devangshu Datta, CEO of Third Eyesight, a retail consultancy firm in Delhi. Datta says retailers projected that organised retail will grab 20 per cent of the total retail market by 2012, while it still languishes at 5 per cent. Now that those projections seem unreal, large groups such as Aditya Birla Retail and Reliance Retail have slowed their business plans too.

Over the past two years, Spencer’s opened over 300 stores, Reliance opened 900 stores in three years and Aditya Birla 600 stores in two years. Today, some of these stores are shuttered and others may be closed down as well. The most disappointing has been the supermarkets format, which accounted for about 75 per cent of all new stores. “Although many achieved scale in terms of the number of stores, they did not build the supply chain,” says Ajay D’Souza, head of Crisil Research in Mumbai. He adds that competing with kirana stores, which have a 95 per cent market share, became difficult in this period. This, combined with low same-store sales in certain geographies, higher debt and negative cash flows, have caused several stores to shut down. “Your sales have to be very high if you are a retail store in the food category,” he says.

“It is regular customer traffic that drives volumes and retailers have not been able to keep loyal customers to generate profitability,” says Hemant Kalbag, principal consultant at A.T. Kearney in Mumbai. He cites the example of Wal-Mart, whose net sales in the fourth quarter of fiscal 2008 were $106.26 billion, a growth of 8.3 per cent compared to fourth quarter of 2007. Kalbag adds that the business model has to be right, which means the retail store needs to be supported by its assortment of value items in a store, which will generate high store sales. This, analysts say, should also be supported by a strong supply chain. But the slowdown has not helped in this quest.

admin

March 18, 2009

By Sushmita Choudhury

Money Today

March 18, 2009

When you know you are not getting an increment this April, does it make sense to splurge on a designer dress? What if it’s a Rs-26,000 Versace dress being offered at half the rate? On hearing about this sale, 25-year-old Bhavna Krishnaraj had only one question: “You mean I get to own Versace for the price of a month’s partying?” Adds the sales executive and part-time actor who divides her time between Delhi and Bengaluru: “I spend over Rs 13,000 on dining out, discotheque fees and weekend driving holidays.”

When the recession started in the second half of 2008, luxury retailers predicted that high-end brands would be immune as their target group would neither tighten their Chanel belts nor compromise on their lifestyles. Six months on, terms like recessionista and chicko-nomics are in and the Richie Rich club is shying away from luxury. This only means it’s party time for aspirational customers like Krishnaraj because high-end brands, desperate to encourage footfalls, are rolling out unheard of discounts, some even going up to 70%.

Some good bargains may be over as this is the time retailers typically start unveiling fresh stock, but don’t lose heart. There are plenty of end-of-season sales that show no signs of ending. Says Abhay Gupta, executive director, Blues Clothing Company, that represents several top labels in India, including Versace: “Discounts encourage the undecided, aspiring customers to be drawn into the client base. India offers a very large aspiring class that wants to get into the luxury bracket and these promotions help.”

| “Given the current economic situation, every retail segment, including luxury, is getting impacted.” – Devangshu Dutta, CEO, Third Eyesight |

Apart from Versace, Ashish Soni and Corneliani are also trying to tempt impromptu purchases by offering 50% discounts. Crave Armani? The world-famous suits at the Delhi outlet are now 40% cheaper. At the Malini Ramani outlet, last season’s creations probably cost less than your mobile phone bill. For example, a dress costing Rs 9,500 last year is now going for Rs 2,000. The good news is that most designer brands also have accessory lines. So even if you can’t make place in your wardrobe for a high-maintenance designer outfit, consider picking up add-ons, be it belts or bags. They cost less than apparel, yet carry the same snob appeal.

In addition, Delhi’s Emporio Mall, which houses only luxury brands—Dior, Harry Winston, Louis Vuitton and Tarun Tahiliani, to name a few—has an exciting month-long promotion under way. Shop for at least Rs 10,000 at the mall, which should not be difficult given the price tags, spin the fortune wheel at the lobby and walk away with guaranteed gifts, ranging from a discount voucher for one of the stores in the mall to free gifts. In addition, if you participate in the lucky draw, you may drive home in a BMW.

The cut-price couture mania is not limited to the capital. Many a luxe store at The Collection-UB City in Bengaluru has announced a sale. For instance, Moschino is selling its inventory at half the marked price. Also at Bengaluru, Samsaara, the multi-brand luxury boutique housing collections by top Indian designers, is offering a 50% discount. If you don’t think Rs 1,500 is too steep for a negligee, then Etam is the place to go. The luxe French lingerie brand has a flat 70% off on its entire stock at its Bengaluru and Delhi outlets.

While recession-proof luxury has been globally established as an oxymoron, the India story stands out. This is one of the very few retailing hotspots where high-brow brands that, as a rule, don’t mark things down, have been compelled to offer rebates. For instance, Versace CEO Giancarlo Di Risio recently commented that the brand’s core customer did not queue up for bargains at post-Christmas sales, but was “on the slopes in St Moritz or on a boat in the Caribbean”. Yet, the outlets in India have not balked at catering to bargain-hunters.

Interestingly, most luxury retailers cringe at linking these bargains to recession. Gupta, for one, quotes surplus choice to explain lower same-store, year-on-year sales. “The same customer is being chased by too many brands in a particular product category. Our margins are impacted by higher costs on rentals and other operational overheads rather than recession, which is more of a mediagenerated hype than reality,” he adds. So some brands are calling it the end-of-season sale, while others term it a promotion and most of them don’t advertise it loudly.

Whatever it’s called, it’s probably your first chance to own designer labels without robbing a bank. You’d better hurry, though. These offers are open ‘only till stocks last’. Also, the bargain bonanza is not going to be there for much longer. Industry experts are unanimous in their belief that demand will pick up again in the next six months.

What if consumers continue to play scrooge? According to Devangshu Dutta, CEO, Third Eyesight, a specialist consulting firm for the retail sector, brands have three backup strategies. One is to mark down off-season merchandise (so there may be another round of sales before the winter collections are launched). Another option is to open discount outlets so long as the brand can generate enough leftover merchandise to keep such outlets running round the year. A luxury retailer may even consider destroying leftover inventory since the loss incurred will be less than the cost of damaging the brand image. One can only hope that the discount store format emerges as the preferred beat-therecession strategy in India.