admin

September 30, 2015

Raghavendra Kamath, Business Standard

Mumbai, 30 September 2015

It might not exactly be a battle zone, but the historic south

Mumbai neighbourhood of Fort recently witnessed a quiet retail

war. Not very far from the Bombay High Court runs a busy street

that leads to US coffee chain Starbucks’ first Mumbai store.

Situated near Horniman Circle, a stone’s throw from the Bombay

Stock Exchange, the store experienced quite a crowd when it first

opened. Along the usually crowded street leading up to it are

a dozen other shops that jostle for attention, among which is

a store that has shut down and whose signboard reads ‘The

Lounge’.

It might not exactly be a battle zone, but the historic south

Mumbai neighbourhood of Fort recently witnessed a quiet retail

war. Not very far from the Bombay High Court runs a busy street

that leads to US coffee chain Starbucks’ first Mumbai store.

Situated near Horniman Circle, a stone’s throw from the Bombay

Stock Exchange, the store experienced quite a crowd when it first

opened. Along the usually crowded street leading up to it are

a dozen other shops that jostle for attention, among which is

a store that has shut down and whose signboard reads ‘The

Lounge’.

It’s not unusual to see a shut store in Mumbai’s many

alleys and bylanes, but what’s interesting about this closed

outlet is that it used to be run by one of India’s oldest

and largest coffee chains — Café Coffee Day (CCD).

The story goes back to October 2012, when Tata Starbucks, an equal-stake

joint venture between Tata Global Beverages and Starbucks Corporation,

opened its first store in India in the aforementioned locality.

CCD, owned by VG Siddhartha, wanted to take the fight to the enemy

camp. The Lounge was one such format aimed at countering the sophisticated

look and feel of Starbucks.

The nearly 2,000 sq ft outlet clearly was no match for the global

coffee giant’s maiden store. While business picked up for

the new store, customers deserted CCD’s The Lounge, eventually

leading to its closure sometime in mid-2014. Although Starbucks

is a relative newbie on the Indian café circuit, its brand

recall and growing presence — over 75 outlets in two years

— is giving customers who grew up with CCD a chance to switch

loyalties.

Take Ratnesh Jain, 18, a college student who keeps track of every

penny he spends. Depending on how much time he has on his hands

and the location that is most convenient to him, Jain picks either

a CCD or Starbucks outlet to meet-up, although he says he clearly

prefers Starbucks, a departure from his choice in the past. “It’s

difficult to match the service and ambience of Starbucks. Not

just that, Starbucks delivers value for money in terms of a better

menu with larger and more delicious helpings, as compared with

CCD,” reveals Jain while sitting at a CCD store in upmarket

Colaba.

Jain goes on to explain, “For a very small portion of a

Dark Fantasy cake, CCD charges about Rs. 100, plus extra for toppings,

taking the entire bill to about Rs. 200. Starbucks, on the other

hand, charges around Rs. 200 for a similar dessert and offers

a much larger portion, complete with toppings.” Jain doesn’t

mind that CCD doesn’t offer him free Wi-Fi, although he feels

the pinch of the coffee and food not matching his palate. Many

others like Jain have developed a newfound loyalty for Starbucks,

where they say they find better service and ambience. “You

don’t mind paying more in return for better ambience, lively

atmosphere and an eclectic menu. CCD got lucky as it had a first-mover

advantage and customers did not have much choice back then,”

points out 20-year-old student Ketaki Sharma. She is a regular

at Starbucks and spends hours working on college projects there,

along with her classmates and friends.

Yet another Starbucks patron — 20-year-old Damini Kane —

says there is a clear difference between the service standards

of Starbucks and the rest of the café chains in India.

“CCD should certainly focus on improving its menu, becoming

more customer-friendly and, importantly, make its cafes more inviting,”

says Kane. At a Starbucks outlet, you might find everyone from

office-goers to students, tourists and the like making full use

of the uninterrupted free Wi-Fi.

In response, CCD tried to field the same proposition to draw

in customers and not all loyalists switched camps. Youngsters

like Pakhee Malhotra are clearly not buying into Starbuck’s

phoren halo. “Starbucks doesn’t sell good coffee. It

sells overpriced coffee. To pop about Rs. 200 for a Grande Caramel

Macchiato you must have a really rich dad. Hats off to you for

drinking away money like that,” writes Malhotra in an article

on iDiva. Though this counterpoint seems to favour CCD, in an

age of growing competition and fickle brand loyalty, it needs

to look at ways to fire up its brand pull and improve customer

satisfaction. While the café chain has its task cut out

when it comes to creating a great consumer experience, the 55-year-old

Siddhartha deserves accolades for the manner in which he built

— and, more importantly, ran profitably — an enviable

coffee business for the past two decades.

Freshly ground

The idea of setting up cafés was not even on the agenda for Siddhartha, the son of a coffee plantation owner who is married to the daughter of SM Krishna, the former chief minister of Karnataka. “Getting into the coffee business was incidental. We started off exporting coffee and realised two years later that it would not take us too far,” says the reclusive billionaire as he makes himself comfortable at the Lounge outlet at Nariman Point, the central business district of Mumbai. It was in 1994 that he came across an article on a German company called Tchibo, which started off as a 10×10 store in 1949 to finally emerge as a chain of coffee retailers and cafes.

“I was inspired by that and started with 20 stores in south

India selling coffee powder. In 1995, we decided to take the café

route, since there was a bigger opportunity for value addition

there. In the coffee powder business, the mark-up is 100%, while

in the café business it is as much as 800-900%,” points

out Siddhartha. Taking inspiration from how other international

brands went about building their businesses, Siddhartha and his

team started putting the company together.

While exports continue to be a part of the business, the coffee

arm today comprises a café network, which includes the

value format of CCD, The Lounge for trendy and affluent customers

and The Square for coffee connoisseurs. While Lounges (between

1,000 sq ft and 1,300 sq ft) and Squares (between 2,500 sq ft

and 3,000 sq ft) are located at expensive locations that attract

more affluent clientele, the CCD outlets are at more affordable

locations.

Besides, the company also sells vending machines to institutional

and individual clients, sets up kiosks and is selling brewed coffee

powder through Fresh & Ground branded outlets. (See: A distinct

flavour) When CCD entered Mumbai 14 years back, it opted for smaller

stores as the team wasn’t confident that the market was ready,

apart from the fact that rentals were too high even back then.

“Had we opened 1,500-sq ft stores in Mumbai at that time,

we would have gone bankrupt. Our key competitor at that time was

paying 70% of revenue only towards rent,” points out Siddhartha.

Interestingly, CCD did not opt for expanding through the franchisee

route and instead chose to spend its own capital. However, to

counter high rentals, it entered into revenue-sharing agreements

with corporates as well as fuel stations. At present, 25% of its

outlets are run on a revenue-share model.

“We have five to seven corporate relationships where we

only have revenue-sharing agreements. For them, CCD becomes a

complementary service,” mentions Siddhartha. Highlighting

the ownership approach, the company’s draft prospectus mentions

that complete ownership allows it to control all the operational

aspects of its café operations, thereby, ensuring that

it is able to deliver a consistent experience to its customers.

From a one-store-one-outlet (Coffee Day Cyber Café) format

in Bengaluru to around 1,500 stores, CCD today has a stranglehold

over the café market. Over the past two decades, quite

a few players have come in and set up shop, but none could match

the speed and scale at which CCD grew. Barista, which set up shop

in 2000, is a distant second with 169 outlets, followed by Costa

Coffee with 89 outlets.

Although Barista initially started operations with premium pricing, it rejigged its strategy mid-way, making its menu more affordable. But that has not worked for the coffee chain, which has already changed hands twice. The other fringe players in the café business include the California-based The Coffee Bean and Tea Leaf and home-grown Mocha. Australia’s Di Bella Coffee, which had a troubled presence in the country after exiting a JV in 2013, is now re-entering the market with a new licensee, Electel.

Putting CCD’s growth in perspective, Saloni Nangia, president,

market research, Technopak Advisors, says, “Café Coffee

Day had a very aggressive expansion strategy and it looked at

smaller cities, too. It did not limit itself and adapted formats

depending on the size of the location, thus, ending up in all

sorts of nooks and corners.”

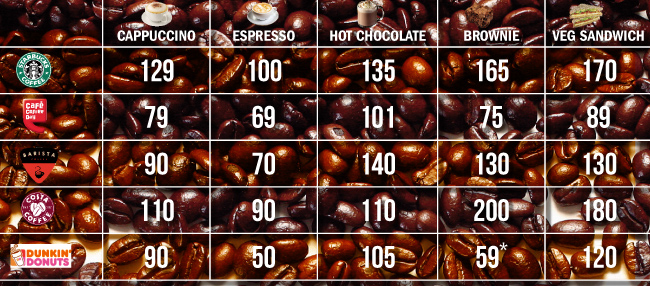

Pricing is another aspect that CCD built its plank on. For a

little perspective, a small portion of cappuccino at Starbucks

is priced at about Rs. 129, while it comes for Rs. 79 at a Café

Coffee Day outlet. A sandwich at Starbucks, however, costs no

less than Rs. 170, while at Café Coffee Day one can have

it for Rs. 89. Today, unlike Starbucks, the café network

has four different price points.

Pricing is another aspect that CCD built its plank on. For a

little perspective, a small portion of cappuccino at Starbucks

is priced at about Rs. 129, while it comes for Rs. 79 at a Café

Coffee Day outlet. A sandwich at Starbucks, however, costs no

less than Rs. 170, while at Café Coffee Day one can have

it for Rs. 89. Today, unlike Starbucks, the café network

has four different price points.

For instance, what it charges at an uptown Mumbai outlet will

be very different from what it charges in Navi Mumbai, a Greater

Mumbai Metropolitan suburb. On average, however, CCD is still

the cheapest among the café and quick service restaurant

(QSR) chains. “We are 57% cheaper than the competition. Will

they reduce prices by 40% and still be able to pay their rentals?”

quips Siddhartha. While he does have the upper hand over his rivals,

CCD has its own share of problems.

Storm in a coffee cup

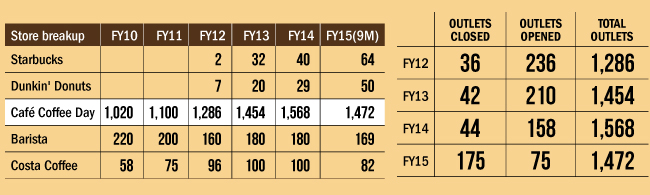

Over the past four years, the vertically integrated CCD has had to shut over 300 stores, even as it opened close to 700 stores over the same period. A record 175 outlets were closed in the nine months of FY15 alone . The company’s draft prospectus mentions that in 2014, it undertook a strategic review of its café network and decided to close certain cafés due to their smaller size, lower levels of performance and higher rentals on renewal of leases.

Putting the development in context, Siddhartha explains, “In Mumbai, 10-12 years ago, we took on lease 400 sq ft stores, which does not make much sense in today’s day and age. Also, ahead of the listing, we wanted to do a one-time clean-up.” Incidentally, amid the closures, CCD’s average sales per day (ASPD) per café grew by 3.9% from FY12 to FY13 and by 11% from FY13 to FY14, further increasing by 13% to Rs. 13,505 for the nine months of FY15.

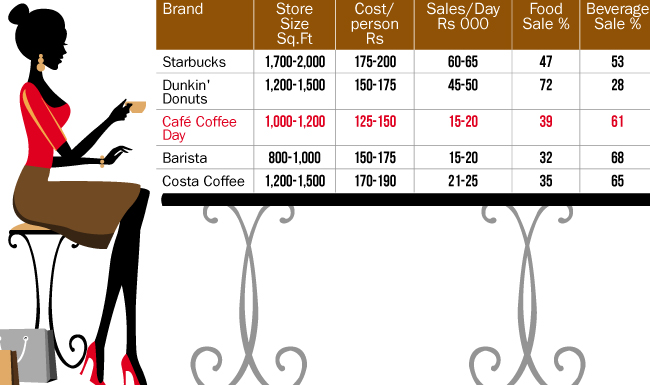

With an average store size of 1,700-2,000 sq ft and average spend

per person of Rs. 175-200, Starbucks delivers ASPD in the range

of rs. 60,000-65,000, nearly four times that of CCD and Barista

(See: Far from hot). Industry observers believe the spurt in CCD’s

average customer spend could partly be because of the high level

of closures in FY15 and the fact that it has opened just 79 outlets

in the nine months of FY15 against 158 for the whole of FY14.

With an average store size of 1,700-2,000 sq ft and average spend

per person of Rs. 175-200, Starbucks delivers ASPD in the range

of rs. 60,000-65,000, nearly four times that of CCD and Barista

(See: Far from hot). Industry observers believe the spurt in CCD’s

average customer spend could partly be because of the high level

of closures in FY15 and the fact that it has opened just 79 outlets

in the nine months of FY15 against 158 for the whole of FY14.

Siddhartha, however, is not giving up on his expansion plan.

The company plans to spend Rs. 88 crore from the proposed IPO proceeds

to set up 216 outlets and 105 kiosks by FY17. “The way I

see it, India can have thousands of stores on the highways at

our price point. On the Kanyakumari-Madurai highway, we have two

stores; between Goa and Mangaluru, we have three. That is a very

small number. We have sold 1.3 billion cups of coffee and tea

this year. Over the past five years, we have grown 30% in that

business. This is only the beginning of our growth story,”

he avers.

However, after getting aggressive with the Lounge and Square formats to take on Starbucks, Siddhartha had to scale back his plans as he found the move unviable. According to sources, around 2011, Siddhartha wanted to have 25% of CCD’s total outlets under the Lounge and Square formats. But by 2013, realising that the capex involved for both the formats was twice that of a regular CCD outlet, Siddhartha decided to change tack.

As a result, the Lounge format is restricted to 42 stores currently

and the Square format to just seven stores. Though Siddhartha

is a prudent competitor, what is helping him is that other café

players are happy playing second fiddle to CCD. “It is a

typical expansion curve. First, you aim for scale and brand recognition

and then focus on quality of profits as the model stabilises.

Our expansion is now value-based and profitability-centred. It

also has to do with market conditions and spending sentiment as

a whole,” says Virag Joshi, president and CEO, Devyani International,

which runs the Costa Coffee chain.

As a result, the Lounge format is restricted to 42 stores currently

and the Square format to just seven stores. Though Siddhartha

is a prudent competitor, what is helping him is that other café

players are happy playing second fiddle to CCD. “It is a

typical expansion curve. First, you aim for scale and brand recognition

and then focus on quality of profits as the model stabilises.

Our expansion is now value-based and profitability-centred. It

also has to do with market conditions and spending sentiment as

a whole,” says Virag Joshi, president and CEO, Devyani International,

which runs the Costa Coffee chain.

CCD, however, will have to counter competition that is slowly

building up from QSR players such as Dunkin’ Donuts and McDonald’s’

McCafe. Dunkin’ Donuts has opened 50 stores since its entry

in 2012. In case of McDonald’s, which introduced the McCafe

brand three years ago, the economics work out even better, as

the new brand is run from within the existing McDonald’s

outlet, thus saving on rentals.

Amit Jatia, vice-chairman, Westlife Development, the master franchisee

of McDonald’s in west and south India, says, “What works

for us is that we already have about 210 restaurants at prime

locations in the west and south markets, with about 50-odd McCafes

within them. What this format does is bring incremental revenue

for us without any extra real estate costs. We already have accessibility,

so what we are doing is introducing our customers to coffee and

subsequently ramping the business up.” McDonald’s plans

to take up the McCafe count to 70 by the end of FY16 and nearly

double that number in another two years.

Jatia acknowledges that the coffee business in India is nascent

but growing. What he’s betting on, however, is the potential

that the category promises. “The real café chain story

will unfold over the next two to three years. The market could

get polarised. McCafe is not just about coffee but doubles up

as a beverages platform for us as well, and we have to ramp it

up quickly,” he adds.

Just like McDonald’s, Jubilant Foodworks, which introduced

the Dunkin’ Donuts brand in India, sees the brand serving

the dual purpose of a QSR and a café chain. Dev Amritesh,

president and CEO, Dunkin’ Donuts, says, “We are in

a sweet spot between a QSR and a café. This kind of positioning

is very nascent and the opportunity to create an interesting experience

is immense. Donuts differentiate us from the rest — the product

has a strong novelty and pull factor. It complements the category,

which is important to the overall business.”

Gimme more

While no one can beat CCD in terms of its scale, with Starbucks, Dunkin’ Donuts and McCafe entering the picture, industry benchmarks have moved up significantly when it comes to customer experience. In other words, even as it has one eye on profits, Coffee Day Enterprises will have to ensure a greater consumer pull.

“It has scale but still needs to work on experience management, wherein similar customer experience is delivered across the chain. It remains to be seen how CCD will fare wherever it has multiple coffee and QSR chain brands around it,” feels Nangia.

Concurring with the view is Devangshu Dutta, chief executive, Third Eyesight, a retail consultancy. “A significant threat to older café chains lies within their own business. The biggest challenge in this sector is making sure that brand desirability, ubiquity and product-service consistency are balanced. Indian chains run the risk of becoming less desirable as compared with international brands, or may deteriorate in their product-service consistency with rapid growth.”

And while Starbucks with its limited presence may not be a challenge

for now, what it has done to the detriment of CCD is that it has

spoilt the consumer, especially the youth segment.

“Starbucks has made our customers more demanding. They want the experience of Starbucks at CCD prices. Today, 60% of CCD’s business is generated by repeat customers and 40% by new customers. The big challenge is getting the share of the 40% without losing the existing 60%,” says an ex-CCD employee. The challenge for Siddhartha in creating a greater consumer experience is multi-pronged, as it involves staff, the right menu mix and investing in a better ambience. Point to staff-related issues and Siddhartha says, “We have 13,500 people working for the brand. Yes, we have attrition, although employees at above-the-store level have stayed with us. At the top level, we have 700 people with an attrition of not more than 5-6%.” But the issue is with the front end, which deals with customers. “We interview 100 and shortlist 30, but at the end just 15 join us, and they, too, do not last for more than a year,” says an insider.

Siddhartha does not refute the observation. “For someone

earning Rs. 10,000 per month in Mumbai and having to travel two hours

to work, the quality of work is always a tricky issue. However,

training can make things better.” Initially, the staff was

trained for just six days, but over the past year-and-a-half,

the company has adopted a policy of retraining recruits a month

later, for another 10 days.

“We have a school in Bengaluru where 500 people are trained

each year. If we increase our training programme from six days

to three months, the quality will improve tremendously,”

opines Siddhartha.

When it comes to creating a good ambience, Siddhartha says that

in Mumbai alone, CCD has opened 20 stores of over 1,000 sq ft

each. “These stores have a better ambience and are as good

as any international cafés.”

Realising that existing cafés, too, would need sprucing

up, the chain is looking to spend Rs. 60 crore on refurbishment

of existing outlets, besides improving vending machines. The other

critical challenge that the chain needs to work on is the inconsistency

in the quality of its beverages and its limited food menu. In

the cafe´ market, beverages primarily dominate the stock

keeping unit and sales mix, given the nature of the coffee retail

space.

For CCD, beverages contribute 61% and the rest comes from food.

Starbucks, on the other hand, has an average beverage sales contribution

of 53% and the rest is food. In an earlier interaction with Outlook

Business, Avani Davda, CEO, Tata Starbucks, had mentioned, “Food

will definitely be a key part of our business here and it is something

we will focus on.” In fact, Taj Sats has helped the chain

develop a menu that keeps in mind local preferences. So, there’s

a cardamom-flavoured mawa croissant that Davda says has “done

quite well”, besides tandoori paneer roll, murgh kathi wrap

and chatpata paratha wrap, among others.

In the case of CCD, till two years back, food was sourced from 210 vendors and today, that number is down to just four. Siddhartha is clear about the revenue mix that he is comfortable with. “Food is complementary and we will do things like serving a cookie with a cappuccino. We want to keep that 60% intact. Food will never exceed 40% of our revenue.” Coming to inconsistency in terms of coffee taste, Siddhartha points that CCD sources handcrafted coffee, which makes the taste inconsistent. “A lot of companies have the technology for mechanised brewing. We, too, can manufacture our own machines and that can be done when we think we need to.”

If CCD has to increase its same-store sales growth and profitability, it will have to look at ways to offer consumers more menu options, especially at a time when expansion will eat into profits on account of depreciation. “Fundamentally, CCD will have to work on improving its billing value,” says Nangia.

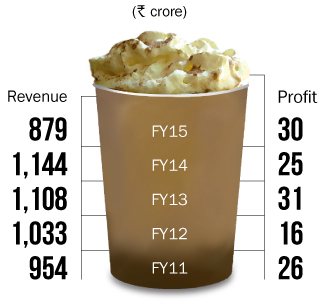

Given that the company reports profitability for the entire coffee segment, it’s not clear if the café business is profitable on a standalone basis. “Typically, 30% of CCD outlets bleed, 40% barely break even and the remaining 30% drive the business,” says a company source. In fact, profit from coffee and related businesses for FY14 was Rs. 25 crore, a decline of 19% from the same period a year ago, although it bounced back to Rs. 30 crore in the nine months of FY15.

Though coffee and allied businesses account for over 50% of revenue and are profitable, on a consolidated basis, the entity has been loss-making for the past three financial years — all through FY14 and in the subsequent nine months of FY15, with a consolidated debt of over Rs. 2,800 crore. Of this, the debt in the coffee retail business accounts for only Rs. 300 crore, of which the promoter plans to repay Rs. 125 crore.

The company, which counts KKR and Rakesh Jhunjhunwala among its

investors, aims to utilise Rs. 633 crore — about 55% of the

issue proceeds — towards partial repayment of loans availed

by the company and its subsidiaries and invest the balance towards

expansion of its coffee business. Jatia believes that the IPO

will help CCD keep its momentum going. “CCD has been a front-runner

for coffee in India. Once it has additional funds, it will be

able to reinvent itself,” he feels.

Clearly, Siddhartha realises that the café market might just be hitting escape velocity and he does not want to let go of the opportunity. “I would be kidding myself if I say I have got it 100% right. We realise we have made mistakes and will rectify that, although you must also look at great American brands and how they were placed when they were 20 years old,” smiles Siddhartha, as he eyes customers who have just made themselves comfortable at The Lounge.

(Published in Outlook Business.)