admin

July 13, 2026

Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT)

Bengaluru, 13 July 2026

India’s vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means.

For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives.

Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint the company would rather optimise for “quality selection” than chase ultra-fast deliveries, arguing that customers today are looking for reliable availability and curated choices rather than insisting on receiving products in 10 minutes.

Lightspeed-backed fashion startup Slikk is pursuing a similar path. Founder Akshay Gulati said the company’s focus since inception has been building a wide catalogue rather than aggressively acquiring users.

The shift comes as the sector enters a more pragmatic phase. Quick fashion startup Blip shut down within a year of launch last June, while rival Klydo has recently pivoted its business model, raising questions about the viability of firms in every category.

The crop of vertical quick commerce startups—focused on rapid delivery within a single, specific product category—has largely emerged over the past two years, inspired by the explosive growth of grocery-focused pioneers such as Blinkit, Swiggy Instamart and IPO-bound Zepto, which have accustomed consumers to receiving groceries and everyday essentials within minutes.

Other prominent startups include Plazza for quick delivery of medicines, Instafix for mobile repairs within minutes, and Dazzl for at-home salon services.

Kalaari Capital noted in its 2025 report that quick commerce had already captured about two-thirds of online grocery orders and around 10% of India’s overall e-retail spending in 2024, transforming consumer behaviour and building the infrastructure for specialised vertical players to emerge.

“Speed was never a real moat but became a hygiene factor once every significant player could promise 10-30 minute delivery,” said Devangshu Dutta, founder and chief executive of consultancy Third Eyesight. “Assortment depth, availability, trust, and sustained price-value have been, and will remain, the true differentiation levers. For categories such as medicines and baby products, credibility and compliance outweigh saved minutes, apart from urgent purchases.”

“Unit economics can become healthier only where there’s a clear reason for frequent and repeated purchases. Groceries and medicines are repeat, low consideration categories, while fashion is high consideration, driven by fit, styling and browsing. The best quick commerce categories have low or no returns and high order frequency, whereas rapid fashion delivery faces high return rates due to product mismatch against customer expectations (sizing, fit, fabric and colour),” Dutta said.

Different categories, different playbooks

While fashion startups are investing heavily in discovery and inventory refreshes, Ozi believes the opportunity in baby care lies in curation and premiumisation.

Sah said each sub-category within baby care presents a different operational challenge. Consumables require deep availability of long-tail brands, while fashion depends on filtering products for quality rather than listing everything available. Ozi, which delivers wipes, diapers, and baby food, deliberately curates brands instead of maximising assortment, targeting parents willing to pay slightly more for trusted products.

“The customer behaviour has shifted from discovery first to search first,” Sah said, adding that shoppers today are not necessarily looking for ultra-fast delivery, but nor are they willing to wait several days. “A modern-age customer values quality. They are happy to pay an 8-10% or 12% differential, but they need quicker access to better brands and better assortment.”

Fashion startups argue that their challenge is different altogether.

Gulati said Slikk has built its business around supply rather than customer acquisition, claiming that stronger assortment has helped steadily reduce acquisition costs. The company replaces 30-40% of inventory in every dark store each month and is expanding neighbourhood by neighbourhood instead of spreading rapidly across cities.

Slikk might also consider introducing private brands for apparel, given their higher margins, Gulati said.

Bengaluru-based fast-fashion e-commerce startup Knot, which raised $5 million from 12 Flags and Kae Capital in December 2025, is investing heavily in back-end technology. Its app captures user preferences through swipe-based interactions, while its dark stores carry much wider assortments than horizontal quick commerce operators – offering a vast, multi-category collection of goods – and customise inventory based on local demand.

“We look at fashion as a data science problem and not really an intuition problem,” co-founder and chief executive officer (CEO) Archit Nanda said.

Nanda said fashion’s long-tail nature—which relies on selling small quantities of several unique products rather than depending on a few popular items – means inventory commonality across dark stores is significantly lower than grocery, requiring specialised supply chains and hyperlocal merchandising.

The profitability test

The changing strategies also reflect growing investor scrutiny of unit economics.

Slikk’s Gulati said investors continue to back the category but increasingly want proof that businesses can balance growth with profitability rather than relying on heavy customer acquisition spending. He believes execution in neighbourhood-level operations, assortment and brand partnerships will ultimately determine the winner.

Knot’s Nanda said that fashion combines high average order values with healthy margins, making the category attractive despite its complexity.

However, analysts believe that not every vertical is equally suited to the model.

“Looking ahead, horizontal cross-subsidy will work better, with established, well-capitalised players (Myntra’s M-Now, Nykaa Now) including quick delivery into an existing catalogue and logistics network rather than building it standalone. For narrow, high-trust verticals (medicines, baby care) where the value is availability and authenticity rather than impulse, and where margins can support the delivery cost, quick commerce can work,” Dutta noted.

Kalaari Capital’s 2025 report on vertical quick commerce similarly argued that specialised players will win by solving category-specific pain points, with assortment depth, customer experience, and category expertise emerging as key differentiators.

(Published in MINT)

admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

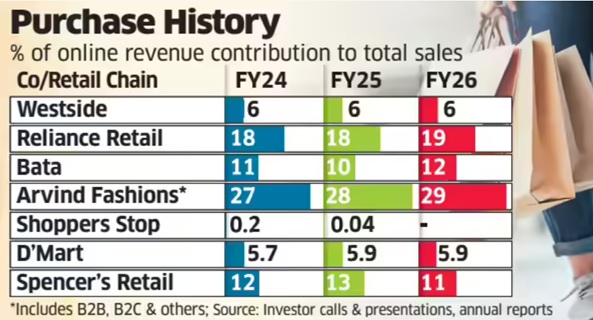

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

September 22, 2025

Christina Moniz, Financial Express

22 September 2025

It is already the largest player among organised fumiture makers with over 15% of the market. With 1,000 stores, it has the widest retail store footprint among organised players. The 102-year-old brand is also the second-largest revenue con-tributor to the parent enterprise.

So why is Interio tinkering with its name, logo and colour attributes?

“We want to move away from being viewed as a functional brand to more of a design-led lifestyle one. We have a wider range of offerings that are more modular and aesthetic,” says Reshu Saraf, head of marketing communications at Interio by Godrej.

As a first step, it has a new logo and name change – from Godrej Interio to Interio by Godrej. The brand has earmarked ₹50 crore towards an integrated campaign across TV, digital, outdoor and in-store branding to promote its new proposition over the next year. Overall, it will invest ₹300 crore in expansion and technology with the goal to more than double revenues to ₹10,000 crore by FY29.

Younger consumers don’t see furniture as utility but as lifestyle, observes Puneet Pandey, strategy head and managing partner, OPEN Strategy & Design. “By moving from ‘solid and sturdy’ to ‘stylish and aesthetic’, the brand earns the right to play at higher price points as well. Design-led positioning will also unlock repeat purchase since people no longer wait a decade to change their furniture based on utility; they want constant upgrades to refresh their living spaces as their tastes evolve,” he notes, adding that Interio needs to make the marketing leap from “catalogue to culture”.

Saraf says the brand is also building differentiation with its customer experience. “We’re using digital tools for store walkthroughs and visualisers to help visualise our products in the home. Our product portfolio, which is deeply personalised ane tailored for Indian sensibilities, it is a major differentiator that few other brands offer,” she points out.

E-commerce is also a focus area with the brand looking to increase the revenue share from 15% to 20-22% by 2029. The company is leveraging Al to improve the search functionand sharpen personalisation. Saraf adds the that offline too, the brand will have large format experience centres to help people envision what their rooms could look like, along with mid-size and small-format stores.

Interio also plans to widen its retail store footprint from 1,000 to 1,500 by 2029.

As per industry estimates, the Indian furniture market is set to grow at 11% annually to reach $64.1 billion by 2032 from $30.6 billion in 2025. It is this growth momentum that Interio is looking to cash in on.

Built-in differentiation

Although a significant chunk of Interio’s business comes from its home remodelling services, within the furniture category, it competes with global players like IKEA and digital-first brands like Pepperfry. The challenge for Interio in this market is to embed the design-led positioning in its productsandcus-tomer experience, says Nisha Sam-path, managing partner at Bright Angles Consulting.

One of its biggest advantages is the Godrej brand. “The Godrej brand stands for many values prized in interiors such as quality, trust, reliability and durability with a ‘Made in India’ tag. However, the brand has not been so successful in building an image of cutting-edge design and innovation. These are new values that can make the brand more contemporary,” she remarks.

Devangshu Dutta, CEO of Third Eyesight concurs, pointing out aside from nimble competition, Interio’s key challenges also come from the dual pressures of increasing consumer expectations for rapid delivery and customisation on the one hand, with aggressive price competition on the other.

(Published in Financial Express – Brandwagon)

admin

May 5, 2025

Mint, 5 May 2026

Priyamvada C., Sneha Shah

Urban India’s pet parents are driving a wave of investor interest in the pet care space. A clutch of startups such as Heads Up For Tails, Supertails, and Vetic are now in fundraising talks amid rising demand for premium products and services

While Supertails looks to raise about ₹200 crore by the end of this year, Heads Up For Tails is eyeing an investment from domestic investment firm 360 One Asset over the next few months, according to mul tiple people familiar with the matter.

Vetic, a tech-enabled chain of pet clinics, is looking to raise a sizeable round and has begun discussions with investors, they said, adding that some of these transactions may see existing investors part exit their stake.

Supertails and Vetic did not immediately respond to Mint’s requests for a comment. While 360 One declined to comment, Heads Up For Tails’ founder Rashi Narang denied the development.

Investor interest in pet care surged in the years following the pandemic, driven by a wave of new pet adoptions and rising disposable incomes. In 2023, pet care startups raised a record $66.3 million across 16 rounds, led by one major transaction ― Drool’s $60 million fundraise.

While 2023 saw a funding spike driven by Drool’s large deal, overall funding activity in 2024 was more broad-based, with fundraising at $17.9 million spanning 13 rounds, as per Tracxn.

“Pet ownership in India is estimated to be less than 10% of overall households, but growing at a rapid pace with rising incomes, especially among urban consumers. In developed economies, pet ownership can exceed three in four households, and that headroom for growth is reflected among the upper income segments in India,” said Devangshu Dutta, chief executive of Third Eyesight, a management consulting firm.

He added that urban couples and singles in many cases are even opting to become “pet parents” instead of having children.

Platforms such as Supertails, Drools and Heads Up For Tails have been the big beneficiaries of this shift. Drools raised $60 million from LVMH-backed private equity firm L Catterton in 2023, while Supertails raised $15 million led by RPSG Capital Ventures in February last year.

Similarly, Supertails, which is in talks to acquire Blue 7 Vets, a multi speciality veterinary clinic, as part of its strategy to expand offline, will also raise capital to fund the acquisition of new customers, investments in technology, and the expansion of healthcare services, including Super-tails Pharmacy and build an omni-channel experience for consumers.

The company raised about $15 million in its series B funding round last year led by RPSG Capital Ventures and existing investors Fireside Ventures, Saama Capital, DSG Consumer Partners and Sauce VC.

(Published in Mint)