admin

July 13, 2026

Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT)

Bengaluru, 13 July 2026

India’s vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means.

For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives.

Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint the company would rather optimise for “quality selection” than chase ultra-fast deliveries, arguing that customers today are looking for reliable availability and curated choices rather than insisting on receiving products in 10 minutes.

Lightspeed-backed fashion startup Slikk is pursuing a similar path. Founder Akshay Gulati said the company’s focus since inception has been building a wide catalogue rather than aggressively acquiring users.

The shift comes as the sector enters a more pragmatic phase. Quick fashion startup Blip shut down within a year of launch last June, while rival Klydo has recently pivoted its business model, raising questions about the viability of firms in every category.

The crop of vertical quick commerce startups—focused on rapid delivery within a single, specific product category—has largely emerged over the past two years, inspired by the explosive growth of grocery-focused pioneers such as Blinkit, Swiggy Instamart and IPO-bound Zepto, which have accustomed consumers to receiving groceries and everyday essentials within minutes.

Other prominent startups include Plazza for quick delivery of medicines, Instafix for mobile repairs within minutes, and Dazzl for at-home salon services.

Kalaari Capital noted in its 2025 report that quick commerce had already captured about two-thirds of online grocery orders and around 10% of India’s overall e-retail spending in 2024, transforming consumer behaviour and building the infrastructure for specialised vertical players to emerge.

“Speed was never a real moat but became a hygiene factor once every significant player could promise 10-30 minute delivery,” said Devangshu Dutta, founder and chief executive of consultancy Third Eyesight. “Assortment depth, availability, trust, and sustained price-value have been, and will remain, the true differentiation levers. For categories such as medicines and baby products, credibility and compliance outweigh saved minutes, apart from urgent purchases.”

“Unit economics can become healthier only where there’s a clear reason for frequent and repeated purchases. Groceries and medicines are repeat, low consideration categories, while fashion is high consideration, driven by fit, styling and browsing. The best quick commerce categories have low or no returns and high order frequency, whereas rapid fashion delivery faces high return rates due to product mismatch against customer expectations (sizing, fit, fabric and colour),” Dutta said.

Different categories, different playbooks

While fashion startups are investing heavily in discovery and inventory refreshes, Ozi believes the opportunity in baby care lies in curation and premiumisation.

Sah said each sub-category within baby care presents a different operational challenge. Consumables require deep availability of long-tail brands, while fashion depends on filtering products for quality rather than listing everything available. Ozi, which delivers wipes, diapers, and baby food, deliberately curates brands instead of maximising assortment, targeting parents willing to pay slightly more for trusted products.

“The customer behaviour has shifted from discovery first to search first,” Sah said, adding that shoppers today are not necessarily looking for ultra-fast delivery, but nor are they willing to wait several days. “A modern-age customer values quality. They are happy to pay an 8-10% or 12% differential, but they need quicker access to better brands and better assortment.”

Fashion startups argue that their challenge is different altogether.

Gulati said Slikk has built its business around supply rather than customer acquisition, claiming that stronger assortment has helped steadily reduce acquisition costs. The company replaces 30-40% of inventory in every dark store each month and is expanding neighbourhood by neighbourhood instead of spreading rapidly across cities.

Slikk might also consider introducing private brands for apparel, given their higher margins, Gulati said.

Bengaluru-based fast-fashion e-commerce startup Knot, which raised $5 million from 12 Flags and Kae Capital in December 2025, is investing heavily in back-end technology. Its app captures user preferences through swipe-based interactions, while its dark stores carry much wider assortments than horizontal quick commerce operators – offering a vast, multi-category collection of goods – and customise inventory based on local demand.

“We look at fashion as a data science problem and not really an intuition problem,” co-founder and chief executive officer (CEO) Archit Nanda said.

Nanda said fashion’s long-tail nature—which relies on selling small quantities of several unique products rather than depending on a few popular items – means inventory commonality across dark stores is significantly lower than grocery, requiring specialised supply chains and hyperlocal merchandising.

The profitability test

The changing strategies also reflect growing investor scrutiny of unit economics.

Slikk’s Gulati said investors continue to back the category but increasingly want proof that businesses can balance growth with profitability rather than relying on heavy customer acquisition spending. He believes execution in neighbourhood-level operations, assortment and brand partnerships will ultimately determine the winner.

Knot’s Nanda said that fashion combines high average order values with healthy margins, making the category attractive despite its complexity.

However, analysts believe that not every vertical is equally suited to the model.

“Looking ahead, horizontal cross-subsidy will work better, with established, well-capitalised players (Myntra’s M-Now, Nykaa Now) including quick delivery into an existing catalogue and logistics network rather than building it standalone. For narrow, high-trust verticals (medicines, baby care) where the value is availability and authenticity rather than impulse, and where margins can support the delivery cost, quick commerce can work,” Dutta noted.

Kalaari Capital’s 2025 report on vertical quick commerce similarly argued that specialised players will win by solving category-specific pain points, with assortment depth, customer experience, and category expertise emerging as key differentiators.

(Published in MINT)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

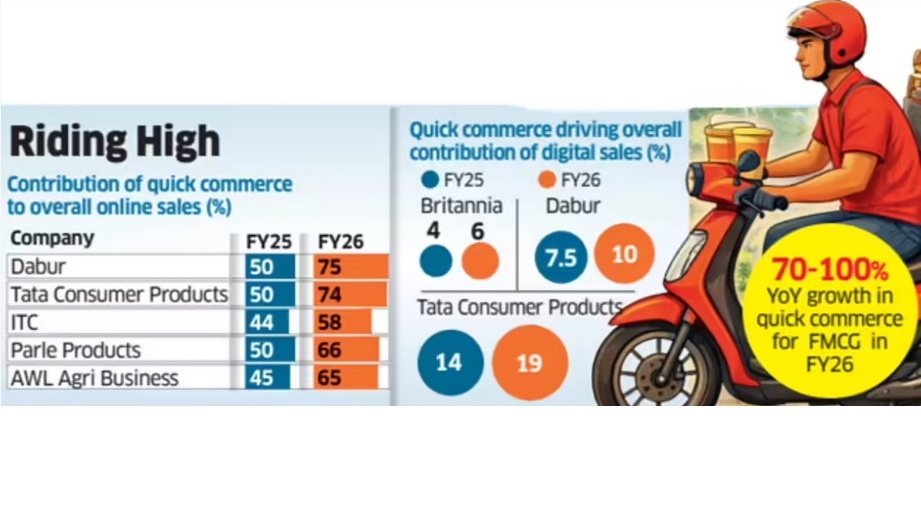

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 6, 2026

Vaeshnavi Kasthuril, MINT

Mumbai, 6 May 2026

Fashion retailers are speeding up deliveries to keep pace with instant-gratification shopping driven by quick-fashion startups, with established players and newer brands taking sharply different approaches.

For example, brands such as Biba and The House of Rare have adopted a more calibrated, infrastructure-led strategy rather than a rapid overhaul of existing store networks. “We’ve been doing this in a very soft way but not necessarily from the same stores because that affects the customer experience,” said Siddharth Bindra, managing director of Biba. Bindra said using retail stores as fulfilment hubs for rapid delivery creates operational constraints, particularly given store sizes and layouts. “We don’t have very large stores; they are anywhere between 1,000 and 2,000 square feet. So that’s not the right efficiency,” he said.

Instead, the brand is evaluating a hub-based model in cities with higher store density, enabling faster deliveries without disrupting stone operations. “If we do, it will be though proper hubs in cities where we have four to five stores, where we would start with quick commerce and accelerate it,” he said. This could enable same-day or two to three-hour deliveries.

The House of Rare, which houses Rare Rabbit (men’s urban fashion) and Rareism (women’s fashion), is adopting a similar approach, evaluating city-levee fulfilment hubs in markets with higher store concentrations to enable faster deliveries while keeping retail outlets focused on walk-in consumers.

The strategy reflects a broader attempt among legacy retallers to belance speed with experience, rather than treating stores as Interchangeable logistics nodes. “The eventual goal is the customer, but it creates a lot of difference in the customer experience” Bindra said, pointing to the trade-offs involved.

Different take

In contrast, some brands are moving more aggressively to integrate stones directly into fulfilment networks.

Libas, an initial public offering (IPO)-bound apparel company, is networking its operating model to plug its physical retail network Into a faster, hyperlocal delivery system.

Earlier, the 12-year-old company followed a more traditional structure. Online orders were largely fulfilled from central warehouses and delivered over a few days, while stores primarily served walk-in customers, with the two channels operating independently.

That is now changing. Libas is using its stores and nearby warehouses as local fulfilment points, allowing it to service orders within a much smaller delivery radius,

“At Libas, the time frame will be approximately 60-90 minutes at the max,” said Bhavay Pruthi, senior vice president, e-commerce and product management.

The rollout has been gradual, starting with select cities and limited catchments, typically within a 7-10km radius, where delivery timelines can be tightly controlled. It has also narrowed the product mix initialy to itams that are easier to move quickly.

The push comes as consumer expectations around delivery timelines extend beyond groceries into fashion, forcing brands to rethink supply-chain design,

Rise of quick fashion

The urgency to adapt is being shaped by a surge in quick fashion startups that are attracting investor attention despite heavy cash burm.

The segment has seen a flurry of funding in recent months, with Zilo raising $15.3 million in February led by Peak XV, and Knot securing $5 million in a round led by 12 Flags in December.

It has also evolved rapidly. Quick-commerce platforms such as Zepto, Instamart and Blinkit initially offered a limited range of basic fashion items for last-minute purchases. This has since expanded into a more specialized category, with vertical players offering wider assortments across party, work and occasion wear with rapid delivery timelines.

New entrants are pushing the model further. Wydo, for instance, promises deliveries within 15 to 30 minutes in Bengaluru, while Gen Z-focused offerings such as Newme’s Zip and Snitch Quick are building businesses around near-instant fashion access.

Myntra’s rapid commerce division, M-Now, accounted for about 10% of orders in the locations where it was available as of last November.

“This is the new kind of experience that customers are expecting,” Pruthi said.

Libas is working with third-party logistics providers and quick commerce platforms for the last-mile delivery, while focusing internally on faster picking, packing and order routing. Quick commerce currently accounts for about 2% of its overall sales, with scope to grow as the model scales..

Early results, however, highlight the trade-offs. “We saw very good sell-throughs for e-commerce, but it was cannibalizing existing store sales,” Pruths said.

There are also fimits to what customers are willing to buy through rapid-delivery channels. “Customers do not have the confidence to spend 15,000 for a fashion product from a quick- commerce channel,” he said.

To address this, Libas has tightened delivery radii, curated a more suitable product mix, and is testing stores with attached dark-store infrastructure to balance walk-in and online demand.

Experts say these challenges are structural.

“If you look at fashion, it’s extremely unpredictable, and if you are a brand across multiple products, it’s complicated process,” said Devangshu Dutta, founder of management consulting firm Third Eyesight.

While demand for faster deliveries is rising, it remains a small slice of the overall market, with profitability still uncertain due to limited assortments and high fulfilment costs. For traditional retailers, adopting the model requires a fundamental reworking of supply chains that were not built for near-instant delivery, Dutta added.

(Published in MINT)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

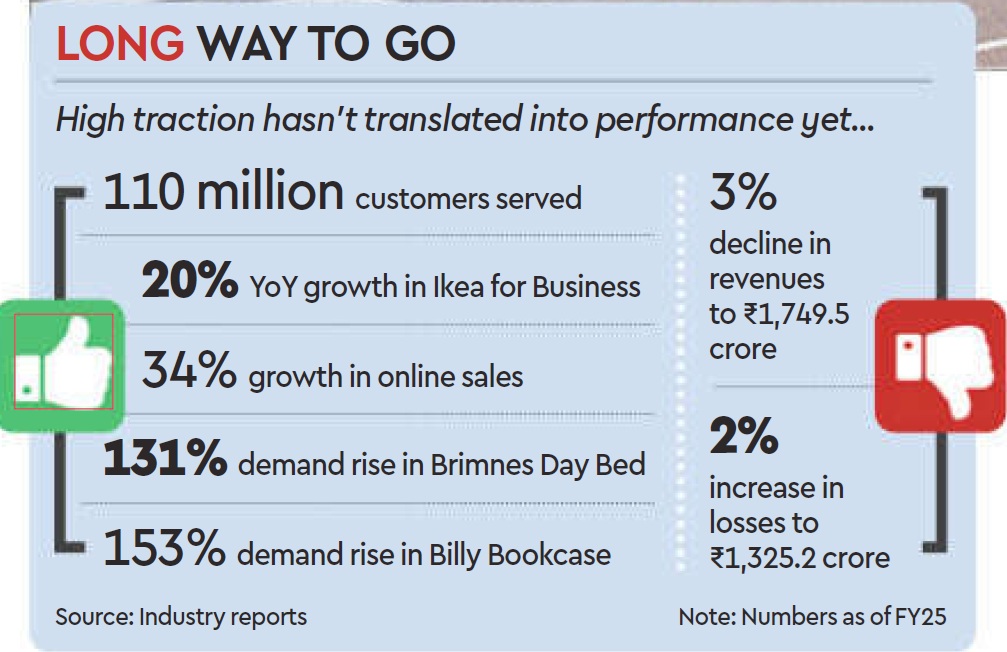

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

February 16, 2026

Christina Moniz, Financial Express (Brand Wagon)

16 February 2026

Starting this month global sportswear maker Nike shifted its e-commerce operations to beauty and fashion marketplace Nykaa to address poor logistics, high delivery times and inventory niggles. With Nykaa in charge, the brand said, customers can expect free shipping on all orders and faster deliveries rang ing from twotofour days depending on the location.

The change comes at a time when Nike is struggling to cope with declining market share and operational and supply-side issues in India. Its physical store count in the country has dropped by half in the past ten years to 100 from over 200 a decade ago. Nike in India undertook major restructuring of its business between 2016 and 2019, closing 35% of its stores in those three years to take a more digital-first approach.

It’s not all doom and gloom though. The brand reported a 14% growth in sales in the fiscal ending March 2025 to clock ₹1,380 crore. But it is well behind competing brands such as Puma (₹3,274 crore) and Adidas (₹3,114 crore), both of which have over 400 stores across the country.

Given India’s size, the competitive landscape and potential, treating it as a secondary export market to be serviced from Singapore was a poor decision on Nike’s part, says Devangshu Dutta, founder and CEO, Third Eyesight.

Nike’s alignment with a local player offers important strategic lessons for global brands with big ambitions in India, especially those in the ₹8,800 crore sportswear market. Brands that have not treated India as an afterthought have succeeded in creating sustained growth and market leadership, says Dutta.

“Most of Nike’s global competitors have treated India as a market high consequence. Nike might be the leader by global revenues, in India is smaller than its global rivals like Adidas, Puma and Skechers. ASICS has a smaller base but is growing at 30% while Lotto is also looking to grow its footprint massively, observes Dutta.

Ever since Nike’s digital-first pivot, its customers in the country have raised several complaints citing delivery failures and poor service, with some deliveries reportedly taking weeks. Its decision to transfer its digital operations to Nykaa in India could potentially address these missteps and reverse the breakdown of customer experience, say experts.

Changing course

“The recent move feels like Nike acknowledging that India cannot be treated as an extension of a global system. It needs local infrastructure, local partners, and a model built specifically for how Indians shop online. Partnering with Nykaa brings local execution muscle that is hard to replicate quickly,” observes Tusharr Kumar, CEO, Only Much Louder, adding that the move is a maturity moment for global brands. “Scale alone doesn’t guarantee success. What matters is adapting to local consumer behaviour, logistical realities and service expectations,” says Kumar.

That said, Nike’s shift won’t be without challenges. The biggest one will be balancing scale with brand control, notes Yasin Hamidani, director, Media Care Brand Solutions. “While Nykaa offers strong reach and trust, Nike will need to ensure its premium positioning, product storytelling, and customer experience don’t get diluted. If managed well, this move doesn’t necessarily hurt Nike’s brand,” he states.

However, he adds that competition like Adidas and Puma, with stronger on-ground retail and omnichannel presence, may gain an edge if Nike’s visibility or momentum slows. “The partnership with Nykaa must feel strategic and not like a retreat,” he cautions.

Given that Nykaa is also a marketplace for other activewear brands, it remains to be seen how the platform maintains Nike’s premium customer experience. “On its own platform, Nike could control everything from storytelling to checkout flows and post-purchase engagement. Nike will now need to adjust to sharing customer data, promotional calendars, and operational priorities with a partner platform,” says Somdutta Singh, founder & CEO at Assiduus Global, adding that striking the right balance between leveraging Nykaa’s scale and maintaining Nike’s distinctiveness will be key.

(Published in Financial Express – Brandwagon)