admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

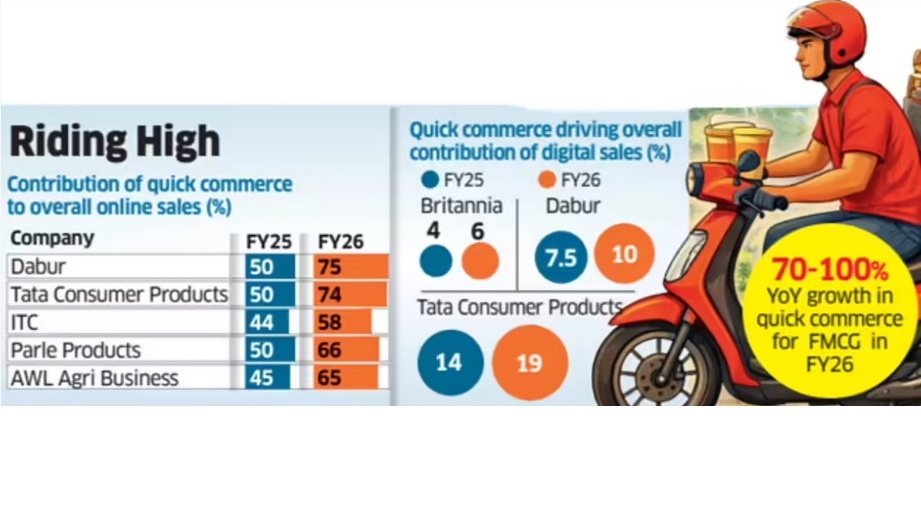

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 25, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 25 May 2026

Value fashion retailers across the country are likely to face margin pressure in the upcoming quarters as rising crude oil prices are driving up the cost of polyester and other fabrics. Executives at V-Mart Retail Ltd, Vishal Mega Mart Ltd, and Kewal Kiran Clothing Ltd (KKCL) said crude oil-linked inflation has begun to push up yarn and sourcing costs across apparel and general merchandise categories, with the full impact expected to play out over the next few months.

Value fashion retailers face a double whammy: their heavy reliance on polyester and synthetic blends exposes them to crude-linked inflation, while their price-sensitive customer base leaves little room to pass on rising costs without hurting demand.

Apparel contributes about 22.8% of the overall revenue of the country’s largest retailer, DMart, in FY26. Rising polyester and fabric prices could also weigh on this share, which has been declining since FY20.

“We see almost 60% to 70% consumption of polyester yarn or poly-based product lines, which have or will get impacted,” said Lalit Agarwal during the company’s March-quarter earnings call. Agarwal said that yarn prices had already risen sharply in recent weeks. “There is a rise of almost 10% to 15% in the yarn prices, which effectively converts to almost 5% to 7% in the apparel prices,” he said.

“Cost increases are at multiple points. One, of course, is raw material, which is not only fabric, but also polyester buttons, thread, packaging, all of that,” Devangshu Dutta, founder of Third Eyesight, a consulting firm, said. “Because with value, you cannot really pass on the price hikes so readily to the consumer.”

Dutta said that lower- and middle-income consumers were already under financial stress from broader inflationary pressures, “so, they will not be able to absorb price hikes as easily as well.”

Ebitda margins in Q4FY26 are 10.9% for V-Mart Retail, 13.6% for Vishal Mega Mart and 19.1% for Kewal Kiran Clothing.

Double whammy for value segment

Gunender Kapur, CEO of Vishal Mega Mart, during the company’s March-quarter earnings call, said the inflationary impact had started becoming visible towards the end of April and would likely intensify in the coming months.

Despite rising input costs, retailers said they are avoiding broad-based price hikes on entry-level products amid fragile demand conditions in the value segment.

Entry-level products for these retailers range from ₹199 to ₹399, with some going up to ₹1,500.

“We would never tinker with the opening price points and the lower price points in these difficult times, because those are the customers who are the most vulnerable in inflationary situations,” Kapur said.

Hemant Jain, CEO of KKCL, said the company was willing to absorb part of the pressure on profitability to protect revenues and market share.

Jain also said the company had not yet implemented price hikes despite the inflationary environment.

To cushion the impact, companies said they are increasingly relying on cost optimisation, fabric innovation, premium fashion products and deeper expansion into smaller towns to sustain growth.

V-Mart said it was attempting to offset part of the inflation through alternative fabric usage, sourcing efficiencies and tighter inventory planning.

The retailer has also blocked orders in advance and is utilising existing yarn and fabric inventories available with vendors to soften the immediate impact of rising prices.

Vishal Mega Mart’s Kapur said it has revived cost-saving measures from the post-Ukraine cotton inflation cycle, including replacing cartons with gunny bags, removing polybags from some apparel categories, and shipping footwear without outer cartons.

The retailer has also increased the use of computer-aided design systems to reduce fabric waste during cutting.

Premium products, private labels offer buffer

These value retailers are also increasingly depending on premium and higher-fashion assortments, where consumers are relatively less price sensitive, to absorb selective price increases while keeping entry-level products affordable.

Kapur said Vishal Mega Mart’s large private-label portfolio, which contributes over 74% of its revenue, gives it greater flexibility to manage pricing pressure while maintaining discounts against national brands.

KKCL on the other hand, said it would absorb part of the inflationary impact rather than immediately pass on higher costs to consumers.

These retailers are also increasingly leaning on expansion into smaller towns and deeper markets to drive incremental growth as discretionary spending in larger urban centres remains uneven.

Value fashion retailers have underperformed the broader market amid growing concerns over rising input costs and margin pressure. Shares of V-Mart Retail, V2 Retail Ltd, Vishal Mega Mart and Kewal Kiran Clothing have fallen between 4% and 11% on a year-to-date basis, while the benchmark BSE rose 6.1% during the same period.

(Published in MINT)

admin

May 15, 2026

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving “imported inflation” and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below):

1. Dual Impact on Industry and Consumers:

2. Vulnerability of Small Businesses (SMEs):

3. Income vs. Expenditure Strain:

4. Ripple Effect of Crude Oil Beyond Logistics:

5. Shifts in Consumer Spending Patterns & “Shrinkflation”:

The panel noted that while the Reserve Bank of India (RBI) has adequate foreign exchange reserves to defend the rupee temporarily, the definitive solution relies heavily on the cooling down of global geopolitical tensions (such as the Middle East conflict affecting the Strait of Hormuz). Until then, Indian consumers will need careful financial planning and smart spending adjustments to navigate this inflationary phase. [Video below.]

admin

May 6, 2026

Vaeshnavi Kasthuril, MINT

Mumbai, 6 May 2026

Fashion retailers are speeding up deliveries to keep pace with instant-gratification shopping driven by quick-fashion startups, with established players and newer brands taking sharply different approaches.

For example, brands such as Biba and The House of Rare have adopted a more calibrated, infrastructure-led strategy rather than a rapid overhaul of existing store networks. “We’ve been doing this in a very soft way but not necessarily from the same stores because that affects the customer experience,” said Siddharth Bindra, managing director of Biba. Bindra said using retail stores as fulfilment hubs for rapid delivery creates operational constraints, particularly given store sizes and layouts. “We don’t have very large stores; they are anywhere between 1,000 and 2,000 square feet. So that’s not the right efficiency,” he said.

Instead, the brand is evaluating a hub-based model in cities with higher store density, enabling faster deliveries without disrupting stone operations. “If we do, it will be though proper hubs in cities where we have four to five stores, where we would start with quick commerce and accelerate it,” he said. This could enable same-day or two to three-hour deliveries.

The House of Rare, which houses Rare Rabbit (men’s urban fashion) and Rareism (women’s fashion), is adopting a similar approach, evaluating city-levee fulfilment hubs in markets with higher store concentrations to enable faster deliveries while keeping retail outlets focused on walk-in consumers.

The strategy reflects a broader attempt among legacy retallers to belance speed with experience, rather than treating stores as Interchangeable logistics nodes. “The eventual goal is the customer, but it creates a lot of difference in the customer experience” Bindra said, pointing to the trade-offs involved.

Different take

In contrast, some brands are moving more aggressively to integrate stones directly into fulfilment networks.

Libas, an initial public offering (IPO)-bound apparel company, is networking its operating model to plug its physical retail network Into a faster, hyperlocal delivery system.

Earlier, the 12-year-old company followed a more traditional structure. Online orders were largely fulfilled from central warehouses and delivered over a few days, while stores primarily served walk-in customers, with the two channels operating independently.

That is now changing. Libas is using its stores and nearby warehouses as local fulfilment points, allowing it to service orders within a much smaller delivery radius,

“At Libas, the time frame will be approximately 60-90 minutes at the max,” said Bhavay Pruthi, senior vice president, e-commerce and product management.

The rollout has been gradual, starting with select cities and limited catchments, typically within a 7-10km radius, where delivery timelines can be tightly controlled. It has also narrowed the product mix initialy to itams that are easier to move quickly.

The push comes as consumer expectations around delivery timelines extend beyond groceries into fashion, forcing brands to rethink supply-chain design,

Rise of quick fashion

The urgency to adapt is being shaped by a surge in quick fashion startups that are attracting investor attention despite heavy cash burm.

The segment has seen a flurry of funding in recent months, with Zilo raising $15.3 million in February led by Peak XV, and Knot securing $5 million in a round led by 12 Flags in December.

It has also evolved rapidly. Quick-commerce platforms such as Zepto, Instamart and Blinkit initially offered a limited range of basic fashion items for last-minute purchases. This has since expanded into a more specialized category, with vertical players offering wider assortments across party, work and occasion wear with rapid delivery timelines.

New entrants are pushing the model further. Wydo, for instance, promises deliveries within 15 to 30 minutes in Bengaluru, while Gen Z-focused offerings such as Newme’s Zip and Snitch Quick are building businesses around near-instant fashion access.

Myntra’s rapid commerce division, M-Now, accounted for about 10% of orders in the locations where it was available as of last November.

“This is the new kind of experience that customers are expecting,” Pruthi said.

Libas is working with third-party logistics providers and quick commerce platforms for the last-mile delivery, while focusing internally on faster picking, packing and order routing. Quick commerce currently accounts for about 2% of its overall sales, with scope to grow as the model scales..

Early results, however, highlight the trade-offs. “We saw very good sell-throughs for e-commerce, but it was cannibalizing existing store sales,” Pruths said.

There are also fimits to what customers are willing to buy through rapid-delivery channels. “Customers do not have the confidence to spend 15,000 for a fashion product from a quick- commerce channel,” he said.

To address this, Libas has tightened delivery radii, curated a more suitable product mix, and is testing stores with attached dark-store infrastructure to balance walk-in and online demand.

Experts say these challenges are structural.

“If you look at fashion, it’s extremely unpredictable, and if you are a brand across multiple products, it’s complicated process,” said Devangshu Dutta, founder of management consulting firm Third Eyesight.

While demand for faster deliveries is rising, it remains a small slice of the overall market, with profitability still uncertain due to limited assortments and high fulfilment costs. For traditional retailers, adopting the model requires a fundamental reworking of supply chains that were not built for near-instant delivery, Dutta added.

(Published in MINT)

admin

May 2, 2026

Neethi Lisa Rojan, Mint

2 May 2026, Mumbai

Fast-moving consumer goods makers are leaning on a mix of price increases, smaller pack sizes and tighter cost controls to navigate raw-material volatility triggered by the ongoing US-Iran war, while still reporting robust volume growth for the March quarter. The ongoing war blew up end February this year, disrupting global supply chains.

Executives at top firms said calibrated pricing and ‘shrinkflation’ are helping them protect margins. The trend shows staples demand have held up, but also points to a gradual pass-through of higher commodity and packaging costs to consumers as geopolitical disruptions keep input prices elevated.

At Hindustan Unilever Ltd, the strategy is already in motion. The company has implemented calibrated price hikes and adjusted grammage across products. “We are taking calibrated pricing action in the range of 2-5%,” chief financial officer Niranjan Gupta said in a post-earnings briefing on Thursday. “We use a combination of both the put-down price as well as optimizing the fill levels,” said Gupta. The management also noted that its products in the homecare segment such as soaps (Lux, Pears, Dove, etc.) and detergents (Surf Excel, Rin, etc.) will be the first to be affected by price hikes. Interestingly, this happened at a time when HUL’s volumes grew the fastest in 15 quarters.

Companies have anticipated how consumers will behave.

“In times of inflation, income uncertainty, etc. essentials such as packaged foods, biscuits, and household cleaning products tend to see trade-down behaviour rather than outright disappearance of demand,” said Devangshu Dutta, founder of management consultancy, Third Eyesight. “Consumers tend to shift to smaller pack sizes or private labels, rather than abandoning categories altogether,” he adds.

India’s retail inflation rose from 2.75% in January 2026 to a 10-month high of 3.40% in March, driven largely by food prices.

That balance between pricing and demand is playing out across the sector. Nestle S.A., the parent company of the Indian entity said it saw 3.5% organic sales growth during the quarter, with RIG (real internal growth or volume growth) of 1.2% and pricing of 2.3% in the January-March quarter.

“The conflict in the Middle East will have some impact on commodity and distribution costs, and possibly on consumer behavior. But it’s too early to know the full extent of this,” chief executive officer at Nestlé S.A, Philipp Navratil said in the analyst call after the results. Its India unit, Nestlé India, reported its strongest quarterly growth in nearly a decade, led by double-digit volume expansion.

HUL reported a 21% year-on-year rise in consolidated net profit to ₹2,994 crore, while Nestle India saw net profit up 27% at ₹1,110.9 crore. year-on-year to ₹1,110.9 crore in Q4 FY26. HUL has also retained its medium-term guidance for earnings before interest, taxes, depreciation, and amortization (Ebitda) at 22.5%-23.5%.

The resilience in volumes comes even as input costs surge. Prices of crude oil-linked materials, especially packaging, have risen sharply following disruptions around the Strait of Hormuz chokepoint. High-density polyethylene, widely used in packaging, jumped about 42% in March from the previous month.

Multinationals are already bracing for the fallout. Tide and Gillette maker Procter & Gamble, said in its quarterly earnings call that it could take roughly a $1 billion post-tax hit to its fiscal 2027 profit from surging oil prices. Still, not all inputs are moving in tandem. Prices of staples such as wheat, sugar, tea and coffee have remained relatively stable, offering some cushion. Edible oils, however, remain a concern.

Palm oil, a critical input in many FMCG products, is seeing supply shifts, as producers such as Malaysia and Indonesia divert output toward biodiesel. AWL Agribusiness, which sells Fortune oil, said in the quarterly analyst call that edible oils faced a 10% price surge in March, which has already been passed to consumers. The company expects to pass on the rise in packaging material prices also soon. The company posted a 53% jump in consolidated net profit to ₹292 crore in Q4FY26, from ₹190 crore a year earlier.

Experts expect the trend of margin-saving strategies to continue.

“Depending on the product, category and brand, we will see a mix of price hikes, shrinkflation and rationalization of SKUs (stock keeping units), and also a shift from brand-related to tactical advertising and promotional spends to boost short-term demand,” Dutta said.

Elsewhere, companies are acknowledging broad-based inflation but are continuing to push through growth. Bajaj Consumer Care reported near double-digit volume gains even as managing director Naveen Pandey noted that “nearly 100%” of its cost base is under inflation. The company plans further pricing actions alongside cost optimization. Bajaj Consumer Care’s net profit for the March quarter more than doubled to ₹63.6 crore from a year ago.

Beyond the basics

The ripple effects extend beyond staples. Fashion, lifestyle and grocery retailer Trent Ltd flagged uncertainty around supply chains and inflation, warning of potential implications for near-term demand. “Duration and intensity of disruptions in the Middle East, along with its second order effect on supply chain, commodity prices and inflation in general has potential implications for near-term demand,” the company said in its results presentation.

Meanwhile, consumer appliance maker Havells India has initiated price increases after what chairman Anil Rai Gupta described as an unprecedented escalation in input costs. “I’ve not seen this kind of a price escalation in the recent past in the recent memory,” he said in the post results analyst call.“ Calibrated price actions have been initiated, he said. Havells India reported a strong 40% year-on-year increase in net profit to ₹723 crore in the March quarter.

More clarity may emerge as additional earnings roll in. Companies with higher exposure to West Asia, such as Dabur and Emami, are yet to report results and could face greater consolidated impact due to regional disruptions. “Companies such as Dabur and Emami will be more affected at the consolidated level due to issues in the MENA or Middle East and North Africa Region (6-8% revenue salience),” said analysts at Motilal Oswal Financial Services ahead of the earnings season.

For now, inventory buffers are offering temporary relief. Some companies have built raw-material stockpiles lasting up to six months, helping them absorb immediate shocks. “In our international markets, our effect will be in the raw material, practically zero to a couple of points maybe because we are well-stocked not just for this quarter, but the next quarter also. We normally carry six months inventory in international,” said Raj Pal Gandhi, whole-time director at Varun Beverages, the largest bottler of Pepsico in India, in the quarterly analyst call. This has helped the firm tide over the challenges in plastic shortage faced in March.

However, companies will now have to buy raw materials at higher prices, leaving room open for more price hikes.

(Published in MINT)