admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

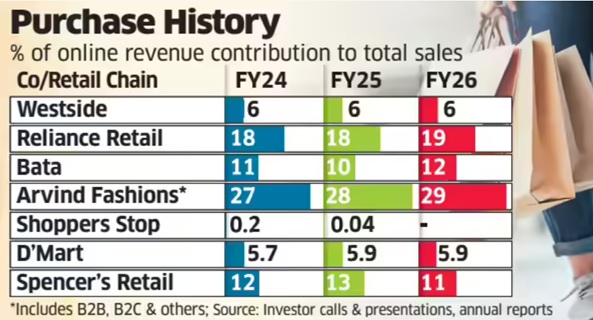

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

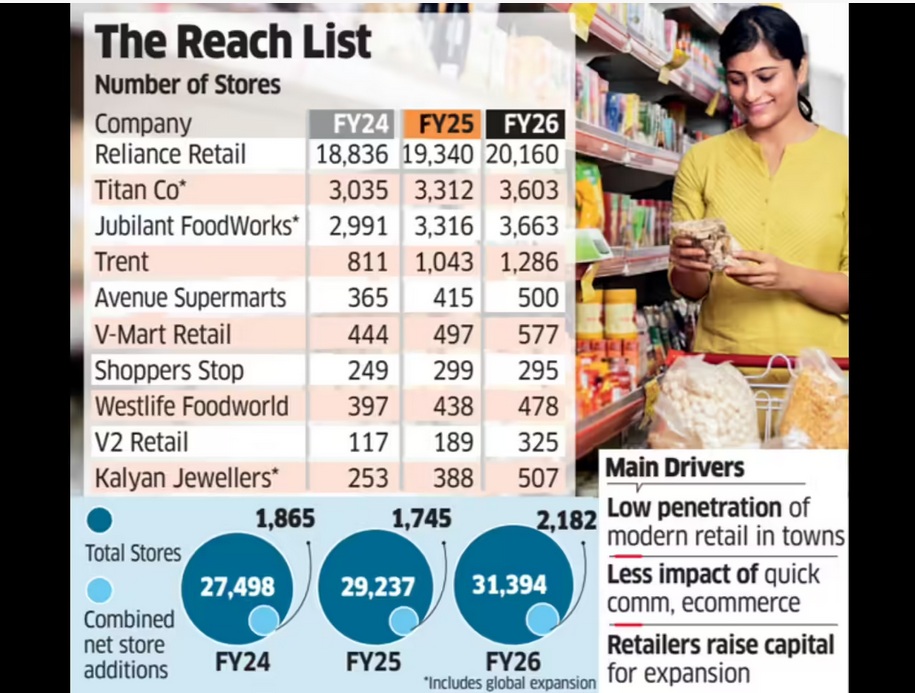

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

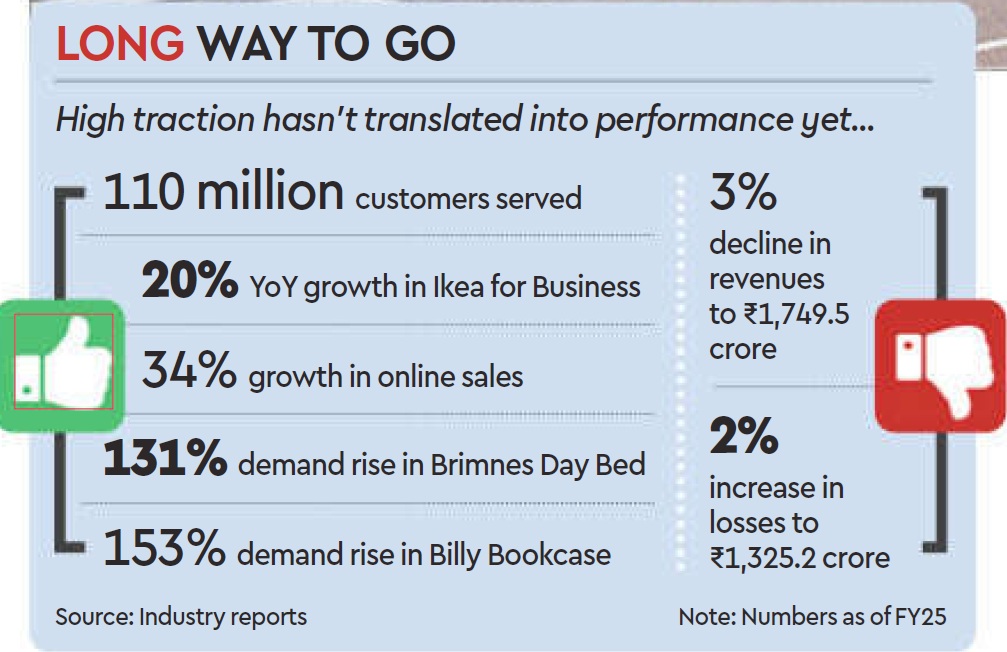

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

December 29, 2025

Yash Bhatia, Impact Magazine

29 December 2025

App, Tap, Pay and Zoom it’s delivered – that is Quick commerce for you. And in India, the narrative has so far been defined by speed, scale, high SKU counts, and the dominance of dark stores. Last week, however, Instamart nudged that model by opening an experiential store in Gurugram, allowing consumers to see and feel select products available on the platform.

The Bengaluru-based company has positioned the outlet not as a conventional retail store, but as a compact experiential format with a sharply curated assortment of around 100–200 SKUs, compared to the 15,000–20,000 SKUs typically housed in a dark store. Spanning roughly 400 sq. ft., the space is about one-tenth the size of a standard 4,000 sq. ft. dark store.

Under this model, sales proceeds are paid directly to sellers. This differs from Instamart’s regular arrangement, where payments are routed through the platform and later settled with sellers after deducting the platform’s share. IMPACT reached out to Instamart for further details, but the company declined to comment.

Sources close to the development say that Instamart has enabled sellers to open branded experiential stores in and around residential societies as part of a targeted consumer experiment. These are not conventional retail outlets, but compact experiential formats with a highly curated SKU assortment, focused on categories where consumers prefer to assess the products first-hand before purchasing, such as fresh fruits, vegetables, pulses, new product launches, and selected D2C brands. The initiative is largely centred on fresh categories and allows sellers to experiment with Instamart’s branding and service ecosystem.

Devangshu Dutta, Founder, Third Eyesight, a retail consultancy firm, says that physical presence plays a vital role in anchoring trust, particularly in premium products, groceries, and fresh produce. “Experiencing a product or brand physically can significantly enhance perceived value and help create stickiness. For this reason, offline stores continue to remain integral to the consumer products sector,” he explains.

Built on the promise of speed and convenience, quick commerce brands have come under growing scrutiny for quality and hygiene lapses at dark stores. Over the past year, several reports have flagged issues ranging from poor storage conditions and compromised freshness to the sale of expired or damaged products, particularly in food and grocery categories.

In some instances, regulatory inspections have led to licence suspensions after authorities identified hygiene violations at fulfilment centres. “Trust is what builds loyalty, and the shift is clearly moving from minutes to confidence,” says Shankar Shinde, Co-Founder, Aisles and Shelves, a behaviour-led brand consultancy in India. Shinde adds that the emergence of offline formats such as Instamart’s physical store aligns with this transition, particularly in grocery and fresh categories where consumers place a high premium on quality and consistency. “Physical touchpoints help reduce consumer anxiety, especially in a market like India, where shoppers still prefer hand-picked fresh produce such as fruits and vegetables,” he explains.

Against this backdrop, the opening of experiential centres could emerge as one way for quick commerce players to rebuild consumer trust by allowing shoppers to experience products in person before purchasing. IMPACT also reached out to Blinkit and Zepto for their views, but both declined to comment.

Kushal Bhatnagar, Associate Partner, Redseer Strategy Consultants, believes the move is aimed at unlocking incremental growth by tapping into offline-first consumers who are not yet active on quick commerce, while also catering to the offline purchase missions of existing quick commerce users. He notes that quick commerce currently reaches only about 75–80 million annual transacting users as of CY2025, even as over 90% of India’s grocery consumption continues to take place offline.

Beyond expanding reach, Bhatnagar sees offline formats as a way to address deeper trust barriers within the category. He adds that such formats can help deepen consumer confidence, particularly in categories where apprehensions around quality and freshness persist in quick commerce deliveries, concerns that are partly alleviated when consumers can experience products first-hand. Additionally, he points out that this approach benefits brands, especially emerging ones that are largely confined to quick commerce or a limited set of platforms, by giving them greater physical retail visibility without requiring heavy investment in traditional distribution networks.

Viewed through a financial lens, the move also carries implications for how quick commerce platforms justify value. Saurabh Parmar, fractional CMO, believes the initiative signals a shift from promise to performance, with a stronger emphasis on optimisation and a more realistic assessment of long-term value creation. He notes that while quick commerce has expanded into Tier 2 markets and seen growth in user numbers, these metrics alone still fall short of fully justifying current valuations. In this context, an offline presence becomes another lever to strengthen the overall business case.

At the same time, Parmar cautions that offline formats cannot replace the core proposition of quick commerce. He adds that experiential centres enhance brand credibility and make quick commerce feel closer to conventional retail, with the potential to eventually extend into other facets of e-commerce. However, he emphasises that quick commerce must continue to remain the frontline, as the sector’s valuations are fundamentally anchored in its speed-led proposition.

Retail experts, meanwhile, view physical touchpoints as a long-standing mechanism for building trust rather than a structural shift.

Dutta adds that such formats complement existing digital trust mechanisms such as delivery consistency, speed, ratings, and reviews by making brands feel tangible and accountable rather than abstract.

Bhatnagar notes that quick commerce currently has an average monthly transacting user base of around 40 million as of CY2025, leaving significant headroom for growth when compared to India’s overall e-commerce base of nearly 300 million active transacting users.

Beyond expanding the user base, he adds that experiential stores can also support wallet-share expansion across categories, which remains a key growth lever for the sector. “Non-grocery segments such as beauty and personal care, electronics, and fashion currently contribute about 25% of quick commerce GMV (Gross Merchandise Value), a share that is expected to rise further. Within groceries as well, platforms can drive incremental growth by building greater depth in fresh produce and staples,” Bhatnagar highlights.

From an operational perspective, however, the offline format is viewed more as a supporting layer than a core growth engine. Dutta sees Instamart’s offline presence as an experimental add-on rather than a replacement for its delivery-led model. The operating processes and economics differ significantly from those of quick commerce delivery, positioning physical formats as a complement to the speed proposition rather than an alternative. If the model proves viable and is backed by sufficient resources, it could eventually lead to a parallel scale-up of dark stores and experiential formats across different catchments.

For now, Instamart’s offline foray remains a tightly scoped experiment rather than a strategic pivot. Its significance lies less in square footage and more in what it signals about the evolving priorities of quick commerce. As the category matures, speed alone may no longer be sufficient to secure trust, loyalty, or long-term value. Experiential touchpoints, if deployed selectively, could help platforms bridge the gap between digital convenience and physical reassurance, particularly in categories where quality perception continues to remain fragile.

(Published in IMPACT)