admin

July 13, 2026

Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT)

Bengaluru, 13 July 2026

India’s vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means.

For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives.

Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint the company would rather optimise for “quality selection” than chase ultra-fast deliveries, arguing that customers today are looking for reliable availability and curated choices rather than insisting on receiving products in 10 minutes.

Lightspeed-backed fashion startup Slikk is pursuing a similar path. Founder Akshay Gulati said the company’s focus since inception has been building a wide catalogue rather than aggressively acquiring users.

The shift comes as the sector enters a more pragmatic phase. Quick fashion startup Blip shut down within a year of launch last June, while rival Klydo has recently pivoted its business model, raising questions about the viability of firms in every category.

The crop of vertical quick commerce startups—focused on rapid delivery within a single, specific product category—has largely emerged over the past two years, inspired by the explosive growth of grocery-focused pioneers such as Blinkit, Swiggy Instamart and IPO-bound Zepto, which have accustomed consumers to receiving groceries and everyday essentials within minutes.

Other prominent startups include Plazza for quick delivery of medicines, Instafix for mobile repairs within minutes, and Dazzl for at-home salon services.

Kalaari Capital noted in its 2025 report that quick commerce had already captured about two-thirds of online grocery orders and around 10% of India’s overall e-retail spending in 2024, transforming consumer behaviour and building the infrastructure for specialised vertical players to emerge.

“Speed was never a real moat but became a hygiene factor once every significant player could promise 10-30 minute delivery,” said Devangshu Dutta, founder and chief executive of consultancy Third Eyesight. “Assortment depth, availability, trust, and sustained price-value have been, and will remain, the true differentiation levers. For categories such as medicines and baby products, credibility and compliance outweigh saved minutes, apart from urgent purchases.”

“Unit economics can become healthier only where there’s a clear reason for frequent and repeated purchases. Groceries and medicines are repeat, low consideration categories, while fashion is high consideration, driven by fit, styling and browsing. The best quick commerce categories have low or no returns and high order frequency, whereas rapid fashion delivery faces high return rates due to product mismatch against customer expectations (sizing, fit, fabric and colour),” Dutta said.

Different categories, different playbooks

While fashion startups are investing heavily in discovery and inventory refreshes, Ozi believes the opportunity in baby care lies in curation and premiumisation.

Sah said each sub-category within baby care presents a different operational challenge. Consumables require deep availability of long-tail brands, while fashion depends on filtering products for quality rather than listing everything available. Ozi, which delivers wipes, diapers, and baby food, deliberately curates brands instead of maximising assortment, targeting parents willing to pay slightly more for trusted products.

“The customer behaviour has shifted from discovery first to search first,” Sah said, adding that shoppers today are not necessarily looking for ultra-fast delivery, but nor are they willing to wait several days. “A modern-age customer values quality. They are happy to pay an 8-10% or 12% differential, but they need quicker access to better brands and better assortment.”

Fashion startups argue that their challenge is different altogether.

Gulati said Slikk has built its business around supply rather than customer acquisition, claiming that stronger assortment has helped steadily reduce acquisition costs. The company replaces 30-40% of inventory in every dark store each month and is expanding neighbourhood by neighbourhood instead of spreading rapidly across cities.

Slikk might also consider introducing private brands for apparel, given their higher margins, Gulati said.

Bengaluru-based fast-fashion e-commerce startup Knot, which raised $5 million from 12 Flags and Kae Capital in December 2025, is investing heavily in back-end technology. Its app captures user preferences through swipe-based interactions, while its dark stores carry much wider assortments than horizontal quick commerce operators – offering a vast, multi-category collection of goods – and customise inventory based on local demand.

“We look at fashion as a data science problem and not really an intuition problem,” co-founder and chief executive officer (CEO) Archit Nanda said.

Nanda said fashion’s long-tail nature—which relies on selling small quantities of several unique products rather than depending on a few popular items – means inventory commonality across dark stores is significantly lower than grocery, requiring specialised supply chains and hyperlocal merchandising.

The profitability test

The changing strategies also reflect growing investor scrutiny of unit economics.

Slikk’s Gulati said investors continue to back the category but increasingly want proof that businesses can balance growth with profitability rather than relying on heavy customer acquisition spending. He believes execution in neighbourhood-level operations, assortment and brand partnerships will ultimately determine the winner.

Knot’s Nanda said that fashion combines high average order values with healthy margins, making the category attractive despite its complexity.

However, analysts believe that not every vertical is equally suited to the model.

“Looking ahead, horizontal cross-subsidy will work better, with established, well-capitalised players (Myntra’s M-Now, Nykaa Now) including quick delivery into an existing catalogue and logistics network rather than building it standalone. For narrow, high-trust verticals (medicines, baby care) where the value is availability and authenticity rather than impulse, and where margins can support the delivery cost, quick commerce can work,” Dutta noted.

Kalaari Capital’s 2025 report on vertical quick commerce similarly argued that specialised players will win by solving category-specific pain points, with assortment depth, customer experience, and category expertise emerging as key differentiators.

(Published in MINT)

admin

July 9, 2026

Neethi Lisa Rojan & Vaeshnavi Kasthuril, MINT

Mumbai/Bengaluru, 8 July 2026

The collapse of the US-Iran peace deal in less than a month has rattled India’s consumer sector, reviving fears that higher oil prices and fresh supply-chain disruptions could squeeze demand just as companies were betting on a broader recovery.

The renewed uncertainty followed US President Donald Trump’s declaration on Wednesday that the peace deal with Iran was effectively over, alongside Washington’s decision to end a sanctions waiver on Iranian energy supplies. The market reaction was swift. The Nifty FMCG Index fell 2.49% on Wednesday, underperforming the broader market as all 15 constituents declined, led by Dabur India, Hindustan Unilever, and Tata Consumer Products, whose shares fell 3-4% each. The benchmark Nifty50 ended 2.12% lower after renewed hostilities in West Asia pushed crude prices higher.

Executives and analysts said companies have little room to respond immediately, leaving them to closely monitor devel opments as risks to costs and consumer spending mount. “I don’t think companies can react on this kind of a short notice,” said Arvind Singhal, chairman of consulting firm The Knowledge Company. “It takes 2-6 months to make any change in your plans and strategy. I think right now the Indian FMCG (fast moving consumer goods) companies will be watching the progress of monsoon more carefully than the Strait of Hormuz.”

Even after the US-Iran peace deal took effect on 18 June, consumer companies were unlikely to have expected immediate relief, analysts said.

“While everyone hoped for a cessation in hostilities, smart management teams would work on the realistic expectation that even with a ceasefire, pent-up supply chain input costs need to be absorbed over time, and pricing plans must be factored accordingly,” Devangshu Dutta, founder and chief executive of consulting firm Third Eyesight, said.

“Given that the conflict zone is active, I don’t think there is any immediate likelihood of pricing freeze or reductions, even though demand in rural areas as well as in lower-income urban segments is likely to be hit from both sides ― earnings and expenses.”

Large consumer goods companies including Dabur, Emami and Godrej Consumer had recently told investors they remained confident about consumer demand, including in rural markets.

But the renewed rise in crude prices, coupled with erratic monsoons marked by rainfall deficit in some regions and flooding in others, threatens to complicate that outlook. Higher fuel costs could lift prices of crude-linked raw materials such as plastic packaging and ingredients used in soaps and creams, while persistent inflation could push consumers to cut discretionary apne ding and trade down even on staples.

Major consumer companies had already raised prices or reduced grammage across packaged food, beverages and personal care products in the March quarter.

“As far as the crude prices are concerned, that is probably the only variable where the government has to decide as far as pricing of crude or the petroleum in India is concerned,” Singhal said.

That comes at an awkward time for India’s largest consumer companies, including Hindustan Unilever, which had earlier this year told analysts they intended to drive growth through higher volumes rather than price increases. A renewed bout of inflation could undermine that strategy.

(Published in MINT)

admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

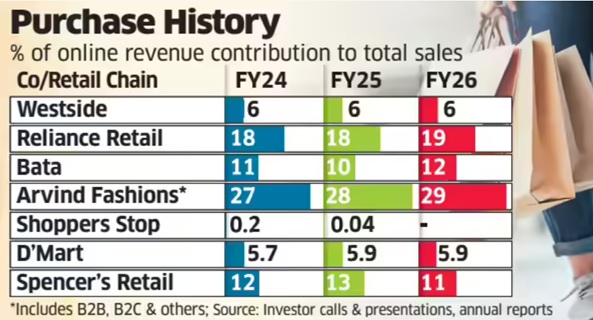

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 27, 2026

Kartikey Kashyap, Financial Express

27 May 2026

Three campaigns took home the Grand Prix awards from Goafest this year: Kansai Nerolac Paints”The Barefoot Journey” by Tribes Commu-nication in the Media category; Mountain Dew’s “Darescore” by Leo in Digital & Technology; and Center fruit (Perfetti Van Melle India)” Kaisi Jeebh Laplapayee”” by Perfetti’s in-house team in the Best Use of Voice/Technology category.

All three were exceptionally creative and scored high on likeability and novelty. There was another common element that tied the three together: How they used creativity to solve real brand problems.

Take PepsiCo’s Mountain Dew Darescore campaign. Nepal’s tourism economy relies heavily on mountaineering, but over 90% of global tourist revenue flows into Mount Everest. As a result, there is overcrowding on Everest, starving the country’s other formidable peaks of income and attention.

Enter Mountain Dew. In partner-ships with the Nepal Tourism Board and the Discovery Channel, the brand built the world’s first algorithmic mountain grading system. Leo aggregated decades of expedition records, terrain complexity maps, seasonal weather hazards, rescue failure rates, and first-hand Sherpa wisdom. They funneled these metrics into an engine and assigned a quantifiable “Dare Score” to individual peaks. This data visually demonstrated that height does not equal danger, giving climbers an scale to gauge terrain toughness.

The genius of the campaign was its consumer utility. Mountain Dew printed smart QR codes on millions of its beverage bottles. When a user scanned the bottle, it unlocked an immersive digital hub, where users could simulate climbs, map out route plans, read real-time weather conditions, and submit expedition inquiries. The campaign took Mountain Dew’s slogan, “Darr Ke Aage Jeet Hai” and algorithmically decoded it for real-world application.

The result: It Swept Goafest 2026 and collected medals across vastly different categories including Integrated, Brand Experience, Social Content, and Video Craft, besides the Grand Prix. “Darescore is a powerful example of how brands are moving from storytelling to measurable participation. For decades, adventure culture celebrated only the final summit. This campaign changed the lens, it quantified courage itself,” says Prabhakar Mundkur, director, advertising & media, Percept. “What made this Grand Prix-worthy was the fusion of technology, gaming logic, data and brand philosophy into one seamless experience.”

If the Darescore campaign embedded data into storytelling, Nerolac chose to stay away from the beaten path. Its “Barefoot Journey” was a hyper-local activation designed by Tribes Communication for Nerolac Perma NoHeat, an acrylic-based, heat-reflective exterior coating. The campaign focused entirely on real-world product performance.

Every summer devotees visit various religious sites and walk barefoot along sweltering walkways or wait in queues on hot concrete floors.

Along with local authorities, the teams coated thewalkways of several high-footfall temples across south-ern India with Nerolac Perma NoHeat paint. The paint reduced the surface temperature of the pathways by up to 15°C offering relief to devotees.

This campaign won the jury over with its simplicity. According to Devangshu Dutta, founder & CEO, Third Eyesight, “Though the campaign might target a small audience, it made an impact by shifting the frame,” Dutta points out. “The campaign turned advertising into lived experience,” Mundkur says. “People didn’t just hear a claim, they felt it. This is media not as interruption, but as empathy.”

For its part, Centre fruit brought back its hoary “Kaisi Jeebh Lapla-payee” tagline using generative AI. Teaming up with WPP, BharatGPT.ai and Google Cloud, Perfetti created voice-based GenAl interactions in local dialects that turned feature phones smart. “What made the experience special was that it felt less like advertising and more like a conversation,” says Gunjan Khetan, director marketing, Perfetti Van Melle. Al was an enabler of accessibility and a tool to build cultural relevance, Khetan adds. “The brilliance lay in how it con-verted a simple sensory reaction -the uncontrollable craving triggered by taste – into a scalable interactive idea. It was playful, memorable and unmistakably Indian. More importantly, it proved that consistency in -brand codes, when combined with fresh execution, can become a formidable creative asset,” Mundkur says.

There you have it. Winning creative awards is validating, but solving the client’s problems through that creativity remains the bellringer.

(Published in Financial Express)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

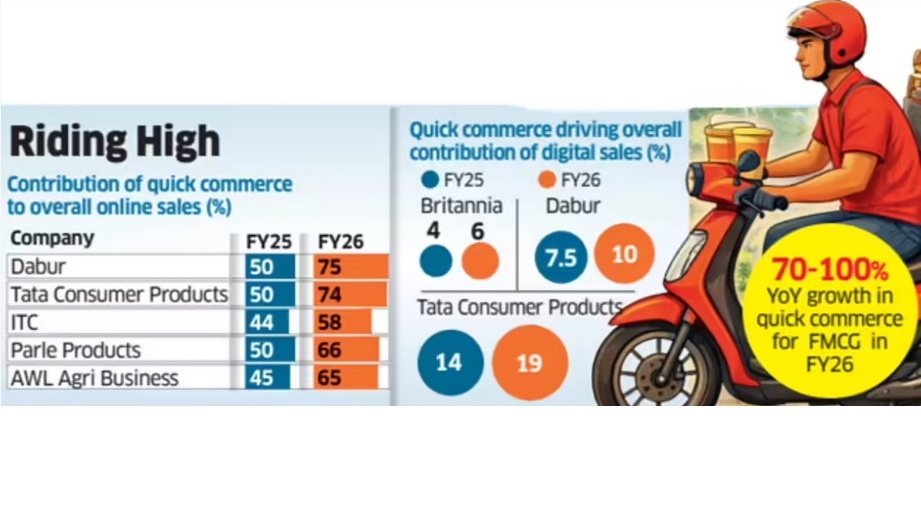

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)