admin

January 25, 2017

Raghavendra Kamath, Business Standard

Mumbai, 25 January 2017

To expand its storage capacity in India, Amazon had opened its largest Fulfilment Centre in Sonipat, Haryana.US-based e-commerce giant Amazon took about a million square feet of office spaces on lease last year, making it equal to what it took between 2008 and 2015 in the country.

Founder and chief executive Jeff Bezos said last year that it would invest another $3 billion in India, amid intense competition in the e-commerce space.

Much of the leased space could be used for seller and development services, besides a 30,000-sq ft building in Bandra Kurla Complex for its India headquarters.

According to Propstack, a data analytics firm for commercial property transactions, various Amazon entities have leased about 1.3 million sq ft since 2008.

Amazon launched its online marketplace in India in 2013 but had been present in the country for eight years for research and development services.

An Amazon India spokesperson said: “As a policy, we do not comment on what we may or may not do in the future.”

Properly consultant Colliers International elaborated on the latest activity by Amazon as the year closed — 100,000 sq ft in the Mohan Co-operative area in Delhi, 150,000 sq ft in Ambience Corporate Tower 2 in Gurgaon and 300,000 sq ft in World Trade Tower Noida.

Before that, through 2016, it leased 90,000 sq ft at Ambience Corporate Tower II NH8 in Gurgaon and 350,000 sq ft at Mindspace, Madhapur, in Hyderabad.

Rival Flipkart, which operates through Flipkart India, Flipkart Internet and Flipkart Payment Gateway, recently took 600,000-sq ft office space in an Embassy group project in Bengaluru.

“Amazon has been investing systematically in expanding its product portfolio, bringing Indian merchants on to their Indian and global platform, and expanding its delivery infrastructure,” said Devangshu Dutta, chief executive officer at retail consultancy Third Eyesight.

Dutta said with its plans to grow private labels and the current e-commerce foreign direct investment regulations which require companies to increase the share of unrelated merchants, the Bezos-led company requires significant organisational capacity and hence is growing office spaces.

Added Raja Seetharaman, director at PropStack, “Amazon is going ‘all out’ in the battle for e-commerce market share in India. They realise that India would be their next biggest market outside the US. With a median age of 27 and growth rate of 6.5-7 per cent, Amazon is willing to invest ‘whatever it takes’ to win.”

The company’s long-term investments, along with futuristic technology like drone deliveries, which it is already piloting in the US, indicate that Amazon is well positioned to be a leader in the e-commerce sector, Seetharaman said.

LEASE DEALS IN 2016

Source: Colliers International

(Published in Business Standard)

admin

January 17, 2017

Suparna Goswami, Forbes

Bengaluru, 17 January 2017

The past week saw India’s Flipkart appointing a non-founder CEO who is also part of Tiger Global Management, the online marketplace’s largest investor firm.

A few days later, Snapdeal, another large Indian online marketplace, brought in real estate firm Housing.com’s CEO Jason Kothari as its chief strategy and investment officer. This news comes on the heels of a recent merger between Housing.com and real estate brokerage firm Prop Tiger, which has raised funds from SoftBank – a major investor in Snapdeal.

Are we seeing a pattern of investor overreach into startups in India?

With this latest SoftBank connection, many are starting to lament how young businesses in India are facing excessive interference from venture capitalists. Some experts tracking the ecosystem have written about the number of years left before “impatient investors take control of the startups” – but how well founded are these suspicions? I spoke with a few local venture capitalists for their side of the story, and perhaps unsurprisingly, many were upset with the media for “sensationalizing” a trend that’s not quite the harbinger it appears to be.

Dev Khare from Lightspeed India Partners Advisors, a VC firm, says things shouldn’t be viewed as black and white. “Just because Flipkart announced a professional CEO who happens to have an association with its investor firm Tiger Global Management doesn’t mean [its] founders no longer will have a say in the company,” says Khare.

“In the end it all boils down to making money. If a company isn’t doing well, the equity that VCs and founders jointly hold will have no value. I don’t see this as a battle between VCs and founders,” he says.

For other VCs, it’s all about the individual needs of a company, and labelling the investor’s role as “interference” is the wrong way to approach the issue.

Tarun Davda, managing partner with VC firm Matrix Partners believes that all investors look out for the wellbeing of their investment, no matter how that presents itself.

“We’re helpful when asked for advice but never fool ourselves into believing that we know more about the business than the founders,” says Davda.

He believes there are often cases where founders feel they can better serve their company by bringing on a more experienced CEO, particularly where founders may lack the experience or skills to take a company ahead through all stages of evolution. Davda provides the example of Google, probably the biggest startup success story of our generation, which had to bring in Eric Schmidt as its CEO early in their journey.

Devangshu Dutta, managing partner of venture accelerator PVC Partners, chalks up the media reaction to local culture. Dutta says Indians have a habit of looking down on founders for handing control over to an outsider.

“There is no harm in accepting that sometimes a company needs a new person at the helm to turn around things,” says Dutta. “In India, we tend to take these things as failures; but [they] could be the outcome of well thought out strategic decisions.”

And in reality, for many startups the Flipkart and Snapdeal episodes are a non-issue; founders are aware of their capabilities and strengths, and their limitations.

Ganesh Shankar, founder of FluxGen Technologies, an IoT startup, is fine to pass on the reins of the company to a person who doesn’t alter the company culture too much. “I guess I [would] be glad if I can find a person willing to take on the top leadership role provided he or she has the experience to scale the business,” he says.

Others view it as a matter of practicality, that these seemingly hard decisions are part of the fiduciary responsibility of the VCs towards their LPs.

Pallav Pandey, CEO of startup BroEx, doesn’t believe that VCs interfere in a company’s affairs unless they’re forced to. “Both founders and investors are stakeholders and after having given enough time to founders [to succeed], if it is inevitable that a new CEO needs to be brought in to steer the company forward, then it should be done,” he says.

However, not all agree with this view. One startup founder I spoke with, who asked not to be named because of the potential harm to his business’ relationships, says the reality of a boardroom meeting is darker than what’s usually projected.

“Founders and VCs are fair-weather friends. One can’t expect things to be always amicable. The main flip side of raising huge funds is that somewhere down the line a founder’s opinion gets diluted. That’s a hard reality,” the founder says.

(Published in Forbes)

admin

January 17, 2017

![]() Suparna Goswami, Forbes

Suparna Goswami, Forbes

![]() Bengaluru, 17 January 2017

Bengaluru, 17 January 2017

The

past week saw India’s Flipkart appointing a non-founder CEO who is also

part of Tiger Global Management, the online marketplace’s largest

investor firm.

The

past week saw India’s Flipkart appointing a non-founder CEO who is also

part of Tiger Global Management, the online marketplace’s largest

investor firm.

A few days later, Snapdeal, another large Indian

online marketplace, brought in real estate firm Housing.com’s CEO Jason

Kothari as its chief strategy and investment officer. This news comes

on the heels of a recent merger between Housing.com and real estate

brokerage firm Prop Tiger, which has raised funds from SoftBank – a

major investor in Snapdeal.

Are we seeing a pattern of investor overreach into startups in India?

With

this latest SoftBank connection, many are starting to lament how young

businesses in India are facing excessive interference from venture

capitalists. Some experts tracking the ecosystem have written about the

number of years left before “impatient investors take control of the

startups” – but how well founded are these suspicions? I spoke with a

few local venture capitalists for their side of the story, and perhaps

unsurprisingly, many were upset with the media for “sensationalizing” a

trend that’s not quite the harbinger it appears to be.

Dev Khare

from Lightspeed India Partners Advisors, a VC firm, says things

shouldn’t be viewed as black and white. “Just because Flipkart

announced a professional CEO who happens to have an association with

its investor firm Tiger Global Management doesn’t mean [its] founders

no longer will have a say in the company,” says Khare.

“In the

end it all boils down to making money. If a company isn’t doing well,

the equity that VCs and founders jointly hold will have no value. I

don’t see this as a battle between VCs and founders,” he says.

For

other VCs, it’s all about the individual needs of a company, and

labelling the investor’s role as “interference” is the wrong way to

approach the issue.

Tarun Davda, managing partner with VC firm

Matrix Partners believes that all investors look out for the wellbeing

of their investment, no matter how that presents itself.

“We’re

helpful when asked for advice but never fool ourselves into believing

that we know more about the business than the founders,” says Davda.

He

believes there are often cases where founders feel they can better

serve their company by bringing on a more experienced CEO, particularly

where founders may lack the experience or skills to take a company

ahead through all stages of evolution. Davda provides the example of

Google, probably the biggest startup success story of our generation,

which had to bring in Eric Schmidt as its CEO early in their journey.

Devangshu

Dutta, managing partner of venture accelerator PVC Partners, chalks up

the media reaction to local culture. Dutta says Indians have a habit of

looking down on founders for handing control over to an outsider.

“There

is no harm in accepting that sometimes a company needs a new person at

the helm to turn around things,” says Dutta. “In India, we tend to take

these things as failures; but [they] could be the outcome of well

thought out strategic decisions.”

And in reality, for

many startups the Flipkart and Snapdeal episodes are a non-issue;

founders are aware of their capabilities and strengths, and their

limitations.

Ganesh Shankar, founder of FluxGen Technologies, an

IoT startup, is fine to pass on the reins of the company to a person

who doesn’t alter the company culture too much. “I guess I [would] be

glad if I can find a person willing to take on the top leadership role

provided he or she has the experience to scale the business,” he says.

Others

view it as a matter of practicality, that these seemingly hard

decisions are part of the fiduciary responsibility of the VCs towards

their LPs.

Pallav Pandey, CEO of startup BroEx, doesn’t believe

that VCs interfere in a company’s affairs unless they’re forced to.

“Both founders and investors are stakeholders and after having given

enough time to founders [to succeed], if it is inevitable that a new

CEO needs to be brought in to steer the company forward, then it should

be done,” he says.

However, not all agree with this view. One

startup founder I spoke with, who asked not to be named because of the

potential harm to his business’ relationships, says the reality of a

boardroom meeting is darker than what’s usually projected.

“Founders

and VCs are fair-weather friends. One can’t expect things to be always

amicable. The main flip side of raising huge funds is that somewhere

down the line a founder’s opinion gets diluted. That’s a hard reality,”

the founder says.

(Published in Forbes)

Devangshu Dutta

January 10, 2017

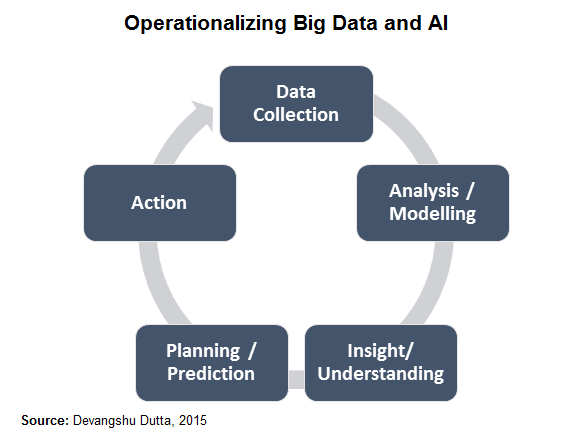

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

admin

January 9, 2017

Sharleen Dsouza, Bloomberg Quint

Mumbai, 9 January 2017

As demand for ayurvedic products grows, especially driven by Yoga guru Baba Ramdev’s Patanjali Ayurved Ltd., FMCG major Hindustan Unilever Ltd. has relaunched its Lever Ayush brand in southern India, the biggest and most competitive market in the space.

The Rs 32,000-crore HUL will offer 20 Lever Ayush products for as low as Rs 30 in the hair, skin and oral care categories across Tamil Nadu, Kerala, Andhra Pradesh, Telangana and Karnataka — the five states are home to several local ayurvedic brands

Patanjali, which largely operates in the north, offers products for as low as Rs 25.

Why South India…

“Traditionally, the southern market consumer is a strong user of ayurvedic products, which could have made HUL consider launching the product initially in the south,” said Devangshu Dutta, chief executive officer at Third Eyesight, a retail and consumer products consulting firm.

“Our current focus is to ensure a successful launch of the new range in these markets to build a scalable and profitable model. We will consider the expansion to other markets at a suitable time going forward,” HUL said in an emailed response to BloombergQuint

There are several well-established brands in the south, the largest market for ayurvedic products, and HUL will find it difficult to make inroads, says Sageraj Bariya, vice-president and analyst at East India Securities.

“(HUL) has been present in the ayurvedic segment with Lever Ayush for a long time, but this has not been their core competency area. In terms of price points, Hindustan Unilever will be competing closely with Patanajli, which has products in a similar price range. It looks difficult for Lever Ayush to really give a stiff competition to Patanjali and other players in the south,” Bariya says.

There are more than 15 ayurvedic brands in southern states, the prominent being Dhathri Ayurveda, Sakunthala, Pankajakasthuri, Heena and Siso.

Patanjali, which has done well in north India, has also managed to make a mark in the south despite local ayurvedic brands having a strong presence, says brand consultant Hairsh Bijoor, founder of Harish Bijoor Consults Inc.

Pricing Pressure

In terms of pricing, HUL is competing with Patanjali head-on. The largest consumer goods company in the country has priced its products in the Rs 30-130 range, close to that of Patanjali’s Rs 25-110.

South-based Ayurvedic brands have priced their skin-care products 30 percent lower and toothpastes 20 percent lower compared to other major brands in the space.

In December 2015, HUL had acquired Kerala-based Moson Group’s Indulekha for Rs 330 crore, just when competition in the ayurvedic segment had started to witness some momentum.

HUL decided to relaunch Lever Ayush to compete even more fiercely in the ayurvedic space by offering lower prices as Indulekha products are more premium in terms of pricing.

“Despite having Indulekha in their portfolio, the company has re-launched Lever Ayush as HUL wants a larger market share in the ayurvedic space, and I expect the company to launch more ayurvedic products going ahead,” said Prashant Agarwal, joint managing director at business consulting firm Wazir Advisors.

Arvind Singhal, chairman of management consulting firm Technopak Advisors, believes HUL’s strong distribution channel will help the company.

Patanjali Factor

Lever Ayush, launched in 2001, failed to perform because the ayurvedic market was relatively small, though growing at a steady pace, experts say.

“With the entrance of Patanjali, the Yoga guru awakened the latent demand for ayurvedic products, which is now an eye-opener for other FMCG companies to get aggressive in the ayurvedic space, as every consumer player wants a share in the expanding ayurvedic market,” said Agarwal.

Patanjali’s turnover grew over two-fold to Rs 5,000 crore in the financial year 2015-16. The company sees it rising to Rs 40,000 crore by 2018-19, according to an Axis Capital report released on December 12, 2016.

(Published in BloombergQuint)