admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

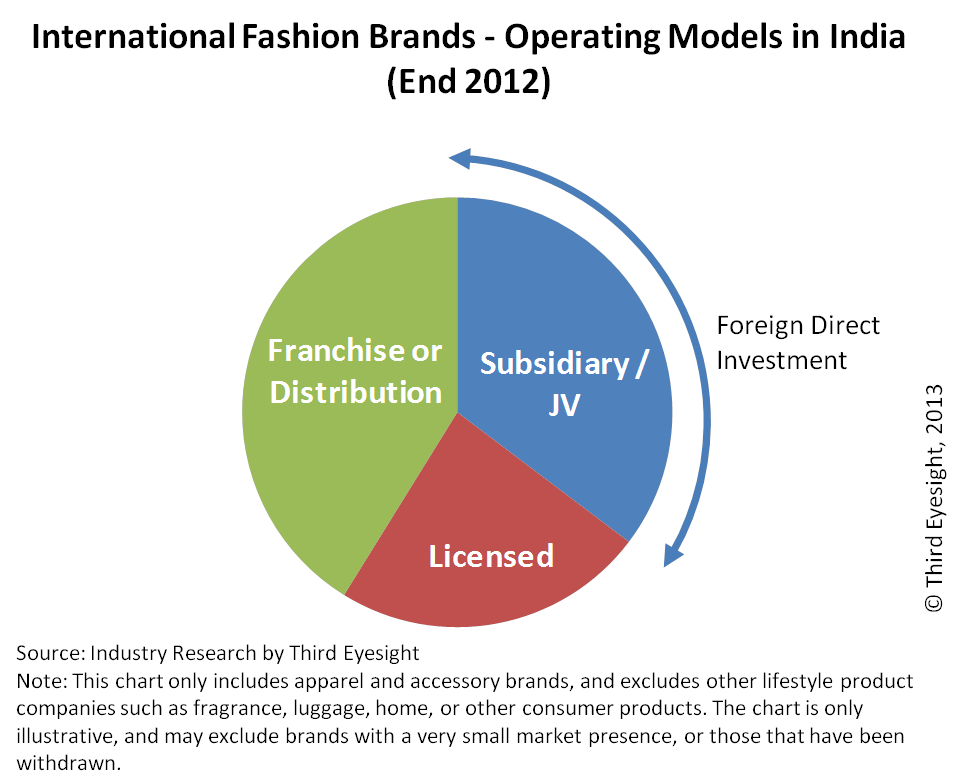

Routes to Market – The Evolution

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.

admin

January 17, 2013

![]() Vishal

Krishna, Business World

Vishal

Krishna, Business World

![]() Bangalore,

January 17, 2013

Bangalore,

January 17, 2013

In

February 2010, Future Group founder and group CEO Kishore Biyani

delivered a lecture at Coimbatore’s Bharathiar School of

Management and Entrepreneur Development. He said his business

ideals were driven by LSD (Lakshmi, Saraswati and Durga). Unless

we create wealth for all strata of society, learn from experiences

and create a strong identity, we will never become an economic

superpower, he told the audience.

In

February 2010, Future Group founder and group CEO Kishore Biyani

delivered a lecture at Coimbatore’s Bharathiar School of

Management and Entrepreneur Development. He said his business

ideals were driven by LSD (Lakshmi, Saraswati and Durga). Unless

we create wealth for all strata of society, learn from experiences

and create a strong identity, we will never become an economic

superpower, he told the audience.

That lecture echoed in May 2011, at a meeting to discuss a new

initiative with select senior executives at the group headquarters

in the SOBO Central Mall, Mumbai. At the end of the presentations,

Biyani told them in chaste Hindi, “Is mein dhan hi dhan hai.”

Translated into English, it means “there is enormous wealth

in this”. Translated into reality, it is a Rs 10,000-crore

opportunity for the Rs 15,000-crore Future Group; besides having

the prospect of creating thousands of livelihoods.

What Biyani was referring to is now taking shape at a 110-acre

site 100 km north of Bangalore, in Tumkur. This Rs 500-crore food

park — the first of two that he intends to set up by early

2014 —is at the heart of Biyani’s push to backward integrate

his group by creating a parallel FMCG business which, he hopes,

can be scaled up to be among the biggest in the country.“We

want to be one of the top three FMCG players in this country,”

he says.

At play here is Biyani’s ingenious instinct: If India is

changing, so are eating habits. “The future is in value-added

food. We see our customers evolving this decade because of the

changing economic conditions,” he says. He

defines value-added food as: TV dinners, frozen foods, ready-to-eat,

baked items, packaged fruit and vegetables, food pastes and curries.

With the food park, Biyani is also challenging the current norm in the retail industry where large rivals such as Reliance Retail, Bharti Easyday and Aditya Birla More source white label and private label products from contract manufacturers rather than getting into manufacturing themselves. So why is he going against the grain? Logistics is 13 per cent of the retail cost of food products. If the food park could reduce this to 5-6 per cent, the group stands to create a lot of “dhan” since food business accounts for 50 per cent of Biyani’s Rs 15,000-crore annual revenue. Eventually, like Walmart, Biyani will hope to sell at least 50-55 per cent of his products through white or private labels as against 35 per cent today. Private label food products earn an average net margin of 65 per cent versus 10-15 per cent from branded products. “We have the customer knowledge from our retail stores that allows us to take this bet,” says Biyani.

“For Biyani, an idea can mean not just a business opportunity but a way to bring investors together to make that product scale to potential,” says B.S. Nagesh, Biyani’s friend, and vice-chairman of the Rs 2,000-crore Shoppers Stop.

To Make It Work

These are hectic times for Biyani. He is pacing up and down in one of the Future Group’s conference rooms in Bangalore, even as he makes multiple phone calls and sips green tea. When sitting, he multi-tasks between an iPad, a Samsung smartphone and a BlackBerry. He tells the person on the other end of the phone to not think negatively and to get on with the work as planned. During his conversation with BW, he is mostly on his feet; he takes a break to listen to executives explaining the progress at the Tumkur project. At times, he slips into deep thought. Often, he runs out to acknowledge a business associate, holds a discussion, and then returns to the conference room.

When it goes live in 2014, the Tumkur park will connect farmers spread over a 300-km radius to six agri cooperatives or collection centres. The produce will go from the collection centres to the food park, where it will be sorted and graded. Some of this will reach stores while the rest will go into processing. The food park will also house pulping, milling, flouring, spice and dal (lentil) units. It will have an 80,000 sq. ft cold store to supply fruits and vegetables round the year. Biyani has also planned a manufacturing centre for 60 medium-sized food processing companies that can make ready-to-eat food for group company Future Ventures using raw material supplied by the food park.

“No one in India has created an integrated food park business, and the country needs this to generate employment in manufacturing and to create a new consumption boom for people,” says Biyani. It will be the job of Future Ventures to transport the products to the kirana network across India, and to the group’s 600 stores through Future Logistics.

But this is just the food aspect of the new business. For non-food

FMCG, the business plan envisages bringing in manufacturing units

of large FMCG majors such as Hindustan Unilever (HUL) and ITC

(talks are on with both), as well as large FMCG contract manufacturers.

For the latter, Biyani plans to provide ready-to-use infrastructure.

If required, the bulk of the responsibility for raw material sourcing

and logistics will be taken care of by various Future Group entities.

The plug-and-play infrastructure could be of immense value to

foreign retailers as the new FDI policy requires them to spend

50 per cent of their investment in backend infrastructure. With

the food park, the foreign retailer need not buy expensive land.

Instead, it can sub-lease it and set up manufacturing operations.

This move satisfies the backend investment requirement of the

FDI policy, and allows foreign retailers to focus on frontend

retailing.

Re-Inventing The Group

Biyani has come a long way in planning the park. At the beginning of last year, analysts considered Future Group a sinking ship. Its biggest company, Pantaloon Retail’s revenue was rising but net margins were almost flat — in the 0.5-1 per cent range. The group is yet to file its annual results for 2011-12 because of a restructuring and will file 18 months’ results in February 2013. It had also piled up a massive debt of over Rs 7,600 crore, whose interest burden had been taking a toll on its profits.

Biyani has managed to pare the debt. He hived off equity in various group entities, even selling businesses such as Future Capital Holdings (which carried 50 per cent of Future Group’s debt) and the Pantaloon fashion format. The biggest move came when he raised Rs 1,600 crore by selling 49 per cent stake in the Pantaloon format to the Aditya Birla Group in 2012.

The financial restructuring brought debt down to less than Rs 1,200 crore by November 2012. “It is good to be out of it,” says Biyani. Then he turns around to the presentation board and, after some thought, says, “That era was different. The business environment and opportunities were different. It was Future Capital Holdings and its NBFC debt that created a lot of confusion for us. I am not just back on track, I have been so for some time now.”

Biyani’s eyes are now focused on the Tumkur park. Work is in full swing at the 110-acre parcel of land acquired from the Karnataka Industrial Development Board. Land is being levelled before construction can begin for the fruits and vegetables centre, the cold store and ripening chambers. Amid the chaos and din, Praveen Dwivedi, a former ITC veteran of the farm supply chain initiative and cigarette business, is busy speaking to farmers and contractors on the project’s execution. Since he is solely responsible for the project as the president of Future Ventures, he works with an iron fist.

Dwivedi is used to inadvertent delays. He makes frequent calls to government officials, keen as he is on securing the 10 MW of power required for the food park immediately. He also wants to have everything — from water to drainage lines — ready in eight months. The project report says the park will need 500,000 litres of water, drawn from the Hemavathi river in Tumkur, and for which a reservoir is being readied. A few farmers are threatening to stop the movement of Dwivedi’s trucks. But he is not perturbed. “This project will eventually employ more than 2,500 people. It will change the way food processing is envisioned in this country,” says Dwivedi.

The Unique Selling Point

The idea of a food park is actually borrowed from China. The Chinese industry is 18 times the size of India’s $70-billion food processing business. An average food park in China is 200 acres in size and has investments of close to a billion dollars each. China has over 30,000 large food processing companies that process everything from meat to cheese and from raisins to nuts. China exported over 500 million tonnes of dry milk powder in 2011 alone. The Chinese industry is projected to reach $2 trillion (from $1.2 trillion) by 2018.

In India, Future Group’s Tumkur project is one of the 15 projects to take off from the posse of 30 mega food park schemes floated by the ministry of food processing. These projects are entitled to a government grant of Rs 50 crore and have been floated as a special purpose vehicles, with government representation on the board till they are commissioned.

Projects that have been commissioned include the 147-acre Srini

Food Park in Chittoor, Andhra Pradesh, with an investment of Rs

200 crore by five promoters; the 80-acre Patanjali Food Park in

Haridwar, Uttarakhand, with Rs 100 crore invested so far; and

the 70-acre International Mega Food Park in Chandigarh, with Rs

150 crore from International Farm Fresh. A couple of these projects

are for pulping fruit and processing vegetables for export and

are betting on revenue from leasing land. The Patanjali Group

is also promoting ayurvedic products of Baba Ramdev.

“Reliance, Spencer’s and Aditya Birla (Group) have connections

with farmers, and a huge private label play. But no one has done

food processing on their own,” says Pinakiranjan Mishra,

national leader of consumer markets, Ernst & Young. He adds

that low margins in manufacturing will be offset by retail sales.

Reliance Retail’s grocery business is close on Future Group’s

heels. It achieved Rs 4,000 crore in food and groceries in under

six years of operations from 600-odd stores. The company’s

total retail business generated revenues of Rs 7,600 crore. Sources

say that the company sources at least 30 per cent of its fruits

and vegetables from farmers. That the company is serious about

its retail business is evident from the fact that the group has

infused Rs 12,000 crore in the retail business and will spend

another Rs 13,000 crore over six years.

Similarly, Bharti Retail’s Easyday format has over 200 stores, and is working with 2,000 suppliers to increase its private label content from 25 per cent to 40 per cent by 2015. Its partner Walmart works with 20,000 suppliers in China alone and sources 95 per cent of the products locally. The Bharti group has already committed Rs 9,000 crore for the retail business.

But the competition does not deter Biyani because he already has the retail scale, and the food processing business will focus on value-added products, which will be largely exported; only about 30 per cent will be for domestic use.

“The world is looking to India for food processing with the Chinese food industry under scrutiny for not maintaining quality. Imagine the scale we can build on,” says Dwivedi. And scale is the question that Dwivedi has to find an answer to. He cites the example of an industrial pizza machine that can make 20,000 pizzas an hour, saying there has to be commensurate local consumption, which is unlikely to happen. “Can we use the same machine to make chapattis, parathas, rotis and other baked items, besides pizzas? This will allow us to utilise the machine to the fullest instead of letting it sit idle,” he says. Scale is essential because the food park will eventually have a major portion of its business contributing to exports. “Eventually scale will be possible only through exports,” says Dwivedi.

Getting Retail Into Play

Even though he will rely heavily on exports, Biyani has his entire retail chain of more than 600 supermarket and hypermarket stores backing him in rural, semi-urban and urban regions of the country to utilise the production from the food park. He has 315 Big Bazaar and Food Bazaar stores in major cities; 200 KB’s Fairprice shops; 38 Big Apple Express stores; and 37 Aadhaar stores. “There is a larger opportunity in retailing with KB’s Fairprice shops,” says Biyani.

He adds that he wants to empower the kirana as a franchisee and is identifying 10,000 franchisees to open KB’s Fairprice shops over this decade. Till now KB’s Fairprice shops were limited only to Delhi, Mumbai and Bangalore. “We are also going to acquire or take over many more small retail stores in a couple of years,” says Biyani.

A few years ago, Nilgiris, a retail chain owned by UK-based PE fund Actis in Bangalore, mooted the idea of experimenting with the concept of empowering small entrepreneurs to use its brand name. The project did take off with at least 50 successful small entrepreneurs who understood modern retailing. But it is intrinsically difficult to find local entrepreneurs who can work with corporate processes across every city. Nilgiris’ small entrepreneurs were usually retired executives or businessmen who wanted to experiment with retailing. But it was Nilgiris that provided the backward linkages and supplies. If such a plan is executed by Biyani, he would have the largest network of stores that he can supply to from the food park.

And this is something that other food parks do not have access to. Along with subsidiary companies like Future Supply Chain and Future Logistics, he hopes to complete the farm-to-fork loop. “India is a fascinating country to do business in. And with such a young population, it is only the beginning of what we as a group can achieve,” says Biyani.

Between The Cup And The Lip

Despite enormous planning, Biyani still has a few issues to grapple with. More than integrating farmers into the food park, it would be a challenge to convince large FMCG players such as PepsiCo, Dabur, HUL and Britannia to set up shop in the park.

“There needs to be commonality in a food park, much like in an automobile cluster, which has a large anchor, if the project has to succeed,” says Devangshu Dutta, CEO of Third Eyesight, a retail consultancy. He adds that there is a business case if the Future Group can create an ecosystem in the food park where each entity works towards a common benefit.

About seven years ago, various state governments had asked individual entrepreneurs to set up food parks with a subsidy of Rs 4 crore. Many local businesses bought the land, but failed to open food parks. In Karnataka, small mango pulping units (30 tonnes-a-day capacity) started but remained operational only for about six months of the year. Similarly, textile parks became a real estate play. In many cases, the units set up functioned in silos rather than with a unified vision.

“These businesses were set up without market linkages, so they didn’t take off,” says Biyani. He says that Capital Foods, in which he has a 43 per cent stake, will be one of the larger private food processing companies in the park, and will act as anchor with a 100,000 sq. ft factory.

“Since the Future Group is back to pure-play retailing, it can focus on new businesses such as food processing that can supply food products to its retail formats and also create new markets with exports,” says Harminder Sahni, managing director of Wazir Advisors, a retail consultancy.

Perhaps, this is the beginning of the emancipation of Biyani the entrepreneur. Always a risk-taker, he is now ready to take bigger risks in a journey that will determine whether he is as successful in FMCG as he has been in retail.

admin

January 10, 2013

![]() Nupur

Anand, DNA (Daily News & Analysis)

Nupur

Anand, DNA (Daily News & Analysis)

![]() Mumbai,

January 10, 2013

Mumbai,

January 10, 2013

It’s

not even mid-January yet, but a "flat 50% off" sale

is already on at an apparel brand outlet at Mumbai’s poshest mall.

It’s

not even mid-January yet, but a "flat 50% off" sale

is already on at an apparel brand outlet at Mumbai’s poshest mall.

This unseemly break with tradition – the two-week-long ‘sale’ season used to start in the third week of January, offer nominal discounts initially but jack them up later towards half price is not a case in isolation.

Sale, that four-letter word with the power to smoke out even

the tight-fisted shopper from self-imposed shopping exile, is

now plastered across all kinds of retail outlets at malls.

What’s more, several brands are already offering ‘flat 40-50% off’ in the first week of their sale. And no one knows how long this year’s sale season would last.

Abhishek Ranganathan, analyst at Phillip Capital, says the trend of advanced sale started last year due to infrequent ringing of cash registers. “This was expected to correct from this season. But that was not to be. As a few brands launched their ‘sales’ early again this year, others had to follow suit. For, if you don’t, then you’ll end up losing business to the store next door.”

Retail industry observers say premium fashion brands started the season with deep discounts. Agrees the manager of the apparel outlet at Phoenix. “We’ve realised that we do better business in the sale month of January than we do in July-December. So, in order to attract customers, we’ve started with a flat 50% off.”

There’s more to it, says Devangshu Dutta, CEO of Third Eyesight, a retail industry research firm. “New stock typically starts coming in from mid-February. Since slow economic growth has affected sales for the entire year, companies had to start with deep discounts in order to free up cash.”

Early starts, prolonged duration, deep discounts from the word go… such aspects of 2012 sale had caused concern to the retail industry. And it’s no different this year.

Experts say discounts help inboosting volumes but eat into margins. Worse, a relatively longer sale season was also driving away customers who are not essentially bargain-hunters.

As a result, retailers had started correcting their strategy. Analysts point out that in the past six months, attempts have been made to check inventory and forecast demand. “We’ve been trying to shift to a quicker inventory churn so that we could curtail the sale season, but it may take a quarter more,” says the CEO of a multi-brand outlet.

Retailers say that the extent of footfalls in the first two weeks of the sale season will decide how long the discount period may be extended.

If sales fail to pick up in spite of discounted sales, the sale period may well stretch to a month like it happened last year, say experts.

admin

January 6, 2013

R Krishna,DNA (Daily News & Analysis)

Mumbai, January 6, 2013

Unity

in diversity is one of those maxims that makes no sense in India,

except in the rarest of contexts. Chai, a colonial import, is

one such factor that Indians can identify with regardless of class

and religion. That’s why it’s surprising that there

are few places that serve good tea outside of our homes. Tea from

vending machines tastes artificial. At hotels, the decoction is

rarely fresh. And though tapris do serve good tea, they are over

boiled and sickly sweet.

Unity

in diversity is one of those maxims that makes no sense in India,

except in the rarest of contexts. Chai, a colonial import, is

one such factor that Indians can identify with regardless of class

and religion. That’s why it’s surprising that there

are few places that serve good tea outside of our homes. Tea from

vending machines tastes artificial. At hotels, the decoction is

rarely fresh. And though tapris do serve good tea, they are over

boiled and sickly sweet.

“If I ask you to recommend one place in Mumbai that offers

great tea, you won’t be able to come up with a clear answer,”

says Amuleek Singh Bijral, founder of the Bangalore-based tea

chain, Chai Point. According to him there is a demand for good

chai that is not being met. “In terms of sheer volumes, tea

is consumed far more than coffee in India,” says Bijral,

“It is just that nobody has given it the kind of branding

that coffee enjoys. There is an opportunity for organised players

to come in to address this need.”

A challenge Starbucks faced

However, tea chains like Chai Point, which have come up in the last five years or so, face an uphill battle. Tea’s popularity in Indian homes, in fact, acts against its image. Coffee is considered a lifestyle statement, while tea is ordinary. It’s easy to convince a consumer to spend upward of Rs 80 for a cup of coffee. However, even Rs 30-40 for a cup of tea is considered expensive. Bijral is aware of the problem. “Starbucks had a similar challenge almost 30 years ago when they opened their chain in the US. Coffee was a drink every American prepared in his home. But they created a brand that convinced Americans to spend money on a cup of coffee,” says Bijral. Over the years Starbucks and other coffee chains developed a model such that the coffee chains’ popularity has less to do with the beverage itself, and more to do with the whole experience. Tea chains, on the other hand, are blazing a new path.

Chai Point, for instance, targets the white-collar worker. “Nobody in office takes a cappuccino break. We take a chai break. Office-goers are not looking for a lounge,” says Bijral, “Our outlets are in areas with lots of offices around. We want our customers to come to our outlets several times in a day to have a freshly brewed cup of tea at a hygienic place.”

Delhi-based Tea Halt has put up kiosks in colleges, marketplaces and in office areas. “We first wanted to introduce customers to various kinds of teas before putting up cafes which add to the cost,” says Ankur Agrawal, co-founder, Tisane which runs Tea Halt, “The range of teas we offer depend on the area in which we have put the kiosks in. For instance, near colleges our tea starts at Rs10. Near offices, we offer teas that are more expensive.”

Variety holds the key

While both Chai Point and Tea Halt stress on convenience, Golden Tips, the Kolkata-based tea company has taken a different approach with their own tea lounge, Tea Cosy. “We want to make tea glamorous by offering large variety of teas, as well as sell equipment such as infusers and teapots, stuff that people haven’t tried before,” says Bala Sarda, vice president, business development, Golden Tips.

Sarda says that customers can sample white tea, oolongs, and other varieties of tea at Tea Cosy, and buy the leaves of the ones they like. The leaves can be a blend from different tea estates or sourced from a single estate from different regions in India and the world. “Consumers can get a simple cup of tea at home. What we want to do is to introduce them to the world of tea. The sheer variety of teas on offer and the growing awareness about tea’s health benefits is attracting younger consumers (18-30 age bracket) to our outlets,” she says.

Still, tea chains attract a miniscule crowd compared to coffee chains. But if global trends are anything to go by, things can only get better. Earlier this year Starbucks paid $650 mn to take over the tea company, Teavana. Just two weeks ago Starbucks CEO Howard Schultz announced that apart from introducing Teavana products at their own outlets, the company would open standalone Teavana stores to “do for tea what it [Starbucks] did for coffee”.

It is some such move that will make tea chains contemporary, says Devangshu Dutta, chief executive of consultancy firm Third Eyesight, “It would have been easier for tea chains 20 years ago when coffee was not present in the urban market. Things could change in the future. But if past experience is anything to go by, it will not be an Indian company that will cause the turnaround. Tea chains will need an approval stamp from the West.”