Devangshu Dutta

January 27, 2010

An article in the San Francisco Chronicle sparked off a debate on whether ecologically friendly can be mainstream, whether customers will switch from traditional to eco-friendly fashions and if so, when. There is the view that eco-friendly products are necessarily niche and cannot match up in fashionability and affordability to ‘mainstream’ products.

I don’t think it is an either/or choice between styling and eco-friendly. To sell, eco-friendly merchandise absolutely MUST be comparable to or better than eco-unfriendly merchandise, both in style and quality.

Pricing is another story. The article also quotes Joslin Van Arsdale (founder of Eco Citizen, a San Francisco boutique devoted to Earth-friendly clothing) as saying, “When it comes to buying green or price, the general public will more likely choose the cheaper item on anything, whether it’s fashion or tomatoes.”

While most consumers will not willingly pay higher prices for eco-friendly merchandise, that may change as the cost of being eco-unfriendly goes up through awareness and legislation. There was a time when safety belts in cars were optional at an extra cost. No one would argue against paying the extra price for safety today.

Perhaps many of us would rather trash the planet cheaply because we may not feel the heat within our lifetimes. That is no reason that others, who feel more responsible, will allow that to happen indefinitely.

One way or the other, eco-friendly merchandise will compare in price, too.

Some of the parity will come from reducing the cost of eco-friendly stuff, but the bulk will probably happen because the cost of being eco-unfriendly will go up.

The original article is here – “Green fashion has new cachet“.

admin

January 23, 2010

![]() By

Vishal Krishna

By

Vishal Krishna

![]() Businessworld,

January 23, 2010

Businessworld,

January 23, 2010![]()

An upwardly mobile population makes Bangalore’s suburb Jaya-nagar a lip-smacking catchment area for organised retailers. The significance of this ‘must-have’ location was not lost on Indian retail’s biggies Reliance Retail, Big Bazaar, Aditya Birla Group and Spencer’s Retail. By 2007, all four had already set up 5,000-6,000 sq. ft supermarkets in the area. But the stores were still to break even when they had to deal with a new contender. Dubai-based Micky Jagtiani’s Landmark Group started its 70,000 sq. ft hypermarket in collaboration with Dutch retail chain Spar in the locality in 2007.

Just a year after Jagtiani built his first store in India, the aftershocks of the global meltdown hit the Indian retail industry. The tight money conditions saw even the big Indian retailers slow down their expansion plans. One would have assumed that Spar, being a newcomer, would find the going tough in this period as well. But in the midst of the slowdown, Spar has added one hypermarket and one supermarket in Bangalore. Another hypermarket is expected to come up in March. In fact, managing director Viney Singh is preparing a nation-wide plan to launch five more stores by the end of the year and at least 10 in the following four years.

| SPAR |

| MD: Viney Singh. Promoted by

Micky Jagtiani Stores: 3 (30,000-50,000 sq. ft hypermarkets) Plans: 15 stores in five years; Present in Bangalore The stores sell fresh food, FMCG products and private label food. The first retailer to own stores with large cold rooms and space to help logistics solutions |

Landmark, which also owns Lifestyle, Home Centre and Max retail chains, is among a handful of retailers still expanding rapidly after an investment storm blew through India’s $350- billion retail industry, first giving rise to a huge tide, before the inevitable ebb. In the past 48 months, local entrepreneurs pumped in $10 billion (around Rs 46,200 crore at Rs 46 to a dollar) in a dozen formats to strengthen their presence in the market as the government pondered over opening up domestic retail to foreign companies. But lack of experience, poorly conceived strategies, over-ambitious plans and a slowdown triggered by the global recession has left them all bruised and battered. Weaker retailers such as Subhiksha who over-reached, had to bite the dust. Those left standing are taking a breather for the moment.

But as the haze clears, nearly a dozen new players beyond the Big Five – Kishore Biyani’s Pantaloon, K. Raheja group’s Shoppers Stop, Mukesh Ambani’s Reliance Retail, R.P. Goenka Group’s Spencer’s and Aditya Birla Retail’s More – are moving briskly to build up significant retail empires. Most of them are small, but they have survived the worst part of the slowdown. They are experimenting with models very different from the Big Five. They may still be tweaking their models but they are confident and competitive. And more than anything else, they are proving that you need pluck, not necessarily loads of money, to weather a storm.

But can they graduate to the next level and become serious rivals to the Big Five? Can they scale up their models without hitting the same roadblocks that the Big Five did in their quest for growth? Those are the big questions facing this pack of retail enthusiasts.

It is inevitable that as they open more stores and expand into more areas, at least some of the players featured in this story will stumble. Some will fade away. And some opportunistic ones have already started negotiating to sell out at a profit to a bigger player instead of trying to build a long-term business. But at least a few of them are showing the determination that market leader Kishore Biyani wore five years ago.

Their reasonable successes, despite varied interests and diverse strategies, infuse hope that India’s choppy retail industry may be settling down.

| DANGER ZONE In a highly competitive market, smaller retail chains have cracks in their business models |

|

Behind The Scenes

Interestingly, hypermarket player Spar is an exception in this lot of new players because, first, it has a retailing pedigree, and second, because it is backed by a big group with deep pockets. Most of the others are product companies that have now got into the retail business. A few are backend specialists who have logically forward integrated to set up retail stores.

Take the case of Bangalore-based Uday Singh whose Rs 200-crore hybrid seeds company Namdhari Seeds got into retail sale of premium fruits and vegetables through Namdhari Fresh. Singh, who is the parent company’s managing director, says he was so busy building the seeds business that retail was just a natural extension and nothing more. Though food retailing can take more than five years to break even, Singh says the Rs 30 crore-Namdhari Fresh turned cash positive in 2009. Having tasted blood, he now plans to expand the 20-store chain in Bangalore to 100 in the next two years.

However, the past couple of years were tough for Namdhari Fresh, which had to shut eight stores in Delhi when the state government clamped down on use of non-commercial property for commercial purposes. “It was a big loss for us. But we are still growing by 30 per cent,” says Praveen Dwivedi, CEO of Namdhari Fresh.

On similar lines, Delhi-based REI Agro – a rice producer and exporter – hived off its retail entity REI 6Ten in 2007 and took it public. Leveraging its connect with farmers, the company launched 21 stores of 1,000 sq. ft each stocking private labels in rice, staples, spices and other items. “The concept behind 6Ten was to create not a monthly grocery store but rather a daily needs store,” says Danish Beg, REI Agro’s assistant finance controller, adding the retail business reported a net profit of Rs 22 crore in 2009. The company now has 300 stores across 10 cities such as Delhi, Nagpur and Kolkata.

| 6TEN |

| Promoter: Sanjay and Sandip

Jhunjhunwala Revenue: Rs 800 crore Stores: 300 in all (supermarkets and convenience stores of 700-1,100 sq. ft) Present in 10 cities including Delhi and Mumbai The listed entity is a fresh food and and FMCG retail chain |

Similarly, in 2007, when denim and apparel manufacturer Arvind Mills restructured its loss-making apparel retail business into three kinds of stores – Megamart (150 stores), Flying Machine (60) and Arrow (70) – they seemed to have hit the sweet spot. The 1,500-sq. ft stores with distinct identities – Megamart for affordable, mass-market products from multiple brands, Flying Machine for trendy apparel and Arrow for the executives – was just the formula. The retail and brand business now generates Rs 550 crore, about 15 per cent of Arvind Mills’ revenues. Suresh J., CEO of Arvind Lifestyle Brands and Arvind Retail, says the retail business turned cash positive in 2009. “The business is growing by 40 per cent and we are planning to add over 100 stores by next year,” he adds.

| ARVIND RETAIL |

| CEO: Suresh J. Revenue: Rs 330 crore Stores: 280 (hyperand small-format) Plans: 100 more stores in two years; Present in Bangalore; The apparel retailer houses 80 per cent private labels along with other brands |

His main focus is on opening Megamart stores across India. “We have a symbiotic relationship with the larger retailers. We follow a market saturation strategy before moving to new geographies,” says Suresh. Analysts say Arvind’s strategy of targeting 30 tier-3 cities such as Nashik and Namakal, has been the key driver behind its retail business.

Going the same direction is Delhi-based apparel maker Koutons Retail, which chose the franchisee route to ramp up to 1,360 stores in 10 years, more than 400 in the past four years. It owns 100 of these 1,000 sq. ft-stores and plans to open another 100 company-owned stores in two years. “The franchisee route is yielding results. It has not only reduced costs, by minimising capex, rentals and employee costs but has also led to an increase in sales since franchisees make an extra effort for their sales incentives,” explains D.P.S. Kohli, chairman of Rs 1,000-crore Koutons Retail. The retail chain, however, is yet to break even operationally.

| KOUTONS RETAIL |

| Chairman: D.P.S. Kohli Revenue: Rs 1,000 crore Stores: 100 (small format 1,000-1,500 sq. ft) Plans: 100 more stores by 2011 Present in multiple cities; Manufacturer-turned-retailer of apparel |

An exception from the food and apparel pack is the Bangalore-based Rs 400-crore mattress manufacturer Kurlon. For long, the company used its 5,000 franchisees to sell mattresses. However, in 2008, Kurlon ventured into organised retail for the first time in Bangalore and Mumbai with 17 Kurlon Nest stores, which sell everything from mattresses to bed linen. The idea is to have a one-stop shop for all home furnishing needs. “People have never slept more than they did last year during the recession,” quips Kurlon chairman T. Sudhakar Pai, referring to the job losses during the slowdown. Pai says the business grew 35 per cent in this phase. He now expects to open over 100 stores in three years and has targeted a break even in two years.

| KURLON NEST |

| Promoter: T. Sudhakar Pai Stores: 17 (large format — above 5,000 sq. ft) Plans: 100 more stores. Get funds for expansion through private equity or by listing by the end of 2010 Present in Bangalore; Sells furnishing, mattresses, linen and even custom-made furniture |

Supermarket Warriors

Neighbourhood supermarkets is a business where the Big Five have mostly been humbled. They raced to set up hundreds of stores, but have had to write down several thousand crores from their balance sheets, freeze expansion and overhaul strategy. Among them, Reliance has shut 50 supermarkets, Aditya Birla Retail 70, Spencer’s 150 and Pantaloon Retail 10. The reasons for the closures have varied from government or political opposition, poor choice of location, bad logistics and other operational issues.

Analysts such as Third Eyesight’s Devangshu Dutta believe the Indian customer is disloyal to organised retail brands and, therefore, the supermarkets cannot compete with kirana stores, in the short term. Indian retail’s numero uno Kishore Biyani told BW he was sceptical about small 2,000 sq. ft stores and stopped expanding his small format Food Bazaar in 2008. But small may well be beautiful as far as many of the newcomers are concerned.

A case in point is the Delhi supermarket chain Big Apple promoted by Express Retail that belongs to Lalwani Holdings and Chaurasia Group, which have interests in tobacco and real estate. Starting out in 2005, Express Retail had set up 65 stores with an average size of 1,500 sq. ft and an initial investment of Rs 100 crore. High rentals forced it to shut 20-odd stores in the past two years, shaving off 10 per cent from its topline. However, Express Retail’s CEO, P. Anand Murthy, claims it has turned cash positive in 2009. “Skyrocketing rentals have always been a concern. If a location does not reap profit for us, why would we keep it open?” says Murthy. He adds that each closed location had its own strategic issues – no parking space, strong competition from kirana stores, among others.

| BIG APPLE |

| Promoters: Lalwani Holdings

and Chaurasia Group. P. Anand Murthy is the company’s

CEO Revenue: Rs 170 crore Stores: 42 (convenience and mini-supermarkets of 1,500-3,000 sq. ft); Present in Delhi The food and FMCG chain has direct tie-ups with farmers for fresh supplies |

Another company that jumped on to the supermarket bandwagon is the vegetables, fruits and FMCG retailer Spinach, a subsidiary of real estate major Wadhawan group. “We tried the farm-to-fork connect,” says Kapil Wadhawan, chairman of Mumbai-based Wadhawan Holdings, which started the Spinach chain in 2006.

The group planned an investment of Rs 300 crore to expand Spinach, which has close to 50 stores across India. They have targeted a three-year break even with their five brands in retail – Spinach, Sangam, Sabka Bazaar, Maratha Stores and Smart Retail. The Sangam and Maratha Stores cater to the specific needs of Maharashtrians. Smart Retail is not very different from Spinach, but is smaller in size with 1,000 sq. ft stores. Sabka Bazaar (bought for Rs 100 crore in 2007) again targets local catchment areas. The average size of the stores is 2,500-3,000 sq. ft and their private labels bring in 20 per cent of the business. The group is still trying to perfect its act, with some stores doing well while others showing patchy performance.

| SPINACH |

| Promoter: Kapil Wadhawan of

Wadhawan Holding Stores: 220 including other brands average size is 2,500-3,000 sq. ft) Present in Mumbai and Delhi Sells fresh food and FMCG products. Has 20 per cent private labels |

One player who thinks the experimental phase is over and is willing to pull the throttle is Delhi-based Samir Modi’s venture 24×7. The chain’s USP is convenience stores that are open round-the-clock. Modi, son of Godfrey Phillips group’s chairman K.K. Modi, says he has experimented with the formula in his four outlets in Delhi. One of the stores has downed shutters but Modi remains unfazed and is planning to expand to 100 outlets in 18 months.

| 24×7 |

| Promoter: Samir Modi of Modi

Enterprises Stores: 3 (1,000 sq. ft convenience stores) Plans: Rs 100 crore additional investment and expanding to 100 more stores in two years. Plans to break even in three years; Present in Delhi; Is an FMCG-based convenience store |

“Nothing like this has existed in the country. Such outlets are born out of a change in lifestyle,” says Samir Modi. 24×7 targets those who work till late in the night. The business was set up with an initial investment of Rs 4 crore but is going through a Rs 100 crore expansion. “There was a need for convenience stores for working Indians, based on the western model,” he says.

The Pitfalls Ahead

Before we understand why the new players are so upbeat, we need to understand why some retailers have floundered. Analysts say the food and apparel businesses are all about rotating inventory. But food is tougher because of its complex supply chain. If a retailer is sourcing directly from farmers, investing in a cold chain is imperative. Then, the logistics of sending the produce to the many smaller stores from a warehouse becomes a nightmare for quality management. “Fuel cost and pilferage is the problem,” says Ajay D’souza, head of Crisil Research in Mumbai. Combine this with high operational costs and the lack of cash to manage the working capital cycle, and you will understand why Subhiksha’s 1,600-store chain collapsed.

Other organised retail chains have also run into funding and cash flow problems once they reached a particular scale. Nilgiri’s is another such troubled supermarket chain. It has over 90 stores in Tamil Nadu, Karnataka and Andhra Pradesh. Recently, it faced management troubles with Actis, the UK-based private equity firm, and the promoter family of M. Chenniappan getting into a tussle over the sale of property worth Rs 90 crore and a rights issue of Rs 35 crore that could reduce the promoters’ stake by 2-3 per cent. Actis owns 65 per cent of Nilgiri’s, while the family owns 35 per cent.

| NILGIRI’S |

| CEO: Vikram Seth Stores: 90 (supermarkets Of 3,000-5,000 sq. ft) Plans: 200 more stores in two years Present in Chennai and Bangalore; The fresh food and FMCG retail chain operates mainly through franchisees |

A member of the promoter family told BW that Actis had gone ahead with the rights issue without the family’s approval. But, sources close to Actis say that the family was kept informed and the rights issue was necessary to bring in fresh capital needed for expansion. Sources add that Actis aimed at turning around the retail chain in four years before planning its exit. The promoter family sold 65 per cent stake to Actis in 2006 for Rs 300 crore. Actis expanded the supermarket chain to over 90 stores through franchisees and plans to open 200 more stores in three years. While Actis declined to comment on the situation, the Chenniappan family says that it is losing control over the chain it had initiated. The family’s move to the company law board (CLB) to stop the rights issue was vacated. The CLB has asked the company’s management to provide details of the utilisation of the funds from the rights issue. A copy of the CLB order is with BW.

Searching For The Mantra

The ones who seem to have a better shot at moving to the next level of play have one thing in common – they are integrated players. Invariably, it is the strength derived from their integration that has saved them from collapsing in poor market conditions.

Namdhari, for instance, has been working with farmers for 25 years. The company had prior experience of managing the fruits and vegetables supply chain, and has ended up building the retail chain around that. The company owns 18 refrigerated trucks and uses the cold chain expertise to service new markets across India. “We have evolved into modern retail based on a strong backend,” says Dwivedi of Namdhari Fresh. He says why many have failed is because modern retailers tried to get into the retail business without any experience or understanding of backend operations, especially of how farm economics worked.

| NAMDHARI FRESH |

| CEO: Praveen Dwivedi. Promoted

by Uday Singh, MD of Namdhari Seeds Revenue: Rs 30 crore; Stores: 20 (2,000-3,000 sq. ft mini-super markets) Plans: 100 stores in two years; Present in Bangalore; Also supply to the UK |

Similarly, Arvind Mills and Koutons already had established supply chains that they had mastered over several years. In apparel private labels, it is each individual store that sends its requirement to the manufacturer and the supply chain is managed seamlessly. It is not as complicated as the food segment where you need to maintain freshness of the products. REI Agro and Kurlon are two organisations that have built their retail chains around their core products of rice and mattresses but have expanded the offerings in the store to make it a worthwhile trip for the shopper. While REI’s stores stock spices, lentils and the entire range of FMCG and food products, Kurlon’s stores stock bed linen, mattresses and even custom-made furniture.

Some of those that did not start off controlling their supply chains have ended up doing so. For instance, Spar – which has a large selection of fish and meat to cater to expats in Bangalore – has seven cold rooms in each of its stores. It also has tie-ups with around 80 farmers (for vegetables and grains) in Hoskote, near Bangalore, and also with small poultry farms and meat suppliers. Delhi-centric Big Apple’s USP is its direct tie-ups with farmers in Haryana, Rajasthan, Himachal Pradesh and Uttar Pradesh for fresh supplies of items such as rice, pulses, fruits and vegetables. “Local connect is very important for retailers and that is where the business is – making brands affordable to an aspiring segment of the population,” says D’Souza of Crisil. Spinach has also integrated heavily. About 20 per cent of Spinach’s vegetables and fruits are sourced from farms, the rest come from mandis.

“It is all about pricing. Discounts should compensate with people buying other things to make the store profitable,” says Wadhawan. Spar also differentiated itself from other crowded supermarkets through its store design. It left more space between aisles, similar to Spencer’s. Spar’s 7-10 feet space between the racks is among the widest in the country.

Defining Moment

The question is: having come this far, will the newcomers get into the next round easily? The new retailers may have seen through the slowdown but they are not yet above water. Many, such as Koutons, are not even cash positive.

As retail is a volume game, the smaller retailers cannot remain hidden in a geography or industry niche and hope to survive. Only when they scale up will they be fully exposed to the vagaries of the cutthroat retail business.

The biggest hurdle is financing. "Retailers still have a difficult time raising loans for new projects. It will remain a business driven by equity funding," says Pinakiranjan Mishra, national leader of retail and consumer practice, Ernst & Young. Pantaloon CEO Biyani says that it was only the liquidity squeeze that killed some retail entrepreneurs last year. "If money could have been raised on time, then retailers would not have been in trouble," he adds. REI’s 6Ten has had to curb its ambition too. Promoters Sanjay and Sandip Jhunjhunwala had planned to invest Rs 1,500 crore to open more than 1,000 stores. But they have stopped at 300 because cash to expand the retail business has become hard to come by.

The organised retail industry could only raise Rs 2,000 crore through initial public offerings (IPOs) and the total private equity investment in Indian retail was close to a dismal Rs 2,000 crore this decade, says Pankaj Jaju of Enam Securities. "Very few Indian retailers will become large because funding is not available for the long term," says Jaju. He adds that the biggest bottleneck to retail was that private equity investment from abroad was treated as foreign direct investment (FDI) by the Indian retail policy and this was turning out to be a bottleneck for the growth of the industry. Bankers stay away from the retail business because they have no collateral to fall back upon if the retailer goes out of business. In the case of Subhiksha, bankers and private equity players could not recover the money as the business had no real assets. The real estate was owned by landlords, and the only assets were furniture and fixtures, whose value cannot cover the defaults for the recovering bank.

Their other big challenge in going national will be managing the supply chain. While the new players have exercised a tighter control in smaller geographies, their skills in managing nation-wide logistics and supply chains are still untested. Whether a Big Apple or Spinach can manage their chains as efficiently if they grow manifold and start operating in distant parts of the country is still to be seen.

Analysts such as Mishra believe that 2010 will bring relief to retailers from exorbitant rentals (which account for as much as 20 per cent of costs for some retailers), which are projected to fall.

The defining trend in the year, however, will be consolidation. "There are many lesser known retailers who want to sell. There is good valuation for people who have created scale and their brands are only known in niche geographies," says Deepak Srinath, director of Bangalore-based Viedea Capital Advisors, which advises smaller business houses that set up retail chains. Srinath says the industry was looking to consolidate because entrepreneurs cannot scale up owing to scarce institutional funding for expansion and managing their working capital. Therefore, retailers who are running out of cash are merging with larger players to survive.

| AGAINST GOLIATH Some smaller chains are holding up better than the big players in generating revenue |

| BIG PLAYERS: Spencer�s Retail: Rs 9,600 per sq. ft Shoppers Stop: Rs 8,500 per sq. ft Pantaloon: Rs 8,000 per sq. ft Trent: Rs 7,500 per sq. ft NEW PLAYERS: Arvind Retail: Rs 50,000 per sq. ft 6TEN: Rs 26,000 per sq. ft Big Apple: Rs 22,000 per sq. ft Namdhari Fresh: Rs 7,500 per sq. ft Some smaller chains are holding up better than the big players in generating revenue |

"The organised retail space has very little differentiation. Most business models are similar. However, models are still evolving in the country and there is ample opportunity for new players," says Crisil’s D’souza. Faced with the real test of character, the new retailers will have to build scale this year. After all, the rules in this fiercely competitive industry are such that only those who can make that transition will be able to see the light of the in 2011.

[With inputs from Suneera Tandon]

(Copyright: Businessworld)

Neha Singhal

January 8, 2010

A recent experience with one of the quick service restaurants took me back to my post-graduate class of Consumer Service Standards.

We studied five essential elements of service standards, which are:

The last, redressing complaints, is the most important and difficult aspect among these elements. It requires instant responsiveness and sufficient empowerment of staff to manage a dissatisfied customer.

Standard operating procedures requires staff to follow the procedures as they are written, whereas store staff need to immediately respond to a unique situation every time ensuring that personal judgement will be called for on every occasion.

To elaborate on how important is responsiveness and sufficient empowerment of staff; I will like to discuss a recent experience with a quick service restaurant. I will first describe my reactions as a customer to understand the consumer’s expectations and reaction when a retailer is unable to meet the same and then will analyze the same from a retailer’s and a consultant’s perspective.

I ordered for some salad which contains some soye chunks with diced vegetables in some dressings from a QSR. We quite often order from this restaurant and are quite happy with their products and services. However, this time the salad they delivered had only veggies; no soye chunks and no dressing.

So I called them back to tell that they have sent the salad without soya chunks and dressing and if they could replace the same. The boy at the reception said “Please give me your number and my boss will call you back”.

I was feeling really hungry as I didn’t eat breakfast in the morning (rather just had a toast), so in 15 min I gave them a call again which went unanswered. By now the loyalty for the restaurant and likeness for its products had evaporated. So I called again in 10 minutes to tell them to take their salad back and return the money. This time the associate was kind enough to ask if I would like to get the salad replaced, I said no you please take your salad back. Fifteen minutes latter a delivery boy came to return the money and I returned the salad.

Now let’s analyze the action and reaction of both retailer and customer to go to the root cause of the issue. The product delivered was wrong; however because of the previous good repute of the retailer the customer didn’t mind the mistake and called the retailer to replace the product. The associate at the reception took the phone number of the customer and said that store manager will return the call. Clearly, the service provider was not empowered to take the decision. By the time he was able to figure out that the salad needs to be replaced, 25 minutes had passed by and the customer had lost the patience. However, there were no apologies made by the retailer which is again because of the lack of the redress guidelines or lack of training for the same!

While SOPs are important to minimize the gaps in the service delivery, Redress mechanisms are essential to get things right in case a gap arises in service delivery. Complaint and redress mechanisms require empowering the employees who serve the customers. This enables them to take instant decision as and when the need be.

So while developing or reviewing the SOPs, it is important for retailers to ensure that complaint and redress mechanisms are not only weaved in the SOPs but also provide sufficient empowerment to service providers.

admin

January 7, 2010

By Tarang Gautam Saxena, Chandni Jain and Neha Singhal

In Retrospect

While India was a promising market to many international brands, it was not completely immune from the global economic flu. More than its primary impact on the economy, the global downturn sobered the mood in the consumer market. Even the core target group for international brands, that had just begun to splurge apparently without guilt, tightened their purse strings and either down-traded or postponed their purchases.

In 2008 in the midst of economic downturn, skepticism and uncertainty, the international fashion brands had continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008 targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many players ended up discounting the goods heavily to promote sales while a few also gave up and closed shop.

As the Third Eyesight team had foreseen last year, 2009 saw a further slowdown and fewer international brands being launched during the year. The brands that were launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack and Timberland. Some of these had already been in the pipeline for quite some time and invested a considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

International Fashion Brands in India

After many deliberations, the well-known global brand Donna Karan New York set foot in the Indian market in 2009 through an agreement with DLF Brands to set up exclusive DKNY and DKNY Jeans stores India. The brand is also reported to have signed a worldwide licensing agreement with S Kumars Nationwide Ltd to design, manufacture and retail DKNY menswear in certain specific countries.

Second Chances

Amongst the international brands that have recently entered the Indian market, a few are on their second or even third attempt at the market.

For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills, and the partnership intended opening 15 stores by 2010. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis on retailing international brands within the country. Within a few months of the ending of this relationship, Diesel signed a joint venture with Reliance Brands for a launch scheduled for 2010. Both partners seem to be strategically aligned with a common goal as the international iconic denim brand wants to take on the Indian market full throttle and the Indian counterpart has indicated that it wants to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008, despite plans to open more than 50 stores in the first three years of operations. Miss Sixty has finally entered India through a franchise agreement with a manufacturer of women’s footwear and accessories. The company has currently introduced only shoes and accessories category and is looking at potential partners for its label Energie and girls’ range Killah.

Other brands that have re-entered the Indian market include Germany-based Lerros whose first presence in India was back in mid-1990s. The brand re-entered the market in 2008 through own brand stores and is growing its presence through this route as well as through multi-brand stores.

Oshkosh B’gosh is another brand that had entered India in mid 1990s, through a licensing agreement with Delhi based buying house, Elanco. The licensee found the childrenswear market hard to crack, and closed down. In 2008, Oshkosh re-entered the Indian market through a licensing partnership with Planet Retail and is now available through shop-in-shop counters at Debenhams stores. Reports suggest that it may consider setting up exclusive brand outlets.

During the turbulence of 2008 and 2009, a few brands also exited the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both) to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations and for the amount of effort and money being invested, and that it was better to pull the plug.

Some brands that have been pulled out of the Indian market during 2008 and 2009 include Dockers, Gas, Springfield and VNC (Vincci). Gas (Grotto SpA) is reported to remain interested in the market but has not found another partner after its deal with Raymond fell through in 2007 and all dozen of its standalone stores were shut down.

The Scottish brand Pringle and its Indian licensee did not renew their agreement upon its expiry. The Indian partner has reportedly signed an agreement to launch another international brand in India, while Pringle is said to be looking for new licensee.

The good news is that successful relationships outnumber every exit or break in relationship possibly by a factor of ten. Some of the brands that have sustained are among the early entrants having a presence in India since the late-1980s and 1990s or even earlier. These include Bata, Benetton, adidas, Reebok (now also owned by adidas), Levi Strauss and Pepe. Having grown very aggressively during 2006 and 2007 Reebok quickly became the largest apparel and footwear brand in India, while Benetton and Levi’s are expected to cross the $100-million mark for sales this year.

Entry Strategy & Recent Shifts

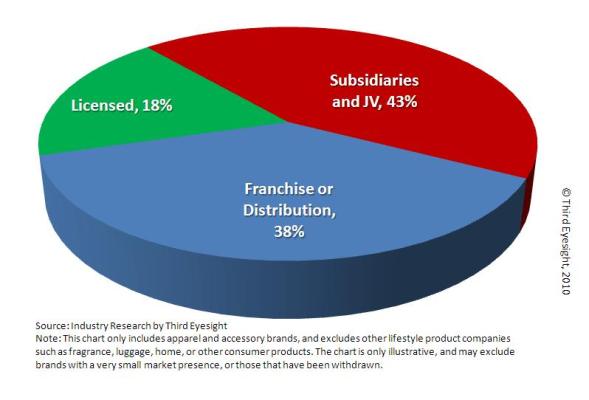

As envisaged in Third Eyesight’s report from a year ago, with changing market conditions and a growing confidence in the Indian market, there has been a shift among international brands in the choice of the launch vehicle. While franchising has been the preferred mode of market entry in the recent past for risk-averse brands, more brands today demonstrate a long-term commitment to the Indian market, and are choosing to exercise ownership through wholly or partially owned subsidiaries and through joint ventures.

In 2009, we have seen a noticeable shift in favour of joint-ventures as the choice for entry into the market. Even the brands already present are looking to modify the nature of their existing presence in India in order to exert more control over the retail operations, products, supply chain and marketing.

Current Operating Structure

(End 2009)

Brands that changed their operating structures and, in some cases partners, in recent years include VF (Wrangler, Lee etc.), Lee Cooper, Lee, and Louis Vuitton amongst others.

Mothercare, the baby product retailer, which is present through a franchise agreement with Shopper’s Stop has, in addition, recently formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores. Gucci, which had initially entered in 2006 with the Murjani Group as a franchisee, has recently changed over to Luxury Goods Retail, and is now in the process of restructuring the relationship into a joint venture.

VF has also been reported to be looking to license Nautica, Jansport and Kipling to a new partner. Until now, these brands were handled through the joint venture with Arvind Brands. Arvind has increasingly focused on its core business, closed stores and scaled down expansion plans for the international brands.

Burberry that had entered India in 2006 through a franchisee arrangement with Media Star opened two stores under this arrangement. It has now set up a new joint venture with Genesis Colors and plans to open 20 stores across the country.

More recently Esprit has also been reported to have approached Aditya Birla Nuvo to deepen its engagement by moving from its distribution arrangement into joint venture as the international brand sees excellent potential in the Indian market.

Buckling up for 2010

Throughout 2009, the one fact that became clear was that the Indian market was resilient. Now, as the global economic condition stabilizes, confidence levels of brands and retailers in India have also improved.

Several launches are already expected in 2010, and possibly many more are being worked upon. In the following 12 months, consumers can expect to find within India acclaimed brands such as Diesel, Topman, Topshop and the much-anticipated Zara. Many more Italian, British and French brands are examining the market.

Most of the international fashion brands already present in the market are also projecting a cautiously upbeat outlook in their plans, while a few are looking positively bullish.

For example, Pepe, an old player in premium and casual wear segment, has reported plans to grow its retail network further and open 50 more franchise stores by September 2010. Similarly the German fashion brand S. Oliver that entered the Indian market in 2007 is looking to grow significantly. It has already moved from a franchise arrangement with Orientcraft to a joint-venture with the same partner, and has stepped up its above-the-line marketing presence. The brand has recently reported its plans to scale up its retail presence to 77 stores by the end of 2012 while also strengthening its presence through shop-in-shop in multi-branded outlets in high potential markets.

Those international brands that have tasted success have not achieved it by blindly importing business models and formulas from other markets. Most have had to devise a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched. These include The Body Shop which decreased its prices by up to 30% this year, and Marks & Spencer which reduced prices by 20-40%. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

On the operational side, the good news for retailers and brands is that the average real estate costs have reduced significantly, although marquee locations remain high. In several locations lease models have also moved from only fixed rent to some form of revenue sharing arrangement with the landlord. And, while the sector has seen some employee turmoil as many non-retail executives who came into the business in the last 5-7 years have returned to other sectors, employee salary expectations are also more realistic.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s recent work with international brands’ business units in India highlights the international players’ concern with ensuring a consistent brand message, improved organizational capabilities right down to front-line staff, and focus on unit productivity (per store and per employee).

We may yet see a few more exits, and possibly some more relationships being reshuffled and partners being changed. However, all things considered, we can look forward to a net increase in the number of international brands in the country.

The Indian consumer is certainly demonstrating more optimism and as far as there are no major unforeseen global or domestic shocks, this optimism should translate into a healthier business outlook for international brands as well. According to early signs, 2010 could be an excellent curtain-raiser for a new decade of growth for international fashion brands in India.

[The 2009 report is available here: “International Fashion Brands – India Entry Strategies”]

(c) 2010, Third Eyesight

[Note: This report is based on information collected from a combination of public as well as proprietary sources, and in some cases may differ from press reports. However, no confidential information has been shared in this report.]

Devangshu Dutta

January 5, 2010

If we were to look at phrases that have cropped up during the recent recessionary times in the consumer goods sector, “private label” has to be among those at the top of the list.

From clothing to cereals, toothpaste to televisions, there is hardly a category that has not seen retailers trying their hand at creating own labelled products.

The first motivation for most retailers to move into private label is margin. On first analysis, it appears that the branded suppliers are making tons of extra money by being out there in front of the consumer with a specific named product. The retailer finds that creating an alternative product under its own label allows it to capture extra gross margin. Typically the product category picked at the earliest stage of private label development would be one for which several generic or commodity suppliers are available.

At this early stage, the retailer is aiming for a relatively predictable, stable-demand and easily available product whose sales would be driven by the footfall that is already attracted into the store. A powerful bait to attract the customer is the visible reduction in price, as compared to a similar branded product. If the product can be compared like-for-like, customers would certainly convert to private label over time.

However, maintaining prices lower than brands can also be counter-productive. In many products, while customers might not be able to discern any qualitative difference, they may suspect that they are not getting a product comparable to one from a national or international brand. And while private label can drive off-take, the price differential can also erode gross margin which was the reason that the retailer may have got into private label in the first place. Over time, such a strategy can prove difficult to sustain, as costs of developing, sourcing and managing private label products move up.

The other strong reason a retailer chooses to have private label is to create a product offering that is differentiated from competitors who also offer brands that are similar or identical to the ones offered by the retailer. Department stores, supermarkets and hypermarkets around the world have all tried this approach – some have been more successful than others. The idea is to provide a customer strong reasons to visit their particular store, rather than any of the comparable competitors.

Of course, when differentiation is the operating factor, the products need more insight and development, and closer handling by the retailer at all stages. A price-driven private label line may be sourced from generic suppliers, but that approach isn’t good enough for a line driven by a differentiation strategy. In this case, costs of product development and management increase for the retailer. However, to compensate, the discount from a comparable national brand is not as high as generic nascent private label. In fact, some retailers have taken their private label to compete head on with national brands – they treat their private labels as respectfully as a national branded supplier would treat its brand.

So what does it take to go from a “copycat” to being a real brand?

Third Eyesight has evolved a Private Label Maturity Model (see the accompanying graphic) that can help retailers think through their approach to private label, whether their product offering is dominated by private label, or whether they have only just begun considering the possibility of including private label in their product range. The model sketches out a maturity path on five parameters that are affected by or influence the strength of a retailer’s private label offering:

In some cases, retailers may have multiple labels, some of which may be quite nascent while others might be highly evolved, clear and comparable to a national brand. This could be by default, because the labels have been launched at different times and have had more or less time to evolve. However, this can also be used as a conscious strategy to target various segments and competitive brands differently, depending on the strength of the competition and their relationship with the consumer.

The interesting thing is that size and scale do not offer any specific advantage to becoming a more sophisticated private label player. Some extremely large retailers continue to follow a discounted-price “me-too” private label strategy where even the packaging and colours of the product are copied from national brands, while much smaller players demonstrate capabilities to understand their specific consumers’ needs to design, source and promote proprietary products that compare with the best brands in the market.

For a moment, let’s also look at private labels from the suppliers’ point of view. As far as we can see, private label seems to be here to stay and grow. Suppliers can treat private labels as a threat, and figure out how to ensure that they retain a certain visibility and relationship with the consumer. On the other hand, interestingly, some suppliers are also looking at private label as an opportunity. They see the growth of private label as inevitable, and would much rather collaborate in the retailer’s private label development efforts. This way they can maintain some kind of influence on the product development, possibly avoid direct head-on conflict with their own star branded products and, if everything else fails, at least grab a share of the market that would have otherwise gone over to generic suppliers.

If you are retailer, I would suggest using the Private Label Maturity Model to clarify where you want to position yourself, and continue to use it as a guide as you develop and deliver your private label offering.

If you are a supplier concerned about private label, my suggestion would be to gauge how developed your customer is and is likely to become, and ensure that you are at least in step, if not a step ahead.

Of course, if you need support, we’ll only be too happy to help! (Contact Third Eyesight to discuss your private label needs.)