admin

September 22, 2008

The Textile and apparel industry is of particular importance to India. It not only provides employment to a broad base of semi-skilled and unskilled labour but also helps to extend the economic bounty to urban and semi urban areas. Though India has a history of thousands of years in global trading of textile, it contributes only 3% to the global exports of textile and clothing.

While the urge to grow exists, there is a huge difference between the current exports of about Rs. 864 billion (US$ 20 billion) and the target of Rs. 2,500 billion (US$ 55 billion) by 2012. To achieve this vision, exports must grow at around 25-35 per cent a year for the next 4 years, depending on how weak or stable the current year is. This growth rate seems difficult considering the fact India has actually grown its exports of textiles and apparel at an annualized growth of a little over 14 per cent from 2003-04 to 2007-08.

Even if the industry looks at increasing the volume of exports to achieve the vision, the ports do not have the handling capacity considering that they currently operate at 91 to 92 % of available capacity.

Hence, incremental thinking will not help to achieve the vision.

Our key concern is the value “lost” by the industry. Being the low cost supplier does not necessarily translate into greater market share. The Indian Industry must look at enhancing the value delivered rather than competing on the cost platform. Indeed, India compares poorly to other countries on the value captured per employee. (For instance, if the export value captured per employee in India was as much as Turkey, India’s exports would be close to China’s exports of US$ 161 billion.)

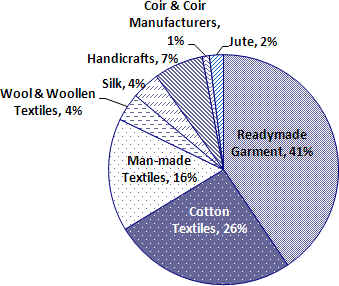

One major concern that needs to be addressed is that India’s exports are still weighted in favour of raw materials and intermediate products, rather than finished products. Apparel exports account for only 41% of India’s textile exports in 2007-08. India’s product mix also needs to be aligned to global market needs, rather than only focussing on “traditional strengths” – this includes enhancing the share of non-cotton products in the basket.

Another area that is neglected is the inherent competitive capability of developing new products. The industry needs to develop and nurture these skill sets to create a sustained competitive advantage in the global scenario. India already provides buyers with value in terms of product development and design, which needs focus and further strengthening.

Further, India’s domestic industry, and its skill at understanding market needs, creating and merchandising product, can also play a valuable role in the industry’s growth.

The competitive advantage offered by being able to influence the development of a product is immense. And given that sourcing lead times are shorter in unpredictable times, a supply base that has been involved with the buyer right from the development stage of the product is most likely to get the final order. Third Eyesight proposes a four dimensional model: Define, Design, Develop and Deliver so as to achieve the industry-wide development, of projecting India as a valuable supplier, and sustaining its value needs.

By creating an ecosystem focused on design and product development, India can create and capture the billions of dollars worth of value that is being lost to other countries.

This is an extract from Third Eyesight’s report presented at the FICCI 3rd Annual Textile And Garment conference in Mumbai. The report was released by the Minister of Textiles, Government of India. To download the full report prepared by Third Eyesight, please click here.

To discuss how we can help you with your specific business needs, please get in touch with us via email (please send it to services [at] thirdeyesight [dot] in) or via this form: CONNECT.

admin

September 22, 2008

Devangshu Dutta

In a departure from popular retail philosophy, Devangshu Dutta calls for a new model of food supply based on multiplicity and diversity. Modern retail must, he says, take into account the changing environment and be sensitive to evolving consumer preferences and to the failures and obsolescence of traditional mass retail models adopted by western developed markets.

Devangshu Dutta is chief executive of Third Eyesight, a management consulting firm focused on consumer products and retail, whose clients include brand leaders and some of the largest companies in their respective markets.

Food price inflation it is still hogging the headlines. It is, after all, an emotive topic. We are terribly concerned not just as food and grocery professionals, but also as consumers and the general public. After all, food and grocery typically account for half of our monthly spend, give or take a few percentage points.

Most students of management, economics, and human behaviour are aware of Abraham Maslow’s classification of human needs into a hierarchy construct. Other economists and psychologists prefer to use other models. Whichever model you consider, the need to eat and the need for security are invariably at the bottom or base level which must be fulfilled the earliest.

The interesting fact is that well after you would imagine these basic concerns have been taken care of, they are actually never far from the surface. This is true not just of the poorest of the poor, but of the wealthy and the well-off as well—whether individuals, communities, or nations.

Increasingly, the agricultural supply chain is dependent on non-renewable petroleum and its products, rather than by the natural energy of the sun being converted into food by the plants.

Is it any wonder that “food security”—the combination of these two—is such a charged subject, especially in these times?

However, a significant set of questions is not really touched in the question of costs and in the question about the continuing security of food supplies: how the food supply chain is structured, how it is driving consumption, what impact that might have on food prices and several broader cost implications.

INDUSTRIALISING AGRICULTURE—FARMING PETROLEUM

Thousands of years ago, when hunter-gatherer human beings stumbled upon agriculture, it was a breakthrough similar to the discovery of controlled fire. Hunter-gatherers were dependent on the natural availability of food, while agriculture created the opportunity to have some control over food supplies and reduce the natural feast-famine cycle. Thereafter, farming, processing and storage techniques kept evolving incrementally to ensure that more food could be produced for each unit of land and effort, and stored for longer – all moving towards ensuring “food security”. This led to the age of empire-building, where monarchs grew their wealth (essentially food territory) with the help of military- imperial complexes, and the greater wealth in turn supported the military-imperial complex.

This remained the trend for a few thousand years, until the age of industrialisation and the age of petroleum. Through the industrialisation and the world wars, the military- imperial complex gave way to a military-industrial complex, which essentially became the military-industrial-petroleum- agricultural complex. Suddenly, there were not just machines to plant, reap, thresh, sort, clean and process, but also petroleum-based and synthetic substances to dramatically increase output and to keep the produce fresher for longer.

As farms industrialised, the parameters that began to be applied were the same as in any factory—how to produce more while spending less—and every year the target was to grow more for less. Underlying this was the principle of “efficiency from larger scale”. The same philosophy played out further down in the supply chain – from processing aimed at extending the shelf-life of the product as it was (chilling, cleaning, sorting) to processing and packing in order to change the nature of the product itself and gain additional value (such as turning tomatoes into puree and potatoes into chips).

Standardisation became a vital link in industrialisation — if you can standardise produce, you can cut down human handling — while you may lose product variety (including flavour and colour) you gain through lower production costs. By reducing unpredictability, you can also concentrate on building the scale of business, because it becomes more repetitive.

The interesting side-effect of this is that, gradually, we are converting ourselves (and people in many industrialised economies already have) into petroleum-burning machines rather than those running on solar energy, because increasingly, the agricultural supply chain is dependent on non-renewable petroleum and its products, rather than by the natural energy of the sun being converted into food by the plants.

The important thing to keep in mind is that, in this switch- over, energy efficiency is actually going down rather than up

Energy efficiency is actually going down rather than up – we are using more calories of fuel source to produce each calorie of food energy.

—we are using more calories of fuel source to produce each calorie of food energy.

So it is worth asking the question: can lower costs actually be costing us more?

THE DEMAND-SIDE STORY

The growth of industrial agriculture has not happened alone, but has been accompanied by the growth of modern or “organised” retail.

On the one hand, large retailers such as Wal-Mart, Carrefour, Tesco, Metro and others, have been widely credited for achieving cost-efficiencies from scale, and then passing on these efficiencies to the consumer in the form of lower prices (and, apparently, higher standards of living). That is a good thing and definitely of benefit to the population at large, especially in inflationary times such as these. Surely, it is good to push for lower costs rather than keeping prices high as a result of inefficient sourcing, wasteful and expensive handling, and non-value-adding costs in the supply chain.

On the other hand, these organisations are driven to standardise their own product offerings, reduce the number of supplier touch-points and increase the volume per supply source.

There is not just a reduction in diversity of suppliers, but also a reduction in the number of product variants. (I’m not referring to the number of “types” of potato chips or packaged meals, but to the actual core food product—the natural species or sub-species that are the basic source.) Of course, agriculture itself is a process of consciously selecting and encouraging species that are more useful to us humans, but industrial

Lower costs can be delivered by reducing the variation of products

Higher sales can come from either having consumers buy more of the same product (which in food does tend to taper off after a while), or by turning the basic product into a “value-added” product (e.g. potatoes into wafers, mash, fries; corn into syrup and food additives, and so on).

THE NEED FOR A DIFFERENT MODEL

We don’t have to look too far into the future to realise that this is not a sustainable model. (Or, as someone pithily said: “Only fools and economists believe in infinitely compounding growth.”) So far, this model has impacted less than a fifth of the world’s human population, but now the growth markets of choice for industrial agriculture companies are China and India. If these two countries move through the exactly same path as have the western economies in terms of agriculture and food processing, given the population base itself the impact may be 5-7 times (or more) on the demand for petroleum as well as the fall-out on the ecosystem.

You may ask: why should retailers and their suppliers worry about this?

Firstly, pure cost considerations – clearly, the costs of petroleum are ranging at the highest levels ever, and explosive demand through industrialised agriculture will only serve to push them up. How far can you push the food bill every month, before people start buying less? What impact would that have on large retail supply chains and farmers whose processes are increasingly built around products of industrial agriculture?

Secondly, what consumers are already beginning to express in western markets will possibly happen in India in the next few years as well: concern about where and how the product has been produced, what has been the fall-out on the environment and on the overall health of people involved with that supply chain as well as the health of consumers. Carbon footprint, food miles and locavores (people who only consume food that is produced within 100 miles of where they live) are terms that companies are increasingly becoming familiar with.

agriculture takes it to a completely different level. Carbon footprint, food miles

The industrial-agricultural-retail economic model can be paraphrased as follows:

Businesses (especially those that are publicly held) need to show growth in profits each year

Growth in profits can come from higher sales at the same cost base or lower costs

Carbon footprint, food miles and locavores (people who only consume food that is produced within 100 miles of where they live) are terms that companies are increasingly becoming familiar with

And an alternative set of questions is also being raised. Is it ok to burn non-sustainable fossil fuel if you get “carbon credits” by planting trees somewhere else—have all the carbon costs been accounted for from the start to the finish of the production process? Is it better to reduce the food miles and have food produced locally in a high-cost economy’s industrial agricultural model, or to have naturally grown foods from a more primitive farm in Africa or Asia where the environmental impact is only the “carbon debit” of the air-freight. And, even if the produce is carbon-friendly, what about the nitrogen footprint (from the fixation of nitrogen into fertilisers) and the methane footprint (from large scale animal farming)?

THE POWER OF THE SMALL AND THE MANY

And finally the question of maintaining diversity must be top- of-mind. For all its so-called inefficiency, diversity is actually a great shock-absorber. Imagine a bean bag or a piece of foam — what gives them their cushioning ability is the space and air between the little balls, or the material. Now imagine a cropland that is attacked by a pest—if there is diversity in the plant population, there is a good chance that certain varieties will survive even if others don’t; unlike a cropland with limited variety which may be totally wiped out (and possibly the farmer with it). Further imagine a supply chain that has multiple suppliers with the same or similar product versus one where the supply base is highly concentrated. Which ecosystem do you think will survive better during times of trouble, even if some of the suppliers—a part of the ecosystem—do not? (One doesn’t have to think too far: the example of the former Soviet Union with its mega manufacturing plants supplying the whole country are a case in point.)

To really find long-term solutions for food security issues, retailers, suppliers, economists and governments need to acknowledge that sustainable safety lies in numbers and diversity. A dispersed economic system with a lot of variety has resilience built in. And the solutions may actually be very close at hand, in the updating of traditional techniques.

It is high time to start figuring out how India (and China) can take the lead in creating an alternative and more sustainable model for food security for large populations, rather than blindly push development models borrowed from the 19th and 20th century western economic history.

Source: FLY ON THE WALL

Send download link to:

admin

September 22, 2008

About Third Eyesight

Third Eyesight is a consulting and management solutions firm focussed on retail and consumer products. Third Eyesight’s professionals have deep and extensive experience in the lifestyle merchandise sectors (such as textiles, apparel, accessories, home, footwear and other products).

Clients that have benefited from Third Eyesight’s experience and expertise include Indian and international retailers, brands and manufacturers, private equity & venture investors, suppliers to the retail sector, as well as government agencies and industry bodies. Third Eyesight has worked with companies that are market leaders (with annual sales of over US$ 80 billion) as well as early-stage and start-up businesses.

Strategy and operational support provided by Third Eyesight for retail and consumer products sectors includes: opportunity scanning, evaluating new business areas, market and industry research, business strategy and business plan development, development of sales and distribution networks, including support with acquiring key client relationships, business due diligence, partner evaluation, strategic alliances, mergers & acquisitions, sourcing and supply chain strategy, merchandising support, operational audits & assessment, training and skill-development, and a variety of other operational support.

Third Eyesight

Tel: +91 (124) 4293478

Website: www.thirdeyesight.in

About FICCI

Set up in 1927, FICCI is the largest and oldest apex business organization of Indian business. Its history is very closely interwoven with the freedom movement. FICCI inspired economic nationalism as a political tool to fight against discriminatory economic policies. FICCI’s commitment is now directed at changing the economic landscape of India, through reforms that expand the space for private sector and public private partnerships. FICCI is the rallying point for free enterprises in India. It has empowered Indian businesses, in the changing times, to shore up their competitiveness and enhance their global reach.

With a nationwide membership of over 1,500 corporates and over 500 chambers of commerce and business associations, FICCI espouses the shared vision of Indian businesses and speaks directly and indirectly for over 2,50,000 business units. It has an expanding direct membership of enterprises drawn from large, medium, small and tiny segments of manufacturing, distributive trade and services. FICCI maintains the lead as the proactive business solution provider through research, interactions at the highest political level and global networking.

In the knowledge-driven globalised economy, FICCI stands for quality, competitiveness, transparency, accountability and business-government-civil society partnership to spread ethics-based business practices and to enhance the quality of life of the common people.

Myth–Busting as an Introduction: Let’s Not Rebottle Old Wine There are many myths that are prevalent among the observers of the Indian textile and apparel industry. Here are a few illustrative ones that point to the need to seriously review of the way the Indian industry competes globally:

Myth # 1 – To grow, India needs to do what China has done:

Comparisons between the two countries are bound to happen, and surely there are some areas for India to learn from China. However, the fact is that India does not have many of the advantages that China had in the past (including a huge business portal in the shape of Hong Kong), nor can it so quickly build the advantages that China has developed over the last 15 years in terms of production capacity, infrastructure etc. India’s political and administrative structure, financial systems, and internal dynamics are completely different. Some obvious internal gaps need to be filled in India’s case, but sustainable competitiveness cannot be built through a copy-China strategy.

Myth # 2 – India is competitive because Indian labour is cheap:

India has low salaries and wages. But studies show that most Indian clothing factories are less productive, possibly even only half as productive as factories in India’s major competitors on the global stage. Add to that inefficient factory management, expensive power, higher financial costs, and costs of bureaucracy and corruption. The true cost of business can be far higher for Indian businesses – and with the market determining the price boundaries for exporters, it’s no surprise that many of them are losing money.

Myth # 3 – Indian handiwork is irreplaceable:

When embroidery was automated, suppliers of embroidered goods from Delhi and its surrounding areas certainly felt the heat but they maintained a competitive edge due to embellished (sequinned / beaded) products that are a staple in the “value-added segment” and that flood the market whenever the “India-look” is in. However, in recent times, machinery manufacturers have developed equipment that can provide the same look. The only difference is that the beads and sequins are stuck on with adhesive rather than being stitched on. The buyer is not likely to care about the production method – after all, the quality and look produced on these machines is more consistent, and the garment is less expensive because the machines have a very high throughput.

Myth # 4 – Compared to China and other Asian giants, the fragmented supply base of Indian manufacturers is more flexible and can competitively fulfil small orders:

For long, the small-scale reservation created a situation where the size of the factory was determined by an investment ceiling rather than by business economics. This base of small factories, by default, fitted into a specific competitive niche, where buyers wanting to place small orders (say, less than 2,000-3,000 pieces in a style) would mostly come to India, as most other factories around the world worked with higher “minimum-order quantities”. However, with retailers switching to the new mantras of quick-response, efficient supply chains and reduced inventory exposure, manufacturers in other countries are now working on much smaller orders.

Myth # 5 – India needs to focus on its core strengths – for example, India has a sustainable advantage in cotton that will maintain its competitive edge:

One of India’s great strengths is one of its greatest weaknesses. Due to its suitability to India’s climate, cotton has naturally achieved a very high share of the Indian production base. However, the global market is skewed in favour of man-made fibres. Cotton accounts for just about a third of global apparel consumption (including blended fabrics where cotton is used along with other fibres). For India to remain a globally-significant player, Indian production and exports must be aligned to consumption patterns – that means a strong thrust in products made out of synthetic fibres, as well as natural fibres such as wool. Similarly, Indian manufacturers need to look at the product range that their customers wish to buy, and identify new areas into which they can enter.

Perspective: India

The textile and apparel industry is of particular importance to India. The sector directly and indirectly results in the largest employment next to agriculture and retailing activity in the country. Its presence is not confined to the urban centres of industry and commerce – the textile sector is the most deep-rooted industry in rural India as well, and has been historically so.

India is one of the world’s oldest major textile suppliers and once was, in fact, the largest by far, with a recorded history of global trading in textiles dating back several thousand years. We treat globalisation as a new phenomenon – the fact is that many thousands of years ago, the Egyptian civilization was trading with the Indus Valley civilization, the Chinese and the Romans had discovered each other way before US department store buyers landed in Hong Kong and Korea.

The textile sector in India started industrialising in the late-1800s and early-1900s, heralding a new era for growth. However, shortly after independence in 1947, the industry was constrained by licensing that limited mill capacity growth and other restrictions that forced companies to remain small-scale.

Later in 1962, just as India’s exports had begun to grow, quota-restrictions closed the gates to free trade, nipping India’s exports in the bud. For years, quotas determined where buyers could place orders, and trade was accordingly channelled and fragmented. Preferential trade arrangements placed further constraints, as both the US and the EU provided duty-free and quota-free access to some countries.

The net result is that India currently has just over 3 per cent of the global exports in textiles and clothing. However, despite its low share, India remains among the Top-10 exporters of textiles and clothing in the world.

After the removal of quotas in 2005, India was expected to grow its share of the global marketplace. However, views varied widely on whether India really had the mettle to stand-up to China – the largest exporter. Some observers and even people from within the industry expected India’s share to decline in global trade.

India has actually grown its exports of textiles and apparel from US$ 13.6 billion in 2003-04 to US$ 20.5 billion in 2007-08, an annualised growth of a little over 14 per cent. During a similar period, China has grown its exports from US$ 95 billion to US$ 161 billion, with an annualised growth rate of almost 20 per cent.

Given the current market share positions, it is unrealistic to expect India to catch up with China any time soon. However, the trend clearly is towards a re-integration of India’s industry with the global trade.

India’s Global Textile and Clothing Trade

Source: Government of India Trade Statistics, Third Eyesight Analysis

We also feel that past perceptions, and prejudices ignore the potential India offers as a sustainable and strategic supply base. Among the Top-5 low-labour-cost clothing suppliers

(China, Turkey, Mexico, India, Bangladesh), only China and India do not have preferential access to their major markets and yet compete very effectively on the basis of their inherent strengths.

The fact that India is one of the few countries in the world that offers:

A vertical industry structure, from fibre to clothing

A large and replenishable low-cost pool of labour

A multi-product capability

Product development skills

A large domestic market that can sustain the industry in the face of global competition

The last is an important and under-weighted factor in the Indian industry’s competitive strategy. Worldwide, countries that have strong sectors for textile, apparel and other lifestyle products, have very strong domestic markets and strong ‘brand delivery’ mechanisms. The focus, in these countries, is not just on production but the entire ecosystem for the industry. We believe that India should be no different.

So far, exporters and domestic-market focussed companies have had very little common ground to work on. As compared to the customers based in the western markets, the domestic market needed very small quantities per style, processes and systems were weak, with high responsiveness required from the supplier – for exporters it was an “unviable” market to step into. On the other hand, for domestic buyers, exporters were far too rigid in their processes, payment terms, minimum quantity requirements etc. That has started to change with the emergence and significant growth of modern retailing in India (the so-called “organised retailing”).

Although many people believe that modern retailing is a recent development in India, the fact is that the textiles and apparel sector has been at the forefront of its development since the 1950s-1960s, when the first chains started coming up. In about 30-years significant single-branded dealer-networks (now widely morphed into exclusive branded outlet chains and franchise networks) were built by textile and then apparel companies.

However, since the mid-1990s, there has been significant and visible development in the domestic market for textiles, apparel and other lifestyle products. Large retail chains have begun appearing, and new platforms have emerged for apparel and textile companies to grow their business domestically. The large Indian retailers’ requirements have more in common with western retailers and brands (the customers for India’s exporters) than ever before. This provides an opportunity for the two sectors to work more closely together.

Thus, with its long history, and these two growth engines – the export industry and the domestic market – we believe the Indian textile and apparel sector can retain its significant role in the country’s economy, and create a differentiated position among global trade that is sustainable into the future. However, as the global economic growth slows, the domestic economy follows and inflationary pressures push up the cost of doing business, fresh thinking is also needed to keep the sector in growth mode.

The other urgent driver is the vision of what India’s export numbers could potentially be by 2012: Rs. 2,200-2,500 billion. The number currently stands at a little over Rs. 864 billion, and to achieve the vision, exports must grow at around 25-35 per cent a year for the next 4 years, depending on how weak or stable the current year is.

India’s Textile and Apparel Exports (Rs. Billion)

Let’s not debate whether this vision is achievable or not. The purpose of a vision being articulated is to drive the actions that will help in achieving it.

What is very clear is that this vision is not “incremental” in nature, and incremental thinking will not help in realising it.

Even if we assume a robust incremental growth rate of 15 per cent per annum, India’s exports will only be able reach Rs. 1,500 billion by 2012.

If this vision is to become reality, if India’s textile and apparel industry is to change from being (as described by the head of an international company) “the eternal hope” to a true global leader, the industry and the institutions supporting it, including the government need to put in place a radically different course of actions.

This report is not being presented as a definitive strategy document for the Indian textile and apparel industry, or for the Government to mould its policies. However, it does attempt to present a view on historical and recent developments, the constraints that the industry cannot wish away and must, therefore, embrace, and also to highlight the factors that can create a sustainable competitive advantage for India as a leading global resource of textiles and apparel products.

A Health Check on the Indian Industry

While the All-India Index of Industrial Production registered an increase of 8.1 per cent during April-March 2007-08, as against the corresponding period of the previous year, the growth of textiles sector was slow.

Although Jute & other vegetable fibre textiles (excluding cotton) registered significant growth (33.1 per cent), the other textile sub-groups showed small growth rates. Wool, Silk & Man-made fibre textiles registered a growth of 4.2 per cent followed by Cotton Textiles (4.1 per cent) and Textile Products [including wearing apparels] (3.3 per cent) as against the corresponding period of previous year.

According to Ministry of Textiles, during fiscal 2007-08, spun yarn production increased by 4 per cent and cloth production increased by 3.9 per cent. The handloom sector recorded the highest growth (6.0 per cent) followed by the power loom sector (4.5 per cent).

The Indian textile industry is export-weighted, with almost 55 per cent of the total production being exported. The US market is the largest destination for Indian textile and apparel exports. The recessionary trend in the US and relentless ascent of the rupee led to a decline in the total trade with India in 2007, resulting in smaller orders, lower prices and deep uncertainty for apparel exporters.

Indian exporters are now trying to increase their share in EU market and diversify to other markets other than US. However, the market scenario in most major global markets is looking grim in the short term.

Though the dollar’s appreciation this year should have brought a breather to exporters, the benefits of a weaker rupee has been offset by the surge in costs and the global economic slowdown. India’ textile & clothing companies’ margins are under severe pressure due to rising cost of raw material, fuel, real estate and more expensive credit.

In addition, many of India’s competitors have recently enhanced their export incentives in the context of declining demand in the US and EU markets. For instance, China has increased VAT refund rates from 9 per cent to 13 per cent for synthetic textiles and from 11 per cent to 13 per cent in case of others. Pakistan has introduced Research & Development assistance of 6 per cent for garments.

Clearly, India’s exports are still too weighted in favour of raw materials and intermediate products, rather than finished products, and this is a major concern if one looks at the long-term competitiveness and value-capturing capability of the industry.

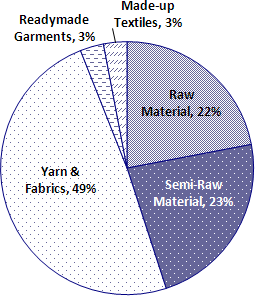

Imports have also begun to grow in India, although the numbers are still small. Import of fabrics and other products for conversion into clothing has been allowed duty-free for several years, and now imports are also growing for domestic consumption.

Imports up to April-February 2007-08, indicate an overall increase in both, rupee terms and in US$ terms, to 3.78 per cent and 16.71 per cent respectively. Imports of Readymade Garments (RMG), Made-ups and Raw Materials increased by 36.80 per cent; 28.93 per cent and 11.75 per cent respectively, in rupee terms, over the corresponding period of the previous year.

Send download link to:

admin

September 15, 2008

In the simplest terms, sourcing entails “buying a product”. So presumably, if you have the need for a product and know the cost at which you want to buy it, and you can find someone who can sell it to you, it should be a straightforward transaction. What happens in reality is often somewhat different.

The Sourcing Process

You start with a product in mind, with certain specifications. You build certain sales projections based on past performance, forecasts etc., you evaluate supply bases, select one or more suppliers, factor in a logistical plan to get the product from your supplier to your distribution centre or stores, manage the communications, often including information technology to control the 2-way flow of information, and finally hope to achieve the margins that you had planned for. That may well happen, but equally there is all possibility that it might not. On the supplier’s end, equally, the customer’s sales forecasts might not be achieved which might lead to reduced order quantities, the logistics provider might delay or even lose your entire shipment, causing claims, or even loss of a customer.So is a sourcing relationship a gamble?

“Sourcing” is made up of two elements, both of which contribute to the success or failure:Global Business Trends

Let us look at what the trends in global business are. One the retail side, three major trends are clearly visible: cross-border retailing is growing, retail consolidation is increasing, and retailers are opting for multiple formats to reach their customers. All of these changes are prompted by the objective of maximising the “consumer ownership” – either by accessing new consumers (in other countries or in a different market segment) or accessing the same consumer who might express different needs at different times. These three major trends are even becoming visible in the same retailer, for example:

Each trend places a different set of demands on the sourcing and supply strategies and structures. For example, cross-border moves create the need for multiple supply bases, due to differential production costs as well as import regulations, and also highlight the need to manage increasing logistical complexity. If a supplier is to keep pace with its major customers, it must be able to service them in multiple locations equally well.

Consolidation through mergers and acquisitions creates the opportunities for economies of scale, brings out the need for large, well-equipped suppliers, but also provides the opportunity for supplier rationalisation, which can be a threat to the business of suppliers who may not appear among the list of the “best” suppliers for the newly merged retail business.

Format migration creates different service needs for the same retail customer; for example, a high street retailer who normally has only marginal merchandise returns might face the need to handle as much as 15-30% returns on a new catalogue or internet business. Different formats, or different markets can also require product diversification due to different sizes, or different price-quality norms.

Global Trade Trends

On the other hand, on the trade side, there have been significant shifts in terms of trade agreements such as transitioning of the GATT to WTO, which promises lower import barriers (quotas, duties) and regional agreements such as NAFTA, which are collectively leading to encouraging trade across borders.

There is an increasing availability of new low cost supply

bases in close proximity to the major markets (such as Mexico

for North America, and Central Europe and North Africa for Western

Europe) where export growth is booming, creating serious competition

for the well-established trade routes such as Asia to North

America and Western Europe, or intra-EU trade.

| Table 1. Cross

Border Apparel Trade |

||

| 1997 Trade (billion US$) |

1990-97 Compounded Annual Growth Rate | |

| Traditional Global Flows | ||

| Intra-Western Europe | 44.2 | 2% |

| Asia to W. Europe | 19.4 | 5% |

| Asia to North America | 29.1 | 5% |

| Total | 92.7 | 3% |

| “New” Regional Flows | ||

| E. Europe and N. Africa to W. Europe | 7.7 | 22% |

| Intra-Asia | 21.5 | 14% |

| Mex. & Latin America to N. America | 11.3 | 22% |

| Total | 40.5 | 17% |

The trend towards cross-border trade is clearly visible, particularly in the US and EU, where imports have gained market share from domestic production. In the EU’s case domestic production, while still higher than imports in terms of share, has actually declined since 1990. USA sourcing shifts point towards a clearly dominant share of sourcing from within the Americas, and indicate a growth of a “Free Trade Area of the Americas” (FTAA) from the NAFTA concept. This would clearly serve the domestic industry’s competitive purposes as well, since production elsewhere in the Americas could be either owned or closely controlled by US manufacturers.

The EU, on the other hand, seems to be diversifying its supply base. While Eastern Europe and North Africa have come up quickly in the recent years, Asia maintains and is growing a dominant share, with many other bases expanding or appearing, such as the Indian subcontinent and new supply countries in South East Asia.

How Should You Respond?

So what should be your response in terms of future business strategy? First of all some fundamental shifts must be made in thinking about sourcing and supply.

If you are a buyer or a sourcing executive, understand that:A study done by the global consulting firm, Kurt Salmon Associates, calculated that for every new country that you move into, a trial order of 10,000 pieces would cost an additional US$ 42,500 in terms of supplier identification, development, product development, quality assurance etc. – that is over $4 a piece. Is every new opportunity worth that cost? Will you be able to gain adequate margins over significant volumes that will make the initial investment pay for itself? Will the new supply country be able to offer an extensive enough production base that go beyond the first products that you have looked at? And even, could the country actually become a market for you in the future (in which case it makes eminent sense to develop it as a supply base)?

To be most effective in the emerging scenario, look for sourcing platforms or “hubs”: countries and supply bases that not only are strong suppliers right now, but those that can serve as launch-pads to enter other countries. These platforms or hubs are typified by being located amidst many other potential supply bases, they possess intrinsic skills to develop product and manage production, and have access to a variety of raw material, both local and imported. Rather than making the buyer hop countries every time there is a problem or a new opportunity due to lower cost, the hubs allows the buyer to concentrate efforts in a region, develop that supply base consistently over a number of seasons or years, while leaving the low cost or new product opportunities open in other countries in the proximity.

Understand costs completely: these include not only the primary product cost, freight and import duties, but also financial costs (e.g. Letters of Credit, financial administration etc.), cost of quality assurance, remote business management costs etc. Further, the drivers need to go beyond primary cost, market access and quotas, and must take into account measures such as “realised margins”, responsiveness and match with customer proposition.

Low labour cost supply bases exist even close to the major markets now – so is Bucharest better or Bangalore? The answer lies in looking beyond costs alone. What capabilities do you possess within your organisation, and what do you want from your supply base? The more product development, supply management and service capability you can build within your own organisation, the greater the number of potential supply bases. Typically, with a highly developed sourcing organisation you would be able to tap into more low labour cost supply bases.

Three key areas define business focus: Price, Product and Service. Each demands a different approach to the customer, and therefore to sourcing and supply. A price-orientation focusses on efficiency, a product-orientation on innovation and product development, while a service-orientation focusses on reliability and responsiveness. You need to determine what combination of these factors determines your positioning in the competitive marketplace.

Also understand that traditional sourcing, based on seasonal patterns and long, variable lead-times are giving way to new methods. Companies increasingly need to classify their products as core products, seasonal products and fashion products. Core products tend to be basic staple items that provide large amounts of business over long periods of time – the focus in these clearly needs to be on planning, replenishment and efficient, cost-effective, consistent supply. Fashion products on the other hand have a very short selling window, and must be developed and brought to the market quickly – their value is in their newness and their being in the market at the right time – the focus here clearly must be on speed in product development and production.

Research indicates that major companies are indicating a shift in their sourcing from traditional seasonal patterns to replenishment-type of sourcing and “speed” sourcing. Have you analysed your own product range and adapted your sourcing accordingly? If you are a supplier you also need to understand these issues, and must adapt your business strategy suitably. Or else you run the risk of losing your business to a lower cost or more responsive competitor, who might either be next door, or half-way across the globe.

The key to survival in the new millennium clearly lies in:To do so, it is imperative to put in place all the building blocks: appropriate management structures, business performance measures, business processes, training and skill development, information technology and supply chain relationships. Ignoring any of these building blocks will only result in a shaky foundation for future business.

Devangshu Dutta

September 14, 2008

You’ve walked into your neighbourhood supermarket with your shopping list. The particular detergent that your spouse had put on the list isn’t on the shelf and the sales associate is not sure whether they have any in stock (maybe you get the standard line: “whatever we have in stock is already on the shelf”).

You’ve forgotten your mobile at home so you can’t call to check whether a substitute brand or different pack size will suffice, so you walk out with the item still on your list.

And into the local kirana store. The brand and pack size that you were looking for isn’t there either, but the shop-owner says that he will have it in stock sometime during the next 3-4 hours, and can send it over to your home. Or, he suggests, you could also buy an alternative brand (or pack size). At the end of that conversation you would have very likely bought the alternative offered, or would have agreed to home-delivery of the item you were seeking. (A study by the Institute of Grocery Distribution in the UK in 2006 discovered that, in case of non-availability, 40% of the customers end up buying the same product somewhere else.)

Some people would be cheering, “Yea, more power to the underdog small retailer”. But the point of this example is not the victory of the local, independent kirana over the chain-store. The point I am illustrating is that the difference in the business models and formats of these two competitors, and the impact of on-shelf availability.

Modern convenience stores and supermarkets, and the format that is being largely adopted by the chain-stores in India, is the western model of self-service. Compared to the kirana-model of “being served”, modern retailers depend on product being available and visible on the shelf. Very clearly, visibility and availability drive sales.

And in the current environment, retailers are or should be looking at squeezing more sales out of their existing stores (see the earlier column – “Priority #1: Same Store Growth”).

On-Shelf Availability is driven by a number of factors – some are within the retailer’s control, while others are not.

On the vendor side, availability is driven by a number of factors. In India, vendors themselves can be small to mid-sized companies, with distribution systems that are poor in terms of information linkages. The supply chain may comprise of several levels of stockists, distributors, and wholesalers, with an inherent and in-built delay in information exchange. In this situation there is always a phase difference between demand (non-availability) and supply.

Other than the phase-difference, the order-fill rates at the vendor’s end can also be poor due to supply constraints. The quantity available in stock for a certain product at a regional or state level can frequently be lower than the requirement, and in such cases the manager, or the distributor, can end up allocating the available stocks.

These causes can lead to availability that is as low as 60-65% on average, even among the popular products. “Good” vendors can have supply rates of 85-90%, but even in these there is a high variance.

However, the interesting thing is that a very high proportion of stock-outs (around 75% according to the 2006 IGD study) can be attributed to problems within the individual store. These include poor in-store disciplines, lack of awareness of the impact of low availability, too much work for the sales associates or the lack of motivation.

(For instance, 35% of sales executives in British study did not plan to pursue retail selling as a long-term career. In a study carried out by Third Eyesight a few months ago, with retail was being seen as a “growth industry”, that figure in India was about 55% and was closely correlated with the frontline attrition rates being witnessed by Indian retailers.)

One of the critical factors in how on-shelf availability is handled is the very different perception various people have of its importance. The store manager or a sales executive may directly correlate lack of availability with lost sales (and lost incentives), while a category merchant may not find it as critical since he or she may be able to balance the margins through the mix of product and the aggregation of sales across stores. The first critical element to be fixed is to have a common view on the importance of availability communicated across the retail organisation.

The second important element is highlighting the visibility of stock within the store – isn’t it surprising that despite the small size of back-office space, how stock that is showing “on the system” can be so invisible?! The product may be stacked in inaccessible boxes, or may have just been kept in the wrong location.

On busy days and during busy hours, merchandise can arrive at the store and simply “disappear” off the radar for a few hours, since the staff may not have had the time to take the stock into the store’s inventory. It sits in the shipping boxes waiting for stock intake, which may well happen after the peak selling hours have passed.

Sometimes the availability issue comes up because the product is very popular, and it becomes virtually impossible to maintain a high availability during the critical selling windows – a typical example may be health and beauty products or popular snacks, where the aggregate availability may be high during the week, but abysmally low during the peaks. A key feature of these categories is also the large number of SKUs, which can be cause for substitutions in the supply chain, and therefore poor availability of a particular SKU.

On the other hand, fresh produce and dairy may show poor availability if daily reports are configured for end-of-day rather than beginning-of-day stock-checks, since fresh vegetables, fruit, fish and dairy may actually be taken into the store during the early hours in the morning.

Many people believe that the best way to tackle these issues is through information technology.

However, IT is only a tool that can enable a business if the processes are robust and people are attuned to a common objective.

The correct sequence, as for many other aspects of business, is to tackle the people issue first. Awareness and common understand can only happen through consistent communication and widespread training. (The 2007 study by IGD (UK) on this issue highlighted the fact that 61% of the sales associates had not received any formal training, while 23% had no communication about on-shelf availability.)

This communication needs to be not just within the organisation, but across the retailer and vendor relationship. This process is, unfortunately, not enabled by the very tactical and adversarial nature of the buyer-supplier relationship. Retail buyers don’t easily share point-of-sale information with vendors due to a variety of real and perceived barriers – confidentiality, power-issues, competitive pressures.

Fortunately, although it is still early days, chain-stores and vendors in India are already beginning to work together. Very often the exercise is actually being led by the larger, multi-national vendors who have been exposed to the concepts of Efficient Consumer Response (ECR) and Collaborative Planning, Forecasting & Replenishment (CPFR) – concepts that have been around for about 15 years.

However, these frameworks require a significant amount of joint business planning as well as point-of-sale visibility being provided to the vendor, and both of those aspects are still weak in the Indian modern retail ecosystem. Such degree of high transparency will only come in with further maturation of the retail businesses and the vendor relationships. Some of the modern retailers are already able to see consistent availability of over 90% through these efforts, and as word spreads, hopefully so will the practice.

Creating a culture of transparency and communicating the desired levels of availability is the foundation on which robust processes can be built for checking and reporting availability, which then can be enabled through technology. The correct sequence, therefore, is People-Process-Technology, and not the other way round.

In closing, let me show the other side of the coin (after all, this column is titled “Devil’s Advocate”!). The additional sales from better availability are very seductive, and can be very profitable, but up to a point. After a certain level, the law of diminishing returns takes over as the cost of maintaining high availability exceeds the additional margin. Particularly in perishables the possibility of product expiry and spoilage is quite high. Of course, during festive occasions there may be no option but to ensure high availability of perishables such as gift packs of snacks and packaged foods, even at the risk of spoilage or expiry.

Having said that, on the whole, modern retailers in India and their vendors do need to focus on on-shelf availability as a key area for increasing the productivity of the existing stores. For many stores, there is significant room an increase in sales. With real estate and operating overheads remaining high, every extra rupee of sales squeezed out of the current square footage will contribute directly to the bottom-line, a fact that Indian retailers cannot ignore today.